Fortnightly Publication Highlighting Latest Insights From IRF Providers

Company Research

Interfor (IFP CN) Canada

Materials

Lumber prices are already showing signs of improvement and as interest rate cuts continue into 2025, ERA anticipates that ramping demand and constrained supply will drive prices meaningfully higher. On supply constraints, potential Trump tariffs on US lumber imports from Canada and Europe could limit supply in the US, leaving the US South as the sole source of growth next year. Prior sawmill closures and lingering labour challenges will be headwinds as the south looks to ramp up output. IFP is relatively well positioned compared to its Canadian lumber peers in terms of softwood lumber duty exposure (same goes for any additional US tariffs). Meanwhile, stronger FCF generation in 2025 will allow IFP to address investor concerns re. net debt. TP $30 (55% upside).

Edition: 199

- 15 November, 2024

Lumber prices remain in uptrend

Lumber prices remained in an upward trend last week, driven by a myriad of supply-side factors, while demand remained steady at best. S-P-F 2x4 prices finished the week up another $10 at $375, while SYP 2x4s were one of the few products that did not see w/w increases and were unchanged at $334. A looming rail stoppage in Canada and an indefinite curtailment announcement by Interfor (a combined 330MMbf of annual capacity at Meldrim and Summerville) caught buyers’ attention, but lumber takeaway was hampered by inclement weather across large parts of the US South. ERA anticipates that prices will continue to grind modestly higher over the coming weeks as builders gear up for the fall construction season, although a more appreciable improvement in demand may remain elusive until spring 2025 as markets await a first Fed rate cut.

Edition: 193

- 23 August, 2024

BC lumber producers facing it tough

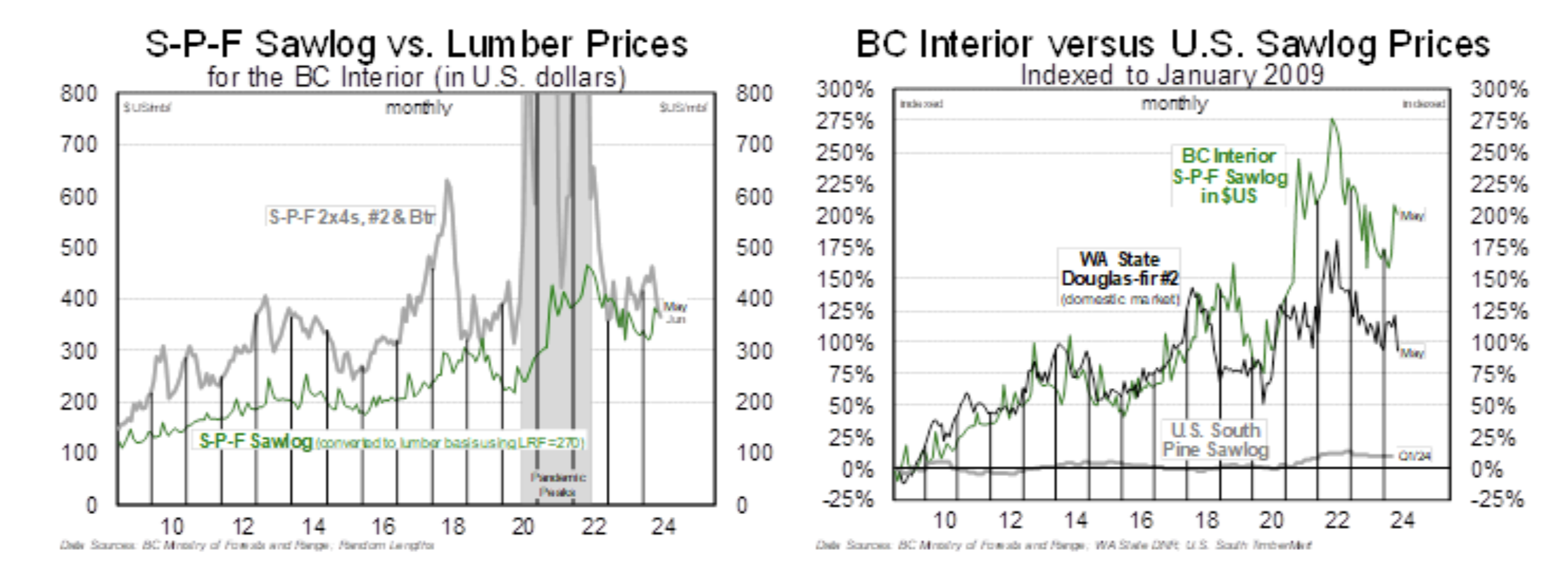

BC log costs are moving higher again (chart 1), and with S-P-F lumber prices rolling over—2x4 prices recently declined to $332—the ERA Forest Products team believe that the majority of BC sawmills are losing money today. Lumber prices are slumping across all species and dimensions, but log costs in BC are significantly higher (chart 2). More downtime is needed in all regions to remedy the issue. How to trade it? Most names will see limited further downside from current levels and upside catalysts remain elusive for now. The team do see long-term value in Canfor ($18 target price), Interfor ($22) and West Fraser ($116) but recommends that investors wait until at least Q4/2024 before building long positions.

Edition: 190

- 12 July, 2024

OSB prices moving higher again, further increases expected

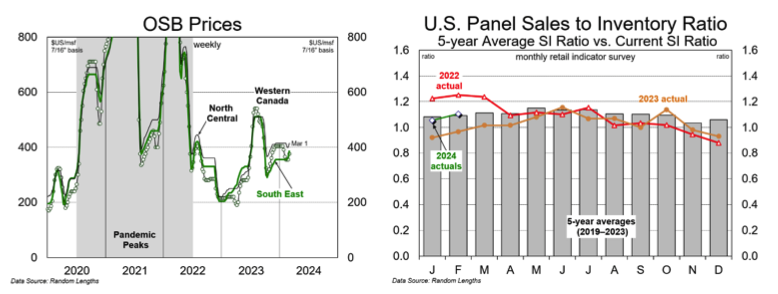

After posting modest declines earlier this year, OSB prices have rebounded from the mid-February low of $411 to $439 (chart 1). At the same time, indicators show US structural panel dealers’ sales-to-inventory ratios are moving higher (chart 2). The ERA team suspect that many OSB buyers delayed wholesale inventory replenishment when it looked like prices were set to roll over this quarter. However, when prices abruptly reversed, they were forced to pull out of their PO books, leaving OSB producers in the seat once again. In the near term, further OSB price increases seem assured and whilst the team sees risk of oversupply for OSB in H2/2024, their outlook has become less negative. Trade recommendations are more focused on the next US housing upcycle as opposed to a seasonal trade around spring building. Over the longer-term, the team sees most upside for TSX:Interfor ($26 target price) and NYSE:Weyerhaeuser ($39 target price).

Edition: 181

- 08 March, 2024

Interfor (IFP CN) Canada

Materials

Investors should start building long positions in IFP - while Q4 earnings were disappointing (and Q1 earnings may be only marginally better), ERA expects lumber demand from residential construction to improve steadily as the year progresses and a raft of sawmill capacity closures this quarter should also help further improve lumber’s supply and demand balance. IFP’s geographic diversity remains its strong point (it has the lowest relative exposure to high-cost BC at just 14% of sawmilling capacity) and a series of forest tenure sales on the BC Coast will continue to boost liquidity over the next several quarters. TP of $26 is based on a 7.0x multiple applied to 2024E EBITDA of $287m. 30% upside.

Edition: 180

- 23 February, 2024

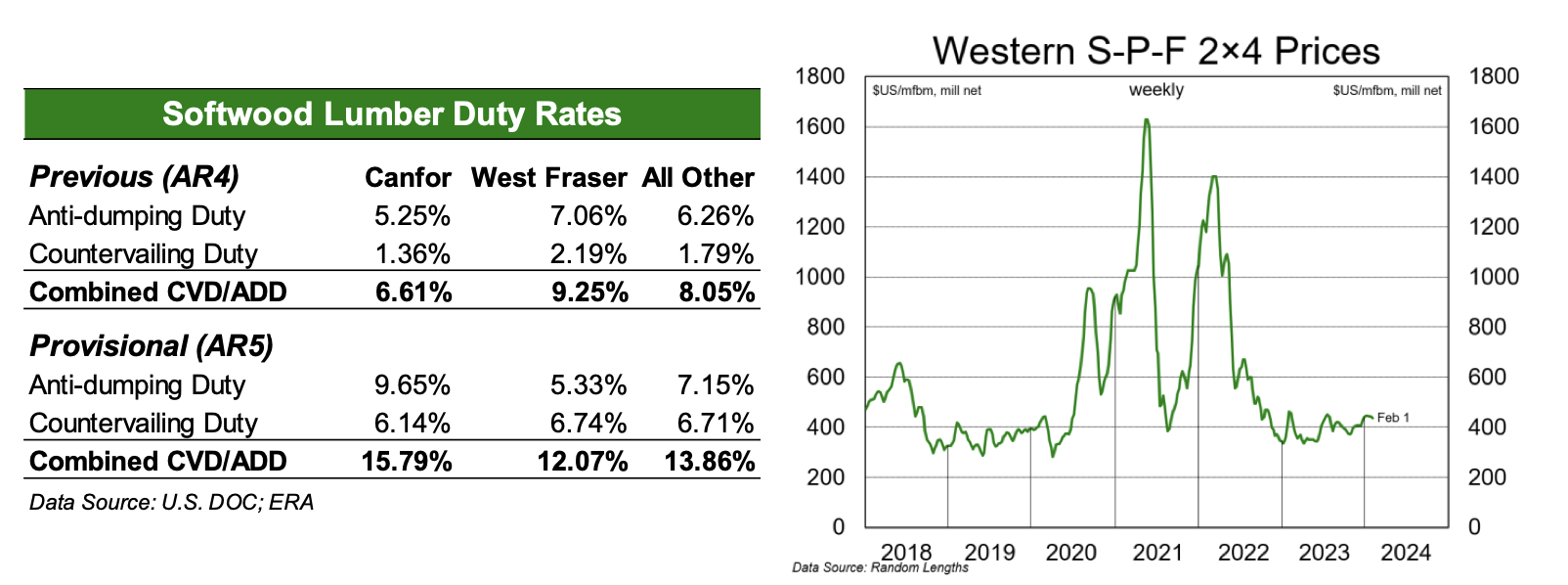

Softwood lumber duties set to move higher this summer

Preliminary results of the US Department of Commerce’s fifth administrative review into the 2022 North American lumber market sees an increase in combined duty rates, pointing to the potential for significant rate increases for next year’s review. Looking to 2023, S-P-F 2x4 prices averaged just $391 and spent most of the year near, or below, cash-cost levels; the ERA team expect that overall duties could increase sharply for the next review. So, who wins? US-based lumber mills (and perhaps Europeans exporting to the US) are the only winners as onerous softwood lumber duties increase Canadian producers’ costs. The release of the preliminary duties does not change ERA’s view on lumber equities, who sees upside from current levels for all lumber names given expectations for a sustained recovery in US housing. Interfor remains their top pick (target price $28), with West Fraser (TP: $116) and Canfor (TP $25) also seeing upside.

Edition: 179

- 09 February, 2024

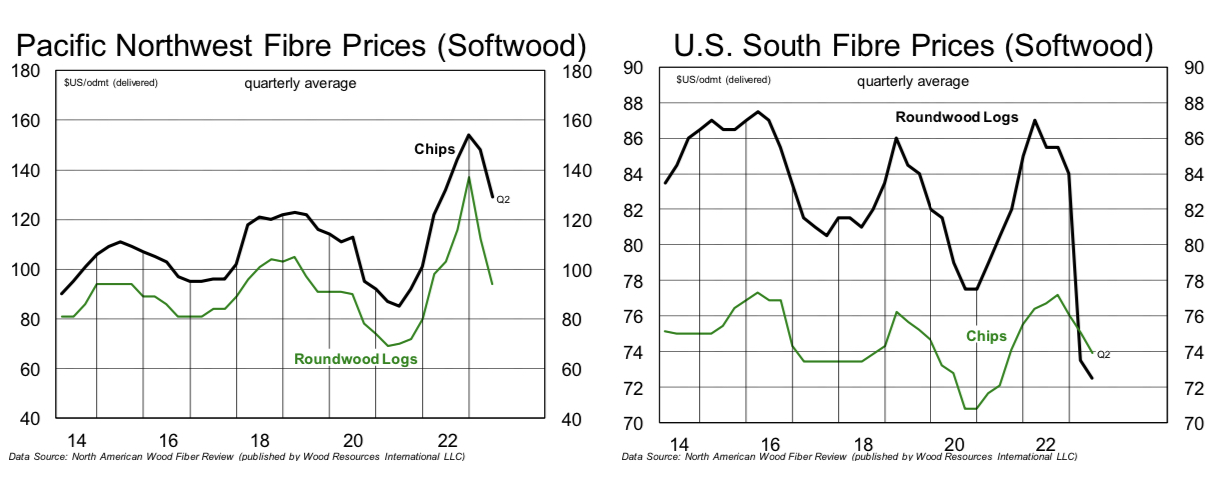

Falling pulp prices will drive down chip revenues for lumber producers

With pulp prices declining, the usual ones will win: low-cost lumber producers who have relied less on by-product revenues for sawmill profitability. This includes the fleet in the US South, where chips and thinnings have been abundant relative to demand for a long time. The ones that will lose are the lumber producers that were already stretched before the pulp-fibre price collapse, including producers in BC. However, rising S-P-F lumber prices will support BC mills in the near-term. Interfor remains the preferred route to lumber exposure; although they see long-term value in the name, they do not foresee a sustainable upcycle until later this year.

Edition: 164

- 07 July, 2023

Lumber: Chopped down

SYP lumber prices are falling, closing the gap with depressed S-P-F levels. Low prices should induce curtailments/closures, but many high-cost producers are resisting; painful quarters await. Panel prices have peaked. Oversupply will become an issue for OSB, requiring supply discipline. Share prices remain depressed (unsurprisingly); however, the ERA Forest Products Research team don’t expect much upside until late 2023. Interfor is their preferred way to play any short-term rally, as well as the long-term thesis.

Edition: 162

- 09 June, 2023

Interfor (IFP CN) Canada

Materials

IFP has the lowest exposure to BC (with its high log costs and exceptionally weak S-P-F prices) of the publicly traded Canadian producers, while 45% of its capacity is in the US south where sawmilling margins will remain healthy courtesy of outperforming SYP prices and consistently low log costs. IFP’s Q1 earnings outperformed peers and ERA expects this to repeat in Q2. As such, they are recommending a short-term trade (TP c.$30), but recommend that investors keep their fingers on the trigger and exit if near-term lumber price appreciation (most likely spurred by further sawmill downtime) isn’t forthcoming. Looking further out, their 9-12-month TP is $34 (60% upside).

Edition: 161

- 26 May, 2023

Interfor (IFP CN) Canada

Materials

4Q21 results will be boosted by the late-year pricing rally and following a remarkable start to the year 1Q22 is shaping up to be a blockbuster - lumber prices have rocketed higher over the past two months with supply interruptions (BC floods and Covid-related worker absences) a bigger driver than (steady, if unspectacular) demand. ERA continues to like IFP’s geographic diversity (and limited exposure to high-cost and freight-challenged BC) and its acquisition of EACOM strengthens this position further. TP increased to $55 (35%+ upside), based on a conservative 4.0x multiple applied to a 75/25 blend of 2022E/2023E EBITDA of $874m.

Edition: 127

- 21 January, 2022