Fortnightly Publication Highlighting Latest Insights From IRF Providers

Company Research

Consumer Discretionary

Brian McGough reiterates his bearish view on FND despite the stock’s ~50% drop since his Apr 24 short call (vs. the S&P +33%). Brian is updating his analysis using his M.A.P.S. (Market Area Performance Study) framework, which tracks store performance by opening cohort. His latest findings suggest that stores opened in 2024 & 2025 are performing even worse than earlier cohorts, reinforcing that FND’s weak comps are structural, not cyclical. New units also show rising market overlap with the likes of Home Depot and Lowe's. While FND is often seen as a housing-recovery play, Brian expects another ~30% downside as earnings, growth guidance and unit expansion continue to disappoint.

Edition: 222

- 17 October, 2025

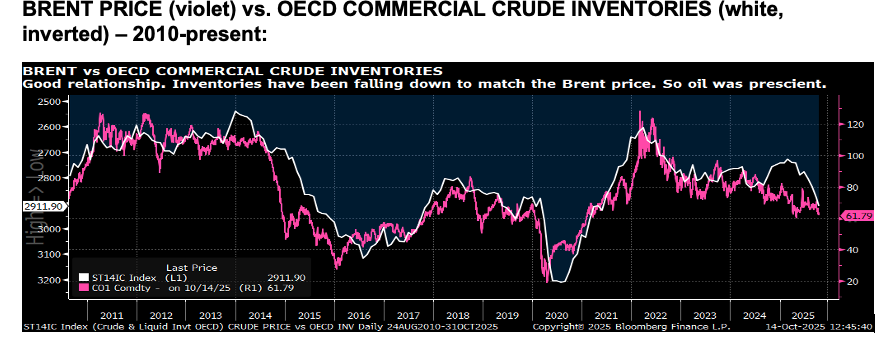

Oil: WTI to fall below $50/bbl?

Michael Churchill says if we are in an oil glut, one has to be open to the risk of oil falling below $50/bbl for WTI. Moreover, if Trump has made a deal with Arab leaders to keep that glut going, then there is no floor until some of the North American players lay down rigs or shut in production. Gas is less at risk for this kind of event since it is already so cheap relative to oil. Michael points out that if the new race for global power is focused around AI domination, it stands to reason that the old E&P elites will be gradually losing their power in geopolitics – particularly geopolitical moves meant to keep oil prices firm. Oil prices began falling in January, in anticipation of an increase in OECD crude inventories. Brent peaked at $82/bbl in January. Shortly thereafter (in February) OECD commercial crude inventories hit a low of 2.73b barrels. Since then, Brent has fallen to $62/bbl and OECD inventories have risen 5% to 2.91b barrels.

Edition: 222

- 17 October, 2025

China: A fragile improvement in PPI

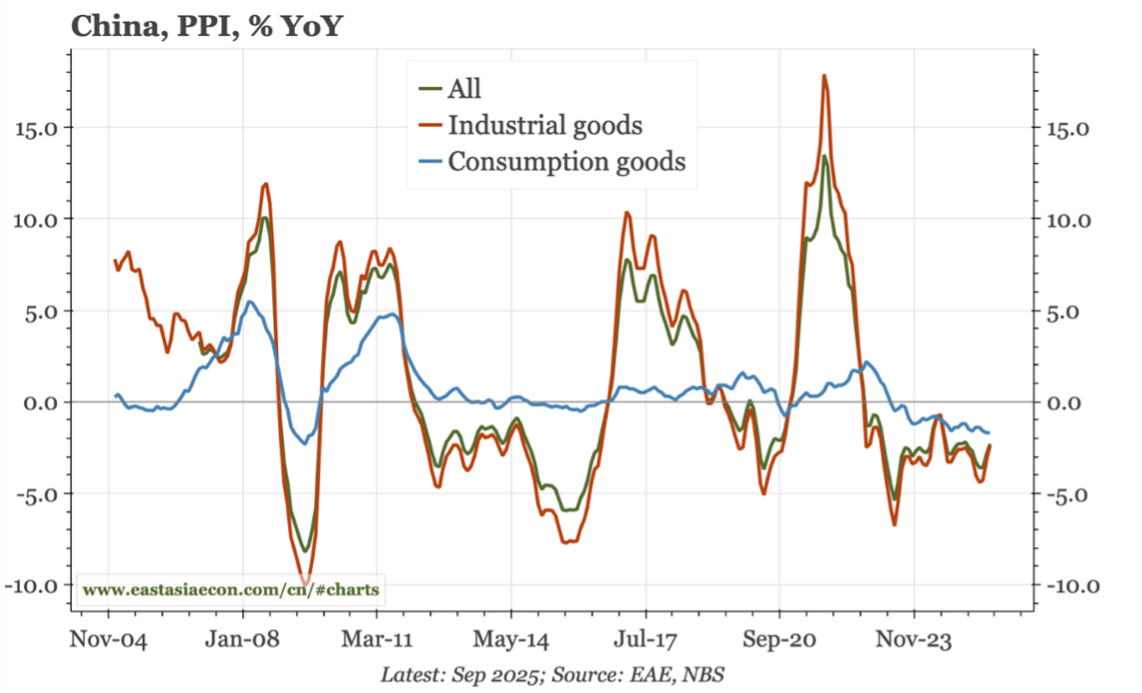

For the first time in more than a year, in level terms, the producer price index (PPI) has stopped falling; however, in year-on-year terms it was down 2.3%y-o-y (versus -2.9% y-o-y in August). That is an improvement, but one that looks fragile. Prices in auto manufacturing – one of the sectors targeted by the anti-involution drive – are falling more quickly than ever, and the "consumption" sector of the PPI in general shows no turnaround. Building material prices continue to be dragged down by the problems in the property market. The stabilisation in PPI is being driven by prices for "industrial" products, namely mining and energy. The short-term leads don't suggest much change in PPI in the next couple of months. But there is some upside risk coming from the YoY rise in global commodity prices (in CNY terms). Paul Cavey remarks that this would be more powerful for China if the construction cycle really finds a floor, allowing building materials prices to do the same.

Edition: 222

- 17 October, 2025

Iron ore: Uncertain markets

For now, volatility in China-centric industrial metals futures will be dictated by tit-for-tat trade measures and heightened risks of a global recession. That said, Atilla Widnell explains that inflation should also serve to push marginal cost iron ore producers higher up the cost curve; raising the cost floor and support for iron ore prices. At the same time, the seasonal expansion in Australian and Brazilian iron ore shipments should also serve to create a cap on prices throughout Q2. The great unknown is whether Chinese authorities will enforce government-mandated steel capacity reductions. If global trade measures remain in-situ, Atilla believes this increases the prospect of Chinese authorities revisiting expansive fiscal & monetary stimulus to defend the domestic economy. He maintains his medium-term outlook to US$95.70–107.84/t CFR China for Q2 2025. His short-term target is updated to US$94.12-95.62/t CFR China due to a potential stronger sell-off of ferrous metals markets and expanding arrivals of iron ore cargoes in Chinese waters.

Edition: 212

- 30 May, 2025

Is carbon markets’ demise hot air?

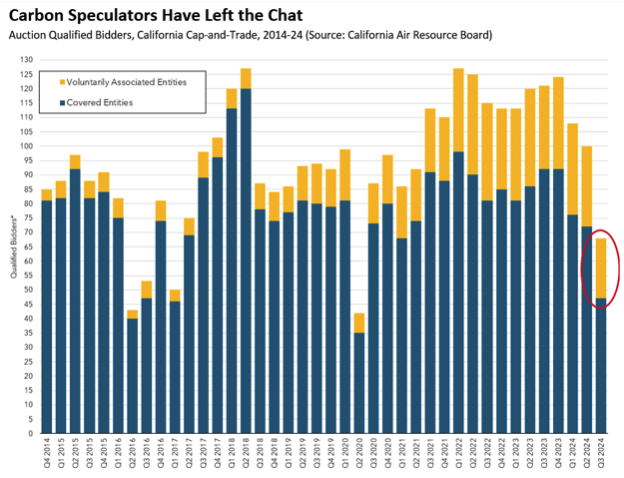

As Trump and populist parties rattle global carbon markets, many speculators have left the market in search of better returns. Recent market auction data from the California Air Resources Board (CARB) show a drop in the share of speculators compared to 2022-23 averages, pressuring carbon prices lower. But the Sustainable Market Advisors team sees investment opportunities, particularly in the Quebec-California market as prices are trading close to their regulated floor value and emissions targets in the regions remain ambitious. Many of the US’s big businesses are also reiterating their preference for keeping a price on carbon. Right now, there appears to be a good entry point for investors willing to take a long view on this asset class.

Edition: 208

- 04 April, 2025

China: Out with the old, in with the new

William Hess highlights two news items that have sent shock waves through Chinese social media and global markets. The first is the formal nationalization of Vanke, one of China’s largest developers, and the other is the emergence of DeepSeek, an open-source AI model from China. These two developments are relevant because they illustrate the continued divergence between the old and new economies in China. The former showcases Beijing’s resolve to avoid financial defaults for major developers, setting a price floor for old economy assets. This floor may be low, but it avoids the abyss. The latter reveals the upside potential for Chinese tech companies via a new generation of “late developer advantages”, meaning the ability to achieve competitive outcomes with binding budget and resource constraints despite the US tech embargo. Exciting times ahead.

Edition: 204

- 07 February, 2025

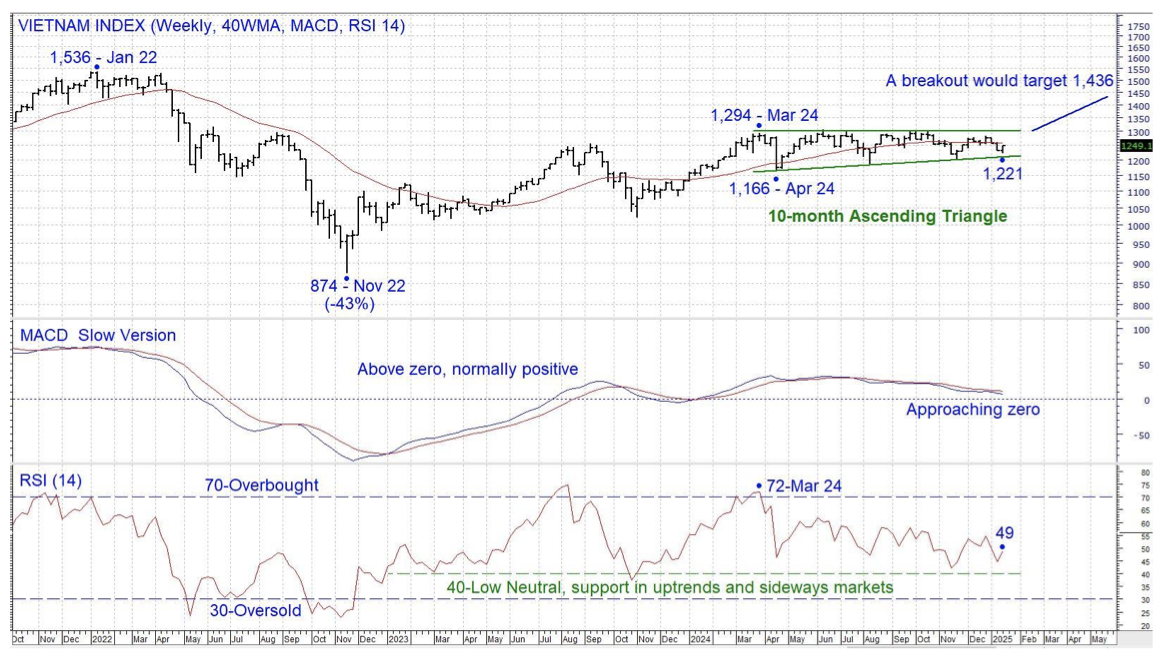

Vietnam: Breaking free?

The Vietnam Index first traded above 1,000 years ago but has since been unable to sustain a move away from that level. In 2022 the index peaked at 1,536, then fell by more than 40% in the same year. However, the short amount of time below 1,000 suggests that the market is converting the old ceiling into a floor. Since the March 2024 peak of 1,294, a potential 10-month Ascending Triangle has formed, a breakout would target 1,436, just below the 2022 peak. Chris Roberts will go 100% long on a weekly close above 1,330, using a daily close below 1,209 as a stop loss. His initial target is 1,436 and then a test of 1,500+.

Edition: 203

- 24 January, 2025

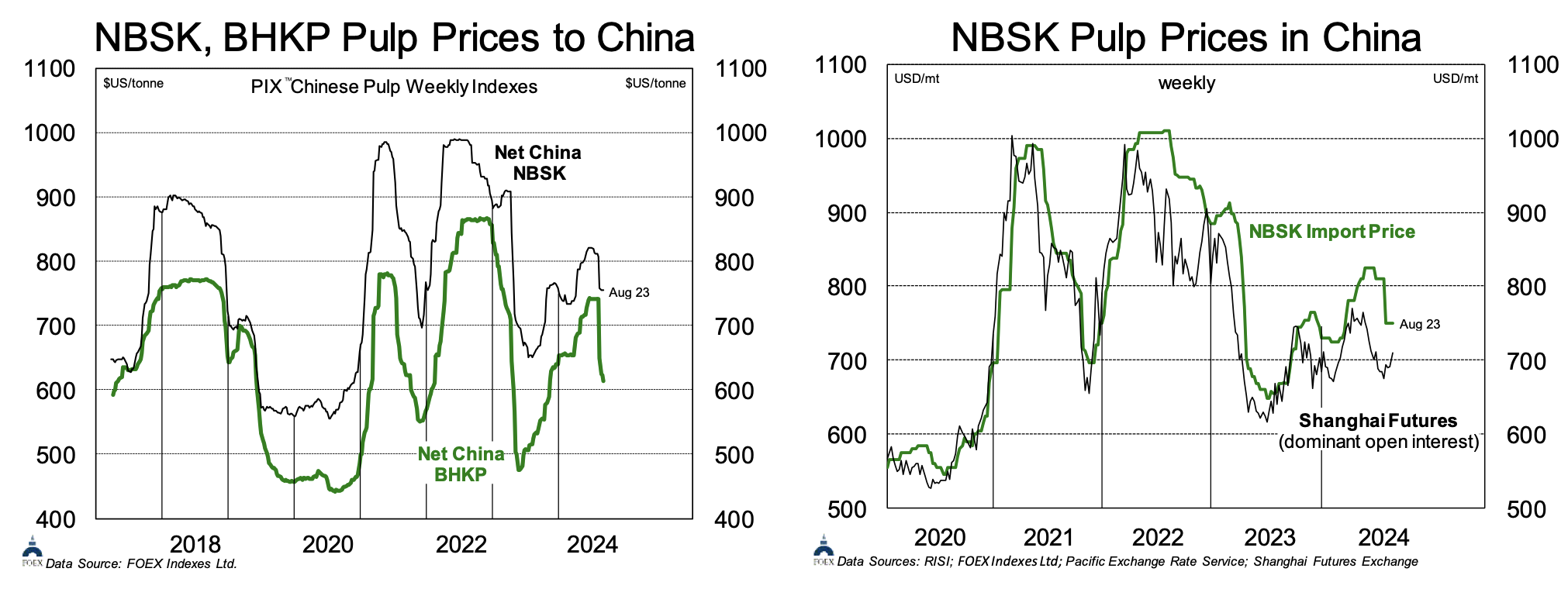

Pulp pricing floor approaching

After an exceptionally steep correction in late July/August, week-over-week price changes for both softwood and hardwood pulps slowed in China (chart 1). Shanghai NBSK futures had been falling for some time, but prices for imported pulp finally began to collapse in early August and have started to climb again (chart 2). The magnitude of the correction has accelerated the pulp pricing cycle and signs indicate that spot hardwood pricing is approaching its trough. For NBSK, the correction has been more gradual and shallower, and new threats to global supply should support pricing in the near term. With 2.0MMmt of mostly NBSK, Mercer is the team’s preferred route to pulp exposure. It is trading at a 3+ year low. While the company has a 2026 maturity to address, it reduced net debt by $45MM in Q2 and expects the same in Q3. The team’s $10 target reflects a 7.0x multiple on 2025E EBITDA of $272MM.

Edition: 194

- 06 September, 2024

China: Credit ratio high, M1 low

In the monetary and credit data for November, there’s no change from recent trends. Given this, the cyclical picture for the economy looks the same. The rise in government borrowing will probably put a floor under growth in the next few months, but there isn’t enough momentum in overall growth to think that the credit impulse is about to lift the economy. Yet despite weak credit growth, the credit ratio continues to creep even higher, now at an estimated 300% of GDP, despite Beijing’s key goal of deleveraging. The pronounced weakness in M1 suggests a continuation of the deflationary momentum into 2024. Having fallen for MoM for 12 of the last 16 months, China is on track to see M1 fall YoY, which would be unprecedented.

Edition: 176

- 22 December, 2023

Oil: The pendulum continues to swing

Economic sentiment with respect to the US remains fickle, the pendulum swinging between sanguine optimism and recession fears. Vandana Hari notes the impact on crude of the changes, with Brent and WTI being yanked up from 1-month and 3-month lows after Chairman Powell’s recent comments. Tensions in the Middle East continue to run high around the Israel-Hamas conflict and crude will maintain some fear premium as long as it drags on. Should there be an actual supply disruption, crude could well surge into the triple digits, but that is not Vandana’s base case scenario. The 3m b/d of OPEC/non-OPEC output cuts are set to run into the year-end and hold a floor under crude. Vandana is NEUTRAL sentiment for the near-term (to mid-Nov) and mildly BEARISH for H2 Nov – H1 Dec.

Edition: 173

- 10 November, 2023

China: The floor has gone

The outlook for a consumption-driven growth model in China looks lacklustre, claims Said DeSaque. Tough market conditions in lower tier cities will depress aggregate national home sales in 2023, despite the apparent return to normality in top tier locations. The removal of the national mortgage rate floor on a city-by-city basis has created an uneven funding environment across the country. It will lower household leverage as existing mortgagors engage in prepayments, which is bullish for financial stability, but it will ultimately be detrimental to consumption in the current state of consumer sentiment and labour market conditions.

Edition: 162

- 09 June, 2023

Oil: A strong floor ahead

The Marex team see prolonged overproduction as unlikely, with Russia likely to fall under Western sanctions similar to what occurred in Iran and Venezuela. If Russian production declines, the recent OPEC action and the potential for the US to refill its SPR will put a strong fundamental floor beneath oil prices barring a major recession. The Saudis appear willing to defend oil prices at all costs and could extend their July production cut indefinitely until prices rally back above $80 per barrel basis Brent.

Edition: 162

- 09 June, 2023

China Iron Ore: Sell in May, come back in October

Iron ore prices in China are a function of steel production in the short-term, credit growth and restocking in the medium-term and property new starts in the long-term, explains William Hess. He still expects a secular decline in the long run against a backdrop of falling property new starts, voluntary steel production cuts and substitution from increased scrap recovery. However, iron ore is currently oversold. Production rates are still relatively high and near-term credit growth will provide a floor for demand. William expects prices to rebound to USD 140 per metric ton before a major retreat to 90-100 per metric ton in late May.

Edition: 157

- 31 March, 2023

Liquidity Risk Model: Best short candidates

ChargePoint (CHPT) - Burns $400m annually, a figure which is rising fast. Expected to run through most of its cash balance by early to mid-2024. Forecasts expect sales to continue slowing. Not expected to breakeven until 2026.

Floor & Decor (FND) - Requires nearly immediate outside financing, primarily due to very high capex spending. Net debt $1.8bn (vs. $200m in 2018). Sales are expected to slow further during 2023.

Natera (NTRA) - Diagnostics company will run out of cash by Sep having burned $700m+ in the past year. Not expected to breakeven until at least 2028. Trades at 5x 2023 and 2024 sales.

Edition: 155

- 03 March, 2023

Fight the tape or the Fed?

The market narrative is shifting to one of no recession and continued growth. As well, global liquidity is putting a floor on the price of risky assets, but at the same time the FOMC warned that a restrictive policy stance would have to be maintained. So, should investors fight the tape or the Fed? Edward Pennock believes the answer lies with investment time horizon. In the short-run, liquidity controls the tape. In the long-run, valuation and interest rates matter to returns. For now, European stock and cyclical industries are the leadership. Enjoy the ride and take shelter if their leadership falters.

Edition: 155

- 03 March, 2023

Consumer Discretionary

Created a niche specialisation in flooring that no competitor can come close to matching - has done so using a scale economy shared model, and as a result now looks to have a long runway of growth ahead. During the last decade sales are up 29% p.a. and EBITDA +35%. Comparable store sales averaged growth of 14.5%. Market share has grown from 1% to 8% and is targeting 33%. $17bn of sales at a 16% EBIT margin gives EBIT of $2.7bn / net income of $2.04bn. A 20x multiple of this figure results in a M/Cap of $41bn (vs. $9.4bn today), that gives an investor IRR of 23% over 7-8 years (capital appreciation only).

Edition: 143

- 02 September, 2022

Consumer Discretionary

R5's research reveals BBY’s business model is suffering from potential systemic challenges around its go-to-market strategy. Specifically, its high-touch showrooming model is under siege, in large part, due to an unprecedented crime wave impacting its stores. Management’s reaction has been to remove product from the floor or lock it up, transforming many stores to go from a showcase to a rather empty, uninspiring experience. This, in combination with flagging demand, deteriorating store conditions and supply chain challenges, leads Scott Mushkin to downgrade the stock to Sell.

Edition: 141

- 05 August, 2022

China: Old habits die hard

Beijing’s focus in 2022 is stability. Niall Ferguson expects China to announce a GDP growth floor of around 5% YoY in March, which will require more fiscal and monetary stimulus. The more that Beijing’s “zero-COVID” policy, export slowdown, and real estate deflation slow growth, the more the central government and the PBoC will turn on the fiscal and monetary spigots. Niall predicts a pick-up in infrastructure investment, looser credit conditions, and two more RRR cuts in 2022.

Edition: 127

- 21 January, 2022

Technology

US SaaS company issued USD 300m 0.25% 2026 senior convertible bond with 37.5% premium. Despite the low bond floor, delta is 54 with positive yield, and top line sales have grown by 31% CAGR. This growth company has little operating history but the demand for their services is robust as many small retailers are shifting their business online. BIGC can provide a suite of services. Mean stock target price is USD 74.64 or +31% upside.

Edition: 119

- 17 September, 2021

West Fraser (WFG CN) Canada

Materials

Lumber prices have corrected sharply after reaching $1600+ in Q2, but historically high prices will persist for at least another year. Market downtime in BC (cost related) should keep the price floor high (~$600) for several quarters, benefitting producers in other regions (73% of WFG’s capacity is ex-BC). Prices may trend sideways for the balance of Q3 as supply chain inventories adjust, but ERA Research expect a strong seasonal trade (late-Sept to May) as R&R demand recovers and housing remains robust. TP C$140 (55% upside).

Edition: 116

- 06 August, 2021

Canadian Oil & Gas

Even with recent OPEC+ news, Veritas Research expects the global oil market to remain undersupplied until 2021’s end, with a floor of $60 per barrel through 2022. With this low case, the setup for Buy Rated Oil Sands Producers is attractive, with Canadian Natural Resources, Cenovus and Suncor all attractive options (FCF Yields of >15% and Net Debt/FFO <1.0x).

Edition: 115

- 23 July, 2021