Fortnightly Publication Highlighting Latest Insights From IRF Providers

Company Research

Venezuela: US intervention

The Don-roe Doctrine is taking shape as the Trump administration intensifies its war against cartels in the Western Hemisphere. The recent deployment of significant military assets to the Caribbean, the authorization of a covert action program in Venezuela, and a rhetorical escalation against cartels are putting intense pressure on Venezuelan President Nicolás Maduro. Now, a constellation of forces—principally driven by US Secretary of State Marco Rubio—is even pushing for direct intervention in Venezuela, up to and including regime change. Niall Ferguson sees a heightened probability of US strikes between now and February. While “regime change” is not his base case, there are meaningful pathways to escalating intervention. Once strikes start, they become very hard to stop. Although Niall expects volatility ahead, bonds have continued to rally, likely due to market sentiment that whatever happens in Venezuela is better than the status quo. Despite the uncertainty, the bond rally looks likely to continue.

Edition: 223

- 31 October, 2025

Argentina: Milei’s landslide

Javier Milei won the Argentine midterms decisively with his candidates winning in 16 of 24 provinces, with ~40.8% of the total vote. Most surprisingly, Milei’s La Libertad Avanza (LLA) even won the Buenos Aires province—home to 37% of the country—after losing a local election by 13 points in September. Niall Ferguson sees the victory as firmly consolidating the government’s programme and renews the value of its alliance with former President Mauricio Macri’s PRO in key districts. Milei’s victory speech was conciliatory and clearly opened the door to new alliances with regional governors, which the US has been insisting on. Niall also expects further changes to the FX regime, which still needs reform. The other key winners are President Trump and Treasury Secretary Scott Bessent, who will see this result as vindicating their support for a Latin American government aligned with the United States. Expect strong rallies in Argentine assets.

Edition: 223

- 31 October, 2025

France: Survival

French Prime Minister Sébastien Lecornu survived two motions of censure on Thursday in the French National Assembly. The oppositional far-right Rassemblement National (RN) and the far-left France Insoumise (FI) were 18 votes short of toppling Lecornu. Parliament will now negotiate the 2026 budget, which it will vote on in December, and Macron can sigh a breath of relief. These negotiations could still fall apart, with the centre-left Parti Socialiste (PS) likely to threaten that it will walk away from a budget deal. That said, Niall Ferguson’s base case is that the various centrist parties that backed Lecornu today will reach a budgetary compromise resulting in a deficit of around 5% of GDP. The rise of French sovereign bond yields is over… for now.

Edition: 222

- 17 October, 2025

From precious to soft

Craig Ferguson has come full circle in recent weeks in his thinking about the beneficiaries of US inflation. For the last few years, he’s been playing gold & silver longs, seeing them as good hedges against a weaker US economy, falling Fed Funds, the USD, and inflation. The story has worked out pretty well for Craig, but now he sees both precious metals as heavily overbought and has now exited his longs. His attention has now shifted to ags, grains, softs and energy commodities, with sugar, wheat and natural gas added to his portfolio to the tune of ~5% exposure. Over the coming weeks, Craig is considering adding corn and cotton and possibly WTI oil to the mix, with the diverse commodities basket potentially reaching 10% of his Growth SMA portfolio.

Edition: 221

- 03 October, 2025

Germany: Angela Merz

Four months in and Chancellor Merz’s government has a mixed record, and Niall Ferguson says that doubts over the coalition lasting until 2029 are justified. However, media forecasts for a near term breakdown are unlikely to be founded, and Niall expects the coalition to survive beyond November of next year. Even if the AfD secures victories in state-level elections, Merz and Vice-Chancellor Klingbeil will be able to use the argument that time must be given for economic recovery before the electorate rushes to the polls for another party. Russia’s antics in testing NATO should bolster the coalition’s cohesion. Niall is positive on German equities and continues to be constructive on German growth, which will in turn boost Europe as a whole.

Edition: 221

- 03 October, 2025

Europe: The Art of War

It’s been a rough summer for Europeans. The EU-US trade deal is highly unpopular, yet European leaders had little choice if they wanted to keep President Trump on their side in Ukraine. Niall Ferguson expects the European Parliament to ratify the deal. At the same time, EC President von der Leyen is looking to diversify trade deals, and Niall expects one with Mercosur countries to be ratified by year’s end. The EC will also walk back commitments under the Green Deal, including softening emissions targets for the auto industry, which will provide businesses with much needed breathing room. Niall expects frozen Russian assets and higher bilateral support from member states to support Ukraine, with defence-only EU bonds materialising next year. He remains bullish on European defence and dual-use tech.

Edition: 220

- 19 September, 2025

US stocks the most overvalued in 130 years

There is no escaping overvaluation if you are a multi-decade investor. The seven typical valuation measures that Craig Ferguson monitors are now at such an extreme that at nearly a 99th percentile rating the level of US equity market overvaluation is now the highest level seen since 1980 when records pretty much began. The signal is clear: long-term investors should be markedly UW stocks and largely out of US equity markets. This may be against consensus as the globe remains OW equities, but this is at a time when old sage Buffett is raising cash to $35 or more of his portfolio just as he did in the two most recent major overvaluation episodes in 1999 and 1966. Chart 2 shows that large global hedge funds are now nearly as short S&P VIX futures (or volatility) as they were in late 2021, just before the Nasdaq plunged by -38%. This won’t end well for equity markets.

Edition: 219

- 05 September, 2025

Argentina: Brace for volatility

As the country enters its midterm electoral season soon and more important national midterms in October, Niall Ferguson comments on how erratic monetary policy, fuelling FX instability and very damaging moves in local rates, undermines the credibility of Milei’s economic team. Data suggests that economic activity has weakened. Niall expects Milei to win the midterms, with citizens endorsing his disinflationary success whilst the opposition remains headless. Yet the likelihood of defeat in the Peronist-leading Buenos Aires province has grown. The September outcome will be crucial to avert further volatility in rates and FX, and Niall believes that the popularity of Milei’s stabilisation plan will give him an opportunity to consolidate public support and steady markets, but do not lose sight of the key fact that October is what matters most.

Edition: 219

- 05 September, 2025

France: Instability ahead

The country is entering another period of political turbulence over next year’s budget. Niall Ferguson sees Beyrou’s days as prime minister as numbered, expecting him to lose the confidence vote on September 8th. This will put President Macron back into the driver’s seat, and Niall expects him to nominate another minority government that can secure a 2026 budget with PS cooperation. Yet such a budget would reduce the deficit only marginally. The other scenario is parliamentary snap elections in autumn, which would raise the risk of a victory for RN. In any case, Niall expects the risk premium on French sovereign bonds to rise in the coming weeks, with Frech political instability a major European theme for 2H/2025.

Edition: 219

- 05 September, 2025

Bolivia’s long goodbye to Evo

After two decades of leftist rule, Bolivians rejected the socialist candidate backed by former president Evo Morales’ party. The two remaining candidates are both eager to introduce fiscal discipline and pro-market policies. Markets have rallied since April on expectations of this pro-market shift, but Niall Ferguson points out that the market is shallow. The country’s weak macroeconomic fundamentals call for painful austerity and structural reforms. Should the election winner quickly commit to fiscal austerity, abandon the peg, and implement reforms, Bolivian assets could see upside. However, investors should expect things to get worse before they get better.

Edition: 218

- 22 August, 2025

Australia: The consumer shines bright

Craig Ferguson says that better confidence in Australia should mean relatively higher AU yields and Aud FX rates, and even stronger AU corporate earnings outlooks. Craig’s chart of the day focuses on the relative outperformance of the AU macro economy, a theme he first noted around 4-8 weeks ago and one which has firmed up with the data inflow over that period. On the one hand, markets still expect a further 2 rate cuts from the RBA in this cycle, but on the other Craig has been arguing that the rebound in AU PMI, NAB, Ai Group, jobs, building approval and even the latest consumer confidence survey all suggest that the country’s economy is in a re-acceleration phase as the RBA’s slow motion 3 rate cut cycle so far starts to have an impact.

Edition: 218

- 22 August, 2025

Super Copper

Craig Ferguson points out that US tariffs uncertainty remains with 50% tariffs on copper imports spiking the metal to new all-time highs. He expects a supply deficit from next year, one that will last for years as electrification and the transition to renewables unfolds. Countries like the US will now build copper strategic reserves, so Craig would not fade this price spike. This may be the start of a major run higher in the commodity and inflation cycle with copper (and gold, uranium and platinum) already leading the way. This may suggest a new super cycle in commodities has begun. This would suggest a super cycle in big ASX miners and the AUD also has begun (be OW both). However, it also is inflationary and would complicate things for global central banks, bond yields and stock markets. Craig is surprised that both BHP and the AUD are not higher as both should be on this news.

Edition: 215

- 11 July, 2025

Industrials

Northcoast raises their TP for the stock to $250 (24x 2026 earnings estimate of $10.58), citing strong execution and share gains in HVAC, helped by FERG's focus on dual/multi-trade contractors and leverage to Daikin brands amid R-454B shortages. Management lifted guidance, with gross margins now seen above 30% and higher operating margin expectations, reflecting strong pricing and easing commodity deflation. Despite weak residential markets, FERG’s diverse end-market model is proving advantageous. With private label potential, sales leverage and underappreciated non-residential exposure, Northcoast sees the stock as undervalued and well-positioned to benefit from shifting industry dynamics and eventual recovery in residential demand.

Edition: 214

- 27 June, 2025

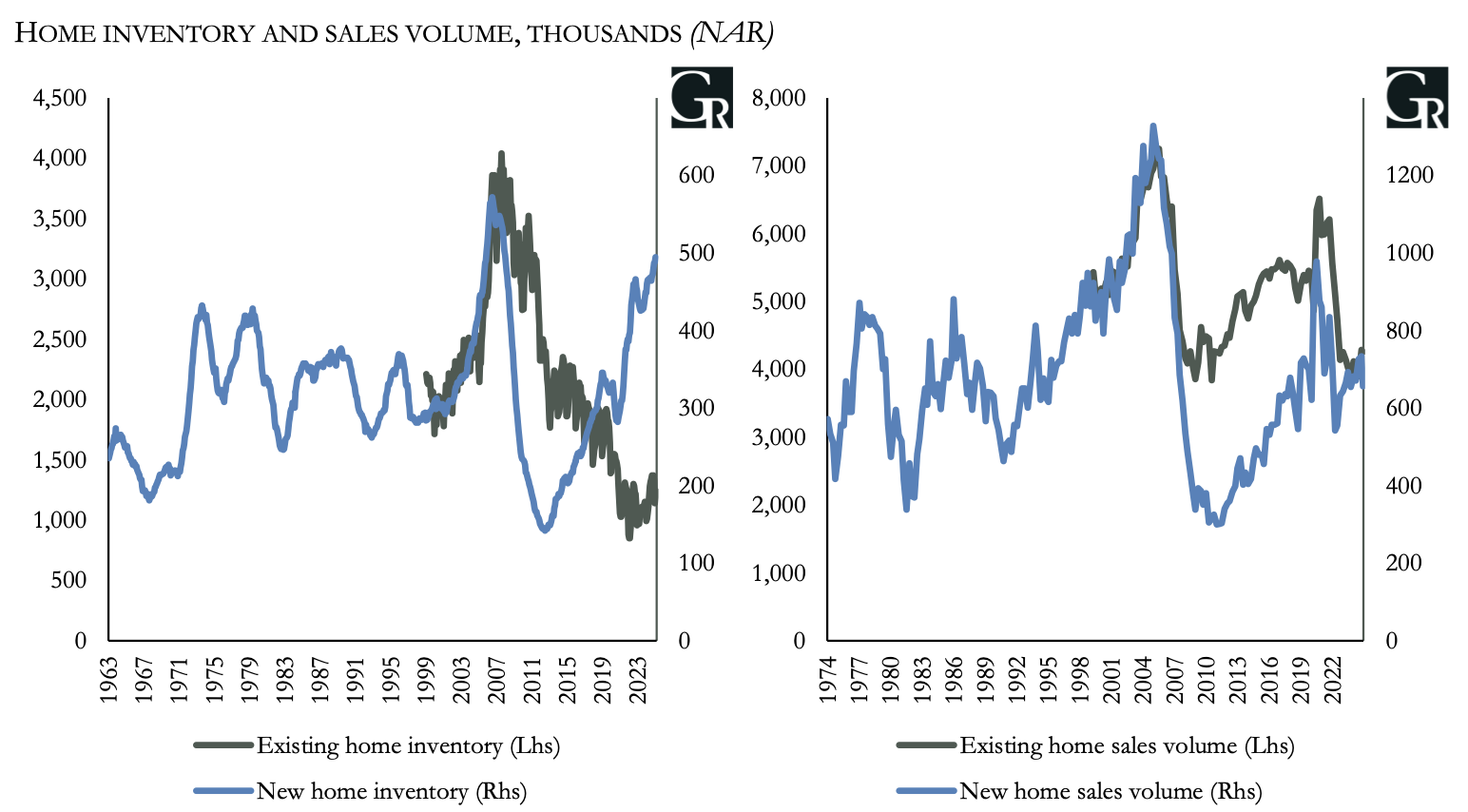

US: Housing hazards

Niall Ferguson points out the signs of weakness in the US housing market in his latest detailed report. Home inventories are high (see chart), whilst unaffordability prices out the median American from buying a home. A continually rising average mortgage rate, even in the best-case scenario, will increase net interest expense and put pressure on household budgets even as the prevailing new mortgage rate declines. Homebuilder-specific negative impacts from the Trump administration’s economic policy, namely reduced immigrant labour and higher prices for import-exposed building materials, all add to the case for bearishness.

Edition: 208

- 04 April, 2025

Middle East: The conflict is about to widen

Niall Ferguson says the collapse of the Gaza ceasefire and the launch of a major U.S. campaign against the Iran-backed Houthis in Yemen are not isolated events—they are likely steps in an escalating sequence that could culminate in strikes on Iran’s nuclear program by mid-year. The U.S. struck first against the Houthis, launching its largest wave of attacks since 2015, then declared “sustained combat operations,” vowing to hold Iran responsible for further attacks. This effectively creates an open-ended pretext for strikes on Iranian targets in Iraq and Iran itself. Meanwhile, Tehran’s hardliners remain entrenched, refusing talks even as economic pressure mounts. With inflation soaring and the rial collapsing, the Iranian regime sees capitulation as a greater risk than economic collapse. A wider conflict looks more likely in the coming months.

Edition: 207

- 21 March, 2025

Canada: The Trump effect

After months of rising fortunes for Canada’s Conservatives, Donald Trump’s return to power in the United States and fresh Liberal leadership at home seems to have reversed the tide. In two months, the Conservatives’ double-digit polling lead has disappeared. Niall Ferguson expects newly elected Prime Minister Mark Carney to announce an early election on March 23rd, with elections in late April or early May. He sees Carney retaining his premiership (60% probability). Post-election, Trump’s escalating tariffs will force Canada to cooperate in order to minimise recession risk and gain more favourable terms for USMCA renegotiation in H1/2025, with Canada making tough concessions on sectoral market access, the trade balance, and Chinese value-added in North America.

Edition: 207

- 21 March, 2025

Germany: An emboldened defence

As is characteristic of its post-war history, Germany’s leaders took a very long time to move. But when they do, they move radically. The recent decision clarifies that Berlin now means Zeitenwende for real and that the geopolitical situation has fundamentally changed, with Europe having to take responsibility for its own security in the medium term. The fiscal howitzer Merz intorduced will benefit all of Europe in economic terms, as not only German, but all European defence companies will profit. With Merz, Germany will have a leader who sees German and European strength as complementary. The consequences for markets, macro, and geopolitics should not be underestimated. Niall Ferguson remains long defence and sees a growing case for European infrastructure and green tech.

Edition: 206

- 07 March, 2025

Navigating a multi-polar fragmented world

Craig Ferguson’s core macro/AA view says a 40yr disinflation cycle ended in 2020 and that a new multi-decade inflationary cycle began. This has seen cash rates rise, global growth slow, rates get cut and inflation fall. At the start of 2025 Craig points out that we are now near the end of the first up (2020/22) and down (2023-24) cycle, so a new cycle may be starting. Craig’s takeaway from his detailed analysis of US/Trump geopolitical & economic policy is to expect stagflation forces to unfold and impact AA portfolios during 2025-28… For now, Craig says we need to face up to the notion that markets are priced for perfection in an uncertain and fragile geopolitical, economic and military world. The new order may last decades, and investors need to position their asset allocations for this important change.

Edition: 206

- 07 March, 2025

Mexico: The Art of (Trade) War

Over the last few weeks, Niall Ferguson’s team met with high level officials and representatives in Mexico. The trip emboldened their belief that President Sheinbaum will do “whatever it takes” to avoid tariffs and preserve USMCA, choosing to concede to American demands on security, the border and the trade deficit, including the trade relationship with China. This stems from a belief that the country will face an immediate recession should the trade war escalate. Despite Sheinbaum’s previous rhetoric against Trump, pragmatism will prevail to preserve USMCA and the economic benefits it has brought to Mexico.

Edition: 205

- 21 February, 2025

Ecuador: Election amidst the chaos

Ecuador is gearing up for a presidential election. An ongoing energy crisis and the collapse of the country’s security apparatus amidst drug cartel violence have eroded President Daniel Noboa’s once-stellar popularity. Yet, Niall Ferguson expects him to win what is in effect a rerun of the 2023 presidential race. Perceptions of political risk might increase in the short term, since Niall expects Noboa to face a competitive run-off against a leftist candidate in April, but he should win it in the end. For the first time, Ecuador’s centre-right may achieve a strong bloc in the National Assembly, as Noboa’s party is poised to win 35% of the seats. Expect a strong legislative coalition, which will secure policy continuity, and a stronger mandate for reform. This makes Niall constructive on Ecuador despite the dire domestic security situation, with sovereign debt looking favourable.

Edition: 204

- 07 February, 2025

Oil: Pressure on all fronts

Oil prices rallied above $80 in the last fortnight after news of a major US sanctions package targeting Russian oil plus expectations of disruption to Iranian supply. Niall Ferguson believes that the impact on Russia is material, taking around 400,000 barrels per day (bpd) off the market, although he expects Russian flows to normalise gradually as workarounds are found. The US is also likely to take ~500,000 bpd of Iranian exports offline. Nonetheless, as the Russian and Iranian oil affected represents less than 1% of global oil demand, Niall thinks oil prices will still trend downwards throughout 2025, given the weak demand growth outlook, strong non-OPEC supply and the increasing risk of a price war launched from within OPEC.

Edition: 203

- 24 January, 2025

US: All on black

Just as the characters in The Hangover did, Trump is putting it all on black. Policy, deregulation, mercantilism, the list goes on. Later down the track, Craig Ferguson says, this will all be inflationary. Ultimately, it is the cost of capital, inflation and bond yield levels that have ended all of the booms of the last 100 years in the US. Too much of a good thing may be about to be had by all, and if that occurs with equities so overvalued the hangover (bear market) when it unfolds is a bad one. Few recall that the S&P was -55% twice in the noughties decade (’03 and ’09), but that is the sort of unwind required when overvaluation gets this big. Dancing while the music is still playing, as was the rule in 2007, appears to be all the rage again now. At some stage though, everyone needs a chair.

Edition: 203

- 24 January, 2025

Asia: Chips and electronics

Niall Ferguson’s spent a week in India and Malaysia, meeting with high-level executives from the tech, semiconductor, and venture capital industries, as well as senior politicians. Both countries are ramping up investments in semiconductor and electronics manufacturing, supported by foreign capital and government initiatives. India is poised to grow its market share in low-end assembly for Western chipmakers and electronics, though talent shortages and bureaucratic inefficiencies hinder progress. In Malaysia, business leaders are concerned about losing market share to Chinese firms in the domestic chip industry, while the government remains accommodative, despite internal debates. The overall outlook is one of optimism, and both countries are well positioned to strengthen their roles in low-end chip assembly for Western tech firms.

Edition: 203

- 24 January, 2025

Australia: Bond markets need to reprice expectations further

This week’s data didn’t come as a surprise to Craig Ferguson, but it did to bond markets that had rushed to price in a 70% change of an RBA cash rate cut come February. After this week’s data release, expectations have been cut towards 50%. Yet Craig believes that the RBA is unlikely to think about cutting rates anytime soon, and that markets may reduce the 50% probability to zero over time. A May cut could be a slight chance if inflation, jobs and GDP weaken but August looks more likely. As such, as cuts gets priced out, the AUD and AU 10yr yields could find support, although the AUD will also be driven more by USD direction moving higher and AU 10yr yields could be more driven by global yield trajectories moving higher rather than the RBA.

Edition: 201

- 13 December, 2024

From Tokyo to Seoul

Niall Ferguson’s team spent two weeks in Tokyo and Seoul and spoke with high-level policymakers, diplomats, economists and investors. Both countries are looking to reduce their US trade surpluses ahead of President-elect Donald Trump’s anticipated tariffs, including by purchasing more US LNG and increasing US FDI inflows. Niall is increasingly confident that the Japanese economy’s wage-price growth cycle and the BoJ’s continued policy normalisation will continue into H1/2025. In Seoul, even President Yoon Suk-yeol's own People Power Party wants him to resign. If he does not resign in the coming weeks, he expects the National Assembly to impeach him. Either way, a snap presidential election in H1/2025 is Niall’s base case. He maintains his bearish outlook on South Korea’s export-dependent economy, which is driven primarily by structural factors rather than political risk, though defence makers will likely return as a bright spot in 2025.

Edition: 201

- 13 December, 2024

Euro: Running behind

For the fourth time in 2024, the ECB cut rates by 25bps. At 3.0%, the deposit facility rate is down 100bps from its peak and approximately half-way down to what many believe to be the neutral rate of ±2.0%. PMIs now suggest that the Eurozone economy may barely grow, so concerns over undershooting inflation have risen. They should, according to Niall Ferguson. However, calls for accelerating the pace of rate cuts are unlikely to gain traction until there is a clearer signal of inflation undershooting and hard data on growth stagnating or even being negative. The ECB could also be prompted to consider a larger than 25bps move if Trump’s trade threats materialise. Nevertheless, Niall’s baseline is that the ECB will cut by 25bps in January and March. In short, they will remain behind the ball. He remains short EURUSD.

Edition: 201

- 13 December, 2024

Germany: Who is Friedrich Merz?

Germans are set to elect a new Bundestag on February 23, 2025. For now, the centre-right Christian Democratic Union (CDU) under party Chairman Friedrich Merz leads in the polls by a large margin. The centre-left Social Democratic Party (SPD) of sitting Chancellor Olaf Scholz could attempt to gain ground by abandoning Scholz and backing the very popular defence minister, Boris Pistorius, as candidate for chancellor. Such a move could upset the race. But even then, Niall Ferguson’s base case remains that Merz will become Germany’s tenth post-war chancellor. Merz would govern with either the SPD or the Greens. His arrival would translate into a loosening of fiscal policy, supply-side economic reforms, more robust support for Ukraine and potentially even the issuance of EU bonds to finance defence spending.

Edition: 200

- 29 November, 2024

Mexico’s political regime change

A month into her presidency, Mexico’s Claudia Sheinbaum is struggling to contain the fallout from her predecessor’s judicial reform. With its supermajority in Congress, her party Morena is keen to advance former President Andres Manuel López Obrador’s agenda, no matter the cost. Meanwhile, the economy has proved surprisingly resilient in 3Q24, but the ongoing constitutional crisis at home and Donald Trump’s re-election to the US presidency will increase the doubts about the coming years for Mexico. Local sources seem optimistic that energy reform will end profligate spending by the state oil company Pemex, with its bonds rising in value ahead of a possible rating improvement. Niall Ferguson expects MXN to depreciate further in the coming year, with lower domestic rates, and is SHORT MXN/USD.

Edition: 199

- 15 November, 2024

Japan: A short run

On Sunday, Japan’s ruling Liberal Democratic Party (LDP) lost its House majority for the first time since 2009. Prime Minister Ishiba Shigeru will now seek to form a government and the House will likely elect him prime minister in November. Opposition parties are divided amongst themselves and two are open to partial cooperation with the LDP. Niall Ferguson expects Ishiba to form a government on a platform of political reform, dovish fiscal policy and a (potentially unfunded) increase in military spending. The most likely outcomes are an LDP-Komeito-led minority government (40% chance) or a coalition involving some sort of combination of Komeito, Ishin and the DPFP (30%). Ishiba is in a weak position, however, and must generate a better result in the Upper House election in July, or will probably have to resign.

Edition: 198

- 01 November, 2024

US: The Dems have fought well, but a Trump win is expected

Polling margins in the 2024 presidential election are even closer than they were at this point in 2020 or 2016. Former President Donald Trump or Vice President Kamala Harris are both well-positioned to win. Polls could underestimate either candidate. Late-breaking events, such as escalation in the Middle East or new opposition research, will impact perceptions of Harris far more than Trump. Harris will be helped by her generational change message, Democrats’ early and mail-in voting advantage, fundraising and abortion ballot measures. But Niall Ferguson narrowly expects Trump to win due to his policy advantages and voters’ doubts that Harris is up to the task. If Trump wins, the GOP will likely have unified control of Congress given a favourable map in the Senate and limited split-ticket voting in the House. If Harris wins, she would likely face a split Congress and thus more legislative constraints.

Edition: 197

- 18 October, 2024

MENA: The big payback

For nearly twenty years, Israeli Prime Minister Benjamin Netanyahu has warned about the perils the Iranian nuclear program poses to the Jewish people in particular and to the world in general. In the coming months, he may finally have an opportunity to destroy the program, leveraging the momentum of Israel’s recent successes to achieve his life’s goal. Despite serious logistical obstacles, Niall Ferguson thinks Israel could manage a conventional strike, the odds of which are elevated (40% probability by year-end). However, he anticipates that an attack on the nuclear program would come at the end of an escalation cycle rather than at the beginning of one.

Edition: 197

- 18 October, 2024

US: Bullish at the wrong time?

Craig Ferguson’s charts highlight the extent of analyst earnings optimism. Chart 1 indicates that analysts expect a 9.4% rise in S&P EPS in the next 12mths, with every sector contributing but energy sector EPS leading the charge rising by over 20%. Is it really possible to see the entire US energy sector record a 20% profit increase in the next 12mths? Global growth has not stopped slowing and downside will only intensify. Furthermore, after holding a 5000 average price target for October 2024, analysts have now jumped well ahead of the S&P’s current level to hold an October 2025 6287 Index target (chart 2). Arguably, right at the wrong time as global growth downside risks accelerate, analysts have increased their bullishness on the S&P to well above current levels. Are they going all in on the soft landing? It certainly looks like it, probably at or near the high.

Edition: 196

- 04 October, 2024

Europe: Budget crunch in Berlin and Paris

In France as well as Germany, upcoming budget negotiations could fracture fragile governments. France’s sovereign risk premium could rise further if Marine Le Pen, the leader of the far-right Rassemblement National (RN), decides to censure Prime Minister Michel Barnier in December. In Berlin, Niall Ferguson expects the Free Democrats (FDP) to exit the three-way coalition of Chancellor Olaf Scholz over budget negotiations this autumn. German snap elections in February or March 2025 would be market-positive. The center-right Christian Democrats (CDU) would most likely emerge victorious and open the door to a slight softening of the debt brake to allow for higher defence spending. In France, however, the risks are to the downside as Barnier braces himself for an exceptionally short term as president.

Edition: 196

- 04 October, 2024

Brazil: Pre-election jitters

Brazil’s economy may be growing faster than expected as moderates win a prolonged battle over the future of monetary policy, but continuing fiscal uncertainty is still casting a shadow over the country’s prospects. Despite Finance Minister Fernando Haddad’s dogged efforts to stabilise public finances ahead of local elections next month, the pressure to spend remains high and private sector analysts expect Brazil’s indebtedness to continue rising. Niall Ferguson agrees. And the political situation is far from ideal, pushing the country toward higher spending amidst a high debt pile.

Edition: 195

- 20 September, 2024

China: Concerns among the crowd

Niall Ferguson’s team spent two weeks in Beijing and Shanghai speaking with sources in economics, tech, finance, and policymaking. Sentiment has improved marginally since the start of the year, but substantial concerns remain about the property sector and the government’s too-little-too-late approach to policy support. Given the rhetoric from the “Third Plenum” and recent weak 2Q/2024 data, Niall Ferguson expects an announcement around October of another RMB 1trn in central government-issued bonds, as well as another bond quota for local governments to purchase unsold homes and aid the flailing property sector. He expects Beijing to target “around 4.5%” GDP growth next year. Geopolitical tensions may have softened lately, yet Niall urges optimism; regardless of the US presidential election outcome, the Chinese firmly believe that Cold War II will remain the status quo.

Edition: 194

- 06 September, 2024

Korea: No credit for Yoon

South Korea’s economy remains resilient thanks to continued momentum in exports and reviving private demand. Regardless, President Yoon Suk-yeol and the ruling conservative People Power Party (PPP) face political headwinds, including a wave of impeachments. Niall Ferguson is short South Korean equities, as rates stay higher for longer in 2H24 and Chinese competition seizes exporters’ market shares. A Harris win in the US will leave their relationship with Korea largely unchanged. A Trump success would be a setback for exporters due to potential renegotiation of KORUS and pressure to appreciate the KRW, but his administration would increase pressure on US allies to raise defence spending. Even if this doesn’t happen, the defence industry is faring nicely with healthy profits and limited competition and will benefit from a bipartisan consensus to support the industry. Niall is long the South Korean defence sector.

Edition: 193

- 23 August, 2024

The history of fraud in Venezuela

After a fraudulent election on July 28th, Nicolás Maduro has been proclaimed Venezuela’s president-elect. As the international community questions the results and the opposition calls on the population to protest, Niall Ferguson reviews previous fraudulent electoral cycles that could serve as a guide for what is to come. Using this applied history framework, he finds that the factors that will determine the ultimate outcome are: a) the cohesion of the Venezuelan armed forces, b) the resistance of the opposition, and c) the ability to coordinate and mobilise civil protests, both inside the country and abroad. Given both Venezuela’s history and the current state of affairs, Niall believes that the military still has incentives to support Maduro at this stage, even if there are some low-level defections. Unless the military supports civil efforts to overthrow Maduro, a transition is unlikely.

Edition: 192

- 09 August, 2024

Venezuela: Maduro’s last stand

Opposition Edmundo remains on the ballot with a high polling lead and Niall Ferguson sees a low likelihood of him being removed ahead of election day. President Nicolás Maduro’s likely strategy of electoral fraud runs contrary to all reliable polling. If there is no fraud, Edmundo should win by a landslide, with clear upside for Venezuelan bonds—Niall does not expect secondary bond trading sanctions to be implemented regardless of the outcome. If Maduro chooses to steal the election, Niall believes he is unlikely to succeed. In his base case, he would expect Venezuelan assets to rally as markets price in the political transition away from Chavismo. This represents a huge opportunity for the country and its assets over the coming years.

Edition: 191

- 26 July, 2024

France: A minority government will not last for long

Niall Ferguson’s base case materialised in France, with voters electing a hung parliament. Yet, to everyone's surprise, the left-wing alliance NPF won the most seats in the second-round vote. The margin of victory is small and is the result of many triangulations in the last week when candidates dropped out to avoid splitting the anti-RN vote. Macron will now nominate a prime minister from the NPF alliance to head a minority government, but this might last only a couple of weeks before the new parliament votes it out again. Niall’s base case thus remains a technocratic caretaker government to take over this autumn and rule France until a new round of elections a year from now. Fiscal policy will remain basically unchanged and France will not throw the continent into a new eurozone crisis.

Edition: 190

- 12 July, 2024

US: Contentious concentration

The US equity market is top-heavy, expensive and exhibiting high beta returns. The current iteration of the technology rally, the Magnificent 7, is riding the wave of AI hype. Niall Ferguson sees near-term risks in the growing disappointment of cloud or AI product revenues, the size of data centre capital expenditures, or the ability of large AI models to scale with compute. For the moment, none of these risks has materialised. However, given the beta-driven nature of the rally, it is reasonable to expect a harsh market correction when a correction does arrive. The historical example of the Nifty Fifty of the 1970s is relevant, which highlights that a crash is not inconsistent with entrenched firms continuing to have strong revenue growth in the ensuing decades.

Edition: 189

- 28 June, 2024

Israel and Palestine: On two fronts

Israel’s strategic dilemma has worsened over the last two weeks. Ceasefire and hostage negotiations have stalled. The fundamental dilemma remains: Hamas believes international pressure will force Israel into de facto capitulation in Gaza, while anything short of Hamas’s political and military destruction would be a defeat for Israel. Combat in Rafah will continue for at least four more weeks. Simultaneously, Hezbollah has significantly ramped up its operations against Israel. Several major incidents this week seem like milestones on the road to war, which Niall Ferguson continues to believe will happen before September. A two-front war is not Israel’s preference, but an emboldened Hezbollah may leave it with no choice—and the growing likelihood of a Third Lebanon War further reduces Hamas’s appetite to reach a hostage deal. Expect the impasse to drag out through June.

Edition: 188

- 14 June, 2024

Argentina: Swift action needed

After six months in power, President Milei’s performance is remarkable. Nobody now challenges his legitimacy and the opposition is leaderless. This is no small feat in Argentina. His popularity appears highly resilient, despite the fiscal shock therapy and recession. If Milei gets his Ley Bases and if Caputo manages to bring inflation down close to the official rate of exchange rate depreciation in the coming quarter, the initial programme will have been a success. Yet Niall Ferguson worries that inflation is being kept down by artificial and/or temporary factors such as frozen prices or delayed subsidy removals. After the Ley Bases passes, the government needs to move fast with the IMF and the lifting of capital controls, which are the necessary preconditions for the economic recovery Milei needs for 2025.

Edition: 187

- 31 May, 2024

Argentina: The fight against inflation

President Milei achieved what he needed to in April. Despite the ongoing recession and protests, Milei delivered on his major political promise: disinflation. The passage of the “Bases” bill in the lower house after weeks of patient negotiations shows Milei’s commitment to the actual delivery of structural reforms. This bodes well for the Senate, where Niall Ferguson expects the law to pass in May. He thinks that as long as inflation keeps falling, the recession will be socially tolerated, and Milei’s political authority will not be severely damaged. He is still doubtful whether disinflation can consolidate. The main risk now seems to be of the FX getting too expensive. Yet the direction of travel remains positive: presidential popularity, disinflation, reforms, and fiscal balance. And so, Niall remains constructive.

Edition: 186

- 17 May, 2024

Japan: Slipping lower

The BoJ unanimously voted to hold rates at 0-0.1% and revised up its estimates of inflation and cut growth forecasts. Governor Ueda continues to dangle the prospect of more rate hikes to come, and an October hike remains Niall Ferguson’s base case. Still, JYP has fallen below 157 to the dollar, the weakest point in nearly 40 years. The risk of currency intervention remains high, but if the Finance Ministry steps in, the broad trend of slow yen depreciation seems set to continue. Niall remains SHORT the yen.

Edition: 185

- 03 May, 2024

Germany’s peace chancellor

Fearful of entering next year’s re-election campaign with a bleak economic track record, Chancellor Olaf Scholz is looking to boost his popularity. Niall Ferguson expects Scholz’s government to revise implementation of Germany’s debt brake to free up an extra €8 billion (0.3% of GDP) to spend in 2025. Niall also expects Berlin to top up its €100 billion defense fund by 2026 at the latest. In foreign affairs, Scholz is increasingly portraying himself as a ‘peace chancellor,’ whose priority is keeping Germans safe and avoiding escalation in Ukraine, not helping Kyiv win. This is a long-standing strategy of Social Democratic chancellors—but it is made more necessary by the rise of not only the far-right pro-Russian Alternative for Germany (AfD), but also the charismatic left-wing, pro-Russian, and anti-migration populist Sahra Wagenknecht.

Edition: 184

- 19 April, 2024

Inflation surprises

Recent data from the EU, UK and NZ show MoM inflation rising, possibly delaying anticipated rate cuts. It has panned out exactly as Craig Ferguson discussed months ago. The persistence of inflation will suppress economic activity in coming months, possibly hitting equity markets if ongoing corrections come true. The bond market is seeing a strategic shift towards longer durations in anticipation of heightened volatility. Craig adds 10yr macro bond LONGs across the curve and is adding USD Index, USD/JPY SHORTs; and AUD & NZD LONGs (against a strengthening USD) to his portfolio. His growth vs defensive is at 32/68%, with defensives including gold, alts, and extended bond duration.

Edition: 184

- 19 April, 2024

Mexico’s electoral countdown

With the two major presidential candidates now clear, Mexico’s election season has finally begun in earnest. Yet the outgoing president, Andrés Manuel López Obrador (AMLO), is reluctant to relinquish the spotlight. He is leaving his successor a toxic brew of rising debt, uncontained drug violence, a more powerful military and large unfinished infrastructure projects. Niall Ferguson expects whoever wins the election to attempt to avoid the capricious policymaking of the AMLO administration and swiftly address the country’s fiscal imbalance. Mexico’s potential as a site for US nearshoring remains, even as trade tensions between China and the United States are increasing the adoption of protectionist measures. He maintains his view that Claudia Sheinbaum will win the election and gradually distance herself from AMLO’s erratic policies afterwards.

Edition: 184

- 19 April, 2024

Building Product Distributors still offer plenty of upside

Industrials

Many market participants are looking for a way to play housing and it would be easy to look at building product distributors and write them off as being overvalued and that you’ve missed out. However, TRG believes this is faulty logic. Builders FirstSource, Beacon Roofing and GMS (as well as others) have margin profiles that have risen to comparable or superior levels in relation to the “premium-valued group” (SiteOne, Pool, Leslie's, Core & Main and Ferguson), but have EV/EBITDA multiples (avg. 10.6x) well below these stocks (avg. >20x). If they gain a more appropriate multiple (for strong SF starts and better margins) on higher EBITDA, then all three companies still offer significant (~70%) upside.

Edition: 183

- 05 April, 2024

Japan: Renewed optimism

The Bank of Japan started normalising its monetary policy in March, raising its overnight call rate to 0-0.1% from its negative lower bound of -0.1%. The first rate hike since 2006 followed wage increases and signals the BoJ’s increasing optimism that Japan is on course for sustained nominal growth and a virtuous cycle of price and wage increases. Given the Bank’s previously short-lived attempts to escape the zero-lower bound, Niall Ferguson expects any moves to be cautious, He expects a 0.25% rate hike by October, after which it will then be forced to pause by goods disinflation. Niall is neutral on the yen, given tactical risks from currency intervention, and is LONG Japanese equities.

Edition: 183

- 05 April, 2024

Europe: A defence renaissance?

Europe once had a large and advanced defence industry. Yet a deep and sustained decline in defence spending following the Cold War has severely diminished its capacity. To remedy the situation, Europeans need to raise defence spending, purchase more “made in Europe” arms, and reverse industry fragmentation. Niall Ferguson believes that on all three fronts there will be some progress over the coming years, notably by adopting a sizable debt-financed EU fund to support Ukraine and boost arms production. However, the reality is that the EU must continue to rely on the US as a security guarantor for the foreseeable future. The upside to going long European defence may be limited in the medium term.

Edition: 182

- 22 March, 2024