Fortnightly Publication Highlighting Latest Insights From IRF Providers

Company Research

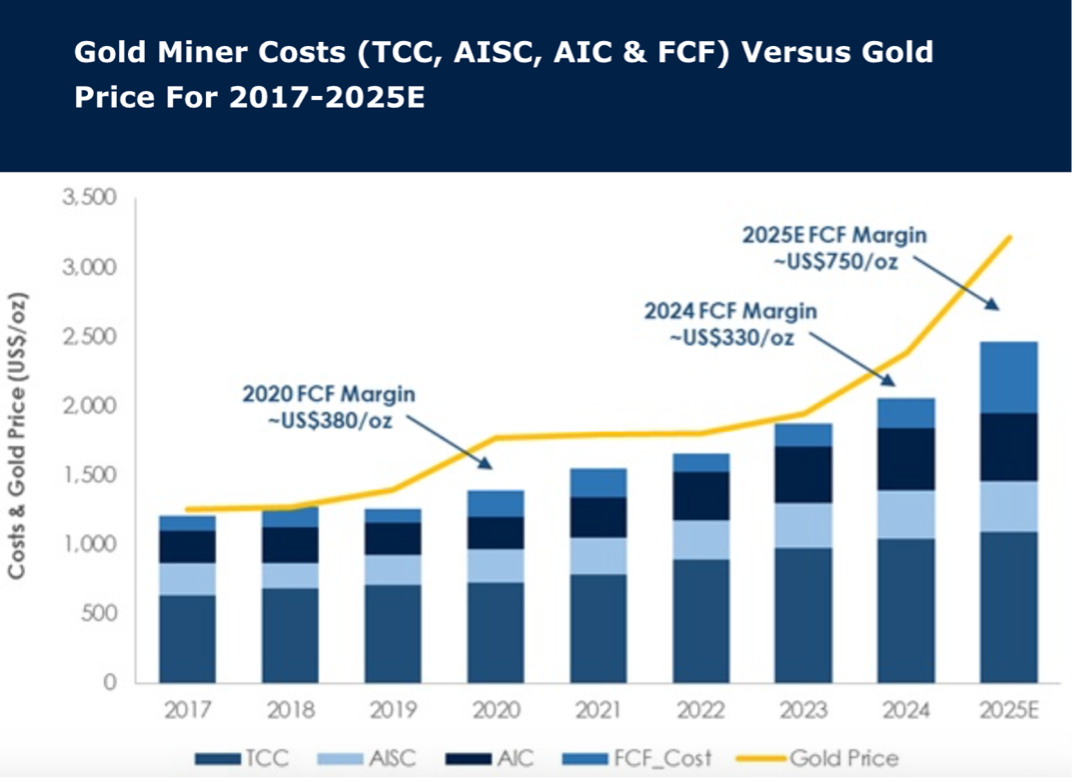

Gold: Higher prices, higher costs

As markets focus on record spot prices in 2025, price-linked costs and general mining inflation are also driving operating costs to record highs. In 2025 gold miner FCF costs are expected to reach a record ~US$2,465/oz, in line with inflation expectations. Positively, gold prices are rising faster and the 2025E FCF spot margin at ~US$750/oz is near double the last high in 2020. Gold miners (covered by Global Mining Research) with the lowest FCF costs in 2025 are Lundin Gold, Wesdome, Kinross and Agnico. Stocks with improvement in FCF costs from 2024 to 2025 are IAMGOLD, Torex and Equinox. Preferred gold stocks are BUY-rated Agnico (delivery and lower-risk portfolio), Kinross (risk reduction and execution), Equinox (transitions from project development to cash generation), IAMGOLD (Côté ramp up and derisking) and Lundin Gold (FDN continues to outperform).

Edition: 210

- 02 May, 2025

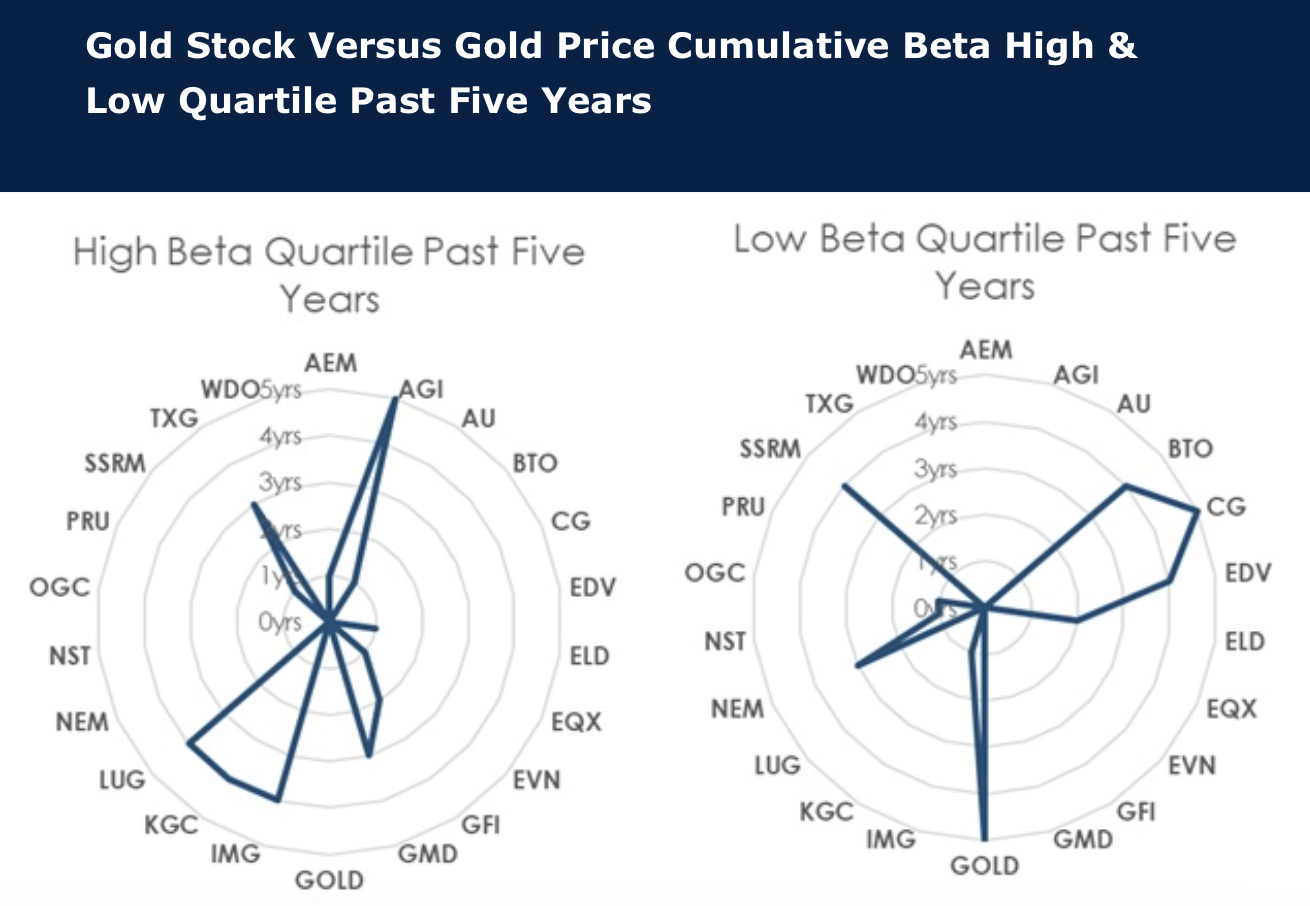

High beta gold stocks outperforming peers

The Global Mining Research team research the correlation of stocks to the gold price and the beta of those stocks. The stocks with consistently high beta to the gold price over the past five years are Alamos Gold, Genesis Minerals, IAMGOLD, Kinross Gold, Lundin Gold and Torex Gold Resources. Stocks with a weak beta to gold price over the past five years are B2Gold, Centerra Gold, Endeavour Mining, Barrick Gold, Newmont and SSR Mining (except 2025), each with mine or management issues, heightened risk or M&A troubles. Market preference for gold stocks appears to be more driven by investor perception rather than quantifiable valuation or sensitivity measures, and investors are preferring stocks with “issues” and aren’t seeking deeply discounted cheap stocks. Preferred gold stocks are BUY-rated Agnico (delivery and lower-risk portfolio), Kinross (risk reduction and execution), Equinox (transitions from project development to cash generation), IAMGOLD (Côté ramp up and derisking) and Lundin Gold (FDN continues to outperform).

Edition: 209

- 18 April, 2025

Gold: Can higher prices translate into cash?

All too often in the last decade for the gold sector, fully loaded costs have come close to equalling the received price. Therefore, one reason gold equities have likely recently lagged spot prices reflects a degree of market scepticism of the sector's ability to translate higher prices into “cash”. Unfortunately, the senior producers have often been key protagonists, but this isn’t the case for all gold stocks. Herein, David Radclyffe updates the sector cost analysis including highlighting Free Cash Flow (FCF) costs and FCF costs plus dividends, seeking to identify those stocks that could bank the proceeds of higher spot prices in 2024. The notional spot margin after base case dividends in 2024E for Agnico Eagle Mines / Barrick Gold Corp / Newmont is ~US$395/GEO, up from US$200/GEO in 2023. However, the best cash notional margins in 2024E could be delivered by Evolution Mining, Lundin Gold, Centerra Gold, and Barrick Gold Corp.

Edition: 186

- 17 May, 2024

Copper vs Gold

Gold miners have traditionally been considered premium rated miners, yet copper stocks covered by GMR have moved to a premium compared to gold and other base metal and bulk miners. Gold stocks are out of favour with valuations underperforming the gold metal price during 2023; the high beta of gold stocks presents an opportunity when the gold price gains traction. Preferred equities include Lundin Gold and Northern Star. Copper stocks remain attractive as supply weakness and low inventories are offset by macro concerns. Preferred stocks are Atalaya Mining and Taseko Mines as junior miners, and Sandfire amongst the mid-larger names.

Edition: 170

- 29 September, 2023

Canadian mines for Canadian owners?

The recent moves related to Teck Resources has prompted some jingoistic statements from mining participants and the government about Canadian ownership of Canadian assets. David Radclyffe examines the ownership of mines in the country, finding that, although Canadian gold mines are mostly owned by the country’s miners, Canada represents just one-quarter of the value of mines owned by Canadian domiciled gold stocks. Should the jingoism be contagious, Canadian miners will be the losers if the insistence of local ownership spreads. Preferred Canadian domiciled gold stocks are Barrick and B2Gold among the senior stocks and Lundin Gold as a junior stock.

Edition: 160

- 12 May, 2023

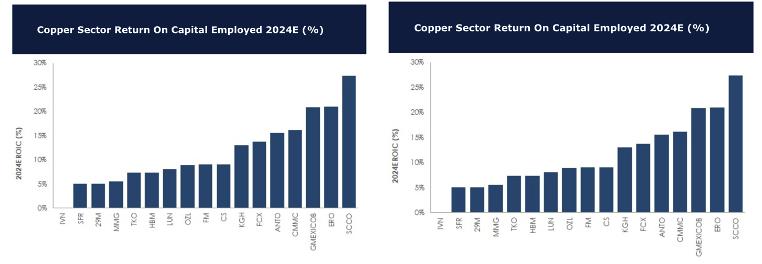

Returns on capital: Copper vs Gold

For 2024, David Radclyffe forecasts copper to enjoy an average ROCE of 11.1%. The standout is Southern Copper Corp, helped by some very low cost and long-lived assets. Relatively new to the market Ero Copper Corp does well, while at the lower end sit Ivanhoe Mines and Sandfire Resources. When it comes to gold, the forecasted average ROCE for 2024 is at 8.3%, with Gold Fields coming out on top and Lundin Gold close behind. The copper sector as a whole continues to generate better real returns on capital than the gold sector, with gold miners continuing to suffer from shorter mine lives and a commitment to M&A to create growth.

Edition: 155

- 03 March, 2023

Gold sector: 2023 looking positive (so far)

Gold prices will always be volatile but two of the unexpected headwinds of 2022, inflation and USD strength, have now peaked. David Radclyffe reviews the outlook for the sector in 2023. He expects gold equity inflows as price and margin pressures of 2022 abate and the potential for surpluses return. M&A is expected to continue, and significant C-suite turnover offers opportunities to reset stale strategies. Preferred stocks are Barrick, Endeavour and B2Gold for scale/value, Northern Star and Evolution for leverage to better gold/copper prices and Lundin Gold and Centerra for attractive potential in smaller caps.

Edition: 152

- 20 January, 2023

LatAM gold producers

One-fifth of global gold production is sourced from Latin America, but investors should be wary of the higher risk regions. David Radclyffe’s latest report examines these small but important nations. Key takeaways include Newmont remaining the preferred senior gold stock, and Torex (in Mexico) and Lundin Gold (in Ecuador) named as preferred mid-sized gold stocks with growth and value appeal in the region.

Edition: 123

- 12 November, 2021