Fortnightly Publication Highlighting Latest Insights From IRF Providers

Company Research

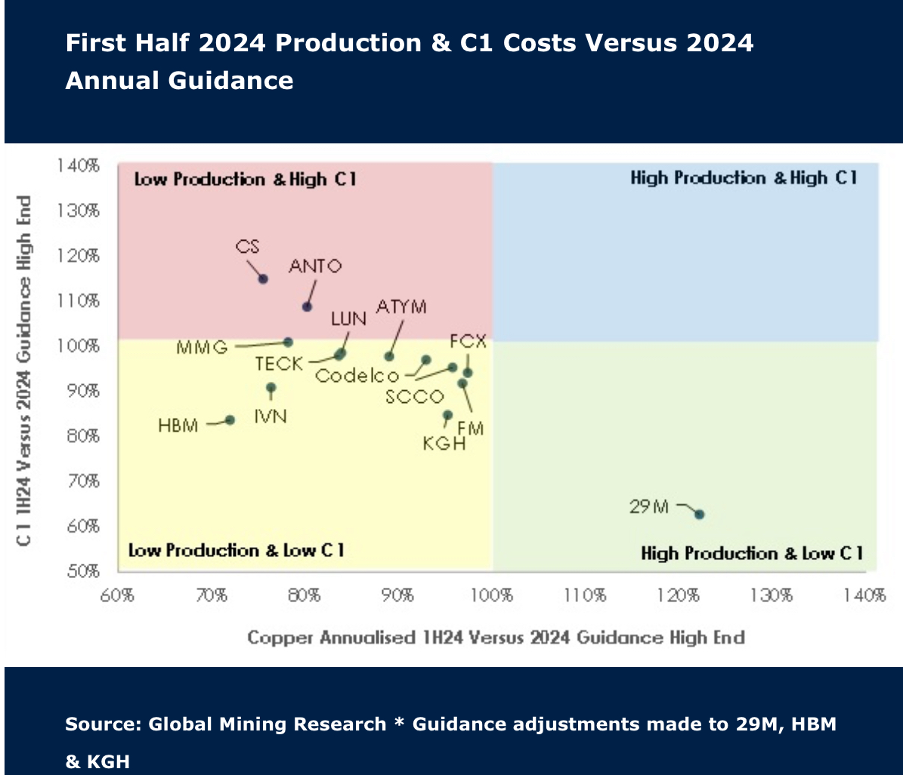

Can copper volumes meet big expectations?

As expected, the first half of the year was met with weaker production, with companies in Global Mining Research’s coverage reporting flat figures of +1.5% and low capex. Costs increased some 4.8%, but this was offset by a ~US$0.60/lb increase in copper prices in the latest quarter. 60% of producers are expecting stronger H2 volumes, but Antofagasta, Ero Copper, Ivanhoe Mines and Capstone Copper are most at risk of missing 2024 guidance. Following the recent pullback and ahead of seasonally stronger Q4 prices, GMR continues to see the sector as attractive. Ratings have been raised for leveraged plays KGHM (to buy) and MMG (to hold).

Edition: 193

- 23 August, 2024

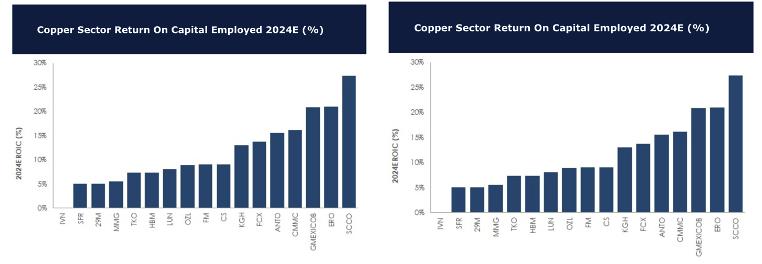

Returns on capital: Copper vs Gold

For 2024, David Radclyffe forecasts copper to enjoy an average ROCE of 11.1%. The standout is Southern Copper Corp, helped by some very low cost and long-lived assets. Relatively new to the market Ero Copper Corp does well, while at the lower end sit Ivanhoe Mines and Sandfire Resources. When it comes to gold, the forecasted average ROCE for 2024 is at 8.3%, with Gold Fields coming out on top and Lundin Gold close behind. The copper sector as a whole continues to generate better real returns on capital than the gold sector, with gold miners continuing to suffer from shorter mine lives and a commitment to M&A to create growth.

Edition: 155

- 03 March, 2023

Preferred copper mine exposure

With copper trading above US$4.00/lb the ability for copper miners to fund initiatives is strong, providing a boon especially for small capitalisation base metals companies. In such a group, David Radclyffe’s preferred exposure is through BUY-rated Capstone Mining and Sandfire Resources, both offering a blend of value and growth, and which have benefited from M&A accelerated growth. Tony Robson considers Ero Copper after its massive underperformance; it is now more attractively priced and the company is pushing exploration hard, but growth is some time out, so he maintains his HOLD rating.

Edition: 132

- 01 April, 2022

Materials

In a bold and transformative step, SFR has announced it has beaten off peers to acquire the Minas De Aguas Tenidas (MATSA) operation in Spain - this is one of the largest copper transactions for some time and it is not cheap (GMR estimates SFR has paid the equivalent of US$3.90/lb LT). Investor interest in the stock is likely to increase significantly given the big jump in Mkt/Cap (it would notionally now have a larger capitalisation than both Hudbay Minerals and Ero Copper). Post deal the miner is trading at a prospective 1.0x P/NPV and 5.9x FY23 EV/EBITDA.

Edition: 120

- 01 October, 2021