Fortnightly Publication Highlighting Latest Insights From IRF Providers

Company Research

Outside of AI, why invest in the US?

US equities remain the world’s most important market, but passive benchmarks are distorted by AI concentration risk. Durable alpha lies in structural themes beyond AI. Power infrastructure (Constellation, Duke, NextEra) will benefit from grid bottlenecks as data centres drive demand. Re-industrialisation (Caterpillar, Honeywell, Rockwell) reflects reshoring and automation. The energy transition (Dominion, Enphase, ExxonMobil) requires trillions in capex. Housing scarcity (D.R. Horton, Home Depot, Lennar) is a structural imbalance. Healthcare innovation (Abbott, Eli Lilly, UnitedHealth) rides longevity and med-tech advances. Cybersecurity (Cisco, CrowdStrike, Palo Alto) is non-discretionary. Generational wealth transfer (BlackRock, Morgan Stanley, Schwab) reshapes capital flows. The AI productivity super-cycle is real, but thematic allocations across these shifts offer broader, smarter US exposure.

Edition: 220

- 19 September, 2025

What’s the right beta for your portfolio?

Trivariate analysed the top 500 US equities for five factors beyond the market: size (top 100 vs. 401-500), growth vs. value, high-quality vs. junk, liquidity and momentum. They focused on 3 different portfolios (min-vol, max-Sharpe, max-return) to show a range of outcomes. Over the last 20 years, the “efficient frontier” or optimal beta for a median portfolio appears to be between 0.95 and 1. If you are looking to lower your portfolio beta efficiently, owning high-quality value stocks with relatively low liquidity is a prudent strategy (e.g. Exxon Mobil, Philip Morris, Lowe’s, Medtronic). If you want to take more risk, the optimal factor loadings would be to add to highly liquid growth stocks that are junk quality (e.g. Tesla, Applovin, Micron).

Edition: 204

- 07 February, 2025

Energy

Pipe to nowhere - Hamed Khorsand believes SOC will be unable to gain all the regulatory approvals necessary to restart the Santa Ynez Unit it acquired from Exxon. SOC is likely to spend much of the cash it has raised and end up giving back the assets to XOM without any compensation, per the purchase agreement. The share price has risen nearly 100% in the past year, but trades with no risk applied to possibilities of delays to the company’s stated timeline to restart Santa Ynez in 4Q24. TP $6 (70%).

Edition: 197

- 18 October, 2024

US: Investing in a Trump Presidency

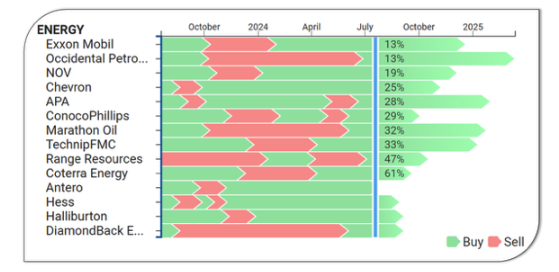

Tenviz has an impressive record of forecasting unexpected political outcomes before they happened, including Brexit, the Covid lockdowns, the WTI oil price drop in 2023, and growing political tensions in France along with their subsequent reversal before the election surprise. Konstantin Fominykh advises investors to follow markets to forecast politics, not the other way around. His recent BUYs reflect a possible Trump win. Energy is an obvious contender, and Konstantin has new buys on the likes of Exxon Mobil and others (see chart). He also sees positive upside for Big Pharma, which will be subject to fewer price controls, and a preference for mid and small caps as they benefit from higher tariffs and lower interest rates.

Edition: 191

- 26 July, 2024

Nigeria: Indecisiveness could discourage investment in oil production

Exxon announced in February the sale of $1.3bn worth of shallow water fields in Nigeria. Since then, Nigerians have been indecisive, with President Buhari attempting to prevent the deal. Allowing it will welcome and encourage the major oil companies’ capital, but this freedom also implies the right for Exxon, and others, to exit ageing infrastructure in areas where local factions run riot at the expense of the oilfields. Buhari needs the major capital; he wants the EU gas deal desperately; those pipelines to Europe are potentially a life saver for Nigeria. But having Big Oil leave the difficult areas? That is a disaster.

Edition: 142

- 19 August, 2022

SBM Offshore (SBMO NA) Netherlands

Energy

Despite a positive outlook for new orders SBMO shares still trade at a relatively high discount to NPV - highlights opportunities to win additional contracts with the likes of Exxon where FPSOs SBMO has been building are very efficient (breakeven price for the ONE Guyana FPSO is pegged at $29/BBL Brent). Analysts at the IDEA have previously demonstrated that each new FPSO contract could add up to €1 to €2 per share in the NPV of the company’s L&O portfolio. This value already amounts to between €19 and €23 per share based on discount rates of 8% and 6% respectively. SBMO shares currently trade at €13.70.

Edition: 135

- 13 May, 2022

Global Clean Energy Holdings (GCEH)

Energy

Is in the final stages of turning a crude oil refinery into a renewable fuel refinery utilising camelina as its primary feedstock - GCEH has a patented camelina seed for refining into renewable diesel approved by the California Air Resources Board, making GCEH vertically integrated. The company has also obtained a product offtake and purchase agreement with Exxon Mobil for nearly all the production from its under-construction refinery, scheduled for commercial production later this year. The Series C Preferred funding completed last month gives GCEH capital to finish construction. It also makes XOM financially invested in GCEH. TP $7.55 (55% upside).

Edition: 131

- 18 March, 2022