Fortnightly Publication Highlighting Latest Insights From IRF Providers

Company Research

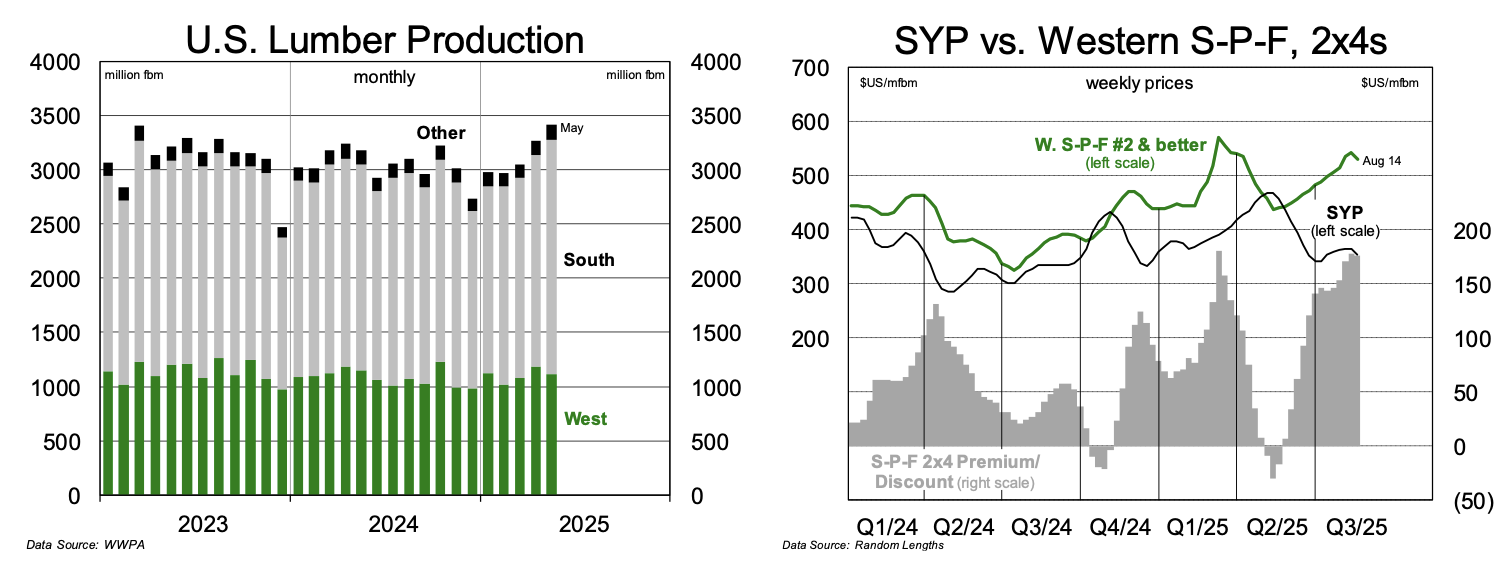

Lumber: Falling demand, rising production

Total US lumber production has risen steadily this year, reaching a higher level in May than any point in 2024 (left chart). All the production was in the South (US). The steady increase comes even as US single family housing starts declined 6% through May, with Southern starts down 10%. It is hard to say who wins from a weak US housing and lumber market, and with lumber demand expected to remain subdued until year-end and throughout 2026, SYP mill capacity reductions will be needed before a sustained lift in SYP prices occurs. Sawmills in the US West appear to be best positioned to benefit from declining Canadian S-P-F supply as lumber buyers appear to view species like Douglas Fir and Hem Fir as closer substitutes for S-P-F. The sustained price increase in lumber will happen, but the mill closures in South US and Canada will be painful. For now, investors should wait.

Edition: 218

- 22 August, 2025

Communications

Douglas Arthur raises his Q4 adj. EPS estimate to $1.10 per share (+34% Y/Y). He anticipates significant profit upswings in both DTC and Content (Studios) to more than offset continued weakness at Linear, lower profits at Sports and softness in Parks. In addition, given no Hulu hit in non-controlling interests and expected lower International Parks profits, adj. EPS should benefit from a lower deduction from non-controlling interests. The stock price has broken its lengthy downtrend with Parks weakness largely baked in, while future hotel bookings suggest a turnaround, a few quarters out. Box office results have been very favourable and the slate is strong. DTC is doing fairly well and the upside profit contribution could be significant in FY25E and beyond.

Edition: 196

- 04 October, 2024

Industrials

AI-hype is aboard the TRI express with the shares recently hitting an all-time high. The stock sells at 23.5x 2025E EBITDA, 40x 2025E Earnings and 37x FCF. This is higher than any other Information Services company Huber Research tracks apart from MSCI (rated OW), but MSCI has a huge moat around its business and 60% EBITDA margins. That is not to say CEO Steve Hasker has not been masterful in re-positioning TRI into growth opportunities and raising the margin profile of the company’s three key segments, but at the end of the day, this is a 6-7% organic growth story, with EBITDA margins in the mid-40% range. Douglas Arthur now estimates 2024 adj. EPS of $3.54 per share (prior $3.80).

Edition: 180

- 23 February, 2024

Consumer Discretionary

On the surface, the fact that CVNA significantly narrowed its EBITDA loss in 1Q23 was very impressive. And the fact that management is saying the company could be EBITDA positive in Q2 is quite amazing. How is this happening? Management is dramatically shrinking the business; marketing has been cut to the bone and Q1 capital expenditures were $32m vs. $220m LY. The flipside is that CVNA still recorded a net loss of $286m. Interest expense was $159m vs. $64m LY. Total gross debt was >$6.5bn. Douglas’ cash flow projections still assume CVNA will need additional outside debt in 2023. Bottom line, this is still a financing tightrope act. 12-month TP $5.00 (60% downside).

Edition: 160

- 12 May, 2023

Communications

Douglas Arthur doesn’t see any crisis occurring at the company as he initiates coverage with a Buy rating in this 70-page report - four aspects stand out: 1) the size and growth prospects of the DTC streaming business; 2) the magnitude and geographic reach of the Parks footprint; 3) the depth, richness and velocity of the company’s content production machine; 4) and, potential earnings power if and when the large streaming business starts to make money. Douglas forecasts adjusted EPS to increase from $3.53 earned in FY22 to $6.90 in FY26, an 18.2% compounded rate of growth.

Edition: 152

- 20 January, 2023

Consumer Discretionary

Race against time - faces a material slowdown right when the company is desperately trying to right-size costs, boost GPU per unit and improve cash flow to address a mountain of debt. Ironically, slower sales volume may ease some of the cost pressures, but Douglas Arthur still envisions a large 3Q EBITDA loss and a FY loss of over $1bn with FCF to be a negative $2bn. At this rate, Douglas believes management will somehow have to tap the debt markets for over $2bn of capital in 2023, further straining the financials. Does not expect CVNA to be EBITDA positive until 2026E.

Edition: 147

- 28 October, 2022

WPP (WPP LN) UK

Communications

A simpler WPP is a stronger WPP - laser-focused around faster growth end markets including ecommerce, retail media and tech. WPP has already raised guidance twice this year, almost completed an £800m buyback and increased the interim dividend by 20%. In addition, a ‘Transformation’ programme is on track to deliver £300m in operational savings. Management’s new full-year guide still implies a significant slowdown in H2 despite it being WPP's seasonally stronger part of the year. Furthermore, there has been no indication that large accounts have plans to cut spending. Douglas Arthur expects forecasts to be beaten this year and next. TP £11.00 (50% upside).

Edition: 143

- 02 September, 2022

DTC Index: Relative valuations at multi-decade lows

Consumer Staples

Douglas Lane’s DTC Index trades at a 45% discount to the S&P 500, which is the lowest prospective relative P/E ratio for the Index since the tech bubble 20+ years ago - Douglas argues value-oriented investors may want to start to move into some of the names in this group given their financial strength, above average gross margins, strong FCF generation and pricing power in what tends to be more defensive product categories. Buy-rated stocks include Herbalife, Nu Skin and Medifast.

Edition: 134

- 29 April, 2022

Corporate HY & Distressed Opportunities: Recent coverage includes...

Iceland - Energy costs, food inflation, and return to workplace post-Covid all weigh on recent bond movements.

Tullow Oil - Spend a dollar to make a dollar; only hedged on the upside for 60% of their planned FY22 production at $78/bbl.

Vallourec - Opportunity in an ill-fitted balance sheet?

Click here for further details and updates on several other names including Douglas, Matalan, Standard Profil and TAP.

Edition: 132

- 01 April, 2022

Are EVs really better for the environment?

Mobilit-e is Climate Transformed’s two-week virtual immersion into every facet of the EV supply chain. Douglas Johnson-Poengsen, CEO of Supply Chains Tracing/optimisation software firm Circulor, delivers the keynote by digging into whether EVs really are better for the environment. To manage the carbon in building an EV, you have to measure it – in this video Paul Krake and Douglas talk about supply chain optimisation, especially for batteries, and debunking myths. Click here.

Edition: 129

- 18 February, 2022

Technology

Sentiment is going down, but numbers are going up! Ignore the cacophony of near-term issues/noise - Street downgrades (expectations that growth will be compromised by disruptors) are unwarranted according to Douglas Arthur. While he expects some disruption, he does not expect NLSN’s central role as currency to change much, if at all - and neither do the major Ad holding companies, who at the end of the day call the shots. Trades at 7.1x forward EBITDA despite emerging financials not that different from higher-valued peers: MSD organic growth, mid-40%’s EBITDA margin, improving balance sheet and heightened potential for a stock buyback. TP $35 (90% upside).

Edition: 128

- 04 February, 2022

Fox Corp (FOXA)

Communications

The new Fox is more profitable than investors expected - two years after it split from 21st Century Fox, the group continues to routinely beat expectations and often by significant amounts. Management are making smart decisions including taking a low-risk, high-reward path to streaming via Tubi - which is on fire (+150% in Q3; FY21E revenue target increased to $350m), avoiding large deals and hoarding cash ($5.8bn). Following yet another earnings beat, Douglas Arthur increases his FY21E & FY22E adj. EPS to $2.95 and $3.05/share (from $2.68 and $2.84). TP increased to $48 (~30% upside).

Edition: 112

- 11 June, 2021