Fortnightly Publication Highlighting Latest Insights From IRF Providers

Company Research

Saint-Gobain (SGO FP) France

Industrials

Following publication of its FY24 registration document, Iron Blue increases their SGO score to 27/60 (newly top quartile). This principally reflects FY24’s P&L benefit from compression in the expense for inventory and bad debtor impairment provisions, which could provide a tough comp effect in FY25. They also note two new contingent liabilities related to a new Grenfell Tower claim brought against SGO subsidiaries as well as assumed Australia asbestos liabilities with FY24’s CSR acquisition. For the first time the FY24 annual report quantified SGO’s reverse factoring activities (€106m). Iron Blue continues to flag sustained stripped out costs and an elevated gap between PPE capex and the P&L depreciation charge.

Edition: 223

- 31 October, 2025

Access to proprietary short-availability data

As many quantitative researchers know, reliable historical short-availability data, especially intra-day, is notoriously difficult to obtain. Recognising this gap and leveraging the accessibility of real-time market feeds, Capital Systems began recording real-time short-availability data for all US equities in Aug 23 and for all USDC-denominated cryptocurrencies on the Binance exchange in Jun 24. The data is of particular use in two areas: 1) Reducing assumption bias in short-selling strategies, especially for hard-to-borrow securities. 2) Alpha capture. Why would Capital Systems share such an edge? The firm trades only a small fraction of the markets it monitors, allowing them to offer this unique dataset on a limited basis to select clients.

Edition: 222

- 17 October, 2025

Technology

Could the stock soar over 100%? KCR argues that CSCO isn’t just cheap vs. AI peers - it is cheap relative to the broader market, trading at roughly the same multiple as Kimberly-Clark despite far stronger growth. Networking product orders have risen 10% Y/Y for 4 consecutive quarters, suggesting investor concerns about a slowdown are unwarranted. Meanwhile, the company’s rapidly growing exposure to AI infrastructure products and shift towards subscription-based revenue both support multiple expansion. CSCO trades at one-third of Arista Networks’ P/E multiple and one-quarter of its EV-to-revenue ratio - even a modest narrowing of the valuation gap would translate into substantial gains for CSCO shares. Finally, a ~5% FCF yield is far too high for a company of CSCO’s quality.

Edition: 222

- 17 October, 2025

How will China monetise AI differently?

China will be a close and capable AI follower, focusing on downstream implementation as the US focuses on upstream. This means the two will not run head-to-head encounters right away, and China can lead in the application of AGI in manufacturing and logistics. Its monetisation path will be more complex but can exist. However, as it stands, China is under-monetising AI vs the US. The Blue Lotus team estimate that consumer (2C) AI applications generated $2.0–3.5bn in the US and $0.3–0.5bn in China (excluding AI-enabled advertising and much of video AI). The US monetises AI globally, with global 2C revenues bringing in ~12x that of China. However, the gap will shorten significantly by 2030, in part by taking a lead on robotics+AGI. The team reiterate their top picks of Alibaba, Hesai, CATL and Kuaishou. Baidu stays as a sell.

Edition: 221

- 03 October, 2025

Something to Snack On: Amazon (AMZN) Drills Lowe's (LOW)

Consumer Discretionary

Amazon ran steep tool discounts over the holiday, highlighting Lowe’s pricing disadvantage. Across 25 items from brands like Bosch and Dewalt, Lowe’s averaged 27.5% higher prices; 15 items were cheaper on Amazon with average discounts of 34.6%, while only one was cheaper at Lowe’s. This follows R5's year-long observation that Lowe’s prices exceed Walmart’s on common goods. The wide gap raises concerns about Lowe’s gross margins and potential sales/earnings headwinds, even if housing improves. Meanwhile, Amazon’s aggressive pricing supports volume growth and advertising profits—a positive for AMZN but a structural challenge for broader retail.

Edition: 219

- 05 September, 2025

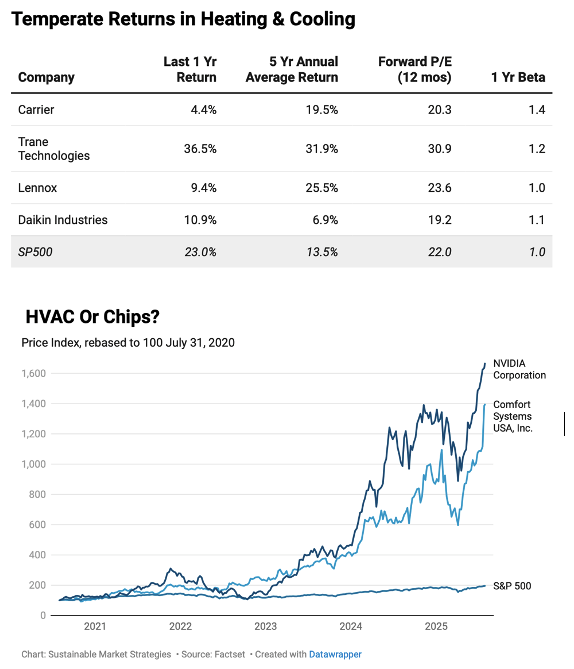

Hot picks for the heat economy

Heat pumps are the go-to solution for building space cooling (and heating), and the Sustainable Market Strategies team expect the bull market in HVAC companies to continue even in the face of subsidy removals. The IEA expects 1.5bn more air conditioners in operation in 2025 than today, driving the need for energy efficient solutions. Heat pump improvements aren’t just good for reducing emissions, they’ve been good for portfolio returns; just take a look at Comfort Systems, which some could mistake for super star Nvidia (see chart). Sure, this performance does stand out among HVAC players, but others have also done well (see table). The tech will become only more important in use cases like food refrigeration and data centre cooling, so demand will see sufficient growth. When it comes to cooling solutions for the data centre boom, look to US companies to fill this gap.

Edition: 218

- 22 August, 2025

Brazil inches towards settling down

Real growth has held up well, but Jonathan Anderson points at general signs of weakening in underlying activity data. Inflation numbers have peaked across the board and should be fading in the second half. And fiscal consolidation has been very visible on an annual basis. In this environment, both real rates and the rates/growth gap remain extraordinarily high - keeping BRL carry attractive and making eventual rate cuts the dominant theme of the coming 12 months. There are two trends to watch that could potentially impede the carry/easing trades: one is widening external deficits, and the other is apparent recent budgetary slippage. Stay tuned.

Edition: 216

- 25 July, 2025

What’s trending in Retail

Consumer Discretionary

Each week, The Retail Tracker offers an insightful perspective on retail, fashion and consumer trends and what it means for the stocks. So far this year, Garage is a standout, nailing the “sexy x comfy” aesthetic for teens and taking share from Aerie and Pink. Gap and Old Navy are “crushing it” with consistently strong assortments, offsetting tariff challenges through fewer markdowns. Meanwhile, Urban Outfitters and Nuuly are gaining traction, with Nuuly emerging as a promising rental and tech-driven play. Aritzia is showing good momentum with its best assortment in some time. Department stores may be in free fall, but the best Macy’s stores have never looked better. In contrast, Lululemon is losing its way, expanding beyond its core and diluting its brand identity, while Bath & Body Works' range of new items is exhausting.

Edition: 214

- 27 June, 2025

Brazil: Maintain long equity exposure

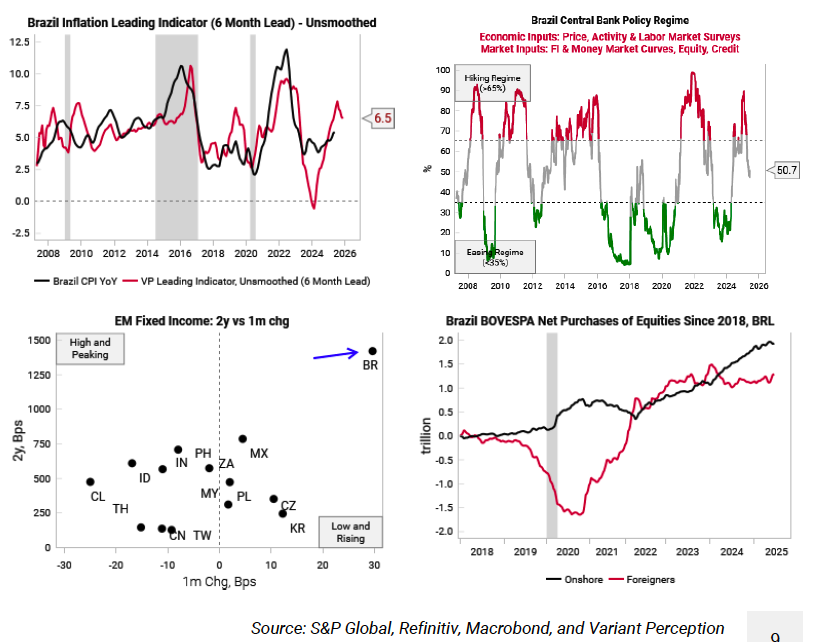

Variant Perception’s inflation leading indicator ticked down again this month, with the unsmoothed 6-month estimate falling to 6.5% YoY (top left chart). Underlying indicators confirm this inflection point, leaving the gap between the Selic rate and inflation the widest since 2005. Brazilian money market futures have also priced in the end of the hiking cycle. Echoing this, the team’s central bank regime model has shifted out of a “hawkish” regime and is now in neutral territory (top right). Meanwhile, the 2-year bond yield in Brazil remains elevated relative to all other EM economies (bottom left). The latest rise in yields over the past month or so is at odds with evidence inflation is rolling over. Investors can expect some lagged negative effects from the tightening cycle, but falling real interest rates are a strong macro setup for domestically-exposed Brazilian equities to move substantially higher from here.

Edition: 214

- 27 June, 2025

US: TINA and Treasuries

Andrew Hunt asks: has EZ deficit obfuscation helped maintain US Economic Exceptionalism? He believes it has and that the hurdle for US balance of payments problems is in fact quite high. Unlike its peers, the US is an economy with a positive output gap, strong credit growth and it is experiencing above trend growth at present. The Fed’s current rate strategy is therefore right for the moment, but this strategy will not suit others. The crowded short USD position may not therefore work for a while… US households are long equities but a shift to a fully or overfunded budget deficit would ask questions of their current asset allocation. Ultimately, the outlook for markets rests on two questions: how will the US budget deficit be financed and can the news flow actually overwhelm the TINA effect and lead foreign investors to reduce their acquisitions of USD assets?

Edition: 214

- 27 June, 2025

China: Overblown concerns

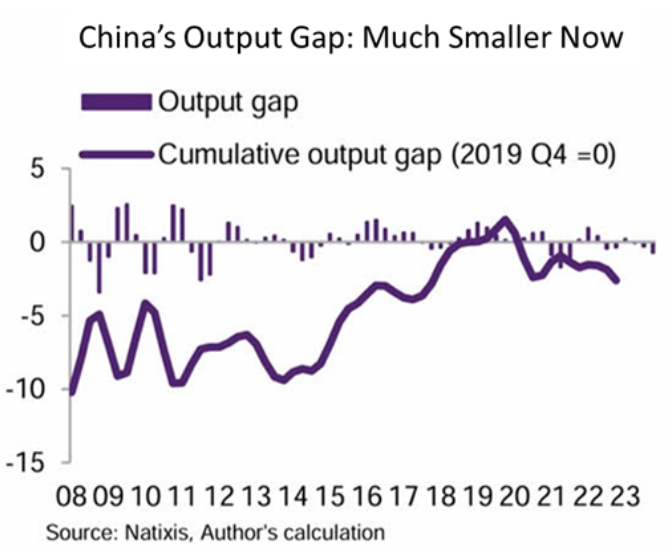

Manoj Pradhan points out that China’s fiscal support started last September, with stimulus starting before the Trump threat even materialised. Stabilising the property sector is a must for releasing consumption, with the ban on mortgage refinancing and falling house prices being some of the biggest reasons for the country’s ailing consumption. Manoj claims that concerns about China being a source of persistent deflationary demand are overblown, with the structural inflection occurring instead over 2012-15. He points to research estimating that China’s output gap over 2012-15 was nearly four times the size of the output gap in the recent downturn (see chart). China is also set to gain more than the US from de-escalation in the trade war. Stay long CHN.

Edition: 213

- 13 June, 2025

What ails JGBs

The MoF understandably believed that it was being prudent by trying to bolster Japan’s fiscal reserves over recent weeks. However, this overfunding of the deficit, on top of the BoJ’s QT, a weak net external counterpart to liquidity growth, and against a background of only modest JGB demand from the banks, has placed upward pressure on yields and crashed monetary growth when the real economy is already softening. High food prices are inflationary to the CPI but deflationary for growth. Andrew Hunt finds that Japan now possesses a small negative output gap for the first time since the pandemic. Given these trends, investors can expect the MoF/BoJ to conduct a further policy U-turn despite high price rises. Andrew suspects that the BoJ’s actions will soon lean more doveish. Indeed, he says Japan’s shift from over-funding to under-funding could occur as the US Treasury begins its own heavy issuance later this summer, ultimately favouring the USD.

Edition: 213

- 13 June, 2025

Ferrovial (FER SM) Spain

Industrials

Ernesto Lopez Mozo (CFO since 2009) acquired €224k of stock at €44.93 - only his second buy despite a long tenure. His first was €129k at €25.88 in Feb 20, making this latest move notable for both its larger size and higher price, after a gap of over five years. Rafael Del Pino Calvo-Sotelo (Chair since 2009) also made a rare €1.8m buy in Mar 25 at €37.17. Both are encouraging insider signals with shares near all-time highs. Meanwhile, Luke Bugeja (Divisional CEO since 2021) sold €929k worth of shares on the same day, which matches a stock award in Mar 25. This aligns with 2024, when he also sold his full award. The sale is not concerning enough to offset Smart Insider’s positive view.

Edition: 212

- 30 May, 2025

Shell: To Be(P) or not to Be(P); that’s the question

Energy

Analysts at the IDEA! weigh in on media speculation about a potential Shell acquisition of BP. While Shell has the financial strength to pursue a deal, acquiring BP would involve taking on its $77bn of debt and other long-term liabilities, including those from the Deepwater Horizon spill. Although synergies are possible, integration would be costly and could disrupt Shell’s shareholder returns, which is key to closing its valuation gap with US peers. The deal would also bring in non-core assets and regions Shell has been moving away from, along with notable cultural differences. the IDEA! suggests caution and favours Shell sticking to its current strategy or exploring other deals instead.

Edition: 211

- 16 May, 2025

WPP (WPP LN) UK

Communications

Following publication of its FY24 annual report, Iron Blue increases their WPP score by 3pts to 30/60 (now top decile; fertile grounds for shorting). This reflects: 1) Higher stripped out costs (41% of PBT adj vs. 30% in FY23). 2) Re-expansion of the gap between accrued income and deferred income after narrowing the previous two years. 3) Another fall in balance sheet bad debtor impairment provisions. 4) Compression of trade receivables. 5) Reduced disclosures in several areas following change of auditor. 6) Moderated CEO LTIP ROCE and FCF targets.

Edition: 210

- 02 May, 2025

Healthcare

Following publication of its FY24 annual report, Iron Blue increases their CTEC score to 28/60 (top quartile / fertile grounds for shorting). Reductions in inventory & bad debtor impairment provisioning contributed 36% of FY24’s Y/Y rise in PBT adj while the trend of restructuring and asset impairment provisions strip outs continued. The gap between PPE/software capex and the P&L D&A charge narrowed Y/Y but remained elevated at 16% of PBT adj. Receivables factoring increased to $43m (FY23: $27m, FY22: nil) while working capital days outstanding compressed to a decade low 47 days (FY23: 57), implying risk of future mean reversion. CTEC lowered the discount rate used to impairment test its goodwill to a blended 10.3% from 13.3% in FY23. This is now below the 11.5% average for Iron Blue’s coverage universe.

Edition: 208

- 04 April, 2025

Special Sits Idea Forum

MYST’s latest buyside event saw a large group of investors offer a diverse set of ideas spanning various sectors / themes. Stocks highlighted include:

Bayer (BAYN GR) - New management advancing turnaround as litigation resolution approaches. TP €40 (65% upside).

CRH (CRH) - Increased pricing power + Ukraine rebuild opportunity to narrow valuation gap vs. peers. TP $135 (35% upside).

NFI (NFI CN) - Earnings / margins to rebound sharply as production issues ease. TP C$40 (200% upside).

Paramount Global (PARA) - Pending deal approval to trigger “structural bid” from Arbs while streaming business inflects. TP $15 (30% upside).

Parkland (PKI CN) - Substantial SOTP upside amid ongoing strategic alternatives process. TP C$54 (45% upside).

Edition: 207

- 21 March, 2025

Japan: Throwback to 1987?

Japanese demand pressure increased even as the economy shrank late last year, and supply side potential remains moribund. The wage/price spiral should therefore continue unless global events lead to a deeper slowdown in demand trends / sharp rise in the JPY. Over the long-term, Andrew Hunt continues to believe that Japan will inflate its way out from under the public debt burden and that the JPYUSD is headed for Y200, but currencies are a relative game and he fears that markets could soon see a “repatriation rally” in the JPY that sees it gap higher in a counter trend move as it did in Q4/1987 and Q4/1998. Any upward move in the JPY would scupper the BoJ’s tightening plans. Could JGBs be viewed as a safe haven for returning funds? In real terms, equity prices are elevated – will they be eroded by inflation as they were in the 1970s, or by asset price deflation? Andrew expects more of the former than the latter.

Edition: 206

- 07 March, 2025

The quiet signs of a market top

Bull markets rarely die with fireworks. Instead, remarks Jawad Mian, they fall in a slow, unravelling process. The reason is simple, not all sectors and styles peak at the same time. Looking at thirty bull-market tops since the mid-1920s, the average gap between the first sector peak and the final high has been seven months. A market can stop being a bull market long before the index starts to fall. Jawad recalls the strategy of Jesse Livermore in 1916, who noticed the signs of the market falling one after the other even as the bulls raged around him. A hundred years later, the game–and human nature—remains the same. Investors have been roaring bulls, but, like Livermore, they’re now watching for the shift. And it’s happening.

Edition: 205

- 21 February, 2025

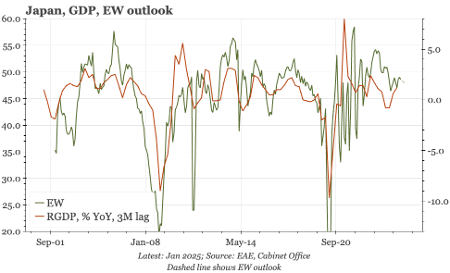

Japan: Wages support surprisingly firm consumption

Paul Cavey points out that the first estimate of Q4 GDP was solid, with growth of 2.8% QoQ annualised, much faster than market expectations of a 1% rise. That takes average growth in the three quarters from April 2024 to 2.5%, closing the gap with the growth path suggested by the Economy Watchers survey. RGDP is now once again back above the pre-pandemic level – though as that was now almost five years ago, this comparison shows how slow the economic recovery has been. The big driver of the strong result in Q4 was net exports, which on its own would have generated GDP growth of 3% annualised. While exports were strong, more surprising was the resilience of consumption in Q4. On a per capita basis, private consumption is now the highest since 2014.

Edition: 205

- 21 February, 2025

US-EU tariffs: This is going to get bad

Donald Trump's tariffs on Canada should be a worrying premonition for what will happen to us in Europe. According to Wolfgang Münchau, the most straightforward reason for the tariffs on Canada is that it allows Trump to raise revenue without going to Congress. If he can make the executive orders stick legally, it’s one of the few tools he will have at his sole disposal. The tariffs on Canada cast doubt on the possibility that the EU will be able to escape or cut a deal to rebalance the trade relationship. In the longer term, there could be disintegration of the collective west, as trade restrictions now put Europe in the same position as China. Trump also signed an executive order mandating independent assessments of the economic costs of regulation, and a net reduction of those costs – expect this to massively widen the transatlantic growth gap.

Edition: 204

- 07 February, 2025

US: Output gap is expanding

Growth may have faltered towards the final weeks of 2024, but in general the last 4-5 months of 2025 witness faster growth than in H1/2024, which Andrew Hunt puts down to being initiated by the wider fiscal deficit. This faster growth looks to have been associated with an expanding positive output gap, suggesting that inflationary pressures are building. These are cyclical and would evaporate if the economy slowed. Real yields in the UST market will continue to be determined by government borrowing trends and their interaction with the banks’ debt monetisation activities, but the nominal inflation component of yields could increase over the coming months unless / until the economy softens. Unless the US returns to QE imminently, yields will rise over the next 5-6 months, or at least until the credit boom ends. Andrew adds that, right now, liquidity is all that matters for US asset prices.

Edition: 203

- 24 January, 2025

Zalando (ZAL GR) Germany

Consumer Discretionary

Iron Blue initiates coverage on ZAL with a score of 28/60, which is top decile (fertile grounds for shorting) and an outlier compared with bottom decile/quartile scores of internet peers Auto Trader (13/60), Rightmove (11/60) and Scout24 (16/40). They highlight 1) Increased use of stripped out restructuring and other costs. 2) Stripped out share-based payments (27% PBT adj). 3) Profit recovery supported by compressed fulfillment, marketing and inventories provision expenses. 4) Pronounced gap between tangibles capex and the depreciation charge. Re. governance, they note CEO variable pay targets that are either undisclosed or below external targets, a non-independent Remuneration Committee and sizeable related party transactions. FY24 sees a change in auditor following the incumbent’s tenure of 13 years.

Edition: 202

- 10 January, 2025

Kone (KNEBV FH) Finland

Industrials

Iron Blue initiates coverage on the stock with a score of 27/60, which is top quartile (fertile grounds for shorting) and their equal highest score in the Capital Goods sector. They highlight 1) Reliance on percentage-of-completion revenue recognition. 2) Sustained stripped out restructuring charges. 3) An ageing debtor book (China construction). 4) Widened gap between capex and depreciation. They also note governance out of line with best practice (elevated non-audit fees, non-independent chair, board & remuneration committee and narrow CEO variable compensation payout metrics) as well as many areas of imperfect disclosure.

Edition: 201

- 13 December, 2024

Consumer Staples

KCR highlights the uncommon relative value available in blue-chip staples stocks. The data is clear: today is one of the best times in 30+ years to buy select names in the sector and KMB appears to be a stock with rapidly improving fundamentals which investors have overlooked. It trades at ~18x projected 2025 earnings, a 10% discount to the S&P 500 and a ~25% discount to peers, despite the strong and consistent earnings and cash flow growth it has reported over the last eight quarters. KMB also trades at a substantially lower multiple of P/FCF (16x vs. 23x-41x for Clorox, Colgate-Palmolive and Procter & Gamble), while offering a materially higher dividend. If the 6x-7x P/E multiple gap were to be cut in half, KMB’s share price could be revalued higher by ~$25.

Edition: 200

- 29 November, 2024

Nope, still no flood of Chinese goods

Once again China is posting a strong trade surplus and the news flow is all about mainland exporters rushing to ship goods to the US in advance of US tariffs. The reality, according to Jonathan Anderson, is that Chinese exports are broadly flat and just in line with the rest of EM. The true explanation behind high trade surpluses is a big "import crunch"; Chinese import spending has fallen well below the EM-wide trend in recent years...and the gap is increasing. China's merchandise trade surplus is embarrassingly high at roughly US$1 trillion - but the "basic" BOP balance is much lower, less than US$300 billion, and this is the figure that matters for Chinese macro policy. China has been and will continue to restrict imports and other outward spending by all means possible.

Edition: 200

- 29 November, 2024

Consumer Discretionary

The company is moving forward with an energy and confidence that has not been seen in a very long time, according to analysts at The Retail Tracker. Despite a lacklustre share price performance YTD, the Gap brand has been showing improvements, while recent collaborations have also impressed. Old Navy looks great. It had a very good BTS and its relaunch of denim with a powerful message was excellent. The ramp up in marketing will only help. Meanwhile, Banana, which had pushed pricing and design too far, seems to be settling back. Although Athleta continues to lag, the stores are cleaner and when they drop a new line, or colour, it is selling. They expect the stock to move higher over the next few months as GAP continues to gain momentum.

Edition: 199

- 15 November, 2024

Bank Negara (BBNI IJ) Indonesia

Financials

Galliano's Financials Research

BBNI is Victor Galliano’s top pick among the Indonesian banks, based on its compelling value and growth credentials. It has the lowest PEG ratio of the big four, undemanding prospective PE multiples and the best PBV ratio to ROE combination. Return trends continue to improve; pre-provision returns have risen after bottoming out in 3Q23, which combine with declining cost of risk to drive better post-provision returns. In addition, the bank’s efficiency ratios have begun to improve. With its CET1 ratio of 19%, BBNI has bridged the gap with Mandiri on capital adequacy and on credit quality it also has the second highest NPL coverage of its peer group, after Permata.

Edition: 199

- 15 November, 2024

India: Diwali bonus

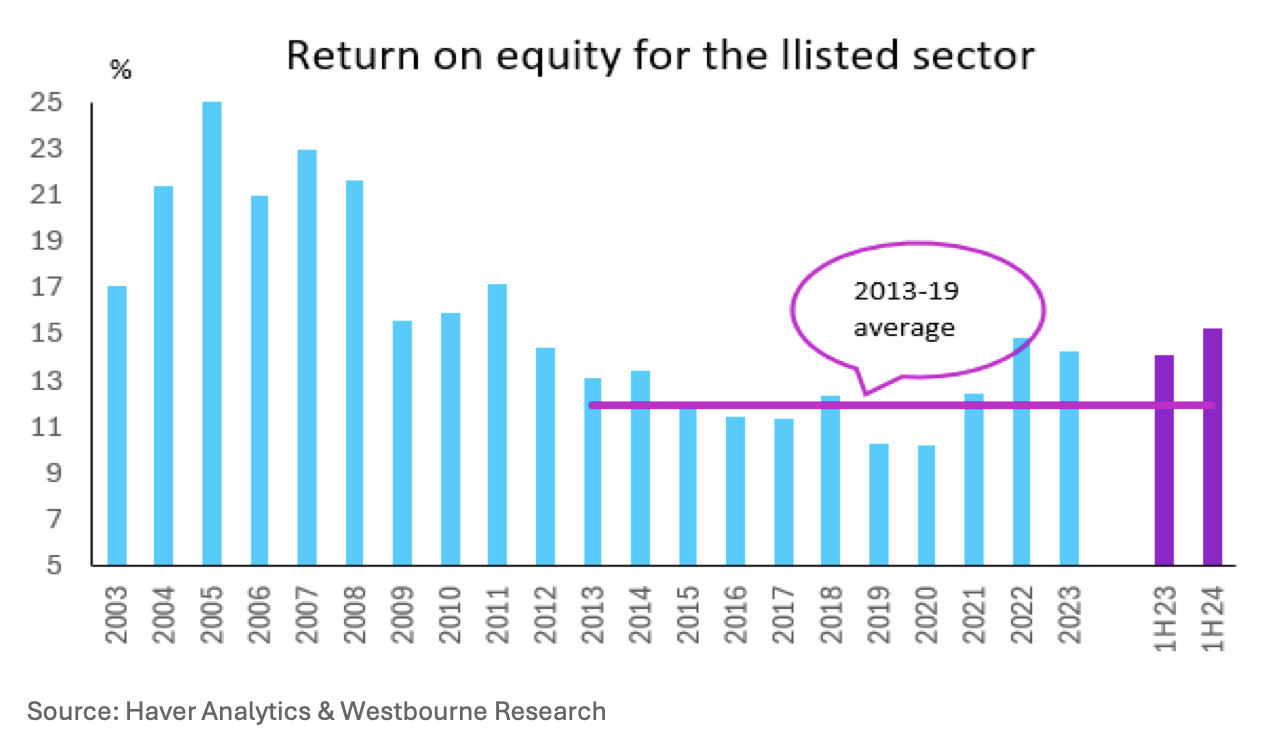

Sharmila Whelan’s latest report dives deep into India’s economy. Business cycle indicators are positive, indicating gathering momentum in the economic upswing, with return on equity climbing robustly since the low point in 2020 (see chart). Even though policy rates are high, the real cost of capital remains low. Private capex is rising and the government is pouring money into infrastructure investment. It’s just a matter of time before the investment cycle goes into full upswing. With the tough structural reforms now over (unlike in China), India represents a multi-year investment story for the foreseeable future. Sharmila recommends overweight Indian equities across industrial sectors and government and corporate bonds, unhedged. Rates are expected to stay on hold in 2024. Coupled with a positive economic outlook, robust corporate earnings, responsible fiscal policies, and a favourable adjusted resource gap, support an unhedged FX position.

Edition: 198

- 01 November, 2024

Communications

Shares of NTT have slumped this year as concerns on mobile performance and local exchange profitability weigh on sentiment even as regulatory and political uncertainty lingers. At the company’s recent IR day, management was able to address the former, focusing attention on improvements in mobile and its regional businesses although we will have to wait for the politicians and regulators to address the latter. Large-cap telecom peers have performed much better than NTT, which has expanded the valuation gap with NTT looking much more attractive at 11x FY24e EPS vs. KDDI (14x) and Softbank (17x). NTT has also increased its dividend 12 years in a row and Kirk Boodry does not expect it to stop now. TP ¥207 (40% upside).

Edition: 196

- 04 October, 2024

Consumer Discretionary

Janet Kloppenburg is encouraged that product assortments at Old Navy and Gap remain highly innovative and very competitive in Q3 which should support market share gain. At Old Navy, BTS demand strength last month is being followed by wardrobing needs for both women and men, with particular strength in wear to work and outerwear. Furthermore, Gap’s Get Loose denim campaign has been well received and is attracting a younger demographic, a major initiative in its strategic brand repositioning. Janet is also very impressed with the brand’s elevated fashion focus. Similar to Old Navy, Gap’s promotional activity is tracking lower Y/Y. She forecasts $0.61 Q3 EPS and $2.00 for FY24, both well above consensus.

Edition: 195

- 20 September, 2024

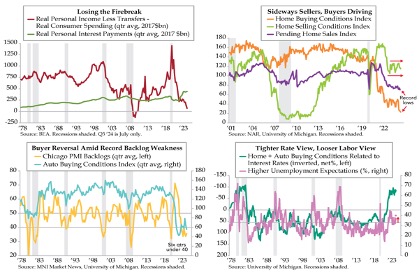

US: Consumer vulnerabilities rising

According to Danielle DiMartino Booth, the gap between the source of US consumer spending and the act itself is closing rapidly in 2024. Downside risk to elevated interest payments against this backdrop raises redder flags for household balance sheets given the decimated aggregate saving rate. Record low home buying conditions and 2024’s abrupt reversal in auto buying conditions suggest household budgets are reaching a critical point, especially as it relates to the sensitivity to interest rates. The Fed’s stubbornly tight policy risks a further deterioration in unemployment expectations. Vol is cheap.

Edition: 194

- 06 September, 2024

Consumer Discretionary

Gordon Haskett Research Advisors

Ahead of the print, GHRA upgrades the stock to Buy and raises their 2Q24 SSS estimate to 4% (vs. guidance of 0%-2%), driving total sales growth of 12.7% to $2.4bn and EPS of $1.00. GHRA’s footfall data has inflected higher on a both a one and two-year stacked basis, while QTD traffic through the first two weeks of 3Q24 has stayed strong (Aug > Jul). Longer-term, they expect BURL's 2.0 Strategy to drive improved comps and margins. The company can close the performance gap to peers and while sceptics will argue that this expectation is largely reflected in the stock and valuation, GHRA thinks investors should barbell higher quality retailers with some turnaround / defensive characteristics to increase alpha.

Edition: 193

- 23 August, 2024

Fraport (FRA GR) Germany

Industrials

Near-term tariff rises at Frankfurt are insufficient to close the gap to its Allowed Reg. Return. Robert Crimes sees Aviation Returns (NOPAT/RAB) of only 3.1% in 2024E and 2.9% in 2025E, c.320bps below Insight’s WACC of 6.2%. In addition to insufficient tariff rises, there are 3 key factors to consider: 1) Weak traffic recovery (lowest of EU peers). 2) High wage rises above inflation (Frankfurt staff costs to rise c.€150m (+19%) in 2024-25E). 3) High expansionary capex. Robert has a Sell rating on the stock given the average upside of Insight’s Global Infrastructure coverage is significantly higher at nearly 100%. Buy rated peers include Aena (TP €369), ADP (TP €234) and Flughafen Zurich (TP CHF330).

Edition: 193

- 23 August, 2024

Technology

Despite its small size (¥76bn M/Cap), ESPEC dominates the environmental testing industry in Japan with a 60% domestic market share and a 30% global share. Environmental testing is often mandated by international standards, as well as national and industry regulations, and product development companies must conduct it. Thus, the company supports pretty much all new product launches. For this global niche status, ESPEC trades at a P/E of 14.3x and P/B of 1.3x. Its dividend yield is 2.5%. The test equipment leader, Shimadzu, trades at a P/E of 21x and P/B of 2.4x. In her latest report, Yuka Marosek looks at whether this valuation gap is justified.

Edition: 190

- 12 July, 2024

UK: Starmer’s policy agenda vs fiscal reality

Laurent Balt asks what a Labour victory means for the UK policy environment. He paints a cautious picture of Starmer, in his lawyerly reserve, loathe to do anything untoward on the macroeconomic policy front. Realistically, he cannot avoid trade-offs once in office: the internal pressure for spending will be high and the fiscal situation is poor. Economic growth will be insufficient to plug the fiscal gap in the short term. Ultimately, there is little room to do much without hiking taxes. A possible answer may come in chancellor-in-waiting Rachel Reeves’ plan to ask major institutional investors to pile into the government’s transition strategy. Combined with Starmer’s predictable, ‘softly softly’ approach, markets may be assuaged that a ’quiet revolution’ in Britons’ economic and social wellbeing may be possible without breaking the fiscal headroom.

Edition: 189

- 28 June, 2024

Technology

Attempts to expand into new areas, such as CRM and developer-focused products, have had limited success, with low penetration rates and integration challenges. Hedgeye does not believe MNDY will successfully bridge the gap from point solution to platform. Meanwhile, in Jan 24, the firm implemented a 20% price increase for customers. This will lead to increased churn/seat reductions and negatively impact win rates on new business. Operating in a highly competitive market with low barriers to entry, MNDY faces rivalry from established players in work management, CRM and devops - ultimately positioning its core product as an add-on solution within a broader ecosystem.

Edition: 189

- 28 June, 2024

Utilities

Kailash’s ranking tools are surfacing high-quality, high-growth stocks with long “economic runways” trading like value stocks. ARIS trades at 7.4x EV/2023 adjusted EBITDA, more than four multiple turns below the overall stock market. Bridging half this gap would push the share price above $20. With 84% of its 2023 revenue in its largest business, Water Handling, from long-term contracts, future revenues and cash flows are highly predictable. The company should generate $45-65m in FCF in 2024, with much dedicated to share repurchases. So, you have a rapidly growing company with a tremendous economic moat repurchasing shares and throwing off enough cash to pay double the dividend you receive as an owner of a large-cap index.

Edition: 187

- 31 May, 2024

Home Improvement survey reveals disappointing results

Consumer Discretionary

Gordon Haskett Research Advisors

GHRA sees a notable drop in both households planning to undertake a home improvement project and the size / scope of that remodel. 1Q24 survey specifics include: 1) Home improvement plans in the next twelve months moderated ~300 bps sequentially to 53.7% but dropped meaningfully Y/Y from 62.3% in 1Q23. 2) 57.3% of respondents have delayed buying a home (up from 56.0% in 4Q23 and above the long-term average of 51.1%), with 56.7% of them instead planning to reinvest / upgrade their current home (down from 64.3% in 4Q23). 3) The amount consumers are budgeting for home improvement projects moderated sequentially to a 15-quarter low of $5,851, or -24% Y/Y. 4) Home Depot maintained its market share leadership, but the gap to Lowe's narrowed to the slimmest margin yet in GHRA’s survey.

Edition: 184

- 19 April, 2024

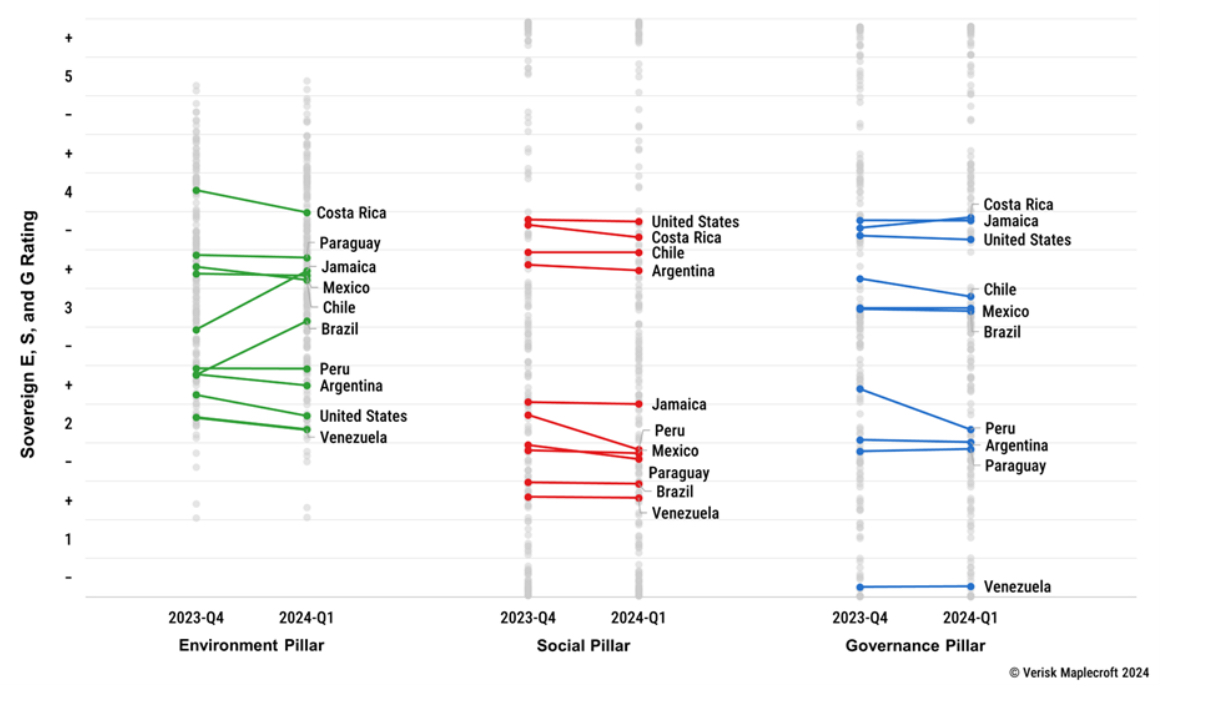

In the Americas, progress is stalling across E, S and G pillars

Overall ESG progress in the Americas remains stalled amid troublesome social and political trends in the form of weaker human rights protections and rising civil unrest. Overall, 22 countries in the region saw their scores slide in Q1/2024, with just 5 seeing improvement. Key improvers included Jamaica, benefitting from a narrowing emissions gap and strengthening government effectiveness, and Brazil, which has seen better Transition Risk performance under President da Silva. Worse performers include Peru, Paraguay and Costa Rica, despite the latter often being a regional outperformer.

Edition: 183

- 05 April, 2024

Saint-Gobain (SGO FP) France

Industrials

SGO’s Iron Blue score increases to 26/60 (newly top quartile / fertile grounds for shorting). This reflects an expanded gap between PPE capex and the P&L depreciation charge (14% of PBT adj, vs. 11% and 7% the two previous years) and another increase in receivables factoring (+6% y/y, +40% since FY20). Stripped out one-off costs remained elevated (10% of FY23 PBT adj). A new contingent liability was named in FY23 concerning competition authority investigations into the additives and admixtures sector in the EU, UK and Turkey, while class actions were instituted in the US and Canada. SGO has also continued to consolidate its Russian operations despite seemingly operating independently from the rest of the group. Iron Blue calculates that €112m of gross cash was stranded in Russia.

Edition: 183

- 05 April, 2024

BoJ and RBA rightly dovish, but still a bit optimistic

Manoj Pradhan comments that being dovish is exactly the right choice for the two central banks, but both were still a bit too optimistic on rising real wages being able to lift consumption. The BoJ has a longer wait before the output gap turns positive and it will need to tread carefully with any rate movements given the role of FX in the economy. The RBA will have to ease by much more than its rhetoric and market pricing suggest, with an outcome similar to the US but without a growth profile to match. Manoj is staying LONG MXNJPY (Banxico will stay hawkish on services inflation and strong growth). He also recommends to stay received Aus 1y1y or 2y1y. For the RBNZ, it is time to recreate a flattener (i.e., add a payer for 2024 to the existing 1y1y receiver).

Edition: 182

- 22 March, 2024

Healthcare

China's laparoscopic robots sector looks set to benefit from policy updates and hospital procurement. With over 180 certificates expected by mid-2024, tender volumes could double, offering significant growth potential. Domestic manufacturers, including MedBot, are gaining market share with second-generation devices narrowing the gap in stability and cost. Toumai, a product of MedBot with government support and competitive pricing, presents a strong alternative to Intuitive Surgical’s da Vinci system which currently boasts c.90% market share.

Edition: 181

- 08 March, 2024

Long & short ideas in the Consumer and Retail sectors

Target (TGT) - product improvements continue; stronger value message positions TGT for a better year ahead.

Gap (GPS) - key brands Gap & Old Navy building momentum; while the new CEO is expected to have a positive impact.

Nike (NKE) - lower expectations off Nov Qtr impacted the stock, but adding back retailers allows for EPS acceleration throughout 2024.

Williams-Sonoma (WSM) - the stock is at an all-time high; sees a mismatch between expectations and earnings performance.

Kohl's (KSS) - continues to struggle with its business, yet the stock has traded up with peers, look for share weakness on 4Q results.

VF Corp (VFC) - not convinced the company can turn it around after a tough 2023 as it looks to trim its portfolio of brands.

Edition: 180

- 23 February, 2024

China: Off the grid

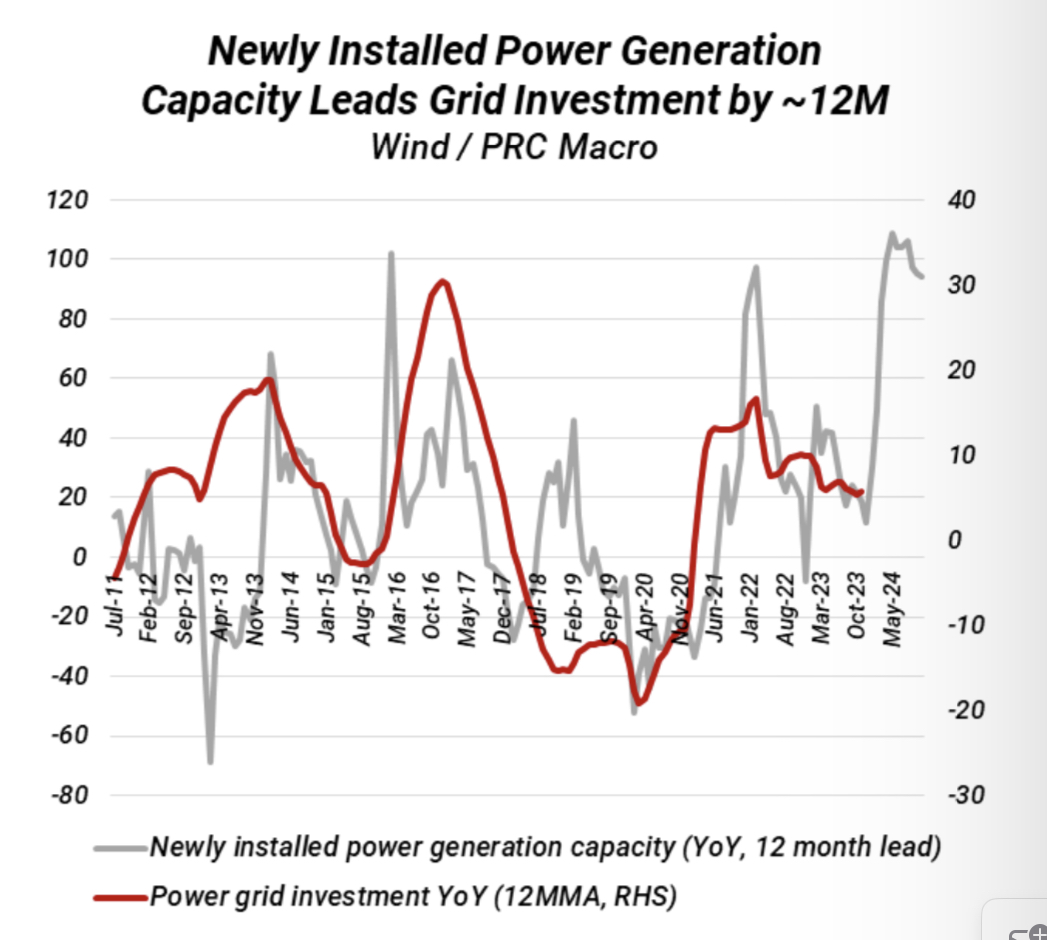

Investors have been worried about a potential contraction to grid investment in China after the State Grid (SGCC) suggested no incremental growth to investment this year. However, William Hess believes the State Grid only provided vague language as a result of the central government’s 2024 targets not yet being finalised. In the context of a massive build-up to renewable energy generation capacity against low connectivity, SGCC is one of the main actors who can close the gap, a glaring imbalance that will need to be resolved in the final budget. William reiterates his call that grid investment in China has been substantially underpriced by markets and could grow by 10% YoY or even higher. As a result, he continues to believe that copper prices could retest former resistance of USD 10,000 per metric ton as early as Q2 this year.

Edition: 179

- 09 February, 2024

Transactions indicate high upside for listed Infrastructure

Industrials

Robert Crimes reviews 138 global infrastructure deals that took place between 2015 and 2023, focusing on the 38 where he had a DCF based NAV. These transactions averaged a -3% discount to Insight NAV but listed valuations trade at a -35% discount. Share prices would need to rise c.50% to close the valuation gap. Robert expects deal flow to continue driven by undervaluation of listed corporates, resilient indexed linked FCF growth and reducing COC. Insight's key Buys to arbitrage from listed to unlisted are Ferrovial, Getlink, Inwit and Cellnex.

Edition: 177

- 12 January, 2024

Materials

This mining services company provides drilling, laboratory and waste haulage services to blue-chip firms. CAPD boasts higher margins than its competitors and has maintained these margins with significant growth over the last 2 years. Ben Jones forecasts EBT margins of ~20% going forward with FCF yield of 25% by 2025. Current trading is strong, having recently signed new drilling and laboratory contracts which Ben expects to add 11% to revenue growth in 2023 and 17% in revenue growth in 2024. The market is failing to price in this growth leaving a wide gap between CAPD’s M/Cap and Ben’s view of intrinsic value.

Edition: 177

- 12 January, 2024

Shipbuilding: Another industry gets China’ed!

Industrials

The Chinese are now the mainstream and that is going to change everything in this industry very quickly, according to David Scott. Chinese yards are moving out of their success in bulk into the more “value-added” segments of the industry such as containers and LNG carriers. Ferries and then cruise ships are next. Of course, the pattern is almost the same as we see with EVs, wind turbines, solar panels, etc. 1) The Chinese turns and ratios are already of an order of magnitude better than the incumbents. 2) The gap is widening further as the China industry scales and vertically integrates into its huge domestic clusters. 3) China’s ever more competitive real effective exchange rate is accelerating this whole process. Yangzijiang Shipbuilding looks set to be a big winner.

Edition: 177

- 12 January, 2024

Tech Trends: Key themes and questions for 2024

Technology

Areas of focus for Sales Pulse in the year ahead will include: 1) Cybersecurity - changing end user priorities and competitive dynamics. 2) UC/CC/CP - will a reduction in seat count negate increased ARPU from AI features? How will continued M&A impact this market? 3) Vendors benefitting from the rapid growth in DevOps / DevSecOps. 4) Gap in orders in 1H24 for networking market as end users digest backlog and we await ramp of next generation. 5) Broadcom acquisition of VMware driving end users to look at alternatives, to the benefit of IBM Red Hat and Nutanix. 6) Ramp of funding for Broadband Infrastructure. 7) Impact of CSP Marketplaces on Distributors and VARs.

Edition: 177

- 12 January, 2024

Bayer (BAYN GR) Germany

Healthcare

ROCGA’s Cash Flow Returns On Investments based DCF valuation platform shows BAYN to be undervalued for the first time in 10 years. BAYN is not a quality company and would not warrant attention, but the valuation gap is compelling with potentially 50% upside. With a few clicks, you can model and value one of 2000 companies across Europe and the US. Other companies that appear on their list of undervalued companies are Ahold, Associated British Foods and Saint-Gobain. A free consultation and trial can be arranged on request.

Edition: 176

- 22 December, 2023