Fortnightly Publication Highlighting Latest Insights From IRF Providers

Company Research

Materials

HBM stands out among copper producers due to its unique gold leverage, sector-leading cost structure and exceptional growth profile. Its high gold by-product production substantially lowers copper cash costs, making it the lowest-cost copper producer in Veritas’ coverage last year as well as 1Q25. The company is also at a profitability inflection point, with Veritas forecasting 2025 EPS to be over 3x higher than in 2024 and HBM’s growth pipeline among the best in the sector, led by its flagship Copper World project in the US, a low-capex, high-IRR development that could expand the group’s copper output by 50%. And this is before Trump's announcement that he intends to impose a 50% tariff on copper imports!

Edition: 215

- 11 July, 2025

US copper continues to atrophy

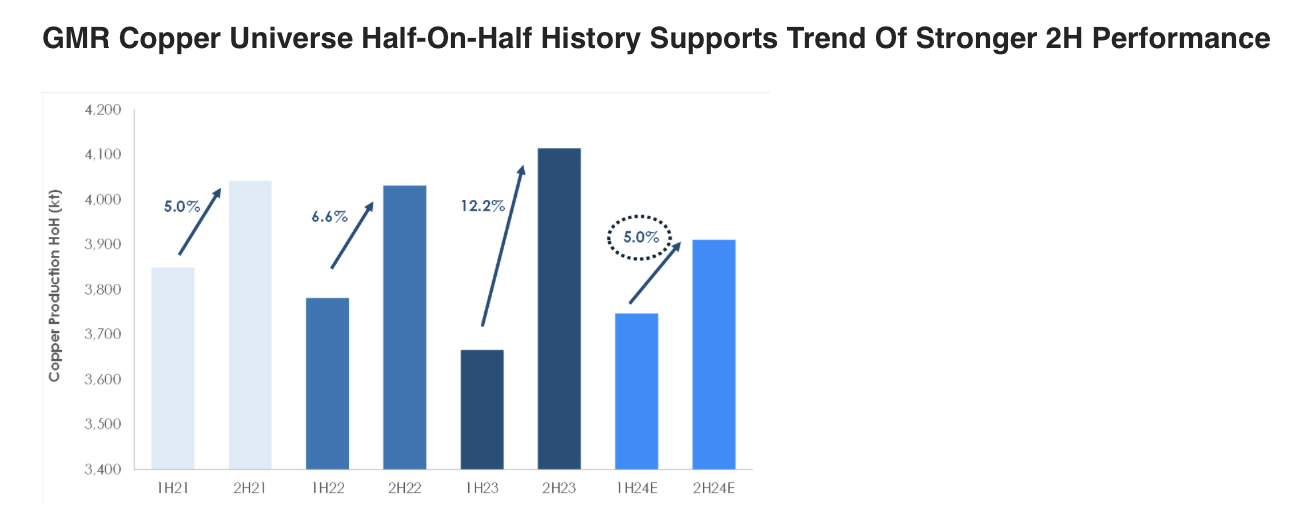

Political and legal challenges continue with few domestic US copper projects advancing (and some then failing), while existing production continues to mature (see chart). Ultimately, stagnation of US domestic production strengthens the upside case for the copper price. The US has the resource inventory to be self-sufficient, yet it is hard to see any of the key larger projects progressing in the mid-term. By the end of this decade, Global Mining Research sees incremental projects lifting volumes to ~1.3Mt/yr from current production at ~1.1Mt/yr. Preferred US-exposed copper plays are Freeport (upside from leach and Bagdad 2X), Taseko (Florence ISL expected to commence in 2025) and Hudbay (significant resource optionality).

Edition: 204

- 07 February, 2025

Copper: Risk to the downside

Copper prices had a strong start to the year. David Radclyffe’s review of the Q1/2024 performance versus 2024 guidance for the December year-end stocks helps put the market tightness into perspective. The key takeaway is that, as with gold companies, copper miners are banking on a strong H2/2024 to meet annual guidance figures. The risk is therefore to the downside, with once again copper producers struggling to either meet guidance or increase production appreciably. Only Hudbay Minerals, KGHM, Southern Copper, Freeport-McMoRan and First Quantum Minerals are tracking to 2024 production expectations. David’s preferred copper miners are in the small/mid-cap space on valuation grounds, including Atalaya Mining, Capstone Copper, Sandfire and Hudbay Minerals.

Edition: 187

- 31 May, 2024

Copper sector: Gold credits to shine

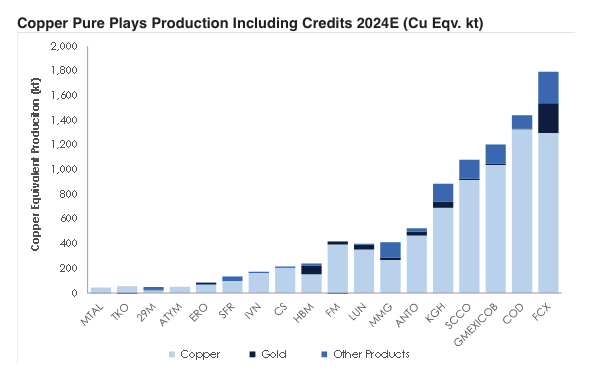

Commodity prices are overall moving in the right direction for the copper sector, with spot LME copper now at ~US$4.25/lb. However, many copper miners enjoy important by-product credits, including molybdenum, lead, zinc, silver and gold. Interestingly, precious metal credits have outperformed other by-products with gold at >US$2,350/oz. The sector is expected to generate ~82% of revenues from copper in 2024E with gold the next highest at ~6%. In 2024E, GMR’s copper universe is expected to produce ~2.2Moz of attributable gold production (~0.5Mt Cu Eqv.). However, analysis shows credits do not always correspond to the best position on the cost curve. Many copper miners don’t receive the full impact of higher precious metals credits due to streaming/royalty funding deals. The best way to play this “free kick” is through Hudbay Minerals, KGHM, and Freeport-McMoRan.

Edition: 184

- 19 April, 2024

Materials

In a bold and transformative step, SFR has announced it has beaten off peers to acquire the Minas De Aguas Tenidas (MATSA) operation in Spain - this is one of the largest copper transactions for some time and it is not cheap (GMR estimates SFR has paid the equivalent of US$3.90/lb LT). Investor interest in the stock is likely to increase significantly given the big jump in Mkt/Cap (it would notionally now have a larger capitalisation than both Hudbay Minerals and Ero Copper). Post deal the miner is trading at a prospective 1.0x P/NPV and 5.9x FY23 EV/EBITDA.

Edition: 120

- 01 October, 2021