Fortnightly Publication Highlighting Latest Insights From IRF Providers

Company Research

Industrials

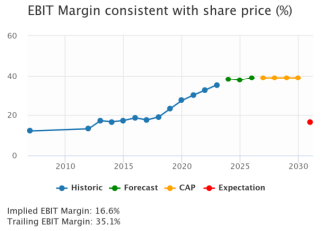

This business has a lot to like - high margins, good growth and plenty of opportunity for more accretive M&A. The Healthcare deal has also left a strong financial base from which to move forward. FY numbers last month were no surprise. Revenues were up 4% and adjusted margins were flat. Analysts had put through some upgrades with the trading statement in early Jan and though the share price has collapsed they put through another round in March. The implied to Y3 EBITM ratio is now back to 43. Willis Welby can see the share price doubling.

Edition: 208

- 04 April, 2025

InterContinental Hotels Group (IHG LN) UK

Consumer Discretionary

Willis Welby remains of the view that the UK has plenty of interesting and growing businesses. IHG features in their latest large cap growth screen - it has great financial productivity and is clearly winning market share. Dollar weakness does not help but the implied to Y3 EBITM ratio is just 84. It is too low. Hilton and Marriott are on 135 and 114, respectively. IHG would make sense GBP20 higher than it is now. Other stocks highlighted include QinetiQ (there is a good fundamental story here alongside some very cautious expectations. Despite a Q2 rerating, the implied to Y3 EBITM ratio is still only 65) and GlobalData (the disposal of part of the Health franchise may prove seminal. Management is talking organic growth >10%, margins drifting higher and accretive roll-ups).

Edition: 194

- 06 September, 2024