Fortnightly Publication Highlighting Latest Insights From IRF Providers

Company Research

Saint-Gobain (SGO FP) France

Industrials

Following publication of its FY24 registration document, Iron Blue increases their SGO score to 27/60 (newly top quartile). This principally reflects FY24’s P&L benefit from compression in the expense for inventory and bad debtor impairment provisions, which could provide a tough comp effect in FY25. They also note two new contingent liabilities related to a new Grenfell Tower claim brought against SGO subsidiaries as well as assumed Australia asbestos liabilities with FY24’s CSR acquisition. For the first time the FY24 annual report quantified SGO’s reverse factoring activities (€106m). Iron Blue continues to flag sustained stripped out costs and an elevated gap between PPE capex and the P&L depreciation charge.

Edition: 223

- 31 October, 2025

DCC (DCC LN) UK

Energy

Following publication of the company's FY25 annual report, Iron Blue increases their DCC rating +3 pts to 27/60 (newly top quartile / fertile grounds for shorting). Key changes vs. FY24: 1) Higher one-off costs: FY25 stripped out restructuring expense increased to 7% of PBT adj, highest in 7 years. DCC also stripped out from headline earnings £74m goodwill impairment. 2) Took £17m profits on disposal of PPE inside underlying profits in FY25, the highest figure in the past decade. 3) P&L expense for inventories write-downs dropped to a decade-low of £5m. 4) DCC continued its strategy of promoting top management from within, with internal promotions to the CFO and newly created COO roles. 5) In its principal risks assessment, DCC highlighted Y/Y risk increases concerning the DCC Technology strategic review and also the impact on its operations from higher tariffs.

Edition: 222

- 17 October, 2025

Galderma (GALD SW) Switzerland

Healthcare

While GALD shares have performed well since the company’s IPO, the stock remains in a "discovery phase", in which its valuation appears expensive amid consensus estimates that do not fully appreciate the underlying fundamental opportunity. Over 50% of cash flows are derived from Botox and dermal fillers, positioning GALD in a duopoly market with a wider moat and longer growth runway than traditional beauty peers. GALD's core skincare business is growing ~10% annually (relative to L’Oreal’s sub-5% revenue growth), driven by exposure to higher value, nascent life cycle segments. The investment case is further supported by the company’s new eczema treatment, Nemluvio, which could generate $5bn+ in sales vs. management’s $2bn guidance. TP CHF230 (60% upside).

Edition: 220

- 19 September, 2025

MSCI emerging markets pullback in process

The EEM-US broke below its 20-day MA for the first time in over three months. Any potential pullback to major base support ($46) should be considered a buying opportunity. As discussed in Vermilion’s weekly Int’l Compass reports, EM countries that they are overweight include South Korea and Greece. Additionally, there continues to be several other countries that are bullish and/or worthy of overweights, including South Africa, Taiwan, Hungary, Czech Republic, Poland, Vietnam, UAE and Pakistan. Turning to China, the Shanghai Composite displays a significant base breakout, and China has been a favourite country to add exposure to over the past month (July 3 Int’l Compass titled “China and Japan Breaking Out” and also July 22 Int’l Macro Vision). As long as base support holds on this pullback, David Nicoski remains bullish and he is monitoring China for a potential upgrade to overweight.

Edition: 217

- 08 August, 2025

Pernod Ricard (RI FP) France

Consumer Discretionary

Woozle’s Q1 channel checks reveal a sharper-than-expected revenue and volume decline with clear underperformance vs. Bloomberg estimates and accelerating market share losses. Despite some stabilisation from pricing actions and marketing efforts, underlying consumer demand remains weak, product innovation execution is poor and competitive pressures are intensifying. In North America, organic revenue fell -3.6% Y/Y, with 83% of respondents reporting declining volumes and 50% missing internal targets. In Europe, organic revenue dropped -1.3% Y/Y, with 60% of buyers citing flat or negative growth. Aperitifs and RTDs performed best across North America, while no clear standout category emerged in Europe. Key sub-brands like Suze and Pastis 51 showed strength, whereas Chivas, Olmeca and L’Orbe underperformed.

Edition: 209

- 18 April, 2025

Healthcare

Following publication of its FY24 annual report, Iron Blue increases their CTEC score to 28/60 (top quartile / fertile grounds for shorting). Reductions in inventory & bad debtor impairment provisioning contributed 36% of FY24’s Y/Y rise in PBT adj while the trend of restructuring and asset impairment provisions strip outs continued. The gap between PPE/software capex and the P&L D&A charge narrowed Y/Y but remained elevated at 16% of PBT adj. Receivables factoring increased to $43m (FY23: $27m, FY22: nil) while working capital days outstanding compressed to a decade low 47 days (FY23: 57), implying risk of future mean reversion. CTEC lowered the discount rate used to impairment test its goodwill to a blended 10.3% from 13.3% in FY23. This is now below the 11.5% average for Iron Blue’s coverage universe.

Edition: 208

- 04 April, 2025

L’Oreal (OR FP) France

Consumer Staples

Woozle’s 1Q25 channel checks reveal organic revenue trends that are materially below consensus estimates. European organic growth of 1.3% lagged Bloomberg’s 2.4% forecast, reflecting subdued consumer demand entering Q2. While targeted promotions stabilised volumes in Skin Care and Hair Care, high-margin categories like Derma and Fragrance underperformed, creating margin headwinds, particularly amid increased discounting pressure in the UK and Italy. Despite widespread price hikes in the Americas, consumer shifts toward lower-priced alternatives indicate weakened elasticity, while flat-to-slightly-up pricing in Europe masks underlying trade-down risks. Inventory conditions were mixed, with optimal stock levels in Europe contrasted by excess inventory in struggling US categories. Additionally, new product launches failed to significantly drive growth.

Edition: 208

- 04 April, 2025

Consumer Discretionary

Janet Kloppenburg was impressed with BURL’s Q4 results and the company’s long-delayed 2.0 plan is now unfolding, supported by supply chain improvements and a shift towards an off-price sourcing model. BURL is also benefitting from acquiring its distribution centres, which enhances cost control. A more experienced buying team has helped to stabilise brand quality and product flow. Higher AUR levels also provide evidence that a higher quality consumer (who wants a deal) is now considering BURL as a value shopping alternative. Janet’s FY25 EPS estimate is $9.30, but looks for upside opportunity throughout the year with infrastructure now better prepared to drive +L to +MSD comps and greater margin and earnings flow through.

Edition: 207

- 21 March, 2025

Consumer Discretionary

New CFO Cath Smith has destroyed a total of (192%) alpha at seven different public companies since 2005. Her below-average ManagementTrack Rating of 3.0 is a downgrade to outgoing Rachel Ruggeri's MTR of 4.3 and will lower SBUX's C-Suite Rating despite CEO Brian Niccol's 8.1 MTR. Smith is classified as a: 1) "Capital Returner" Capital Allocator: 59% of career capital allocated towards Dividends and Buybacks. 2) High F.L.A.G. Risk Concern with a "Bad Compliance Record". 3) Inconsistent Guidance Forecaster: beats 35% of guidance given, misses 17%, in-line 48%. 4) Less Evasive on earnings call Q&A: during her Nordstrom tenure, JWN was ~27% evasive vs. SBUX's C-Suite ~33% evasive over the past five years.

Edition: 206

- 07 March, 2025

IMI (IMI LN) UK

Industrials

Iron Blue initiates coverage on IMI with a score of 26/60, which is top quartile and fertile grounds for shorting. They highlight: 1) Dependence on December revenue recognition. 2) Sustained and elevated stripped out restructuring expense (11% of FY23 PBT adj) & associated use of provisions accounting. 3) Stripped out acquisition software and R&D amortisation (3% FY23 PBT adj). 4) P&L inventories impairment expense reduced to 0% of FY23 PBT adj from 5% in FY20. Iron Blue also notes an internal succession approach for the CEO/CFO roles, sub-optimal controls and many disclosure gaps.

Edition: 204

- 07 February, 2025

Consumer Discretionary

New CEO Jim Conroy added to Paragon’s research pipeline - Conroy joins ROST from Boot Barn, where he created 640% alpha as CEO since 2012. However, his ManagementTrack Rating of 5.7 is a modest downgrade vs. the outgoing CEO Rentler's MTR of 7.0. Other stats include: Conroy is a "Builder" capital allocator: 70% of career capital allocated towards CapEx (Rentler is a "Capital Returner", allocating 69%+ towards Dividends & Buybacks). Conroy is an "Inconsistent Guidance Forecaster": Beats 49% & Misses 39% of the time (Rentler is a "Guidance Sandbagger": Beats 87% & Misses 7%). He has a low F.L.A.G. Risk Concern and very low historical Earnings Call Q&A Evasiveness (Conroy averaged 10% vs. Rentler's 27% over the last 5 years).

Edition: 198

- 01 November, 2024

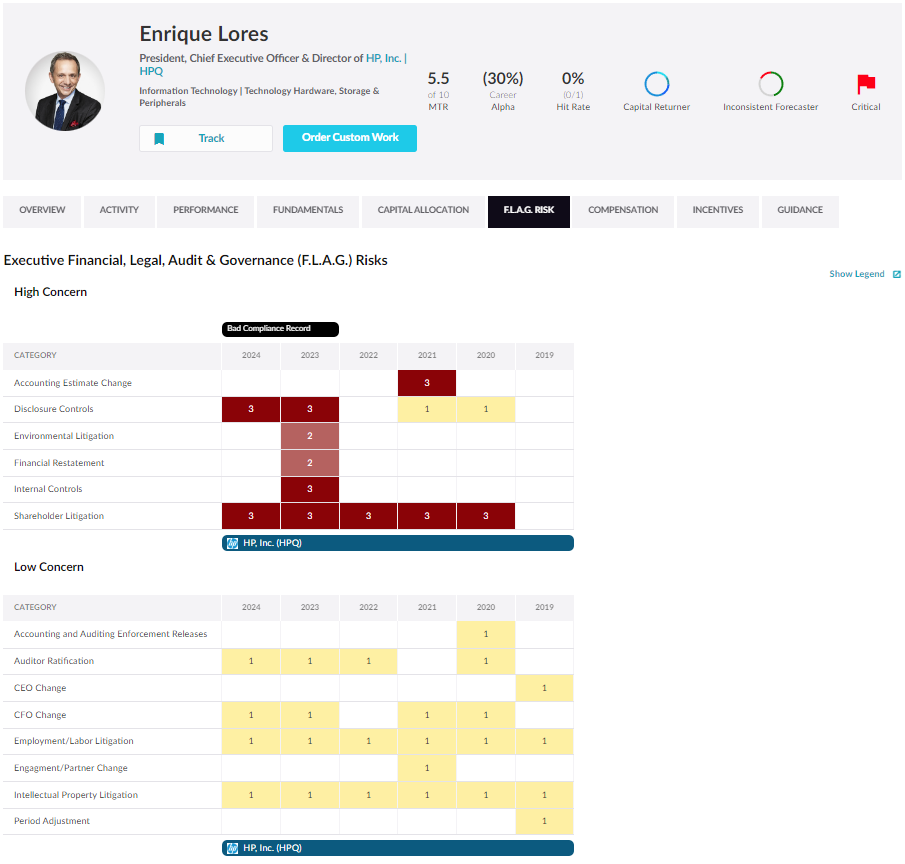

Financials

Enrique Lores replaces John Donahoe as Independent Board Chair. Lores has overseen more than 98% alpha destruction as a member of PYPL’s board since he joined in 2021 and has not created alpha as a CEO nor a board member in his career. In 2023 he received a "Bad Compliance Record" tag because of his "Level 3" Disclosure Controls and Internal Controls F.L.A.G. (Financial, Legal, Audit, Governance) Risks at HP Inc. Paragon also cautions about his incentive compensation - after only hitting 56% of his incentive targets from 2020-2022, Lores was able to convince the board to materially lower his 2023 incentive thresholds...and he was able to meet or beat all of those targets last year.

Edition: 192

- 09 August, 2024

Consumer Staples

CFO-Elect Monish Patolawala's ManagementTrack Rating* of 0.8 is in the bottom 4% of the 1,250 CFOs on the platform and is a significant downgrade to the 5.3 MTR of ADM's existing C-Suite. Patolawala destroyed (113%) alpha as a CFO at 3M; he has 9 "Level 2 & 3" career F.L.A.G. Risks (Financial, Legal, Audit, Governance Flags); a mixed incentive hit rate (achieved 50% of his incentive compensation targets 2020-2023); and is classed as an Inconsistent Sandbagger Guidance Forecaster (beats 51% and misses 28% of his financial guidance to investors).

*The MTR model employs a statistical ML algorithm to predict executive / company outperformance relative to their sector. It utilises 200+ signals and over a 10-year back-test a MTR long-short portfolio generated an average annual alpha of 8% with a 90% hit rate.

Edition: 190

- 12 July, 2024

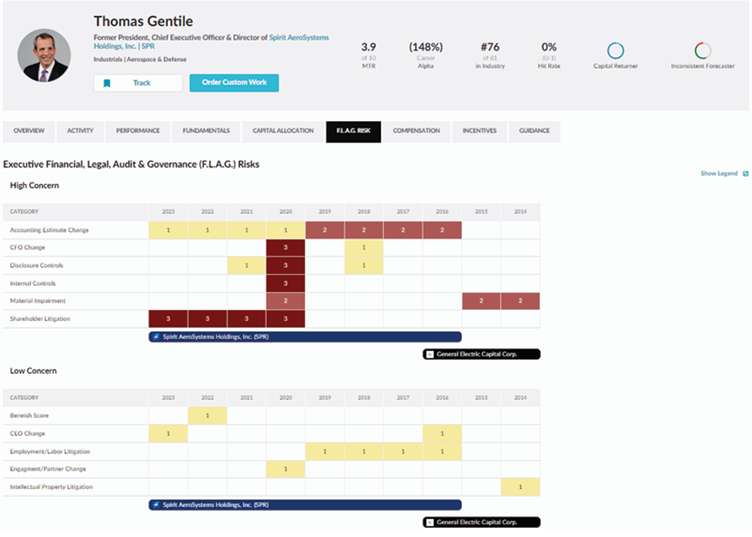

Industrials

Incoming CEO Thomas Gentile appears to be a downgrade to the already under-performing CEO seat at HXL with (147%) career alpha destruction compared to Nick Stanage's (77%). While Gentile brings less "Level 2 & 3" F.L.A.G. Risks than Stanage; his 14 is still considered to be high across all the executives on Paragon’s ManagementTrack platform. Investors should not expect more consistency in trusting guidance from Gentile - he was classified as an “Inconsistent Forecaster” during his tenure as CEO at Spirit AeroSystems. Furthermore, he does not possess a track record as a C-Suite executive of increasing revenue or margins - at SPR revenue declined (26%) and Adj. EBITDA margins declined by (1,470 bps). He left the firm after production problems resulted in the shares declining more than (40%).

Edition: 184

- 19 April, 2024

Saint-Gobain (SGO FP) France

Industrials

SGO’s Iron Blue score increases to 26/60 (newly top quartile / fertile grounds for shorting). This reflects an expanded gap between PPE capex and the P&L depreciation charge (14% of PBT adj, vs. 11% and 7% the two previous years) and another increase in receivables factoring (+6% y/y, +40% since FY20). Stripped out one-off costs remained elevated (10% of FY23 PBT adj). A new contingent liability was named in FY23 concerning competition authority investigations into the additives and admixtures sector in the EU, UK and Turkey, while class actions were instituted in the US and Canada. SGO has also continued to consolidate its Russian operations despite seemingly operating independently from the rest of the group. Iron Blue calculates that €112m of gross cash was stranded in Russia.

Edition: 183

- 05 April, 2024

Playing steep vs safe: CHF/JPY

Andreas Steno finds it increasingly likely that the BoJ will kill the world's last negative policy rates. As an anchor to this view, he finds the CHF safe haven to be a tad overstretched. While Andreas doesn't see any massive inflation problem in Japan, he notes that vanilla forecasts are hinting at higher core pressure and that the services component has yet to capitulate. As a result, he thinks it prudent to be long JPY in relatively carry neutral expressions. The SNB will likely have to follow suit when the G10 cutting cycle commences, while the BoJ can accept to be the odd hawks out for a while due to the exceptional weakness in the JPY over the past few years. He opens a new FX position: SHORT CHF/JPY, target 159.60, S&L 172.35 (spot-ref 170.55).

Edition: 179

- 09 February, 2024

Will 2024 be the start of significant UK interest rate cuts?

Last week saw the PM Rishi Sunak suggesting an autumn UK general election, consistent with David Owen’s last note on the UK. August could be a pivotal month for the BoE’s MPC, with one further meeting (19th Sept) before a possible Oct 10th poll. In the interim, Deputy Governor Ben Broadbent and Jonathan Haskel - who again voted for a rate rise at the last meeting – will step down and Chief Economist Huw Pill’s and Catherine L Mann’s appointments will likely be renewed. A changing composition at the MPC could also have a bearing on what happens to UK monetary policy later in the year. However, David remains far from convinced that 2024 will be the start of the significant rate cuts priced into the curve. He has written before about the biases in the market and amongst many commentators hoping to see the return of much lower rates.

Edition: 177

- 12 January, 2024

Consumer Discretionary

Better high growth stores, convenience and popular deals boost Nov comps. Verbatim's latest channel checks reveal high-end luxury brands including The Ordinary, e.l.f. Cosmetics, Benefit Cosmetics and Tarte Cosmetics have been the top sellers. Inventory levels are just right, however one of Verbatim’s sample respondents reported shortages in brands such as Lancome, Murad and COSRX. Prices across their sample are rising at an average of $2 and mostly on fragrances. Hiring new employees is easier due to the increasing wages and applicant interest. Labour hours are consistent Y/Y. Online ordering is increasingly popular as stores fulfil 20 orders a day on average. Verbatim’s Nov Comp Estimate is +5.3% vs. 3Q23 (Aug-Oct) Actual Comp of +4.5%.

Edition: 176

- 22 December, 2023

China: Improving health?

Niall Ferguson and his team spent a week in mainland China and Hong Kong, speaking to authoritative policymakers, academics, entrepreneurs and financial elites about the country’s economy. They also engaged in high-level diplomatic talks between China and Australia over the past month. Now, Niall is even more convinced that some of the worst financial and macro-economic risks to the economy have passed, with some silver linings or green shoots emerging in key sectors, particularly EVs and green tech. On geopolitics, we are entering a period of sustained détente between China and the US. China’s economy isn’t out of the woods yet, but the recovery now resembles more of a U-shape than an L-shape.

Edition: 175

- 08 December, 2023

Beiersdorf (BEI GR) Germany

Consumer Staples

BEI trades at an unwarranted 30% discount to L’Oreal - Alex Dwek sees untapped improvement potential for Nivea under a new leadership team focused on globalising / modernising the brand with bigger, fewer, and more impactful innovations and global marketing campaigns strategically focused on skin care to accelerate growth in large markets like China and the US. Alex also expects Eucerin to gain market share in dermocosmetics (a market growing double digits) and La Prairie to grow in the luxury segment. He forecasts MSD revenue growth for the foreseeable future and a margin expansion reaching 15.5% by 2025.

Edition: 175

- 08 December, 2023

L&T Finance Holdings (LTFH IN) India

Financials

LTFH faced a substantial INR 26.9bn loss, up to 20% on its FVTPL book, in FY23 due to an accounting policy change involving the reclassification of wholesale loans to fair value. Despite seemingly improving non-performing asset numbers, LTFH's low loss allowance for reclassified loans, coupled with losses on loan sales, raised concerns about its asset quality and disclosure practices. Moreover, inconsistent fair value changes, a puzzling treasury operation and past provisioning flip-flops added to the uncertainty surrounding the company's financial performance and its transition towards retailisation under the banner of Lakshya 2026. The true motivations and hidden costs of this transformation warrants attention!

Edition: 170

- 29 September, 2023

L'Oreal (OR FP) France

Consumer Staples

100% of retailers interviewed by Woozle reported that the cosmetics giant is “clearly strategically outperforming” competitors such as Estee Lauder and Beiersdorf brands, due to quicker innovation and better positioning around the natural, sustainable themes for self-care products. Woozle's latest channel checks (across US, Europe and Australia) suggest OR is trading ahead of consensus forecasts in 1Q23, driven by outperformance in L'Oreal Luxe and Consumer Products, partly offset by weaker than forecast Active Cosmetics sales growth. On the subject of pricing, respondents reported an average increase of 10% Y/Y for OR brands (vs. 7% increase for EL).

Edition: 155

- 03 March, 2023

American Eagle Outfitters (AEO)

Consumer Discretionary

AE brand continues to see higher promotional activity with full price and clearance assortments now offered at 25% off - while slowing consumer spending patterns are likely the primary reason fuelling deeper discounts, JJK are also disappointed in the BTS assortment’s innovation level across both men’s and women's ranges. At Aerie, a key concern is that inventory levels are tracking well above last year, while demand levels moderate. JJK expects discounts to deepen as 3Q unfolds, putting further pressure on the P&L. They cut their FY22 EPS forecast to $1.10 and see no improvement to top line / margin gains until 2H23.

Edition: 140

- 22 July, 2022

L'Oreal (OR FP) France

Consumer Staples

Paul Bulcke (Vice Chair since 2017) purchases €606k of stock at €303. He is on the board as a representative of Nestle (where he is Chair). It's interesting to note that Nestle reduced their ownership in L'Oreal from 23.3% to 20.1% in Dec 21 (at €400) and to see Bulke now make his first ever direct purchase in the stock. Béatrice Guillaume-Grabisch (Non Exec since 2016) also recently purchased €133k of stock. This is only her second purchase and it's notable to see her now buying at nearly twice the price after a 5 year gap.

Edition: 139

- 08 July, 2022

SBM Offshore (SBMO NA) Netherlands

Energy

Despite a positive outlook for new orders SBMO shares still trade at a relatively high discount to NPV - highlights opportunities to win additional contracts with the likes of Exxon where FPSOs SBMO has been building are very efficient (breakeven price for the ONE Guyana FPSO is pegged at $29/BBL Brent). Analysts at the IDEA have previously demonstrated that each new FPSO contract could add up to €1 to €2 per share in the NPV of the company’s L&O portfolio. This value already amounts to between €19 and €23 per share based on discount rates of 8% and 6% respectively. SBMO shares currently trade at €13.70.

Edition: 135

- 13 May, 2022

Spotting opportunities in Greek equities

Covering 22 names (80% of total M/Cap), ResearchGreece provides unbiased research, analysis and ideas on Greek (& Cypriot) equities. They offer a clear-cut, binary rating system: Own It (OI) or Do not Own It (DOI). Two stocks they are particularly keen on are…

National Bank of Greece (ETE) - Deserves to be trading at a higher P/TBV multiple than the current 0.50x; enjoys the highest FL CET1 among Greek banks; will benefit the most from a loan rate increase given its low L/D ratio; boasts the lowest combination of NPE ratio and NPE coverage.

OPAP (OPAP) - Q4/FY results comfortably beat expectations on stronger online contribution (Betting and Casino) and GGR/EBITDA guidance for 2022 points to ~40% growth Y/Y. In addition, the dividend was increased to €1.5/share (11% yield).

Edition: 133

- 14 April, 2022