Fortnightly Publication Highlighting Latest Insights From IRF Providers

Company Research

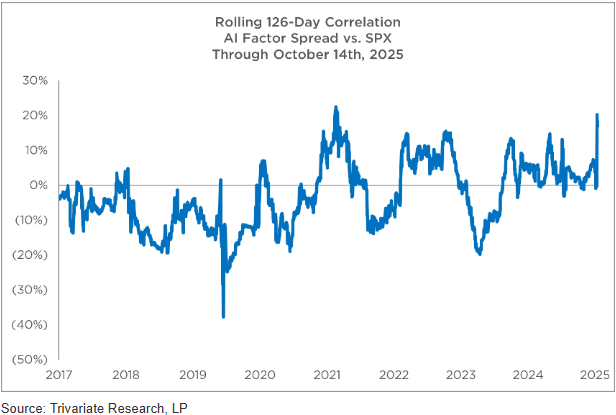

Blow-up avoidance guide - how are you dealing with the S&P500 being an AI factor bet?

While there are plenty of high-quality AI-exposed stocks to own, the challenge is that many non-Tech names have also become correlated to the AI trade. Trivariate screened for stocks with low correlation (<0.2) to their AI Semiconductors basket, that are up >10% in the past 6 months, top-half quality and beta <1 - identifying 28 stocks with a m/cap >$50bn. Given the recent huge moves in speculative names, Trivariate also advises preparing a sell/short list for a potential market rollover. They highlight 24 stocks ($1bn+ m/cap) that are up >100% in 6 months, in the most expensive EV/sales decile and the bottom half of their quality model, companies with high short interest and lower 2026 EPS estimates than at the start of the year, meaning the recent big moves in stock prices are despite a deteriorating nearer-term fundamental outlook.

Edition: 223

- 31 October, 2025

A compelling growth story

AIR highlights Spain as the Eurozone’s standout growth opportunity, further supported by US immigration tightening redirecting talent and labour. The country is benefitting from its strong position in the EU’s €750bn Next Generation EU program, minimal exposure to US tariffs and insulation from Chinese industrial competition. A rapid transition to renewables has driven a 40% decline in wholesale electricity prices over five years, while lower structural taxes and spending continue to support competitiveness. Preferred sector calls include Infrastructure (Acciona, Ferrovial, Sacyr) with robust project pipelines supported by public and private investment; Banking & Insurance (CaixaBank) benefitting from SME exposure and high household savings rates; Real Estate (Merlin, Metrovacesa) poised for catch-up gains vs. other European countries amid supply constraints; and Defence, where Indra Sistemas is well positioned for M&A.

Edition: 222

- 17 October, 2025

Consumer Discretionary

Brian McGough reiterates his bearish view on FND despite the stock’s ~50% drop since his Apr 24 short call (vs. the S&P +33%). Brian is updating his analysis using his M.A.P.S. (Market Area Performance Study) framework, which tracks store performance by opening cohort. His latest findings suggest that stores opened in 2024 & 2025 are performing even worse than earlier cohorts, reinforcing that FND’s weak comps are structural, not cyclical. New units also show rising market overlap with the likes of Home Depot and Lowe's. While FND is often seen as a housing-recovery play, Brian expects another ~30% downside as earnings, growth guidance and unit expansion continue to disappoint.

Edition: 222

- 17 October, 2025

Capital Markets at Risk: Jefferies echoing Bear Stearns

Financials

Charles Peabody believes we are in the mature phase of the capital markets cycle, with revenues likely topping out in 2026, while stocks are expected to turn lower well before then. He recommends selling Morgan Stanley and Goldman Sachs on near-term strength. Credit and liquidity stresses are emerging following the automotive credit, Tricolor and First Brands developments, while syndicated loan offerings are being pulled. He sees echoes of Bear Stearns at JEF, noting that MS and BlackRock have ended relations with Bonita Point, the JEF subsidiary housing First Brands receivables, just as this rapidly growing broker reached top-tier status. Sell Capital Markets, Buy NII - he favours Citi, M&T, Citizens Financial and UBS.

Edition: 222

- 17 October, 2025

Communications

Hesham Shaaban initiates a new tactical long in RBLX, arguing that the recent sell-off following the M Science report has created a “coiled spring” setup ahead of 3Q25 results. His analysis indicates that Concurrent Users have accelerated each month through Q3 and into Oct, contradicting perceptions of a slowdown. He believes the M Science data may not fully capture RBLX’s expanding user base, underestimating bookings growth. If platform activity trends hold, even modest monetisation could yield a double-digit bookings beat for Q3 and stronger Q4 guidance. With the shares up >100% YTD, Hesham expects short exposure to increase into the print, meaning any upside surprise could trigger a sharp rebound if results confirm his thesis.

Edition: 222

- 17 October, 2025

Can a demand sanction on Chinese biotech help US companies?

Healthcare

Blue Lotus examines the early-stage pipelines of 25 Chinese biotech companies (CBT), covering 177 drugs and 278 rival drugs worldwide across 80 biotargets. CBT claims 5 dominant leads, 8 competitive leads and 8 co-leads. Of the remaining 59 biotargets, US biotech companies (USBT) hold leads in 43, of which 31 face "me-better" Chinese competition and 12 "me-too". CBT has been winning by quantity and now increasingly by quality. This raises a dilemma: US demand sanctions could ease competitive pressure for ~49 USBTs (~14% of sector m/cap) but it might also restrict patient access to innovative therapies. Innovent, BeOne, Duality, Junshi and Akeso are highlighted as top early-stage innovators, while 3SBio and SinoBio appear undervalued.

Edition: 221

- 03 October, 2025

Technology

PAR has repositioned itself as a pure-play technology company following the divestiture of its government business, while expanding its TAM through the acquisitions of Stuzo and TASK, which extended its cloud-based unified commerce platform into convenience stores, fuel retailers and new international markets. Although management flagged some caution on ARR growth in 2025, Sidoti expects the company to achieve its 20% growth target in 2026, supported by recent contract wins and a ~$100m pipeline (excluding two large deals, one potentially closing by year-end). The recent share price sell-off is unwarranted, as PAR is well-positioned to win larger customers with more potential for upselling and margin expansion. An improved balance sheet also allows for increased flexibility around further M&A opportunities. TP $97 (150% upside).

Edition: 221

- 03 October, 2025

TKH Group (TWEKA NA) Netherlands

Technology

At its upcoming CMD, TKH is expected to set new mid-term targets to 2029: turnover >€2bn, EBITA margin >18%, ROCE 22-25% and net debt to EBITDA / leverage ratio <2x. While broadly consistent with prior goals, the updated plan is likely to emphasise organic growth. Crucially, with its investment cycle complete and working capital set to normalise, TKH is forecast to generate €600-650m in FCF in the next couple of years. This underpins scope for materially larger share buybacks - potentially €300m, or ~20% of current m/cap - alongside dividends and bolt-on M&A. the IDEA!’s DCF points to fair value of €51.30/share, implying ~50% upside.

Edition: 220

- 19 September, 2025

Industrials

FLY was highlighted at Revelare’s Space Industry Investor Idea event - while still relatively unknown post-IPO, its current multiple prices in significant execution risk. Of its $1bn 2027 revenue target, ~$770m is backlogged and as launch cadence accelerates, EBITDA margins are expected to expand sharply to 30-40%. A diversified backlog, milestone-based contracts and a major Northrop Grumman deal further strengthen credibility. The presenter believes a $10bn valuation is reasonable as a starting point (vs. the current $6bn m/cap) and expects a positive earnings report in Nov as well as another launch coming this fall. Once long-onlys see 2-3 quarters of execution, investors will enter the stock in a much more material way.

Edition: 220

- 19 September, 2025

Mahindra & Mahindra (MM IN) India

Consumer Discretionary

M&M’s decision to pre-announce GST benefits - branding itself as a “consumer-first” OEM - may be less about patriotism and more about inventory management. Dealer checks reveal heavy discounting, even on new models like the Thar Roxx, despite expectations for strong festive demand. Wholesale dispatches have trended down since May, with August volumes (~40k) significantly lower than even last year’s levels. Discounts are valid only until Sep 21st, ahead of GST 2.0 implementation, suggesting M&M is flushing dealer stock to enable a push into Oct’s festive peak. While this strategy could boost near-term volumes, it raises margin risk and potential disruption to the EV transition.

Edition: 220

- 19 September, 2025

Industrials

FAN stands out as a high quality (29% FY24 FCF RoE) mid-cap building products and business services company that has bucked the trend of sluggishness across its core markets. The business has had a very successful buy-and-build strategy, using excess FCF and modest leverage to undertake earnings accretive M&A. The recent acquisition of Fantech exemplifies this and Fighting Financials thinks consensus estimates underestimate the full benefits of this deal. Beyond fundamentals, FAN also fits the profile of UK SMID-caps attracting takeover interest with 1) geographically diversified revenues; 2) high returns on capital; 3) modest leverage; and 4) suffering a discount due to trading on the troubled UK market.

Edition: 220

- 19 September, 2025

Healthcare

Paragon interviewed 7 former senior executives at ATS who worked with BAX's new CEO, Andrew Hider, for more than 36 years combined. Feedback was universally positive. Hider is a disciplined, process-driven leader who blends Danaher-style operational rigour with strong communication and an ability to scale businesses via organic growth and M&A. At ATS, he drove cultural transformation via the ATS Business Model, delivering margin expansion and shareholder returns, though his intense stretch targets and competitive nature created a high-pressure environment that could limit collaboration and agility. His success at BAX will hinge on whether he can balance his relentless operational focus with greater strategic flexibility and adaptability to the slower-moving, more regulated dynamics of the pharmaceutical industry.

Edition: 218

- 22 August, 2025

Financials

The Genius Act has changed America’s relationship with crypto, making it the most attractive country in the world for stablecoins. Abacus’ latest report notes that while the pace of adoption is still unclear, long-term disruption of financial incumbents appears inevitable. CRCL’s model is attractive if USDC can scale, though Abacus estimates ~10x growth is needed to deliver a reasonable IRR - a challenging hurdle. Blockchains are expected to replace legacy infrastructure, with SWIFT the first casualty. Visa and Mastercard face limited near-term risk, but crypto is the primary long-term threat to their duopoly. Stablecoins have the potential to reach >$2trn m/cap in the next few years vs. $260bn today. Abacus sees CRCL as a compelling risk/reward play, with upside potential of 195% outweighing downside risk of 50%.

Edition: 218

- 22 August, 2025

Industrials

H1 revenue rose 35% (+17% organic) as ELIX notched 5 record revenue months in the 6-month period, with margins stable versus recent years. While management expects FY25 results to meet market expectations, analysts have nudged estimates higher. Willis Welby sees ELIX as an interesting cross between a quoted company and a partnership - combining a proven consulting growth model with disciplined, selective M&A. Momentum remains strong, yet despite a recent share price rebound, the implied to Y3 EBITM ratio is still only 34. Given this disconnect, they see potential for up to 70% upside from current levels.

Edition: 217

- 08 August, 2025

Telcos: More selective stock picking required

Communications

European telecom stocks have outperformed YTD, adding to 2024’s gains and validating New Street’s long-term thesis of regulatory improvement. However, with sector upside narrowing to 17% (vs. 31% at the start of the year), returns are likely to become more stock-specific and increasingly dependent on M&A. They highlight French names and Telecom Italia as most geared to deal-making. New Street’s top picks are BT (strong FCF growth); DT (German and US upside); Bouygues (undervalued FCF growth and M&A upside); and Vodafone (special sit. with value to be unlocked). They also recently upgraded Telia to Buy seeing good cost control and the possibility for extraordinary cash returns.

Edition: 216

- 25 July, 2025

Technology

At Revelare’s TMT Investor Idea Event, a long thesis on Unity argued the company is entering a turnaround phase after missteps in M&A, leadership and pricing strategy. With both Create and Grow segments rebounding, 2025 is expected to be a reacceleration year. The launch of Vector, Unity’s new AI ad platform, could restore momentum in Grow, while Unity 6 is showing early traction in Create. EBITDA in 2026 could be $600m+ vs. the Street at $440m. Revelare also hosted a separate discussion with a former Unity executive to further explore the company’s strategic reset and execution path. Since these events Unity’s shares have risen ~40% with further upside anticipated.

Edition: 216

- 25 July, 2025

Communications

Joe Cornell offers a detailed analysis of WBD’s planned spin-off of its Streaming & Studios segments. The move mirrors a broader media trend to separate faster-growing streaming assets from legacy cable operations. The split enhances strategic flexibility - Streaming & Studios could become a more attractive M&A target, while Linear Networks might be paired with a similar business. Joe’s SOTP valuation yields a consolidated target price of $15.00 per share (adjusting for a ~20.0% stake in the Streaming & Studios businesses) for WBD, which implies a potential upside of ~30% from the current market price.

Edition: 215

- 11 July, 2025

The secular bull market for Banks gets a midyear tailwind

Financials

US bank stocks can continue to hit new highs and assume a leadership role in the market, according to Charles Peabody. Fundamentals are excellent, balance sheets are strong and capital is abundant. Meanwhile, the next 12-18 months will likely include a reduction in capital requirements as part of the deregulation process. Reducing the CET1 ratio by 1% can add double digit earnings growth to banks either through buybacks or growing earning assets. Deregulation can also reduce expenses by 1-3% annually. While this process is in place, investors have become accustomed to one way headaches from regulators, and thus, deregulation is only reflected in stock prices after it happens. Charles' top picks are Citigroup, M&T Bank and Citizens Financial.

Edition: 215

- 11 July, 2025

Short ideas deliver 100% hit rate in the first half of 2025

AIR delivered an exceptional 1H25, closing 20 out of 20 European Sell/Short ideas in profit, with an average return of +24.5% per idea. Standout trades included Stellantis (+56%), STMicroelectronics (+55%), Aston Martin (+54%), Remy Cointreau (+53%) and Swatch (+43%). Out of 28 Sell/Short ideas still in force (opened in the last 18 months), 20 are currently making gains. Notable winners include LEM Holding (+51%), B&M (+49%), Alten (+42%) and Mercedes-Benz (+32%). AIR continues to issue an average of 3 high-conviction short ideas per month, making them a must-follow provider for investors seeking consistent alpha from the short side.

Edition: 215

- 11 July, 2025

Technology

IOT trades at 100x forward EPS despite being a mature company with limited history of profitability. The firm continues to rely on low-quality sources of EPS growth to drive earnings beats. In Q1, cash R&D and S&M cuts alone added 6.1 cents to EPS, while stock compensation still exceeds 100% of adjusted EPS and cash flow. Deferred Revenue and Remaining Performance Obligations are growing more slowly than sales and both DSOs are dropping (drawing down DSOs by only 1 day is worth $4m in sales and 0.5 cents in adjusted EPS). With fundamentals increasingly out of sync with valuation, BTN believes even modest signs of slowing growth could trigger significant multiple compression.

Edition: 214

- 27 June, 2025

Special Sits Idea Forum

While all the stocks presented at MYST's latest buyside event could be considered undervalued, many offered significant (i.e. >50%) upside. The most differentiated ideas included: Blackbaud (improving fundamentals more apparent post-EVERFI divestiture; potential M&A target); HealthEquity (new legislation fuelling dramatic TAM expansion + bond portfolio repricing tailwinds); and JBS (multiple to expand as US listing drives increased passive ownership / index inclusion). More familiar names discussed included: Fluor (huge NuScale Power (SMR) monetisation catalyst not reflected in Street estimates); Teva Pharmaceutical (generics cash cow enabling innovative branded portfolio pipeline development); and Warner Bros. Discovery (well positioned for media consolidation wave amid forthcoming business separation).

Edition: 214

- 27 June, 2025

Elis (ELIS FP) France

Industrials

Boring and beautiful - Pierre-Olivier Essig calls ELIS the best mid-cap to buy in Europe right now. Its mission? Helping hotels, hospitals and other hospitality clients eliminate laundry headaches via its vast footprint, microchip-enabled linen tracking and upgrading the quality of cleaning. With much of the sector still yet to outsource laundry services, the opportunity remains compelling. Growth is predictable: ~2% from volume, 2% from price and 2% from M&A annually. EBIT margins just hit a record 35.2% and management's 38% medium-term target is in sight. With +110% upside to his TP of €50 and trading at just 12x 2025 earnings (vs. 50x for Cintas), ELIS looks insanely cheap.

Edition: 214

- 27 June, 2025

Technology

2Xideas sees KEYS as a high-quality compounder with strong competitive advantages and secular growth tailwinds. As the global leader in RF test and measurement solutions, the company benefits from resilient R&D-driven demand (~60% of revenue), ensuring high margins and customer lock‑in. It has built a powerful flywheel around its PathWave software ecosystem. Structural growth trends (5G Advanced, 6G R&D, data centre networking led by AI/ML, automotive electrification semiconductors) drive increasing complexity and testing intensity across value chains, supporting 5-7% organic revenue growth. Operating margins to expand by 480bps to 30.5%, with EPS expected to grow at an 11.4% CAGR through FY31E. 2Xideas sees a potential 2x return with upside from M&A and buybacks.

Edition: 213

- 13 June, 2025

Technology

Trivariate flags PLTR as one of the most compelling short ideas ahead of the June 2025 index rebalance. Having surged nearly 5x since mid-2024, PLTR now trades at a $291bn m/cap and an eye-watering 73x EV-to-forward sales - making it the second most expensive US non-biotech stock with over $50m in revenue. Historically, stocks trading above 30x EV/sales fall to 18x within a year and underperform the market by an average of 22.5%. With PLTR comprising over 8% of the mid-cap growth index, a shift into the large-cap universe will likely trigger major selling pressure. Unless you believe PLTR can grow faster and longer than any company has ever grown, selling now and shorting near June 30th is the logical strategy.

Edition: 212

- 30 May, 2025

Linamar (LNR CN) Canada

Consumer Discretionary

Despite doubling EBITDA over the past 5 years, LNR's valuation multiple has halved. The problem is that the market sees the high returns in the Industrial segment as funding the lower returns in the Mobility segment. Between 2019-2024, LNR allocated ~$950m to Industrial (mainly M&A) at an attractive ~22% incremental ROIC, while reinvesting ~$900m in Mobility (mostly organic), at a mere ~2% incremental ROIC. Veritas maintains a Buy rating on the stock, citing the company’s strong FCF, low valuation (near tangible book value) and insulation from tariff risk. To lift the conglomerate discount, Veritas suggests improved capital discipline, clearer segment disclosure and scaling buybacks.

Edition: 212

- 30 May, 2025

Communications

NXST is one of only two TV broadcasters that is rated Overweight by Craig Huber. The company is generating a tremendous amount of FCF (he estimates $1.65bn after dividends over 2025 & 2026, which is more than 30% of its current m/cap). With a stronger balance sheet than peers, NXST is better insulated from a downturn in the ad market and is well-positioned for acquisitions if regulatory constraints are relaxed in the next year, as Craig expects. He sees huge pent-up demand for another wave of consolidation as well as demand for doing TV station swaps to create duopolies in markets among two top-4 rated TV stations given the cost synergies are massive.

Edition: 211

- 16 May, 2025

Bouygues (EN FP) France

Industrials

New Street initiates coverage with a Buy rating, citing increased prospects for French Telecom M&A as a key catalyst. They consider a Bouygues-SFR deal to be the most likely as the GUPPI is probably too high for an Iliad-SFR merger and Iliad-Bouygues is unlikely as there is no natural seller. New Street suggests an SFR-BTel deal could unlock €8–9bn+ in synergies. Regulatory remedies would likely be manageable amid current political sentiment. Drahi may now face pressure to provide lenders with an exit from SFR. New Street assigns a 56% probability of a merger in their SOTP model and sees 43% upside; they would be a Buyer ex M&A, but M&A could be a game-changer, especially as the dividend can increase by over 50% as well.

Edition: 211

- 16 May, 2025

Financials

Galliano's Financials Research

Victor Galliano upgrades Kyoto Financial to Buy, following what appears to be a sea change in management’s view on equity holdings disposals as well as the president’s opinion regarding Japanese regional bank consolidation. Nobuhiro Doi suggested that the target of JPY100bn disposals by Mar 29 could be increased to JPY200-300bn (up to 30% of total equity holdings; equivalent to 42% of Kyoto’s current m/cap). Such disposals would act as significant catalysts for large share buybacks going forward. In the longer term, Kyoto could be in a strong position to lead a regional bank merger or acquisition, with a look to improving efficiencies. An important factor in determining Kyoto’s “bargaining power” in the consolidation process will be to what extent its shares trade at a premium valuation; it currently trades at a premium in terms of PE multiple, but at a discount in terms of PBV ratio.

Edition: 210

- 02 May, 2025

BAWAG Group (BG AV) Austria

Financials

Fighting Financials reinitiates coverage of BG with a Buy rating, after first recommending the bank at €66 in Jul 24 and removing it from their active buy list at €98 in Mar 25. They highlight a supportive macro backdrop for NIM-sensitive banks, with sticky inflation and low unemployment in Europe. While BG stands out for the fundamental quality of its business and undemanding consensus expectations. Key risks include potential Austrian bank taxes and legal challenges over retail processing fees. Nevertheless, BG is one of the best positioned names to navigate said challenges given its high level of profitability and substantial excess capital (>6% of the group’s m/cap is available for M&A or special dividends / buybacks).

Edition: 210

- 02 May, 2025

90% hit rate on Shorts, while Buy calls also continue to outperform

Since the beginning of 2024, AIR has published 41 Short ideas, 37 of which have generated absolute gains. Standout performers include B&M, LEM Holding, Remy Cointreau, STMicroelectronics, Stellantis and Valeo. In Q1 2025, AIR initiated 6 new Short positions, with LVMH leading the pack, and closed 6 positions, including a 54% gain on Aston Martin. On the long side, AIR’s Top 10 Large Cap Best Ideas returned +7.7% in Q1 this year, outperforming the Stoxx 600’s +5.2% gain. Since inception in 2012, the selection has outperformed the index by nearly 300%. Meanwhile, AIR’s Top 10 Mid Cap Best Ideas Selection delivered +17.3% in Q1, far exceeding the +4.3% return from the Stoxx Europe Mid 200 Index.

Edition: 209

- 18 April, 2025

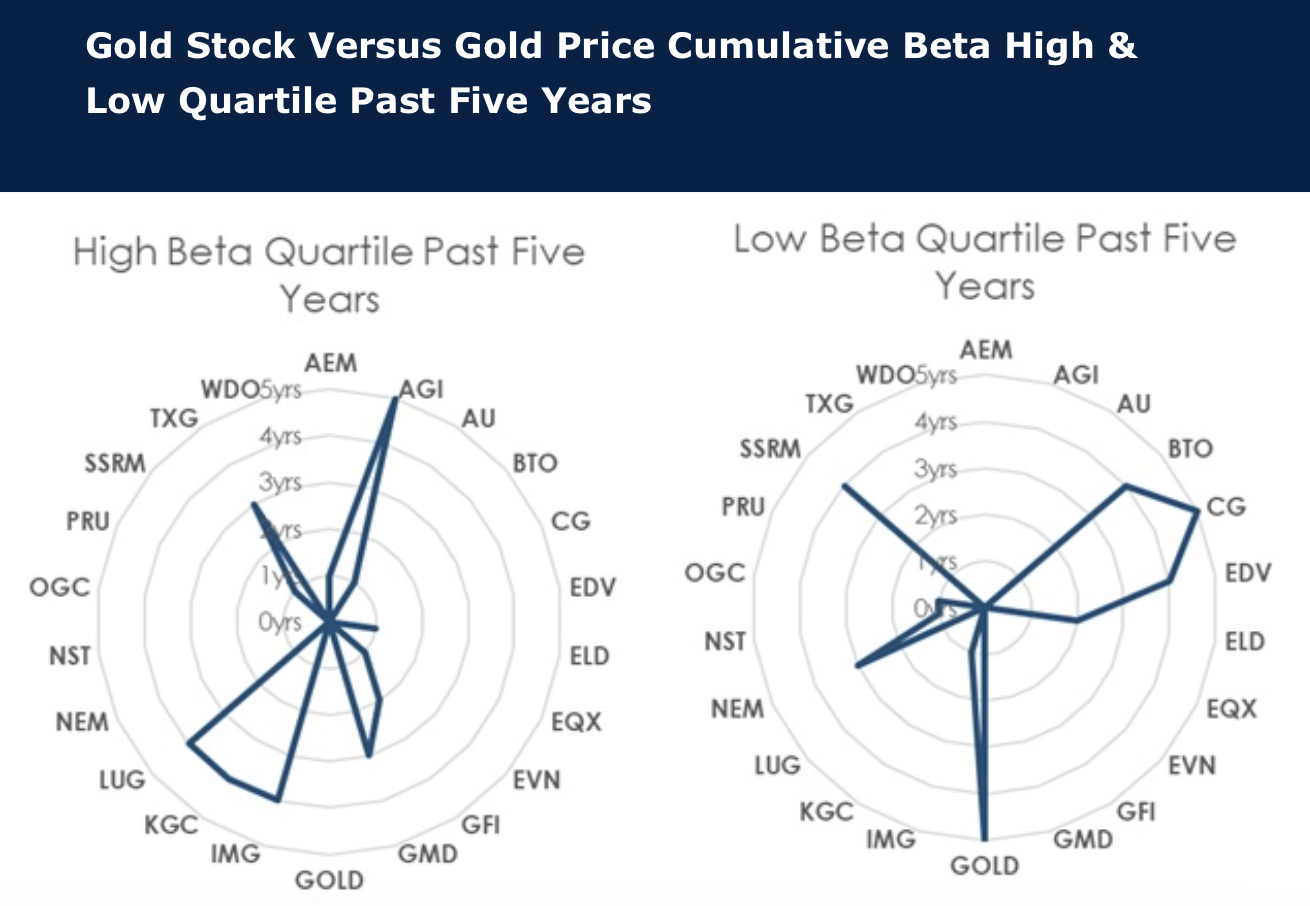

High beta gold stocks outperforming peers

The Global Mining Research team research the correlation of stocks to the gold price and the beta of those stocks. The stocks with consistently high beta to the gold price over the past five years are Alamos Gold, Genesis Minerals, IAMGOLD, Kinross Gold, Lundin Gold and Torex Gold Resources. Stocks with a weak beta to gold price over the past five years are B2Gold, Centerra Gold, Endeavour Mining, Barrick Gold, Newmont and SSR Mining (except 2025), each with mine or management issues, heightened risk or M&A troubles. Market preference for gold stocks appears to be more driven by investor perception rather than quantifiable valuation or sensitivity measures, and investors are preferring stocks with “issues” and aren’t seeking deeply discounted cheap stocks. Preferred gold stocks are BUY-rated Agnico (delivery and lower-risk portfolio), Kinross (risk reduction and execution), Equinox (transitions from project development to cash generation), IAMGOLD (Côté ramp up and derisking) and Lundin Gold (FDN continues to outperform).

Edition: 209

- 18 April, 2025

Dassault Systemes (DSY FP) France

Technology

Siemens is acquiring Dotmatics, a US-based SaaS provider for laboratory management, for $5.1bn. The acquisition appears expensive (16.5x EV/sales and 39x EV/EBITDA for FY25) but strengthens the group’s position in the life sciences sector by expanding its digital twin technology and industrial software offerings. Dotmatics adds a new $5.5bn market opportunity, which could grow to $11bn, covering areas like pharma manufacturing, biofuels and chemicals. SIE’s growing presence in this sector will intensify competition where DSY currently leads the market. While GR20 does not expect DSY to respond by going on a buying spree, there could be interesting opportunities for M&A to enhance the 3DExperience platform (on the Biovia side) or Medidata, particularly to align with its recently launched 3D Universes AI-driven environment.

Edition: 209

- 18 April, 2025

Brazil: Higher for longer

The country remains polarised at the political level, centred around the bitter fight between Lula and Bolsonaro. On the economic front, activity expanded in January after a strong performance in 2024, although Marcos Buscaglia expects a sharp deceleration this year. Downside in Q1 will be limited by agriculture and tourism. The labour market is showing strains already, and Marcos reiterates his view that credit will decelerate fast in the coming months, impacting employment and the wider economy. Inflation came in at 1.31% m/o/m in Feb, but decelerated to 0.64% m/o/m in March. Price pressures more linked to the cycle bring conflicting signals. Marcos expects the BCB to deliver a 50bp hike in its May meeting, then to remain on hold for the remainder of the year.

Edition: 208

- 04 April, 2025

Technology

Cyber diamond in the rough - unloved and out-of-favour, VRNS has underperformed its peers by a wide margin over the last 12 months. However, Felix Wang thinks its fortunes may start to change this year. His bullish thesis revolves around overplayed concerns re. the company’s ongoing SaaS transition and with continued product leadership, alongside a better sales team, VRNS's 2025 ARR and earnings guidance are beatable. Investors are highly sceptical of the company’s ability to reach $1bn ARR by 2027. This is why it is trading at only 6.6x 2026 EV/ARR. With a multiple re-rating and M&A optionality (Google's historic acquisition of Wiz for $32bn could open the floodgates to more M&A in cybersecurity), Felix sees 30%+ upside.

Edition: 208

- 04 April, 2025

Industrials

This business has a lot to like - high margins, good growth and plenty of opportunity for more accretive M&A. The Healthcare deal has also left a strong financial base from which to move forward. FY numbers last month were no surprise. Revenues were up 4% and adjusted margins were flat. Analysts had put through some upgrades with the trading statement in early Jan and though the share price has collapsed they put through another round in March. The implied to Y3 EBITM ratio is now back to 43. Willis Welby can see the share price doubling.

Edition: 208

- 04 April, 2025

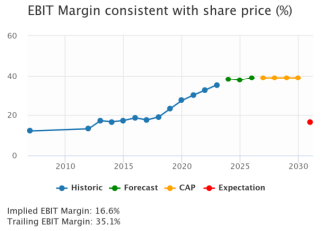

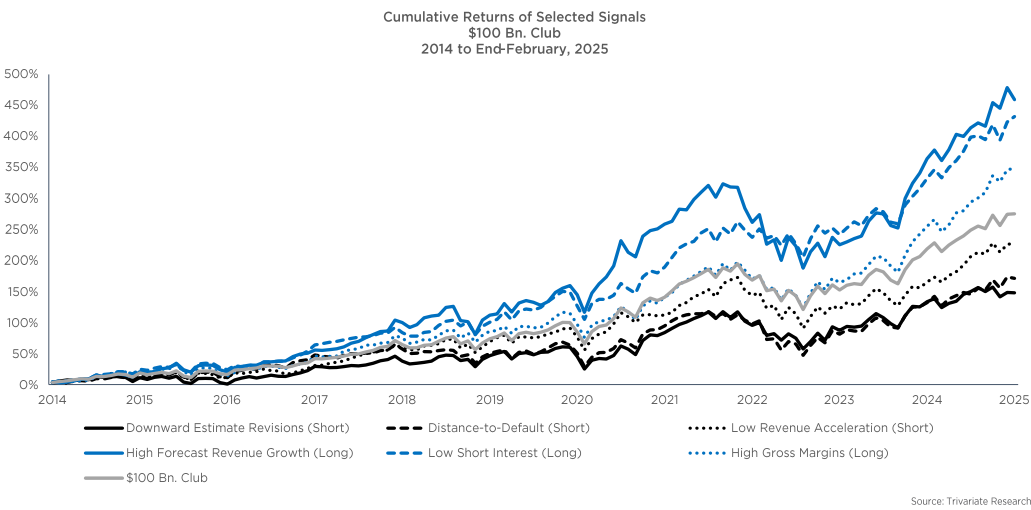

Which stocks >$100bn m/cap are buys now?

With investors searching for value in the current market sell-off and likely looking to buy names among the safer, larger cap universe, Trivariate has assessed the performance of several metrics within the stocks >$100bn m/cap to see if they could systematically pick winners from losers. The best performing signal over the last 10 years, was buying the companies in the top third of forecasted revenue growth, while the second best was buying the one-third of companies with the lowest short interest. The worst performing signals were those in the highest third of leverage and stock volatility (distance-to-default) and those with the worst third of downward earnings revisions. Current long ideas from Trivariate’s $100bn Club Framework include all the Mag 7 (except Tesla), as well as Eli Lilly, Visa and UnitedHealth. Shorts include Goldman Sachs, PepsiCo, Caterpillar and Starbucks.

Edition: 207

- 21 March, 2025

H&M (HMB SS) Sweden

Consumer Discretionary

Q1 channel checks reveal weaker-than-expected SSS growth in Europe (+0.35% Y/Y vs. consensus of +2.65%). While 50% of surveyed store managers reported positive Y/Y revenue growth, driven by new seasonal collections and effective in-store promotions, 30% of stores experienced declines due to competitive pressures and adverse weather conditions, particularly in markets like the UK and Czech Republic. 40% of managers noted declining foot traffic as a headwind, particularly in Eastern and Northern Europe. Seasonal inventory challenges were also cited by 20% of respondents, affecting sales performance in some regions, especially in Switzerland and the UK.

Edition: 207

- 21 March, 2025

Hutchison's mega deal with BlackRock and TIL

Industrials

Drewry Maritime Financial Research

Eleanor Hadland and Eirik Hooper provide a comprehensive assessment of the recently announced ports sale. The deal highlights the growing dominance of hybrid operators (terminal operators owned by carriers) in the market. While the BlackRock / TIL consortium appears to have paid a premium, the strategic advantages likely justify the cost, especially as M&A remains a key route to overcome the high barriers-to-entry in the terminal sector. Competition concerns may also lead to secondary transactions, particularly in Northwest Europe, where regulators could assess that the deal leads to excess market concentration. Click here to watch.

Edition: 207

- 21 March, 2025

Financials

MTB has some of the best banking DNA that Charles Peabody is aware of. This includes a unique community bank strategy; impressive leadership; strong balance sheet with excess capital (unimpaired by unrealised bond losses); excess liquidity (available to be reinvested into higher yield asset opportunities); improving credit outlook; and good earnings momentum (forecasts DD EPS growth in each of the next 2 years). Charles expects MTB to generate a mid-teen RoTCE. The bank has grown TBV at an 8% CAGR over a multi-decade period and he forecasts TBV growth to accelerate toward $116 per share by year-end ’25 and $130 per share by year-end ’26. The dividend is safe even in a recessionary environment.

Edition: 207

- 21 March, 2025

UniCredit (UCG IM) Italy

Financials

Management has been heavily focused on improving the bank’s operations, while also being highly shareholder-friendly, with a commitment to distribute >€9bn by way of dividends and buybacks in FY25e. UCG also has material optionality in terms of M&A and in the context of a Europe that is insecure about diminishing US defensive support and stagnant economic growth, Fighting Financials thinks European regulators will be more open to supporting pan-European corporate “champions” across sectors, including financial services. Ultimately, they see the bank as one of the higher quality, more defensive names, able to benefit from certain structural and geopolitical dynamics coming into play across the continent.

Edition: 206

- 07 March, 2025

LVMH (MC FP) France

Consumer Discretionary

In the past 20 years, Pierre-Olivier Essig has never seen as many red flags surrounding LVMH as he does today. In addition to terrible 4Q24 numbers, he highlights succession change, brand fatigue, low value retention, supply chain ethics, designer casting mistakes, unjustified pricing, as well as specific issues attached to almost every division. Pierre faced huge resistance from clients 12 months ago when he advised selling LVMH shares at €822, however, that proved to be the correct decision and in Oct, he then upgraded the stock to Buy after it fell through €600. With the share price having recently moved back above €700, Pierre turned bearish once again. He expects Hermes m/cap will exceed LVMH’s within the next year.

Edition: 206

- 07 March, 2025

Glanbia (GLB ID) Ireland

Consumer Staples

Vision’s bear thesis focused on growing competition in protein powder, potential lack of pricing power in the face of elevated input costs; weak positioning in diet and RTD category; weak margins, ROIC and FCF; and inventory growth. The share price declined 23% on Feb 26th the day of earnings and the short generated alpha of ~45% vs. Stoxx600. Vision initiated 8 new shorts in 3Q24, 10 in 4Q24 and 4 so far in 1Q25 of which 10 were US, 8 European and 4 Asian. Consistent with their goal of finding liquid, non-consensus shorts, these 22 ideas had avg. m/cap >$15bn, avg. AD$V >$65/day and avg. SI% of free float of <4%.

Edition: 206

- 07 March, 2025

Consumer Discretionary

John Zolidis sees the potential for ~50% of the current m/cap to be returned to shareholders over the next 5 years, while YUMC simultaneously grows its EBITDA by nearly 50%. The company’s ability to grow while this capital return programme is underway highlights both the model and value creation from new unit openings. Its valuation has contracted while domestic restaurant stocks have seen valuation expansion establishing an extreme relative multiple discount. A 10.5x EV/EBITDA multiple generates a 34% 1-year return using 2026 forecasts. Over 4 years, a 12x multiple vs. John’s 2029 estimates produces a double, not including dividends. Downside is protected based on unit growth, cash flow, buybacks and the current 8.6x multiple.

Edition: 205

- 21 February, 2025

Healthcare

Clinical Labs have been among the least attractive subgroups in Healthcare for a really long time, but fortunately for DGX, Tom Tobin thinks the US is entering a New American Medical Economy where prospects finally look attractive. With just a few weeks under their belt the incoming Trump Administration has been all shock and awe with a clear message that they are serious about reform. Tom sees DGX sustaining a reliably higher revenue and EBITDA growth rate leading to upside to both 2025 and 2026 forecasts, through a combination of excess volume, pricing, efficiency gains and M&A, resulting in a stock >$190.

Edition: 204

- 07 February, 2025

Is the diversified model dead?

Materials

GMR recently published a review of the leading mining stocks’ performance over the last five years. For the diversified miners this highlighted weak TSR and overall negative returns stripping out cash payouts. A critical issue facing the group, especially the iron ore-dominated miners, is how to restructure their portfolios for the long-term. GMR reviews six key questions: 1) Is the diversified model dead? 2) Can dividends be sustained? 3) Miners exited coal but should it have been iron ore? 4) Shrinking to greatness might have merit? 5) How to increase EV materials exposure & in which commodity? 6) Is M&A the answer? BHP is their preferred pick, with Glencore second. Vale is very cheap, but it is hard to see a catalyst.

Edition: 204

- 07 February, 2025

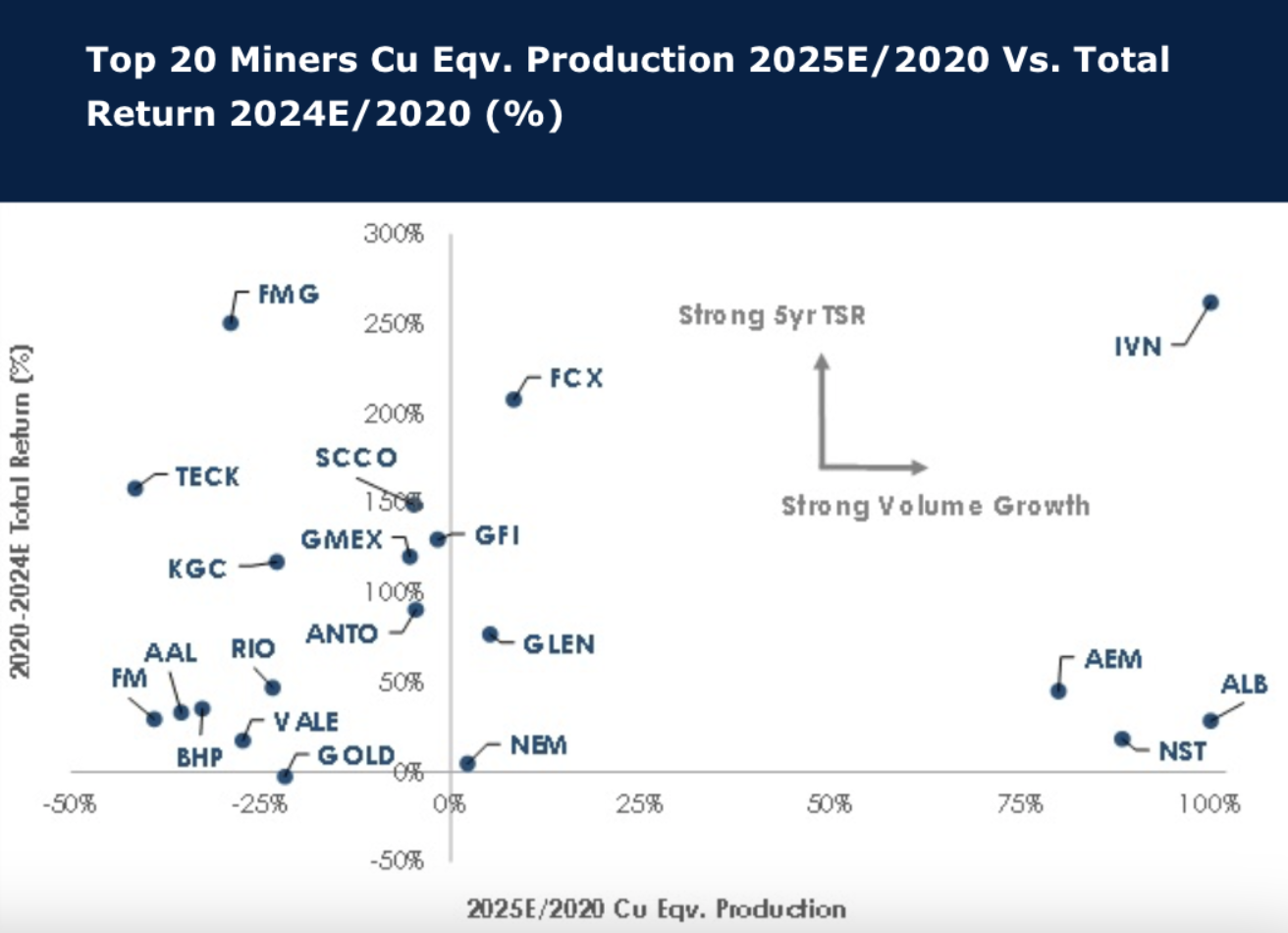

Large cap miners: Performance and growth are not related

As Sellside and Buyside set expectations for 2025, Global Mining Research examines the recent history of the leading miners. Interestingly, only Agnico Eagle Mines Limited, Albemarle Corporation, Ivanhoe Mines Ltd, and Northern Star Resources Limited are estimated to have materially grown through investment and M&A over 2020-2025E. In fact, most miners have shrunk in terms of Cu Eqv. Production, and exiting coal was a clear trend. The copper miners have outperformed, despite iron ore miners clearly returning the most cash to shareholders in dividends. Buybacks should have helped the share price return but there is little evidence this works. For over half the group, a ‘buy and hold’ strategy has not generated a robust return over the period. This reinforces the view that miners are to be traded.

Edition: 202

- 10 January, 2025

EU Telecoms: The calm before the storm

Communications

New Street expects to see an uptick in M&A activity this year after a lull in 2024. Some of the larger transactions are likely to be potential attempts at further 4-3 deals following the successful approvals in Spain and the UK. Key markets where this could happen are Germany, Italy, France, Sweden and Denmark. From an investor perspective, the best way to play this theme would be through Telefonica, 1&1, Telecom Italia, Altice France bonds or Bouygues. Away from potential 4-3 mergers, other fiber deals could still be a further theme in Europe in 2025, and again Telecom Italia comes into focus as a beneficiary of a potential NetCo-OpenFiber transaction.

Edition: 202

- 10 January, 2025

2025 year ahead outlook

Trivariate sees the US equity market as increasingly risky near-term, but eventually ending the year at new highs. Long-term, they see the S&P500 nearing 10000 by 2030, driven by 8.6% p.a. EPS growth. Revenue acceleration will matter more than gross margin growth in 2025 for stock selection. High-quality, low-beta, low forecasted growth outperforms among growth stocks. Value has lagged Growth by 1.3% p.m. for 50 years. Focus on low capital spending and high FCF among value stocks. Small caps are not cheap. Healthcare and Industrials to outperform Consumer Discretionary and Communication Services. Trivariate is tracking 6 Growth baskets: AI Semis, AI Software, Electrification Industrials, Housing / Building Product, Power / Utilities and Healthcare Services.

Edition: 202

- 10 January, 2025

A secular bull market for Bank stocks

Financials

Looking back over the past half-century, Charles Peabody has never felt so invigorated about bank stocks. They are poised to generate fundamentals as good as the market, but trade at a substantial discount to the market. Many of the reasons for this discount are likely to abate in the coming years and investors will take note. He discusses the favourable outlook for bank revenues, asset quality, capital generation and regulatory relief. His top picks include Citigroup (a self-help story with a credible CEO trading at 2/3 of TBV) and Wells Fargo (labouring under an asset cap since 2018 that is destined to be lifted), as well as M&T Bank and Citizens.

Edition: 202

- 10 January, 2025

Technology

What multiple should a ~20% EBITDA growth business trade on? Abacus argues it should be significantly higher than 12x EV/EBITDA (2025) and expects the multiple to expand when FOUR better explains its organic growth and the sustainability of its acquisition strategy. They believe the company has an opportunity large enough to grow gross profit at a 20-30% CAGR over the coming years, split evenly between organic and M&A, where FOUR can acquire at 4x EBITDA post synergies. Near term earnings misses, due to softer macro and slower customer acquisition in Europe, provides an attractive opportunity. TP $164 (75% upside).

Edition: 197

- 18 October, 2024