Fortnightly Publication Highlighting Latest Insights From IRF Providers

Company Research

China: Xi-Trump summit still possible despite tariff threats

William Hess comments that the tumultuous week for US-China highlights the latter’s position: China is happy to drag out negotiations for as long as possible. The backdrop to successive negotiations is a situation of fundamental distrust and geopolitical realignment that Beijing is in no hurry to slow down. These developments set the stage for markets to blow off some steam after recent rallies appear overextended. In terms of activity levels, William’s proprietary indicator for China is showing activity that is moderating but in line with cyclical expectations and far from collapsing. This is consistent with his expectations for Q3 GDP growth that is a tick above the consensus of 4.7%. More important for market expectations will be the Fourth Plenum next week, which should be Beijing’s attempt to improve the macro narrative with structural reform plans.

Edition: 222

- 17 October, 2025

China: A new drive

William Hess notes that this past week saw the proliferation of annual industry “stable growth plans”. These are consistent with the objectives outlined recently which themselves are consistent with expected top-down emphasis on optimising the economic layout and capacity in the next batch of five-year plans. According to comments from MIIT, the weight of stable growth plans will focus on ten industries: the steel, non-ferrous, petrochemical, chemical, building materials, machinery, automobiles, power equipment, light industry, and electronic information manufacturing industries. These are cited as key forces to stabilize the industrial and national economy. As is the case for the steel sector, William sees the latest annual stable work plans as outlines for pending five-year plans to be released in 2026, focusing on improving high-quality supply capacity, optimizing the industry’s development environment, and promoting the effective improvement of quality and reasonable growth of the industry. It’s all part of Xi’s quality productivity drive.

Edition: 220

- 19 September, 2025

China: The balance is shifting

For much of this year William Hess has been following the theme of relative macro stability against a backdrop of micro (sector/corporate) weakness. With some exceptions, this balance is shifting. Most important is that last week saw a massive rerating of forward earnings growth and cash flow per share expectations for the CSI300. Predictably, this follows a bottom for M1 (the old definition) to GDP on a rolling 12m basis and signs of modest but systemic injections of cash. The market view appears to be shifting whereby micro performance is now dominant as macro performance softens. On the macro data, predictable softness to the FAI data, for example, has the important exception that everything tech and IT is booming as energy investment and even manufacturing capex growth slows. This dynamic has worked well for equity market performance in the US and may be gaining momentum in China.

Edition: 219

- 05 September, 2025

China: Tailwinds in equities

William Hess is fully aware that geopolitics may fill the policy void in China, but last week saw a continuation of positive signals behind equity markets. Most important are volume-based measures for the CSI300 that point to strengthening support – William notes that price-volume indicators are pointing to position accumulation rather than intraday trading. Other constructive factors are also worth noting, including falling risk-free and interbank rates, elevated systemic liquidity levels and regulatory mandates for onshore institutional investors to increase equity allocations (which was responded to positively). Another tailwind comes in the form of repatriation of Chinese institutional capital in the face of Trump risks in the US. Sure, the property sector is still in the tank, but this just encourages more asset rotation into equities. The direction of the tide is clear; it’s time to buy the CSI300.

Edition: 218

- 22 August, 2025

USD: A race to the bottom?

According to Charles Hess, the US strategy is to lower the value of the dollar - without affecting its status as the world’s reserve currency - and encourage domestic manufacturing by increasing the price of imports and lowering the price of exports. Trade will shrink among some trading partners and increase between others (i.e., India and Russian oil), as they rearrange their economic relationships. As the US pulls away from the alliances and allies that have granted it primacy as a global superpower and as the provider of the world’s reserve currency, China is attempting to make available a substitute for the dollar-centred international economy via Beijing-centred international organizations and alliances. These Beijing-centred coalitions increasingly trade in their own currencies. Gold, silver and other hard assets will hold their value and increase in price as the dollar declines.

Edition: 218

- 22 August, 2025

Beware of floods

Charles Hess observes that the US National Weather Service issued a record 3,040 flood warnings between January 1 and July 15 this year, more than any other similar period since the modern alert system was put in place in 1986. Meanwhile, the Steve Miller Band claim that they cancelled their entire 2025 North American concert tour because of the combination of extreme heat, unpredictable flooding, tornadoes, hurricanes and massive forest fires. Charles comments that this is further evidence that the climate crisis is not only worsening for risks to property but is also harming the fans of rock music. He feels this is now “getting serious!"

Edition: 217

- 08 August, 2025

China: The RMB’s implicit trading range

William Hess points out that under PBoC’s rigid dollar peg the path for USD/CNY has increasingly resembled that for USD/HKD, with upper and lower trading bands. William expects renewed USD weakening, given that the ongoing trade talks are not sufficient for PBoC to abandon its current target range. His team predict that the Bank will likely allow +/- 2% movement in USD/CNY relative to its daily fixing. Elevated trade tensions and external uncertainty will only reinforce PBOC’s commitment to defending this trading band. Moreover, PBoC’s management of moves to USD/CNY within this trading band appears to be asymmetric. The Bank appears to be more stringent with defending the trading band and daily fixing when the RMB is under greater pressure to depreciate. Against this backdrop, William believes the PBoC will continue to confine USD/CNY to the 7.05-7.35 range for the rest of this year while the RMB depreciates against the CFETS currency basket ~10% by year end.

Edition: 213

- 13 June, 2025

US-China ceasefire doesn’t eliminate market risks

The US-China tariff ceasefire is a win for Beijing. From what William Hess can tell, the Chinese side committed to very little in securing a broad tariff rollback, including a reduction of de minimis tariffs to 54%. However, when markets reopened, they were not trading as expected. William sees markets in Asia trading around two themes: 1) The very modest recovery to metals prices reflects lingering concerns over global growth and the risk of Beijing failing to deliver meaningful stimulus. However, investors are expecting more front-loaded restocking of imports from China by US firms. 2) A rebound to gold prices and a weaker dollar suggest that other US trading partners, especially the EU and Japan, will follow China’s lead and take a tougher stance in future trade negotiations with the US. William thinks investor concerns are warranted and doesn’t see the US-China tariff ceasefire as a credible put against market volatility.

Edition: 211

- 16 May, 2025

China: Nerves of steel

Markets are again speculating that China will cut steel production by 50m tonnes, with traders responding by shorting raw materials and adding long exposure to steel products. There is credibility to the statement, including that NBS revised down crude steel production after being investigated by the government in January. However, William Hess stands by his statement that a 50m cut is unlikely to happen. That said, he thinks a demand air pocket resulting from stimulus and tariff uncertainty will dominate steel production cut narratives before the start of the winter heating season, posing significant downside risk for iron ore. Another policy consideration is the increasing resistance to elevated exports of cheap Chinese steel products in other major economies (ex-US), which remains a risk to current demand forecasts even if no tariffs have yet been placed on Chinese steel.

Edition: 210

- 02 May, 2025

China: Bearish for commodities, supportive for equities

With the National People’s Congress having just opened, Qiushi – the Party’s ideological journal – has been the main voice in the domestic media setting the tone. Public intellectuals and policy advisors have been relatively quiet. However, William Hess notes that as per normal process, local governments held their own NPCs ahead of the central one, and aggregated policy targets sent some interesting signals. Although average local headline growth targets (and related fiscal targets) were dialled back, average growth targets for FAI and retail sales came in at 5.4% YoY and 5.7% YoY respectively. If these targets are achieved, it would be bullish for domestic asset prices. Given the low base and pending expansion of funding for durable goods swap programs, retail sales growth in this ballpark looks achievable. William still sees the overall backdrop as bearish commodities in the short-term, and more supportive of equities (after a potential post-NPC correction).

Edition: 206

- 07 March, 2025

China: Out with the old, in with the new

William Hess highlights two news items that have sent shock waves through Chinese social media and global markets. The first is the formal nationalization of Vanke, one of China’s largest developers, and the other is the emergence of DeepSeek, an open-source AI model from China. These two developments are relevant because they illustrate the continued divergence between the old and new economies in China. The former showcases Beijing’s resolve to avoid financial defaults for major developers, setting a price floor for old economy assets. This floor may be low, but it avoids the abyss. The latter reveals the upside potential for Chinese tech companies via a new generation of “late developer advantages”, meaning the ability to achieve competitive outcomes with binding budget and resource constraints despite the US tech embargo. Exciting times ahead.

Edition: 204

- 07 February, 2025

China: Political messaging fails to inspire

Beijing’s approach so far has been to focus on asset prices and demand as the keys to the 2025 growth equation. William Hess disagrees that demand is the problem. Central economic planners are pretty good at backing out how much demand they need to engineer. Where it comes to stabilising asset prices, this is important to shore up nominal anchors for domestic price expectations and interrupt negative wealth effects. But this is not enough. For asset prices to sustain increases there needs to be tailwinds from stronger cash flow accruing to those assets and incomes that end up with would be buyers. Attention to these income questions largely absent from Q4 stimulus theatre. That said, changes to incomes (and income expectations) should be the byproduct of changes to the underlying economic process(es), and this is where the issues of political leadership and narratives come in.

Edition: 202

- 10 January, 2025

China: Long live stimulus theatre!

The Q4 Politburo meeting delivered a significant shift in macro policy, reinforcing confidence in achieving the 5% growth target for 2025. William Hess claims that on this basis alone, the short-term market reaction is justifiable. However, investors should be realistic about the magnitude of stimulus in the pipeline. Consumption stimulus, for example, is a slow-moving variable with a 3-6-month lag. William is also still waiting for further proof of tangible injections into the system to believe it will actually occur. Nevertheless, he is most bullish on equities, claiming that a 1x increase to the forward multiple implies ~8% upside to the CSI300; joined with a 10% improvement to earnings expectations, this would see an ~18% increase. The backdrop is also bullish for government bonds and developer stocks and bonds in the short term.

Edition: 201

- 13 December, 2024

China: More consumption stimulus rumours

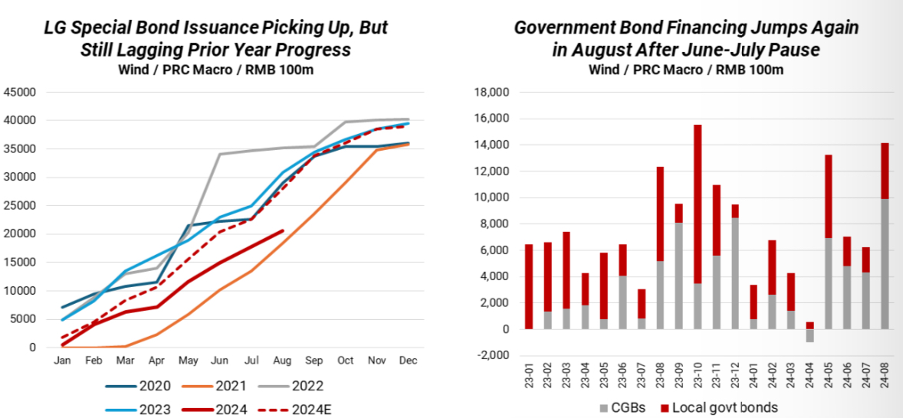

William Hess has very low confidence in rumoured additional stimulus involving either or both RMB 2trn in additional CGBs in H2 and RMB 1trn in consumer vouchers to stimulate consumption. He sees low probability of an increase to the annual deficit, with planners favouring accelerating investment in strategic infrastructure and industrial capacity. However, William does expect a consumer voucher programme for the National Day Holiday, but it will be limited in size and impact. Even without additional stimulus, the acceleration to fiscal spending in H2 will be sufficient to boost growth and base metal demand in Q4 and likely Q1 next year. There are already signs of a re-acceleration to infrastructure project approvals and government bond issuance after May (see chart).

Edition: 193

- 23 August, 2024

Ukraine: Debt restructuring deal is ambitious

Ukraine’s preliminary sovereign debt restructuring deal balances short-term downside risk protection for creditors against substantial debt relief for Kyiv. However, the restructuring is also clearly ambitious given its reliance on unrealistic IMF growth and debt sustainability forecasts, setting the stage for a potential second restructuring around 2027/2028. Max Hess continues to consider the GDP warrants effectively worthless - a view reinforced by the fact that the deal removed cross-default provisions to those warrants. Meanwhile, Russian forces continue to make creeping advances on the front across Ukraine’s Donetsk region, particularly in its south. Max believes that it is likely that Russian forces will control almost the entirety of the Donetsk region for the first time ever by year’s end if the current pace of Russian advances continues.

Edition: 191

- 26 July, 2024

The post plenum mood

At the close of the Third Plenum, William Hess believes that a key question is whether the contradictions in the published Resolution will cut in favour of animal spirits, value creation, and productivity, or the expansion of regulation and bureaucracy in the name of reform. For example, there is encouraging language on preventing the government from improperly interfering in price formation in the utilities and transport sectors, yet some level of intervention is still implied, and it is unclear what for. Additionally, all areas slated for reform will be subject to the creation of “mechanisms”, code for new bureaucracy. The resolution also mentions the need to strengthen Party leadership, military, and social risk prevention/surveillance as preconditions for realising “Chinese style modernisation”, and this reality has to be weighed against the call to liberate social productive forces.

Edition: 191

- 26 July, 2024

China RMB: Buy the rumour and sell the fact?

President Xi recently hosted a preparatory session for the Third Plenum in July. On the previous two occasions, William Hess points out that Beijing’s pivot to growth support helped the RMB appreciate against the USD. Will this occur again? For this to happen, the PBoC and RMB must overcome two technical obstacles: 1) RMB overvaluation against the currency basket, and 2) the large and persistent deviation between the official fixing rate and the market exchange rate. These issues have only worsened recently. Moreover, the current policy and transmission lags for property stimulus and backloaded fiscal spending will raise questions about the efficacy of growth support measures. William has significantly revised the probability of a one-off devaluation of the PBoC’s USD/CNY daily fixing rate by 1.5% from 20% to 60%.

Edition: 187

- 31 May, 2024

China: Credit miss amid the policy void

William Hess thinks the April credit data could indicate that the Q1 fiscal miss is morphing into a Q2 collapse in credit demand. Effective credit demand remains weak and this should give rise to concerns that Beijing will be unable to maintain 5%+ growth with its supply-side led agenda. William’s view is that two related components of the policy agenda are still lacking: 1) there are still expected time lags to the implementation of more effective growth support measures, and; 2) central policymakers have still failed to provide enough policy specifics for key initiatives. Beijing has yet to show us the money, and markets may continue to discount the impact of these programmes heavily, at least in the short-term.

Edition: 186

- 17 May, 2024

China: Steel production, not demand, to drive iron ore in Q2

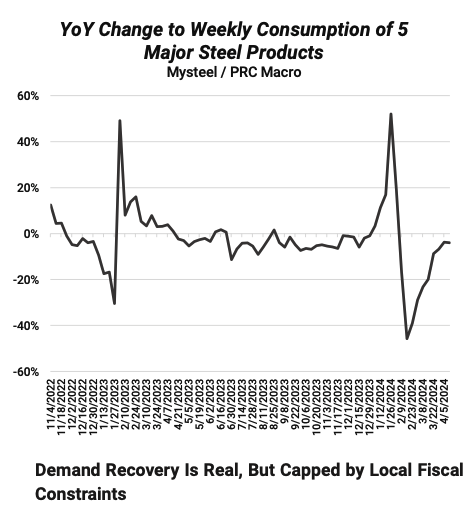

William Hess anticipates the ongoing steel demand recovery in China to peak in May and remain elevated through 2Q/2024. However, the continued slow issuance of local government bonds presents headwinds for this recovery. Consequently, William has revised his 2024 steel demand growth forecast from 1.1% to 0.9%. Contrary to market consensus, he believes that weaker steel demand in China has already been fully accounted for by market participants and is no longer a significant obstacle. A potential game changer for iron ore could be the risk of production cuts. Underreported steel production in Q1 this year might provide the National Development and Reform Commission (NDRC) and steel mills with fewer reasons to reduce production in the second half of the year, which would support better-than-anticipated iron ore demand.

Edition: 184

- 19 April, 2024

Peak domestic crude demand expected in China

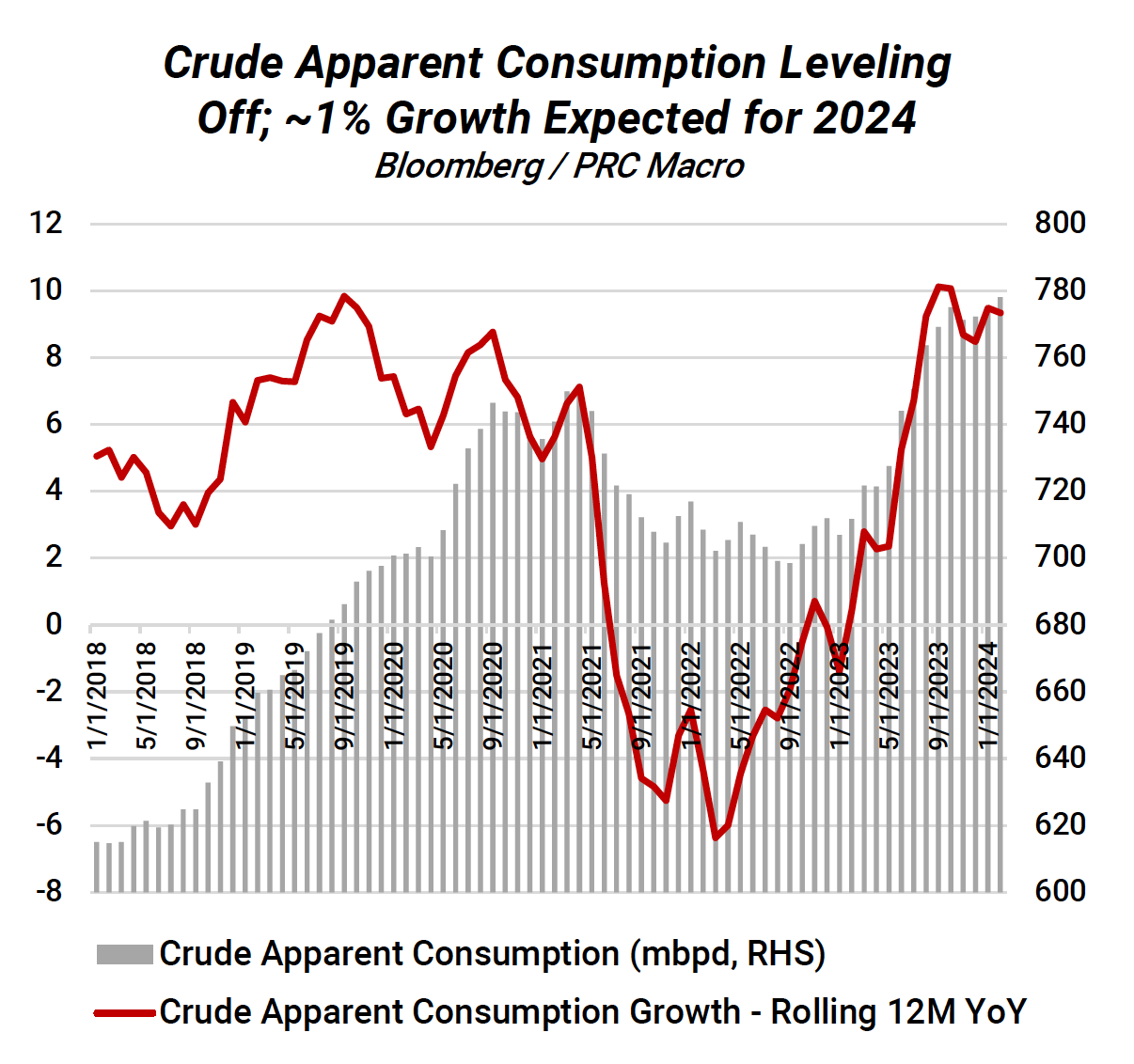

Strong holiday travel data in China sparked debate as to whether this would lead to a sustained recovery for domestic crude demand. William Hess doesn’t think so and advises investors not to mistake seasonal crude restocking and imports as a sign of strength. The recent crude inventory drawdowns are larger than normal, reflecting weak demand expectations on a cyclical basis, a secular domestic view that peak crude demand is nearing and a reduction to teapot operating rates. The coincidence of peak crude demand in both China and the US provides an interesting long-term set up for USD/CNY, especially with markets underappreciating the petrocurrency characteristics of the USD and China’s involvement in the global energy transition.

Edition: 183

- 05 April, 2024

China: Energy, durables and exports support restocking

Jan-Feb macro activity points to a solid growth in export rebound, manufacturing capex and energy-related infrastructure investment against a deterioration to housing construction. On the surface, policymakers should be satisfied with this batch of data and this could make them complacent towards growth support and supporting the RMB exchange rate. However, weak domestic demand and the property sector remain major concerns. William Hess expects a push for an acceleration to public housing construction and further eases in policy on the use of developer funds in escrow. More broadly local governments will likely have to accelerate issuance of special bonds and William expects a 50bp RRR cut in April to facilitate an uptick in fiscal funding.

Edition: 182

- 22 March, 2024

China: NPC improves fiscal outlook but falls short on monetary policy

William Hess believes the NPC report to be uninspiring but “good enough” as a down payment on the 5% growth target. Based on new inputs from the NPC so far, he has marked up his estimate of implied augmented fiscal expenditure growth for 2024. Overall, the NPC work report retained a familiar supply side bias but acknowledged inadequate demand as the primary impediment to a more credible domestic cycle. Apart from onshore equities (which William guesses were instructed to trade higher), markets were unimpressed by the NPC. The report repeated one of the key policy failings of the past 18 months by omitting specific funding commitments for programs like affordable housing construction, subsidies, and related monetary policy language that implied larger injections of cash/base money.

Edition: 181

- 08 March, 2024

China: Off the grid

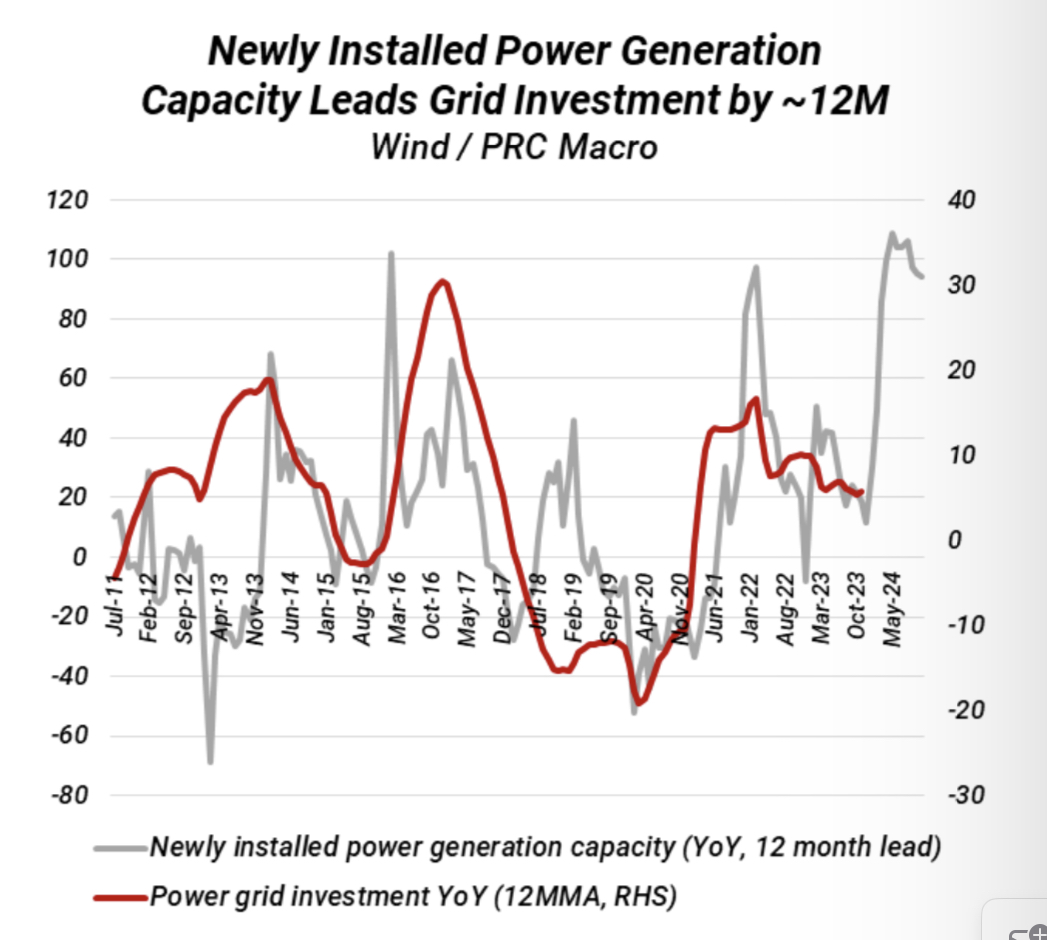

Investors have been worried about a potential contraction to grid investment in China after the State Grid (SGCC) suggested no incremental growth to investment this year. However, William Hess believes the State Grid only provided vague language as a result of the central government’s 2024 targets not yet being finalised. In the context of a massive build-up to renewable energy generation capacity against low connectivity, SGCC is one of the main actors who can close the gap, a glaring imbalance that will need to be resolved in the final budget. William reiterates his call that grid investment in China has been substantially underpriced by markets and could grow by 10% YoY or even higher. As a result, he continues to believe that copper prices could retest former resistance of USD 10,000 per metric ton as early as Q2 this year.

Edition: 179

- 09 February, 2024

China: Holiday blues

So far, there are few indications of sharply lower activity levels outside of normal seasonality. That is, except for PBOC liquidity injections. There is always some form of seasonal liquidity injection for the holiday period, but as William Hess has been noting for weeks, large and highly volatile levels of PBOC net outstanding OMO is indicative of abnormally high liquidity demand from some quadrant(s) of the economy. The property sector and related creditors are the obvious sources of systemic stress. The recent bloodbath in onshore equity markets didn’t help either. But, as has been the case in the interbank market, significant state intervention in equity (and the FX) markets helped to stabilize levels. None of this seems consistent with President Xi’s call to make China a “financial powerhouse”. It also draws into question the policy implications of related calls for a “strong economy, strong currency and strong central bank”.

Edition: 178

- 26 January, 2024

China: Zhongzhi bankruptcy opens door to stimulus

In a pivotal move, a Beijing court accepted Zhongzhi Group's bankruptcy application, a major private financial conglomerate laden with distressed debt and troubled developer projects. Following the nationalisation of Zhongzhi's trust subsidiary in September, a similar fate looms for Evergrande. Onshore investors foresaw these events since their financial licenses were nationalised last September. William Hess sees Zhongzhi's bankruptcy as a positive for property sector policy support, paving the way for broader liquidity injections and demand stimulus for surviving developers. Beijing's shift towards a comprehensive bailout strategy, recognising the inadequacy of selective measures, is noteworthy. Initiatives like Guangzhou's property purchase voucher scheme and Shenzhen's urban village renovation plan aim to de-stock property inventories and rejuvenate construction. William also highlights the PBoC’s commitment to support property sector policies and construction, which – although not directly targeted towards equity markets – will be taken as positive.

Edition: 177

- 12 January, 2024

China: RMB rebound

William Hess continues to believe the recent rebound to the RMB exchange rate reflects a domestic cyclical inflection point. Although this has been helped by a weaker dollar and SOE bank buying, William believes this momentum can be sustained in 2024 as the effects of the manufacturing restocking cycle and official efforts to revitalise FDI and portfolio inflows take over as supporting factors. The restocking cycle will be driven by steel, energy, chemicals, healthcare and consumer electronics, and will last until Q4/2024, helping to bring GDP growth to 6% YoY. Moreover, pending dollar sales by Chinese exporters will accelerate the pace of RMB appreciation against the dollar – William reiterates his call that USD/CNY will return to the 6.9-7 range by the end of this year, and 6.6-6.7 by 2024’s end.

Edition: 175

- 08 December, 2023

China: An alternative take on the Xi-Biden tete-a-tete

The consensus takeaway from the Xi-Biden meeting in San Francisco was that the conversation was restorative and put the bilateral relationship on a more stable trajectory. William Hess fundamentally disagrees with this assessment, seeing potential working level re-engagement as papering over a fundamental divergence of respective strategic postures. Xi arrived at the meeting with three key requests, all of which were denied. So why did he turn up? It was to deliver a direct and solemn message about how Beijing interprets the US strategic posture and the potential consequences that will follow, especially on the issue of Taiwan.

Edition: 174

- 24 November, 2023

China: Beijing painting itself into a corner?

One of the key phenomena right now is the US bear steepener, which may have some room to uptick. William Hess believes Beijing is still worried about potential external shocks from dollar strength and a reversal for US equities. He also thinks that technocratic officials are similarly worried about unrealised losses originating from the property sector and quasi-fiscal credit. More developer losses are expected in coming months, which may lead to a state stabilisation fund of some RMB 500bn. The PBoC continues to signal a growth-supportive agenda, but nothing that will trigger a short-term risk-on rally. William discusses Beijing’s overall policy stance, believing it insufficient to revitalise domestic capital markets and reflate domestic asset prices.

Edition: 172

- 27 October, 2023

China: Beijing all in to avert property and RMB fallout

The PBoC slashed the FX reserve requirement from 6% to 4% in a bid to curb the pace of RMB depreciation, but William Hess sees this only as a down payment and expects the central bank to further escalate intervention before early Q4. He reiterates the view that the previous high for USD/CNY of 7.37 is a line in the sand for the PBoC. Beijing also announced a series of new measures to boost consumption and property demand, which may not be sufficient to stimulate new demand but may tap into pent-up demand. Expect additional measures to bolster property market in September.

Edition: 169

- 15 September, 2023

China: Inflection point

William Hess comments on how the Q2 Politburo meeting marked a policy inflection point, as Beijing’s stance shifted from emphasis on deleveraging to reflation. There will be a natural lag between this shifting stance and a reversal to economic fundamentals, namely manufacturing restocking. However, leading indicators continue to point to late Q3 or early Q4 as the inflation point for the manufacturing inventory cycle. Unlike previous cycles driven by land sales and housing new starts, this one will be supported by the domestic energy transition and demand for durable goods. William believes the beginning of the cycle will confirm a trend reversal for the RMB exchange rate and even A-shares. Expect USD/CNY to return to the 6.9-7 threshold by 2023’s end, and a 20% rebound in A-shares over the next 12 months.

Edition: 168

- 01 September, 2023

China: Energy is the new property

Despite challenges from property developer and local government austerity, China experienced an acceleration in infrastructure investment and energy-related industrial production in June. William Hess sees this as indicating a shift away from the property cycle and towards energy-related investments, driving restocking and downstream durable goods demand. As manufacturing destocking is expected to transition to restocking by Q3, William expects domestic producer prices, RMB exchange rate, A-shares, and copper prices to rebound. Beijing only needs modest H2 growth to meet the 2023 target, reducing the likelihood of significant fiscal stimulus.

Edition: 165

- 21 July, 2023

China: Balance sheet impairments plague property

The current official and market consensus view on China is that macro weakness is a function of inadequate demand. William Hess disagrees, believing that this mistakes outcomes for underlying causes. The latter are a function of ongoing balance sheet repair in large segments of the economy. He continues to expect Beijing to introduce more easing measures in Q2, including steps to lower debt burdens for households and local governments in the form of 15 bp cuts to 5-year LPR in both May and August. However, this alone will not resolve systemic balance sheet problems, and until policymakers address them, the effectiveness of conventional demand side policy measures will remain subdued.

Edition: 161

- 26 May, 2023

Bearish short-term views on base metals and RMB stay intact

Xi’s economics team recently emphasised the “accelerating the construction of a modern industrial system” and “supporting Chinese-style modernization with high-quality population development”. These are clearly longer-term objectives, but they are still relevant to short-term sentiment as China gets back to work after the May 1 holiday. So far, William Hess’s short-term views on base metals and the currency from recent pieces remain intact. He notes that onshore positioning in copper, for example, has turned decisively in this direction after the Politburo Q1 meeting. The latest update to his cyclical indicator for China continues to show a loss of recovery momentum.

Edition: 160

- 12 May, 2023

China: A long-awaited reversal

Jerome Powell’s egomaniacal campaign against evaporating inflation will bring about sharply weaker USD and deterioration of US activity, benefitting the RMB and RMB assets, including equities. A sharp downturn would of course hit China via multiple transmission channels, but William Hess points out that a further loss of confidence in Fed stewardship in the US - not to mention the debt ceiling showdown - could begin to reverse the long-term underperformance of Chinese equities.

Edition: 159

- 28 April, 2023

China Iron Ore: Sell in May, come back in October

Iron ore prices in China are a function of steel production in the short-term, credit growth and restocking in the medium-term and property new starts in the long-term, explains William Hess. He still expects a secular decline in the long run against a backdrop of falling property new starts, voluntary steel production cuts and substitution from increased scrap recovery. However, iron ore is currently oversold. Production rates are still relatively high and near-term credit growth will provide a floor for demand. William expects prices to rebound to USD 140 per metric ton before a major retreat to 90-100 per metric ton in late May.

Edition: 157

- 31 March, 2023

China: Business as usual, or business unusual?

William Hess questions whether Beijing can steer the economy towards Xi's "new development pattern" without structural adjustment funds. The previous round of equity market strength was driven by inflows, but these effects have been waning. William expects the effects of resource front-loading to wear off soon, and there may be room for a pullback as market breadth tops out. The perception is that local governments are still struggling with financial stability management, constrained leverage growth, and lingering ZCP shocks. As a result, significant resources are still being diverted to paying for the past, not Xi's "new development pattern". Beijing's "business as usual" approach to structural shifts in the operation of the economy is the right step in the wrong direction, and market sentiment may get squeezed in the middle.

Edition: 154

- 17 February, 2023

China: Post-Party Congress, Post-ZCP, Now What?

William Hess continues to expect deregulation (big tech) and decentralisation (local fiscal) to be key investment themes for 2023. However, temporary policy reforms without structural political reforms will limit the systemic response. Despite the collapse of the ZCP, politics is not dead. The political leadership will decide the extent of easing in key areas (big tech and property). CCDI has downgraded anti-corruption efforts to focus on “integrating supervision with governance”, implying a focus on KPIs set in Beijing. For full-year 2023, William expects modest headline policy impulses, but in the short-term he expects fiscal and credit front-loading and overshooting…

Edition: 153

- 03 February, 2023

China: Potential policy and macro upside

Earnings expectations in the US and China have both been falling, but with China seeing larger potential policy and macro upside this opens the door for relative equity outperformance. In China, upstream activity levels remain elevated heading into the holiday break, with the appearance of a strong rebound to traffic congestion/flows. This indicates that the first wave of Omicron cases has crested and the overall macro impact is smaller than originally expected. William Hess remains cautious towards the overall rebound to household demand and continues to see the potential for market disappointment once full-year fiscal and credit targets are announced. Where it comes to output, William still sees incentives that skew towards overproduction.

Edition: 152

- 20 January, 2023

A core portfolio holding

James Aitken continues to believe that oil and gas should be a core portfolio holding. He remains LONG Hess and BP, and recommends that investors remain long, too. The recent (past three months) inelasticity of major oil and gas stocks to declining oil prices may be a hint that new (fed up with ESG) buyers are coming into these well-run, cash-flow vomiting businesses.

Edition: 152

- 20 January, 2023

China: Limited developer bailouts

Beijing’s resumption of developer equity refinancing, among other policies, will not revive land purchases and property construction, nor will it put the property sector back on track and prompt a cyclical recovery. According to William Hess, the policies represent a “whatever it takes” moment from regulators to shore up select market traded private developers, prevent broad write-downs on bank assets and protect collateral values. William remains bullish on bonds and share prices for developers on the designated survivors list, but he is still deeply bearish for property sales, new starts, and correlated metals demand.

Edition: 150

- 09 December, 2022

China: National security economics will dominate resource allocation

William Hess believes the increased investment in military-oriented sectors during Xi’s third term will create new sources of growth uncorrelated with structural negatives, with capex likely to increase significantly in coming years. As part of national security economics, we will see more state-owned enterprise mega mergers in strategic sectors, including the semiconductor industry’s shift away from the VC/PE model to one relying on large-cap SOEs. This, along with accommodative monetary policy, should be equity market positive despite the lingering impacts of Covid and the property recession.

Edition: 144

- 16 September, 2022

China: Rate cuts strengthen PBoC’s defense of RMB

William Hess sees the PBoC strengthening FX intervention to confine USD/CNY within a narrow range between 6.6-6.9 ahead of the party congress, and market speculation over risks of USD/CNY devaluation will only strengthen the PBoC’s resolve. The focus of PBoC intervention will be concentrated in the relatively thin offshore USD/CNH market via intervention by state-owned banks with the goal of compressing the onshore/offshore FX spread. William also forecasts interbank rates staying lower for longer in the absence of a major credit impulse associated with land/property sales, and also because William expects further cuts to mortgage rates and average corporate borrowing costs.

Edition: 142

- 19 August, 2022

China: Potential outcomes of the Politburo meeting

Don’t expect a big stimulus push in the short-term. William Hess believes a message will be sent out that stimulus will come if and when necessary, wholly contingent upon downside outcomes for growth in Q3. Energy security will also be a pressing topic, with Beijing potentially diving back into global thermal coal and energy markets to help offset a winter energy shortage. Investors should also listen out for the Politburo hinting at the importance of maintaining a stable RMB exchange rate, which he explains could create a great arbitrage opportunity to be LONG the RMB against a basket and SHORT the RMB against the USD.

Edition: 140

- 22 July, 2022

China: Shallow economic recovery bearish for commodity cycle

Although local governments may retreat from the most restrictive measures of previous Covid outbreaks, gentler measures will still create enough uncertainty to dent a recovery to demand. The recovery to upstream supply continues to be much stronger, and William Hess expects this imbalance to ultimately drive a destocking cycle. This is at the heart of William’s bearish cyclical outlook for commodities and nearer term call for a correction to metals prices.

Edition: 138

- 24 June, 2022

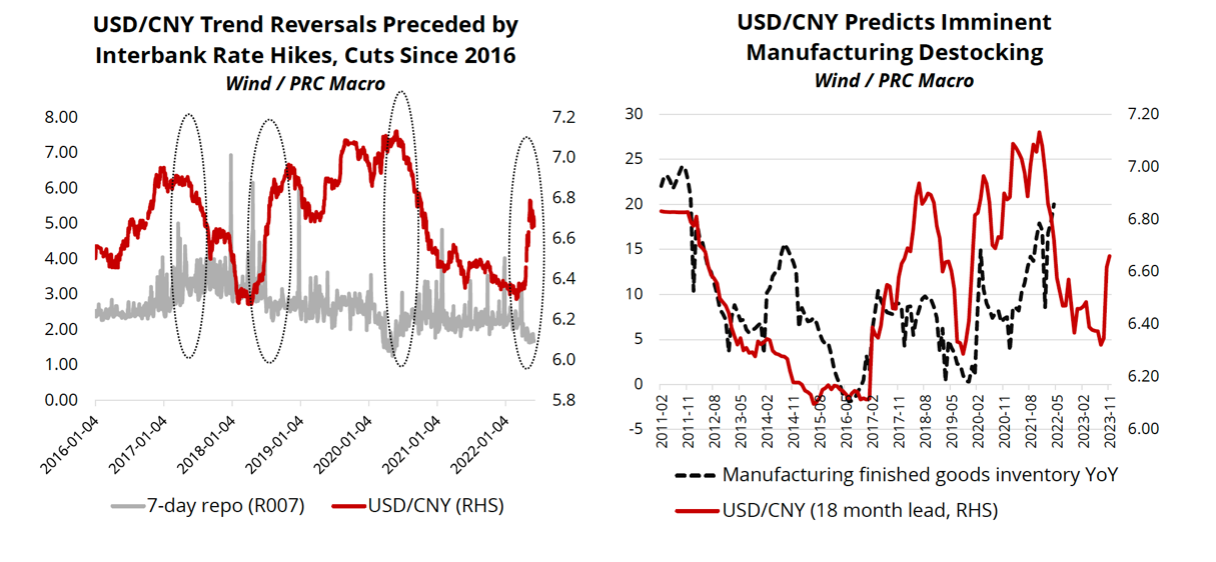

China: RMB depreciation is not over yet

Since 2015 the RMB exchange rate has been primarily driven by PBoC interest rate policies (see chart 1). William Hess sees no intention for the PBoC to exit from its current pursuit of growth/asset price reflation. With greater correlation between USD/CNY and domestic asset prices & the inventory cycle since 2015, the current direction of USD/CNY causes William to be vigilant towards the sustainability of the equity market rebound and imminent risks to base metals prices from manufacturing restocking (chart 2). Expect USD/CNY to test the 6.9-7 threshold.

Edition: 137

- 10 June, 2022

China: Piecemeal stimulus a bull trap for commodities

William Hess claims that most of Prime Minister Li’s recently announced measures are just piecemeal fixes with limited funding. Although he expects Li and others to push for bolder stimulus, he believes the pro-growth camp has not achieved a decisive majority in Beijing. Ultimately, this sets up a bull trap for commodities. The longer the delays on easing Covid policies and on stronger measures to support fiscal spending and the property sector, the bigger the macro hole that will need to be filled.

Edition: 136

- 27 May, 2022

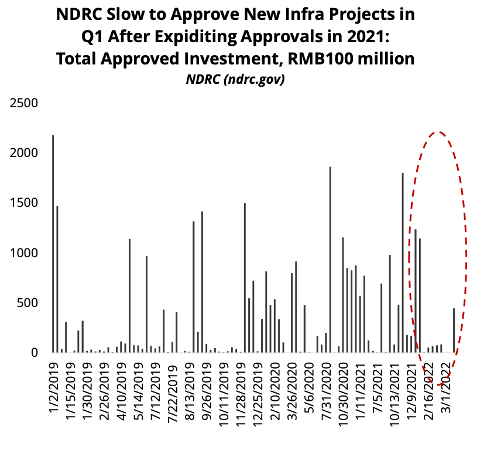

China: Will hopes for infrastructure stimulus fade?

Market hopes for stimulus are running high, but William Hess’s review of NDRC infrastructure project approvals and domestic resource flows suggests lower-than-expected progress on approvals on spending. LGFV bond issuance - a key source of leverage for local infrastructure investment - is down on a YoY% basis, raising the risk that such projects may be underfunded. William still expects Beijing to deliver additional stimulus soon, but market expectations for commodity demand will remain disappointed. He remains bearish on steel, copper and aluminium.

Edition: 135

- 13 May, 2022

China: The economic cost of the latest Omicron outbreaks

The latest outbreaks and subsequent lockdowns have had little impact on upstream industrial production, reaffirming William Hess’s bullish outlook for iron ore and coke. By contrast, domestic logistics and shipping has seen a big hit, with port shipping for domestic trade contracting by 24% YoY and cement shipping by 30% YoY. Expect the PBoC to ease more aggressively to prop up the property sector and initiate toxic asset purchases, including via a 50bps RRR cut in April, which will steepen the yield curve.

Edition: 133

- 14 April, 2022

China: Are policymakers close to pressing the panic button?

William Hess believes policymakers are pivoting from prioritising growth to asset price stability. There are signs Beijing is working on a larger-scale campaign to stabilise the property market (and property prices), and William believes a key step will involve purchases of toxic assets from commercial banks by a state-owned fund, and is therefore bullish for developer and bank stocks. In the past, stronger policy support for property has initially boosted developer shares more than developer bonds, with the latter repricing anticipated benefits more slowly, providing potential opportunities for investors.

Edition: 132

- 01 April, 2022

This isn’t demand destruction, it’s demand construction!

The transitory inflation crew want you to believe demand destruction will soon restore commodity prices to normal levels, yet every so-called government solution involves subsidising demand! James Aitken reiterates how the largest commodities demand construction event is the climate transition currently underway. In fact, as important as the recent repricing of bonds has been, commodities are the world’s new risk-free curve, and everything is priced off them. Recommended related trades include LONG AUD, which will benefit as the world turns to Australia as a trusted commodity supplier, and staying LONG BP and Hess Corporation.

Edition: 132

- 01 April, 2022