Fortnightly Publication Highlighting Latest Insights From IRF Providers

Company Research

Consumer Discretionary

Brian McGough reiterates his bearish view on FND despite the stock’s ~50% drop since his Apr 24 short call (vs. the S&P +33%). Brian is updating his analysis using his M.A.P.S. (Market Area Performance Study) framework, which tracks store performance by opening cohort. His latest findings suggest that stores opened in 2024 & 2025 are performing even worse than earlier cohorts, reinforcing that FND’s weak comps are structural, not cyclical. New units also show rising market overlap with the likes of Home Depot and Lowe's. While FND is often seen as a housing-recovery play, Brian expects another ~30% downside as earnings, growth guidance and unit expansion continue to disappoint.

Edition: 222

- 17 October, 2025

Outside of AI, why invest in the US?

US equities remain the world’s most important market, but passive benchmarks are distorted by AI concentration risk. Durable alpha lies in structural themes beyond AI. Power infrastructure (Constellation, Duke, NextEra) will benefit from grid bottlenecks as data centres drive demand. Re-industrialisation (Caterpillar, Honeywell, Rockwell) reflects reshoring and automation. The energy transition (Dominion, Enphase, ExxonMobil) requires trillions in capex. Housing scarcity (D.R. Horton, Home Depot, Lennar) is a structural imbalance. Healthcare innovation (Abbott, Eli Lilly, UnitedHealth) rides longevity and med-tech advances. Cybersecurity (Cisco, CrowdStrike, Palo Alto) is non-discretionary. Generational wealth transfer (BlackRock, Morgan Stanley, Schwab) reshapes capital flows. The AI productivity super-cycle is real, but thematic allocations across these shifts offer broader, smarter US exposure.

Edition: 220

- 19 September, 2025

Home Improvement survey reveals disappointing results

Consumer Discretionary

Gordon Haskett Research Advisors

GHRA sees a notable drop in both households planning to undertake a home improvement project and the size / scope of that remodel. 1Q24 survey specifics include: 1) Home improvement plans in the next twelve months moderated ~300 bps sequentially to 53.7% but dropped meaningfully Y/Y from 62.3% in 1Q23. 2) 57.3% of respondents have delayed buying a home (up from 56.0% in 4Q23 and above the long-term average of 51.1%), with 56.7% of them instead planning to reinvest / upgrade their current home (down from 64.3% in 4Q23). 3) The amount consumers are budgeting for home improvement projects moderated sequentially to a 15-quarter low of $5,851, or -24% Y/Y. 4) Home Depot maintained its market share leadership, but the gap to Lowe's narrowed to the slimmest margin yet in GHRA’s survey.

Edition: 184

- 19 April, 2024

Consumer Discretionary

Feb sales trends are significantly stronger than Jan and 4Q23 trends, according to Verbatim’s latest channel checks. Higher prices, product availability, warmer weather and promotions are the major factors driving Traffic and Ticket counts. Home improvement, gardening and cleaning are among the top selling product categories. Respondents indicate that their stores are either gaining or seeing no change in their market share and that prices are mostly increasing at an average of 2-3%. Hiring is easier, while wages are trending up. Online ordering is increasing y/y. Verbatim’s HD US Feb Comp Estimate is 0.0% vs. 4Q23 Actual Comp of -4.0%. Click here to access the full report.

Edition: 182

- 22 March, 2024

Home Depot (HD) & Lowe’s (LOW)

Consumer Discretionary

Gordon Haskett Research Advisors

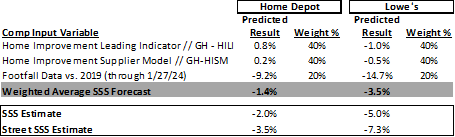

GHRA’s 3-factor predictive model points to upside potential to their 4Q23 SSS estimates for HD and LOW. Based on the weighted average results from their 1) Home Improvement Leading Indicator; 2) Home Improvement Supplier Model; and 3) Footfall traffic data, GHRA believes there could be upside to their estimate for HD of -2.0% (vs. predictive model of -1.4%) and LOW of -5.0% (vs. -3.5%). GHRA is bullish on both stocks, but leans more favourably towards HD given its significantly higher PRO penetration (as DIY faces steeper headwinds while PRO backlogs remain healthy); accelerating store growth; and incremental $500m of cost savings in FY24 that help mitigate EPS downside.

Edition: 179

- 09 February, 2024

Consumer Discretionary

Weakening trends - Verbatim's HD US Aug Comp Estimate is -3.5% vs. 2Q23 Actual Comp of -2.0%. Traffic levels are declining and customer spending is being negatively impacted by inflation, which is making customers focus more on essential spending. Click here to access the full report which also includes details on HD's inventory levels, promotions, market share and best selling products last month.

Edition: 169

- 15 September, 2023

AI driven 10Q / 10K filings analysis

Text discussions within financial filings contain material information - since there are always reasons when companies change their wordings, being alerted to these changes allows investors to realise potential risk factors and opportunities before they are reflected in the market, ideal for idea generation and portfolio monitoring. Recent highlights include Capri (market share fears / no more international expansion), Home Depot (rethinking dividend programme), Keysight Technologies (order cancellation & delays / competitors expand market position), Microchip Technology (ASP concerns) and Monroe (takeover target).

Edition: 164

- 07 July, 2023

Are you finding short ideas the right way?

Adam Parker of Trivariate Research provides a framework for finding “melting ice cubes” - he evaluated prior price performance (momentum over previous 12 months), accruals (disconnects between earnings and FCF), revenue (share loss), gross margins (relative to industry group contraction), earnings declines and downward earnings revisions as potential candidates for “cube identification”. Adam found that no other major fundamental attribute comes close to achieving the level of success at predicting subsequent underperformers as either accruals or momentum. Fundamental analysts who focus disproportionately on revenue share gain and margin contraction to find short ideas are wasting their time. Short ideas include Home Depot, Equinix and Micron.

Edition: 156

- 17 March, 2023

Consumer Discretionary

Likely just the beginning - Scott Mushkin downgraded HD to Sell at the start of the year as he saw a high probability that the home improvement sector would experience challenges going forward. He believed this would become evident in 2Q23, with pressure increasing through the end of 2023 and into 2024. HD’s latest report and guidance issues have only increased his conviction. As a result, Scott has cut his FY23 and FY24 EPS estimates to $15.43 (from $15.73) and $15.77 (from $16.23), respectively. TP reduced to $248.

Edition: 155

- 03 March, 2023

Consumer Discretionary

New high conviction short from Retail analyst Brian McGough - the bearish macro setup cannot be ignored. Brian thinks we could see the most rapid demand pressure ever in the space over 6-12 months. In the last housing recession, HD store comps were down 14 straight quarters and margins collapsed, yet the Street doesn’t have a single down quarter in its model. Brian’s base case EPS figure for FY23 is $14.78 but would not be surprised if the earnings number was closer to $12.00 (vs. consensus at $17.35)!! A 12-13x multiple would see the stock at $150 (50% downside).

Edition: 148

- 11 November, 2022

Corporate Access: 24 events hosted so far in 2022...

Peter Daniel hosts Zoom based calls with interesting industry (public & private companies) thought leaders for institutional equity investors. Highlights from this year include Tamara Lundgren (CEO, Schnitzer Steel); Lee Cooperman (Omega Family Office); Bill Rooney (VP- Strategic Development, Kuehne & Nagel); Ward Nye (CEO, Martin Marietta Materials); Scott Hamilton (President, Leeham Company); and Ken Langone (Co-Founder, Home Depot). Further details and a full list of all the events that Peter has hosted this year can be found here.

Edition: 148

- 11 November, 2022

Something to Snack On: Three that Should Thrive

Consumer Staples

Walmart, Target, and Albertsons, roughed up by last month’s choppy market, are now building momentum and recent pullbacks present buying opportunities. WMT-Home Depot partnership shows a positive business trajectory. TGT is creating an unrivalled total experience allying with Levi's, Apple and Disney. ACI's company specific initiatives, including streamlining purchasing and growing its private brands, show the business is strong.

Edition: 121

- 15 October, 2021