Fortnightly Publication Highlighting Latest Insights From IRF Providers

Company Research

Global bulls

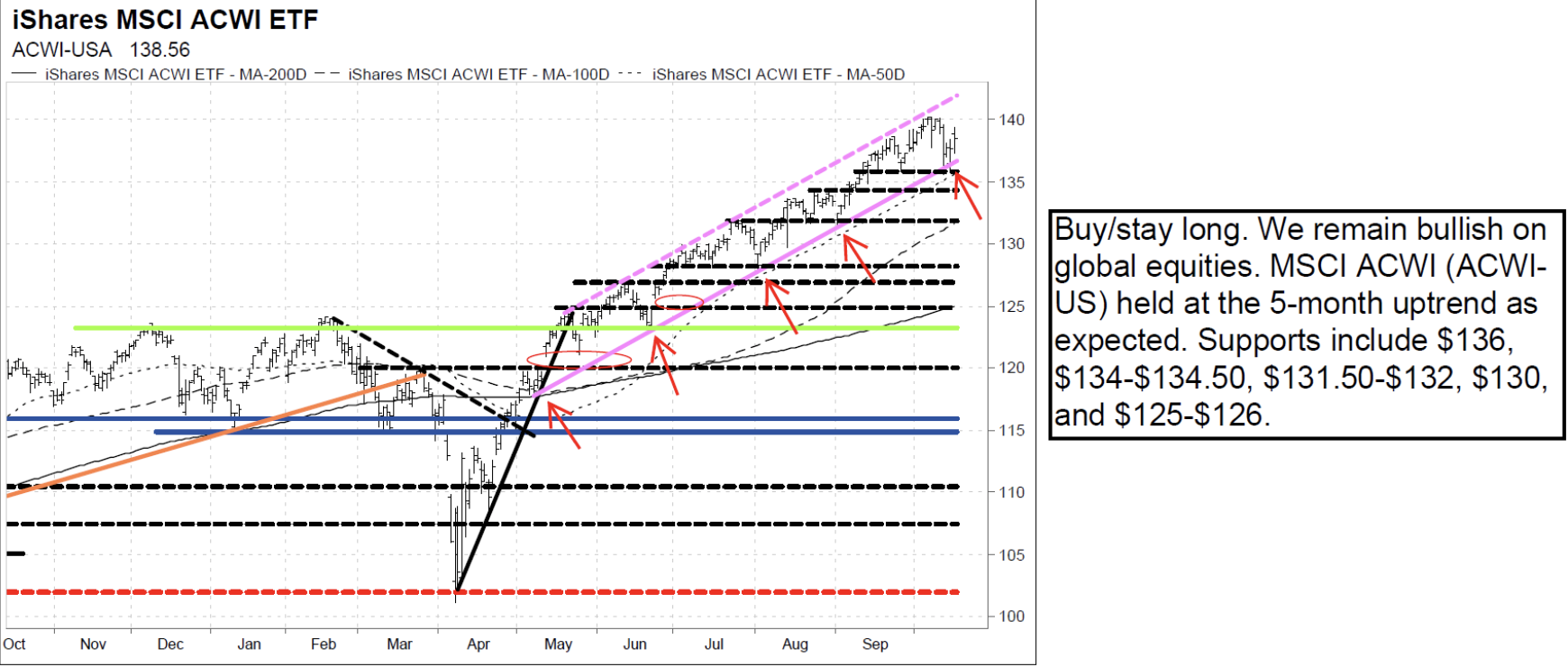

The Vermilion team remain near-term bullish since their April report, with their intermediate-term outlook also remaining bullish. They will maintain this view for as long as market dynamics remain healthy and the SPX and ACWI-US are above 6028-6059 and $125-$126. Their bullish near-term outlook will remain in place as long as the 5+ month uptrend continues on ACWI-US. So far, the latest pullback is testing the uptrend -- buy/stay long. Short-term supports to watch on ACWI-US include the 5+ month uptrend (currently at $136), $134-$134.50, $131.50-$132, $130, $128, and $125-$126. Expect more upside into year-end and early 2026. Remain overweight Taiwan, China, Korea and the US, and bullish on EM particularly MSCI EM Tech and Materials.

Edition: 222

- 17 October, 2025

Remain overweight Taiwan, China and Korea

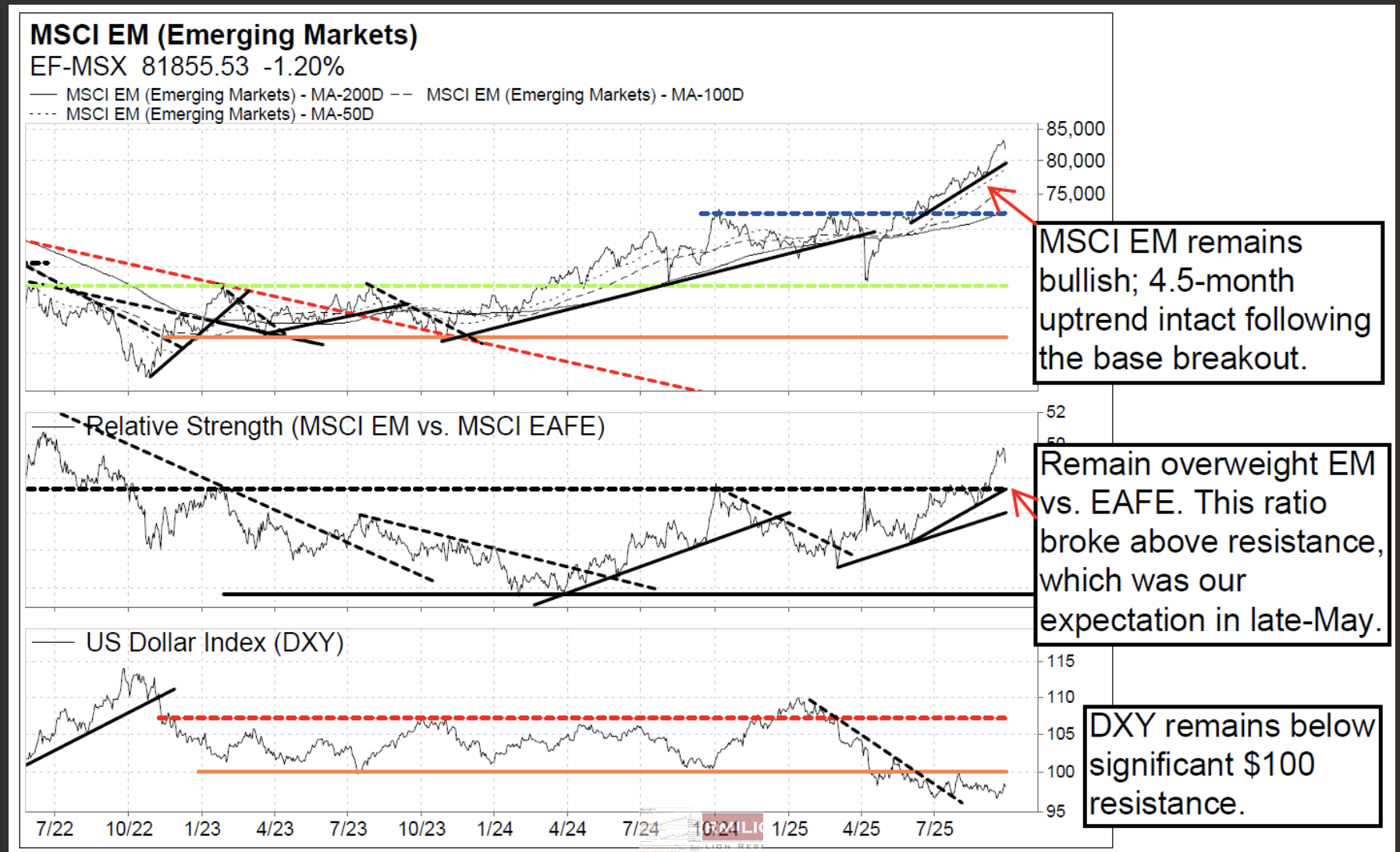

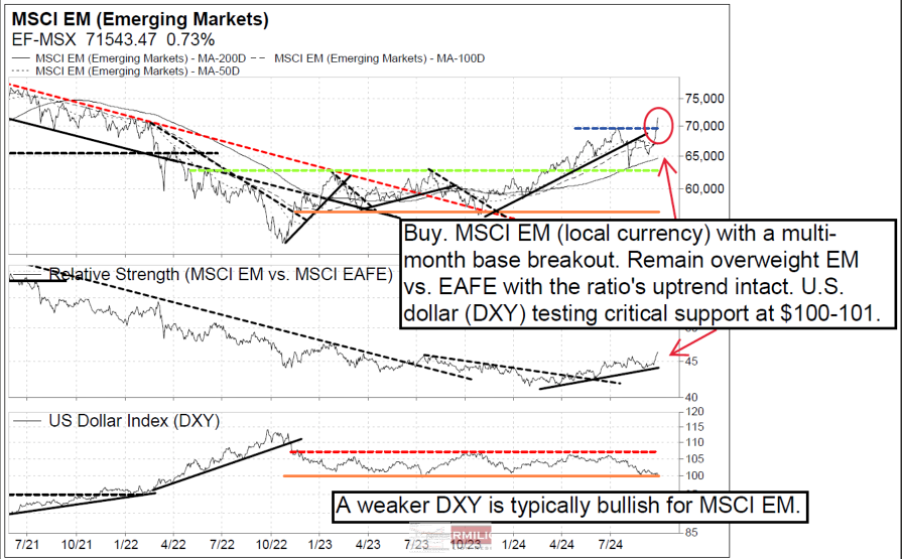

According to David Nicoski, the MSCI Emerging Markets index (local currency) and EEM-US (USD) are both trading within 4.5-month uptrends, and he remains bullish. David expects support at the uptrend, which also coincides with the 50-day MA and $50.65 horizontal support on EEM-US. He would view any pullback to $48 support on EEM-US as a buying opportunity. For EM countries, while price remains attractive, he is downgrading Greece to market weight due to RS deterioration. EM countries where he remains overweight include Taiwan, China, and South Korea. Additional leadership countries include Vietnam, Romania, and Pakistan. For EM sectors, defensive EM sectors (staples and utilities) continue to underperform and are at YTD RS lows; underperformance has continued, as expected -- avoid. Meanwhile, attractive EM sectors where David expects outperformance include: MSCI EM technology, consumer discretionary, materials, and communications. He is also monitoring for a RS bottom on EM health care.

Edition: 221

- 03 October, 2025

US: Risk will become visible

Valerie Gastaldy cannot remember such a quiet market for such a long period. Bonds, commodities, and the dollar are in narrow ranges, and they are remarkably stable in those. It is always tempting to think that the longer the wait, the faster the speed, after the breakout. This is not what she has noticed. In those markets that are heavily traded by algorithms, speed is fast when reversals occur fast, but after ranges, false signals occur and speed starts slowly, to increase with time. The MSCI World, and foremost US equities, are still indifferent to the questions that other assets underline. Valerie thinks risk will become visible if and when the dollar resumes its fall together with US equities. For many weeks now, US equities have been rising as the dollar was falling, or flat. A change in this correlation may underline a change in risk attitudes.

Edition: 219

- 05 September, 2025

Emerging market equities are picking up steam

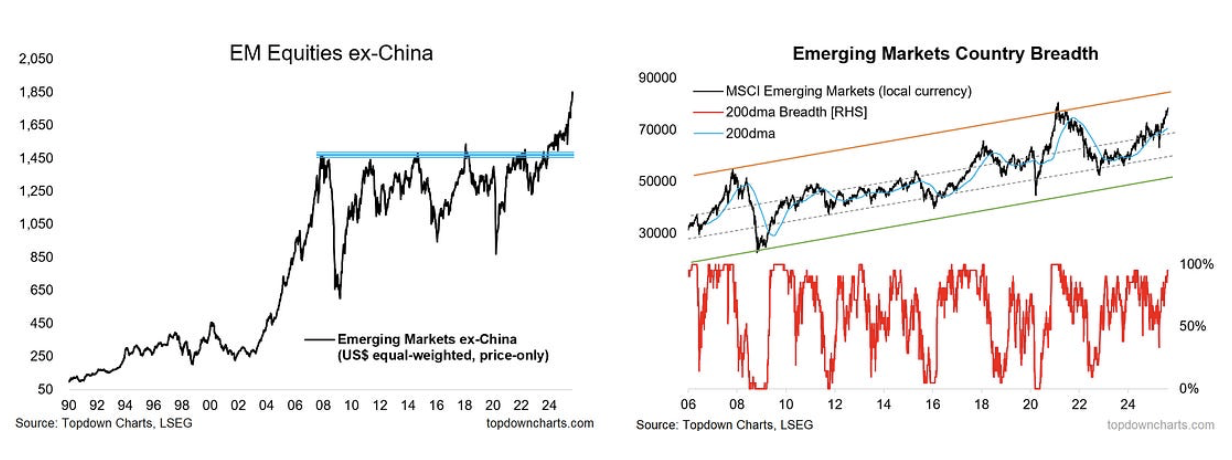

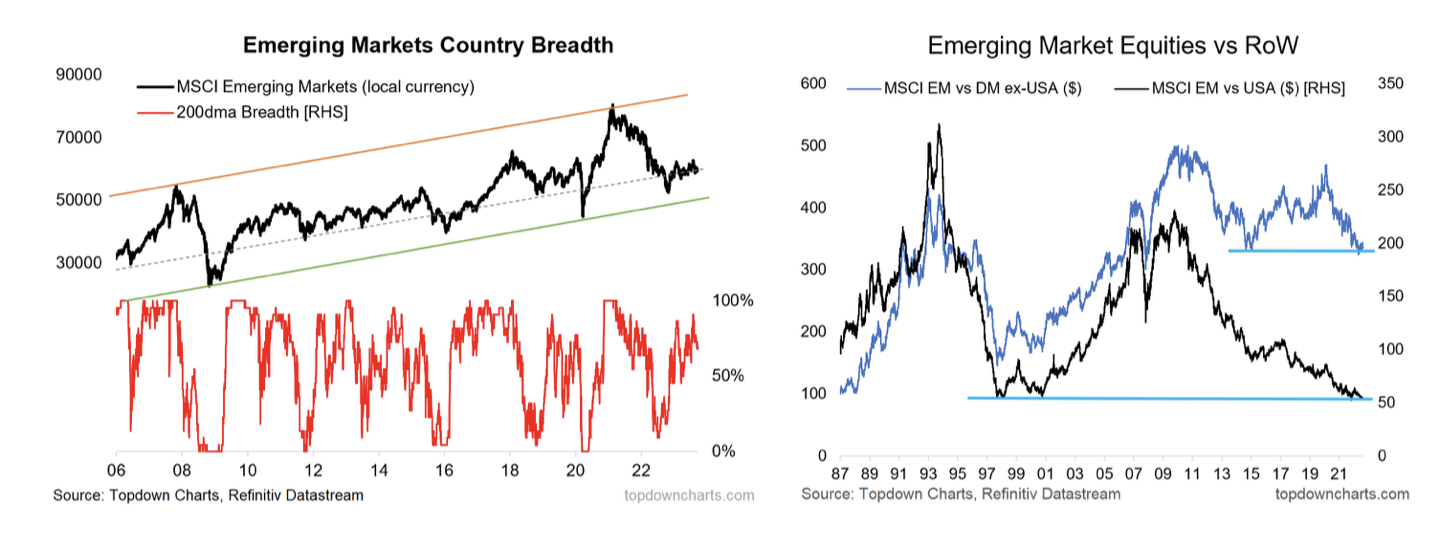

Callum Thomas maintains a bullish view of emerging market equities, noting that equities are accelerating post-breakout. He sees this in both the local currency and US$ indexes. Moreover, market breadth is expanding, indicating broadening strength. Chinese stocks in particular are also finally seeing significant improvement. The picture is very bullish. His charts illustrate how EM equities are picking up steam; the US$ equal-weighted EM ex-China index is accelerating following its breakout and initial consolidation, while the MSCI EM local currency index is also accelerating following the earlier failed break below its 200-day moving average and is doing so with expanding market breadth. He also notes very bullish price action in China, with A-shares breaking out vs the key overhead support level after a year-long period of consolidation. This is a clear sign of bullish strength and looks more like the booming early-2000's than the stagnant 2010's.

Edition: 218

- 22 August, 2025

MSCI emerging markets pullback in process

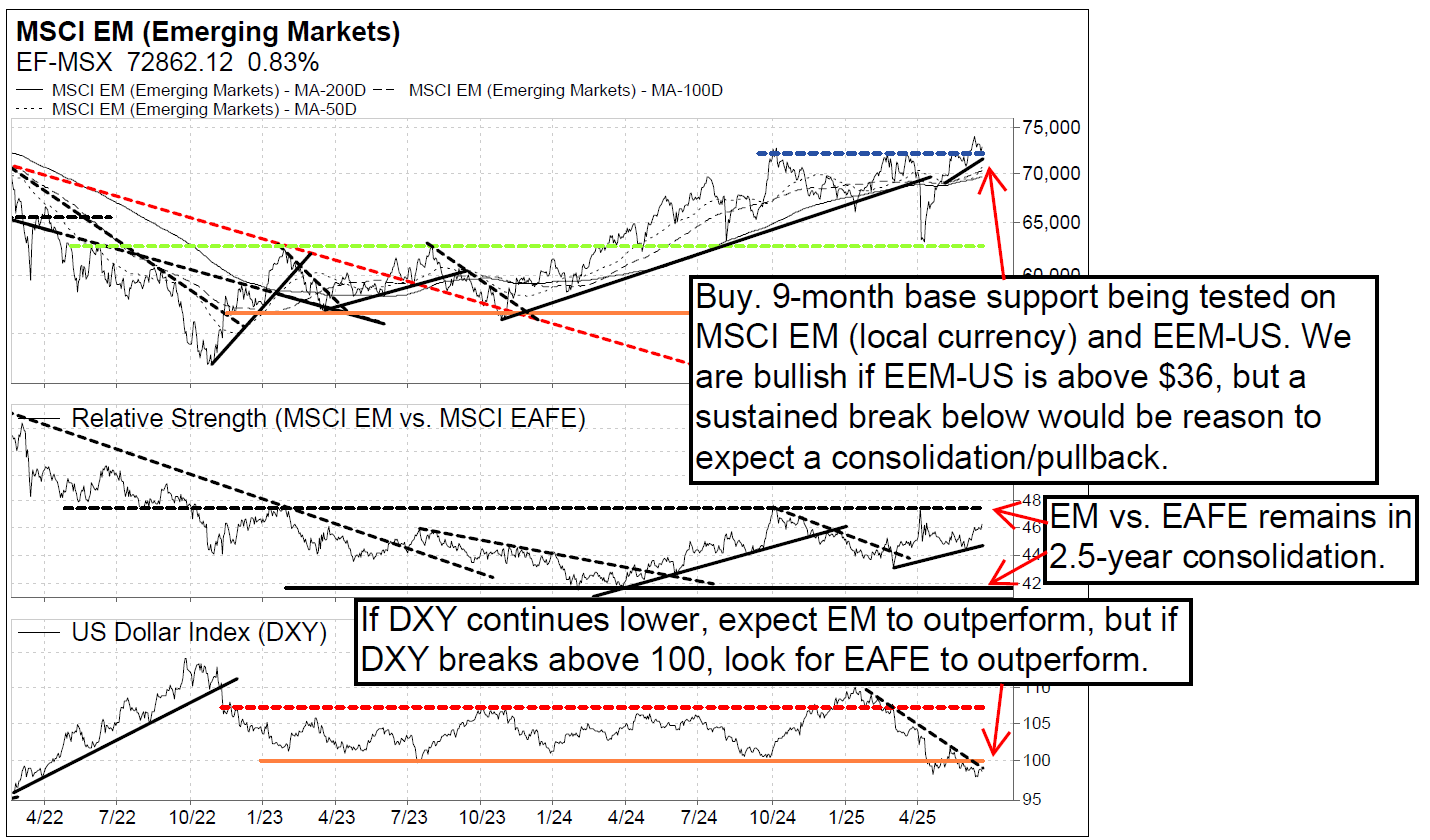

The EEM-US broke below its 20-day MA for the first time in over three months. Any potential pullback to major base support ($46) should be considered a buying opportunity. As discussed in Vermilion’s weekly Int’l Compass reports, EM countries that they are overweight include South Korea and Greece. Additionally, there continues to be several other countries that are bullish and/or worthy of overweights, including South Africa, Taiwan, Hungary, Czech Republic, Poland, Vietnam, UAE and Pakistan. Turning to China, the Shanghai Composite displays a significant base breakout, and China has been a favourite country to add exposure to over the past month (July 3 Int’l Compass titled “China and Japan Breaking Out” and also July 22 Int’l Macro Vision). As long as base support holds on this pullback, David Nicoski remains bullish and he is monitoring China for a potential upgrade to overweight.

Edition: 217

- 08 August, 2025

MSCI Emerging Markets: Testing base support

The MSCI Emerging Markets index (local currency) and EEM-US (USD) are holding above their respective base supports, including $46 on EEM-US. The Vermilion team are buyers as long as EEM-US is above $46, but a breakdown below it would indicate a bearish false breakout; if that were to happen, investors should become cautious and expect a pullback/consolidation. Their top EM picks are South Korea and Greece, and are bullish South Africa, Taiwan and Hungary. Defensive EM sectors (staples and utilities) continue to underperform and should be avoided, but the team expect outperformance from MSCI EM tech, energy, industrials, financials and comms.

Edition: 214

- 27 June, 2025

Korea shines amidst EM breakout

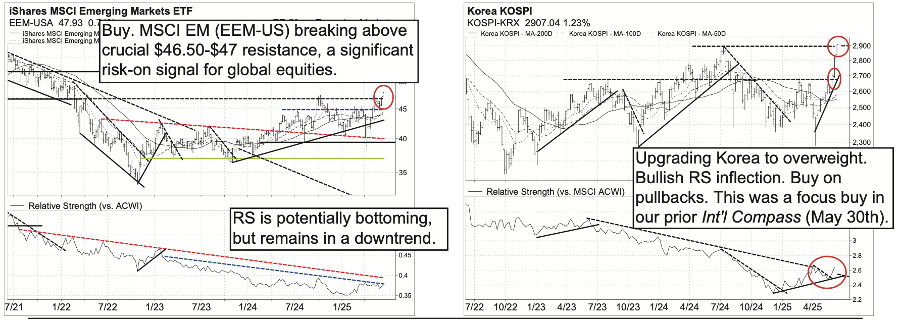

MSCI Emerging Markets (EEM-US) is breaking above $46.50-$47 resistance, continuing the bullish short-term trend. The Vermilion Team are buyers on this breakout, with Korea being their top country to buy. The team are upgrading Korea (KOSPI) to overweight; in their latest report, they discussed how the KOSPI was breaking out of a 10-month base (May 30, 2025), highlighting several large-cap financials and other stocks to buy. The KOSPI has exploded higher since and is now reversing its 2-year RS downtrend. Buy any pullbacks.

Edition: 213

- 13 June, 2025

Xi's Champions: A closer look at fund positioning

Following President Xi’s recent meeting with select private sector leaders, Steven Holden breaks down the percentage of funds invested in each stock, segmented by fund type, from broad-based Global and GEM funds to specialist China strategies (MSCI and A-Shares). As expected, ownership increases as we move from global strategies to China-focused funds. Beyond Tencent, Alibaba, BYD, CATL, Meituan and Xiaomi, representation in non-China funds is limited. Some names, such as Shiyuan and Qi An, are almost entirely absent from all fund groups. Will Semiconductor and Muyuan Foods stand out as the biggest discrepancies - despite decent representation in specialist China funds, they barely register in Global, GEM, or Asia Ex-Japan allocations.

Edition: 207

- 21 March, 2025

Europe: Fattening up

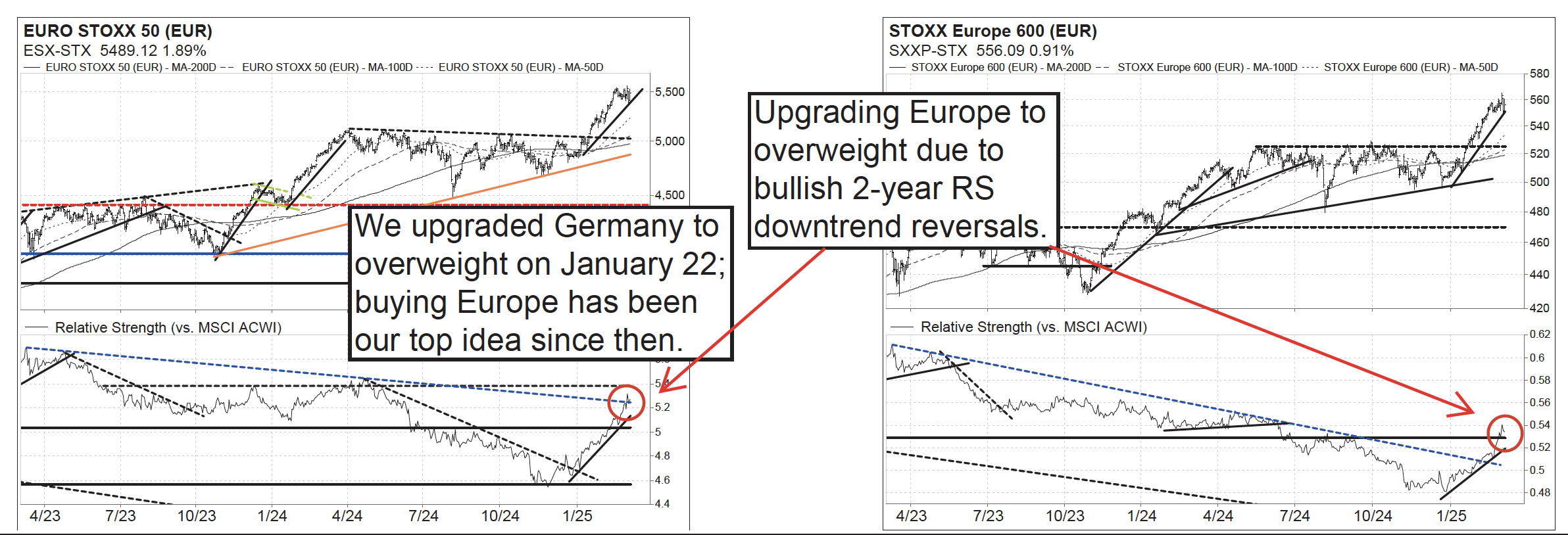

Last week the Vermilion team discussed how both ACWI-US and the S&P 500 displayed false breakouts, and to look for near-term pullbacks to range supports at $116 on ACWI-US and 5770-5850 or 5600-5670 on the S&P 500 in the coming weeks, where they would be buyers. Both levels are close. It is possible ACWI-US finds support here at the 200-day MA as it has already provided two ideal buy opportunities during this 2+ year bull. In Europe, the team has been preparing for a breakout since January, their favourite recent buy idea. They are now upgrading the broad Europe region (EURO STOXX 50, STOXX Europe 600) to overweight due to continued outperformance and participation from other countries. In terms of global equities (MSCI ACWI), the team’s intermediate-term outlook remains bullish as long as ACWI-US is above $116. The team continues to remain overweight the US and Germany.

Edition: 206

- 07 March, 2025

MSCI World hits a new high

There is a new high on the MSCI World Index, but not on US indices. Valerie Gastaldy points out that this seldom happens, but European Equities are responsible for this improvement. Bonds remain in medium-term bearish trends and may have reached their best level for the coming weeks. The Dollar still has a chance of resuming its rally, though it fell below the first key level and may simply resume the long, erratic evolution of the previous two years. Valerie’s MSCI World targets are still at 3960 and 4018, while the invalidation is unchanged below 3778.

Edition: 205

- 21 February, 2025

Bulls continue to run

Vermilion’s outlook remains bullish on global equities (MSCI ACWI). David Nicoski and Ross LaDuke viewed the recent pullback as a buying opportunity and they were watching for $116-$117 support to hold on ACWI-US – an important resistance-turned-support level dating back to July 2024. $116 support held perfectly and they expect immediate upside to continue with both ACWI-US and the S&P 500 breaking above their 1+ month bull flag patterns. They are also upgrading Germany to overweight with RS on the DAX breaking out from a 2-year base. This leaves the US (S&P 500) and Germany as their only two country overweights. Buying Europe is easily their favourite idea currently, following the 9-month base breakout. As long as ACWI-US is above $116, the S&P 500 is above 5650-5670, and the EURO STOXX 50 is above 5030, the team see every reason to remain bullish.

Edition: 203

- 24 January, 2025

It’s risk on

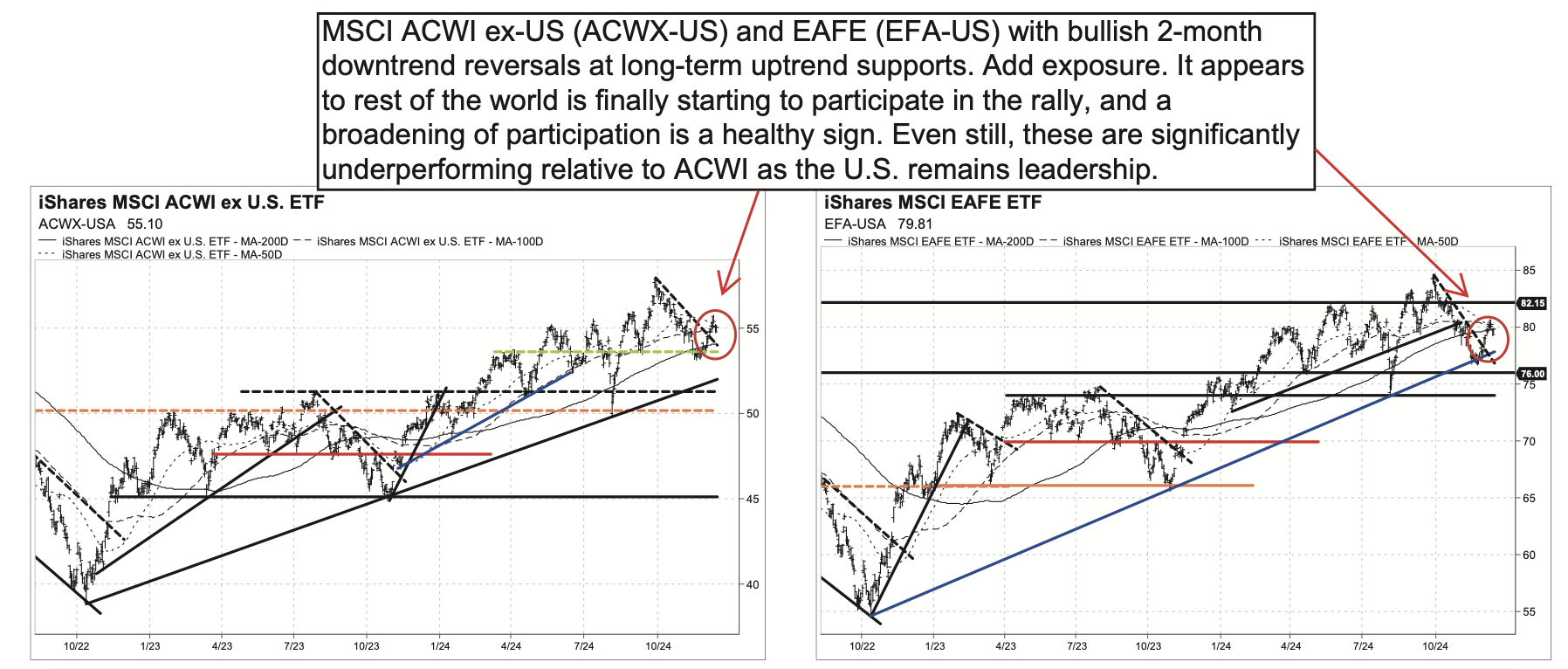

US and European high yield spreads remain at 3+ year narrows. Global sovereign 10-year yields and the US dollar (DXY) remain below critical resistance levels, and have been moving lower recently, as expected. US interest rate volatility (MOVE index) has collapsed following the election. MSCI EAFE and ACWI ex-US display bullish 2-month downtrend reversals. MSCI Emerging Markets (EEM-US) remains above its 200-day MA and the critical $41 level. Mainland China (Shanghai Composite) remains bullish. Global cyclical Sectors are outperforming (Consumer Discretionary, Technology, Financials, and Communication Services) while defensives are underperforming (Consumer Staples and Health Care). The global Discretionary vs. Staples ratio (RXI-US vs. KXI-US) is breaking to all-time highs. All of this strongly points to a risk-on environment (see charts).

Edition: 201

- 13 December, 2024

MSCI EM breaking out on Chinese stimulus

The MSCI Emerging Markets index (local currency) and EEM-US (USD) are breaking out from their multi-month consolidations thanks to significant Chinese stimulus -- add exposure on pullbacks. The Vermilion team continue to favor EM over EAFE, which has been their view since May. India (SENSEX) remains their lone country overweight, although there continues to be a plethora of countries that are bullish, including South Africa, Philippines, Argentina and Thailand. The Hang Seng is the preferred play on China as it displays a base breakout and RS has been consolidating for all of 2024; the team are monitoring for an upgrade to overweight. Nearly all EM sectors are bullish, with the exception of MSCI EM Energy. That said, the only sectors that display meaningful RS improvement are telecoms, consumer discretionary and real estate, which all have a significant weighting to China.

Edition: 196

- 04 October, 2024

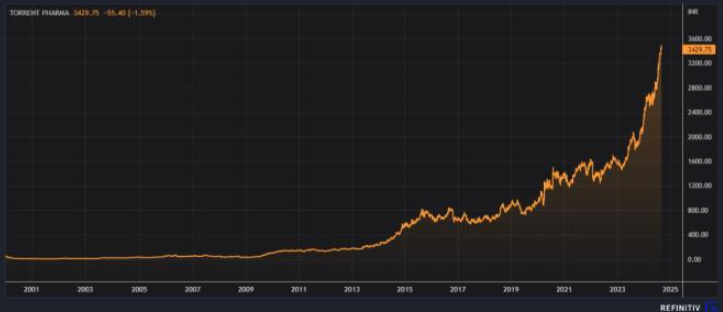

Torrent Pharmaceuticals (TRP IN) India

Healthcare

Nvidia without the drawdowns - TRP has been one of the big success stories of India's stock market. Since 1st Jan 2000, the stock is up 7950% (USD). That compares to MSCI World Health Care (USD) up +650% and MSCI India (USD) up +725%. Crystal Shore purchased TRP in their weekly GTAsia Top 10 Stocks on 2nd Oct 2023. It has been their top performing position, delivering +72% over the past 11 months. Bank Jago Indonesia is their second highest scoring position, with a +33% return (USD) since their purchase just 6 weeks ago.

Edition: 194

- 06 September, 2024

Pullback Underway

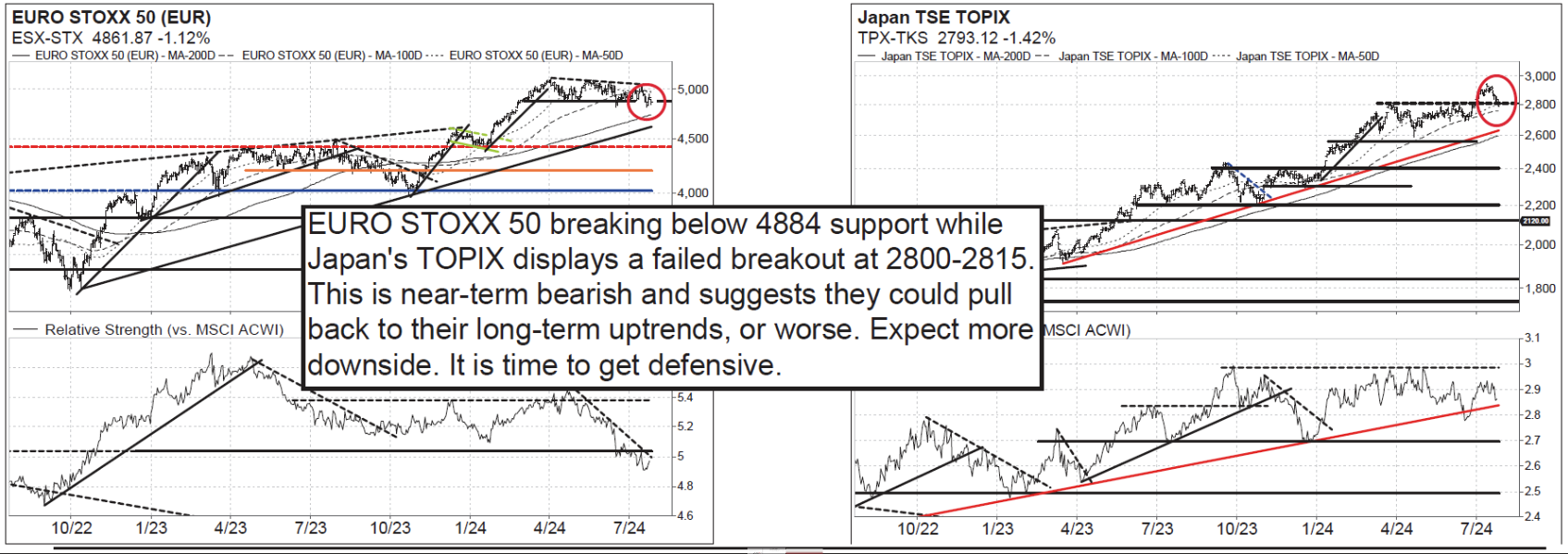

Vermilion’s long-term bullish outlook since Nov 2023 remains intact, but the team believes a 1-3 month pullback has begun. Supports to watch are at $110 on MSCI ACWI (ACWI-US) and $41-42 on MSCI EM (EEM-US), and whether these levels hold or not will determine the severity of the pullback. The S&P 500 is violating its 20-day MA, Europe's EURO STOXX 50 is breaking below 4884, and Japan's TOPIX appears to be staging a false breakout at the 2800-2815 level. This all points to more sideways to lower price action in the near-term. Global value sectors have continued to outperform in recent weeks and this area remains the team’s main focus. They are interested in defensive sectors as global equities pull back.

Edition: 191

- 26 July, 2024

Global retreat

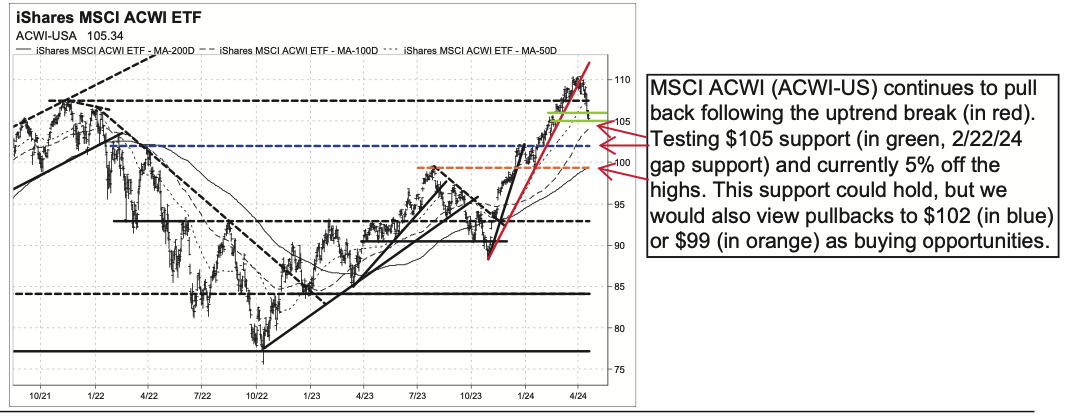

A pullback in global equities is underway following steep uptrend violations on the MSCI ACWI further downside may be limited. Several 5-10% pullbacks are to be expected in any given year – particularly after the historic 5-month rallies – so the Vermillion team view this as healthy and normal within the ongoing bull market. ACWI-US is currently testing important support at $105; if this area were to break, next major supports are $102 and $99. A pullback to $102 would be 7-8% off the highs, while a test of $99 would be 10% off the highs. As long as $99 holds on ACWI-US, the team continue to treat pushbacks as buying opportunities.

Edition: 184

- 19 April, 2024

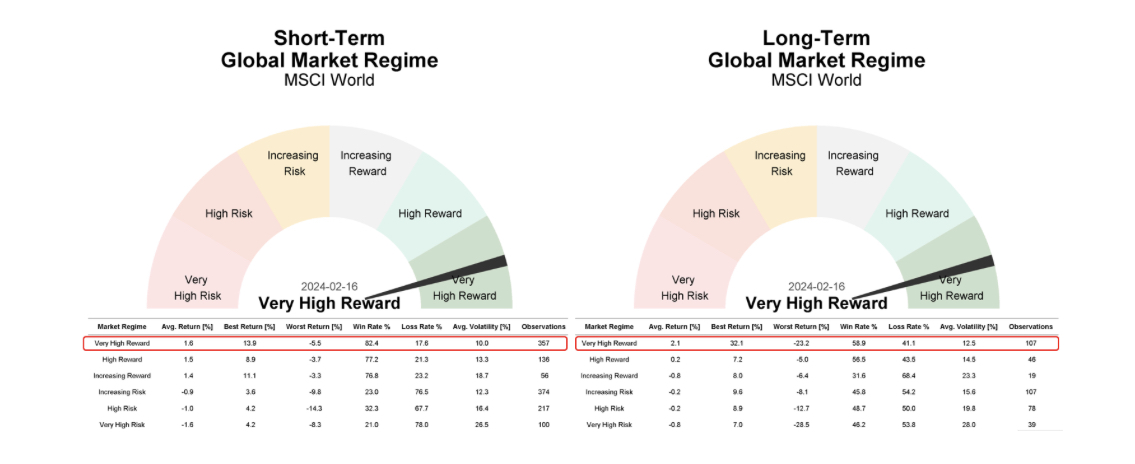

Has the bull market gone ahead of itself?

The MSCI World has surged by 28% since late October, with no pullback exceeding 3%, prompting concerns that the rally may have gone ahead of itself. Despite these impressive gains, WallStreetCourier’s data currently provides no evidence of an imminent correction. The strong uptrend continues to be supported by robust signals from 1500 indicators across 26 major indexes and sectors covering trend, trend quality and smart money positionings. This fact continues to confirm their positive outlook on the MSCI World, which they covered multiple times last year. Throughout history, the MSCI World (MXWO) saw gains in 84.6% of instances during short-term 'Very High Reward' market regimes and in 70% of all cases during long-term ones.

Edition: 183

- 05 April, 2024

The narrowing divide between China and India’s weight in the MSCI Indices

The spread between India and China weights in active Asia Ex-Japan funds has narrowed to the lowest levels in Copley’s 13-year history and now stands at 16.17% vs. a peak of 45.3% in Aug 20. China’s decline over this period has been dominated by Consumer Discretionary, Communication Services and Financials. 3 companies standout as key drivers of the move lower: Alibaba, Tencent and Ping An Insurance. Increases in fund weight have been minimal with PDD, BYD and Trip.com seeing moderate upticks. India’s rise has been driven by the Financials sector. Specifically, 3 banks: ICICI Bank, HDFC Bank and Axis Bank.

Edition: 180

- 23 February, 2024

Industrials

AI-hype is aboard the TRI express with the shares recently hitting an all-time high. The stock sells at 23.5x 2025E EBITDA, 40x 2025E Earnings and 37x FCF. This is higher than any other Information Services company Huber Research tracks apart from MSCI (rated OW), but MSCI has a huge moat around its business and 60% EBITDA margins. That is not to say CEO Steve Hasker has not been masterful in re-positioning TRI into growth opportunities and raising the margin profile of the company’s three key segments, but at the end of the day, this is a 6-7% organic growth story, with EBITDA margins in the mid-40% range. Douglas Arthur now estimates 2024 adj. EPS of $3.54 per share (prior $3.80).

Edition: 180

- 23 February, 2024

Bullish brilliance: Positive outlook on the MSCI World still persists

Since WallStreetCourier emphasised the “very high reward” market regime in mid-Dec, the MSCI World has surged by 6%. This positive market regime continues to be supported by robust signals from 1,500 indicators across 26 major indexes and sectors. Their data reinforces the expectation for a sustained continuation of the global bull run, with all Market Health indicators displaying robust signals. Historically, the MSCI World demonstrated gains in 82.4% of all cases when operating within a very high reward market regime.

Edition: 180

- 23 February, 2024

EM: Wearily bullish

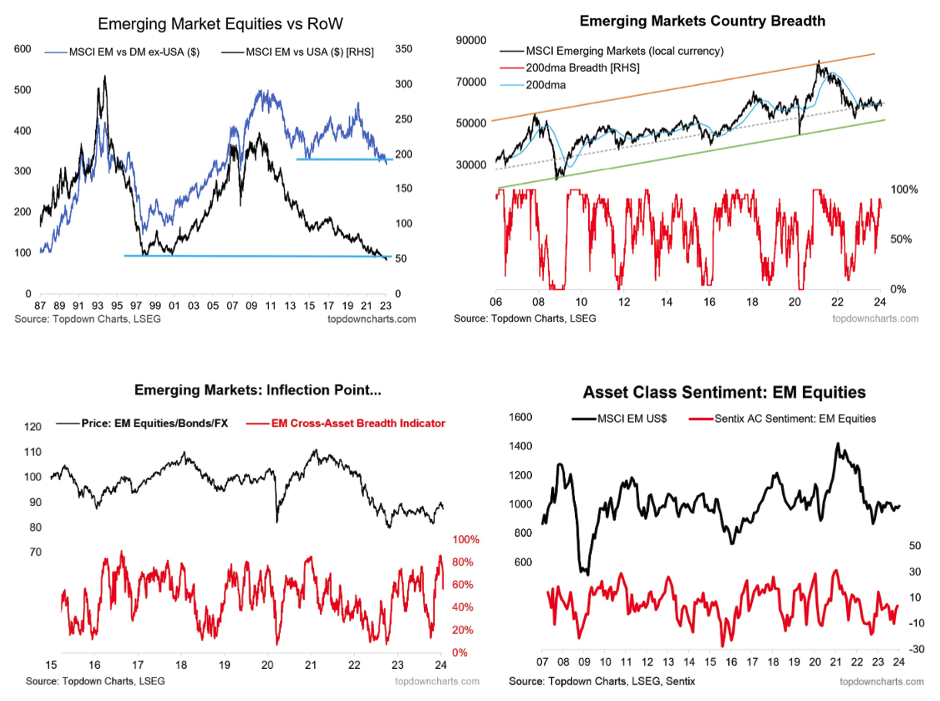

EM equities have broken down through key long-term support lines relative to DM and US equities, which is a concern. However, the MSCI EM index in local currency has held onto its long-term uptrend line with strong breadth. Callum Thomas sees the rebound in the USD as a key risk to EM. There is hope in the form of the EM policy pivot to easing, but this will need to be large and fast enough to offset further USD strength. Meanwhile, the EM cross-asset breadth indicator has held onto its major inflection point and surveyed sentiment on EM is ticking up but is not excessive. The background of cheap valuations, upward trending broader sentiment indicators, the EM central bank pivot, and potential for Chinese stimulus means EM equities remain attractive. Remain bullish but reduce conviction in the face of short-term risks/headwinds.

Edition: 178

- 26 January, 2024

CSD’s Top 10 Asia Stocks have outperformed MSCI Emerging Asia by an astonishing +55% over the past 2 years

The flagship strategy combines 1) CSD’s weekly ranking of 900 Asian stocks and 2) CSD’s country risk scores covering China, India, Taiwan, South Korea, Indonesia, Thailand, Malaysia, Philippines and Pakistan. Top 10 Asia stocks is delivered to subscribers every weekend before the Monday morning market open in Asia. The top 3 performing positions are Hindustan Petroleum (+74.2% since BUY on 15th May 2023); Tata Consumer Products (+31.6% since 2nd Oct 2023 BUY); and Yes Bank (+30.6% since 4th Dec 2023 BUY).

Edition: 178

- 26 January, 2024

How to make money in China in 2024

Jonathan Anderson expects local rates and fixed income markets to remain steady this year, as well as a relatively stable exchange rate – but given how compressed yields and spreads are, this isn’t a particularly attractive sector. Nor is Jonathan interested in China-related commodities, which he believes is subject to downside pressures this year. The more interesting market is equities, where (i) both A-share and MSCI China indices are trading at very low multiples, (ii) inherent price volatility is much higher and (iii) returns are historically uncorrelated with either macro or policy activity. Jonathan isn’t buying stocks today, but is ready to enter once he sees sentiment returning. Offshore high-yield dollar bonds are also a rollercoaster market; spreads have narrowed considerably and he worries that pricing is overly optimistic, but he would revisit exposure in a renewed sell-off.

Edition: 177

- 12 January, 2024

Mexico: Signs of further upside

The Vermilion team are upgrading Mexico to Overweight, citing many reasons to be bullish equities into year-end and the beginning of 2024. This includes bullish price patterns and minimal pullbacks on broad global indexes; the continuing lower trend of the USD; European high yield spreads are at 20-month and 9-month narrows; defensive MSCI ACWI sectors remain in YTD downtrends; and US and non-US small caps appear to be putting in RS bottoms. The significance of the risk-on signals cannot be understated, expect upside to continue.

Edition: 176

- 22 December, 2023

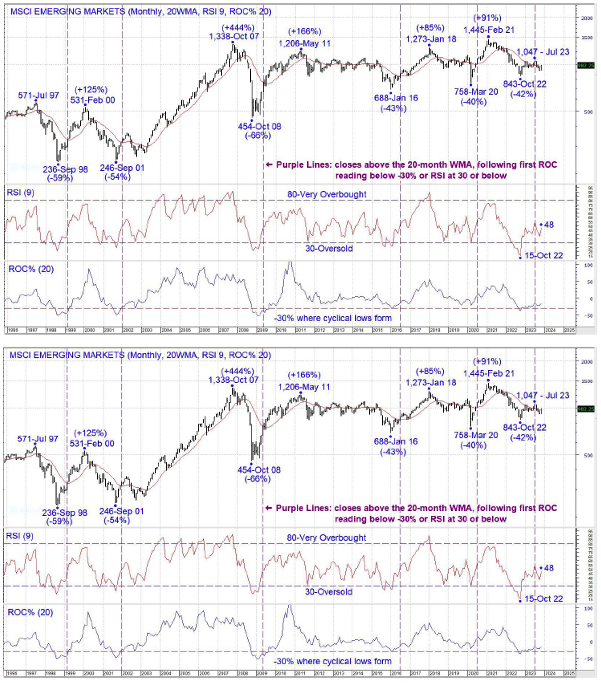

MSCI EM: Time to break free?

Writing about the MSCI EM Index in 2023 feels a bit like a DJ playing a new Earth, Wind and Fire single, but the collective EM is still a thing and looks like it may get more interesting in 2024. The monthly chart shows a peak in October 2007 of 1,338, that is no longer the all-time high but that level marks the beginning of a now 16-year ceiling for the index. On a positive note, the 2008 low of 454 has been followed by a series of rising cyclical lows in 2016, 2020 and 2022. The weekly chart shows an initial 26% rally from the important 2022 low, and the index has now been rangebound for 9 months, forming a potential rectangle. A breakout from the range would signal another cyclical advance, perhaps driven by some improvement in Chinese equities.

Edition: 174

- 24 November, 2023

MSCI EM Index reversing 3-month downtrend

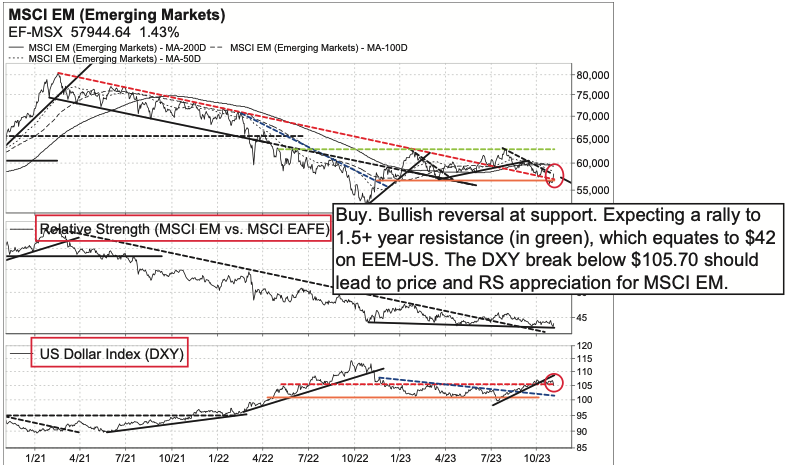

In Vermillion’s prior EM Strategy, Ross LaDuke discussed that MSCI EM (EEM-US) was again approaching major 10.5-month support at $37-$37.50, which has been their important line-in-the-sand throughout 2023, and that as long as EEM-US is above $37, Vermillion are buyers on this pullback. This support level held and EEM-US now displays a bullish 3-month downtrend reversal as the US dollar (DXY) appears to be breaking below $105.70 – all rather bullish signals suggesting this rally is just getting going -- BUY. Ross is bullish as long as $36.50-$37 support holds on EEM-US. His first target is $42, which is 1.5+ year resistance. Additionally, he remains neutral on EM vs. EAFE; the EAFE vs. EM ratio is moving sideways following the 2.5-year downtrend reversal.

Edition: 173

- 10 November, 2023

EM: Positive on all counts, just waiting for a catalyst

EM technicals have been mixed-to-positive with the MSCI EM index ticking along its long-term uptrend line with reasonably strong breadth, and the relative price line vs DM and US zeroing-in on a major long-term support level. Meanwhile the core case still stands: cheap valuations, bearish sentiment – i.e. contrarian bullish, and monetary conditions turning from previous major headwind as EM central banks pivot. USD remains a double-edged sword, with the YoY figure still negative but the DXY brushing up against a major resistance level. Overall, while technicals/value/sentiment/monetary factors are all improving, the still absent key upside catalyst would likely come in the form of a more meaningful pivot to easing by EM central banks, and ideally a weaker USD.

Edition: 170

- 29 September, 2023

Luxury downside

Consumer Discretionary

The MSCI Europe Textiles, Apparel and Luxury Goods Index accelerated to the downside last week - Valérie Gastaldy points out that prices have already fallen below the 38% Fibo since 2022 (at 1325). Should the index correct the rally since 2020, the most reasonable target would be 1207. However, should we be correcting the move since 2009, then the target would be 1020. Re. individual stocks, Hermes is trying to break below its summer lows and the next level where Valérie would consider buying LVMH is at €665. She has set major medium-term support for Moncler at €53.3, but the stock is weaker than the other two and can more easily fall significantly lower if the other two do break equivalent supports.

Edition: 169

- 15 September, 2023

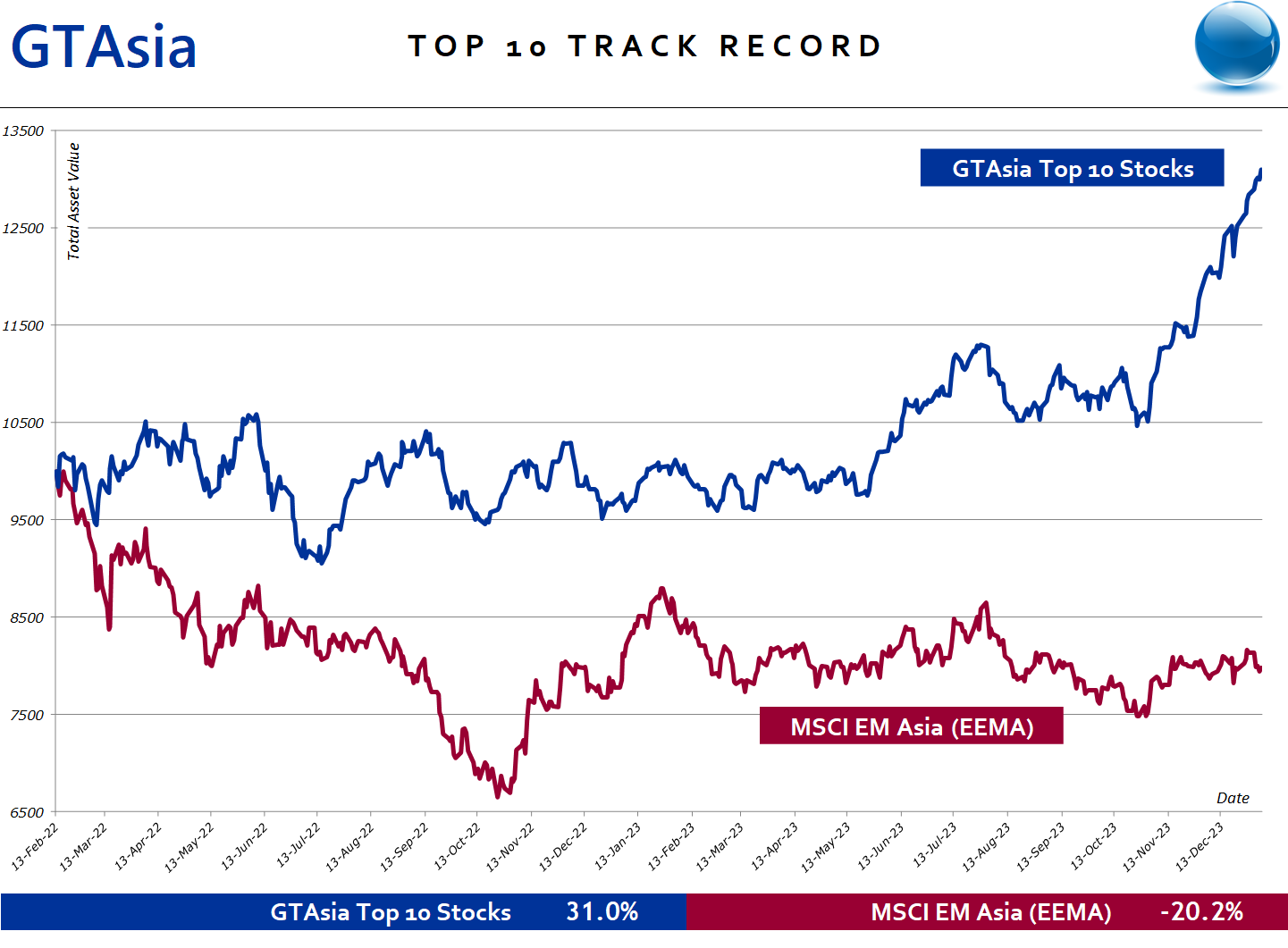

GTAsia Top 10 Stocks delivers eye-opening returns in falling markets

Asia EM has been clobbered over the past 30 months, down -35% since the mid-Feb 2021 high. Crystal Shore Dashboards (CSD) launched their GTAsia Top 10 Stocks on 14th Feb 2022, right in the middle of this meltdown and have generated a positive return: +10% vs. MSCI EM Asia at -21%. CSD achieved this result by systematically ranking 960 EM Asia stocks on a weekly basis. They then ran a macro overlay on these quintile rankings using their Asia country risk scores. Their top 3 performing stocks today: Aurobindo Pharma (+40% since purchase), Gail India (+14%) and Indian Railway Catering & Tourism (+13%).

Edition: 169

- 15 September, 2023

The decline in Turkish investor positioning

Ownership levels in Turkish equities have fallen to new lows among active EM equity funds. The percentage of funds invested in Turkey stands at an all-time low of 31.45%, pushing average holding weights down to just 0.38%. For the first time since 2008, active managers are now running an underweight in Turkey, with just 18.6% of funds positioned ahead of the iShares MSCI Emerging Markets ETF. With both active weights and benchmark weights so small, the risks of not holding a Turkey position are diminishing for the average active manager. Only 16 of the 373 funds in Copley Fund Research’s analysis hold more than a 2% allocation – to bet big on Turkey here is a significant non-consensus call.

Edition: 168

- 01 September, 2023

TMBThanachart Bank (TTB TB) TB

Financials

Conservatively managed TTB produced a strong set of numbers in 2Q23 and the bank's elevated PH Score™ (9.4 out of 10) is indicative of superior relative returns going forward. Paul Hollingworth notes that there were improvements across almost all key variables - in Profitability, Capitalisation, Margin/Spread, Provisioning and in Liquidity. Management's strategy is focused on raising profitability via revenue synergies from the merger, adding a product for each customer (cross-selling of home and auto products plus other consumer offerings), widening digitalisation and continuing to get the CIR lower (40% target). The stock is up +46% since Paul turned bullish (vs. MSCI EM Index -24%).

Edition: 166

- 04 August, 2023

Bullish signs in frontier markets

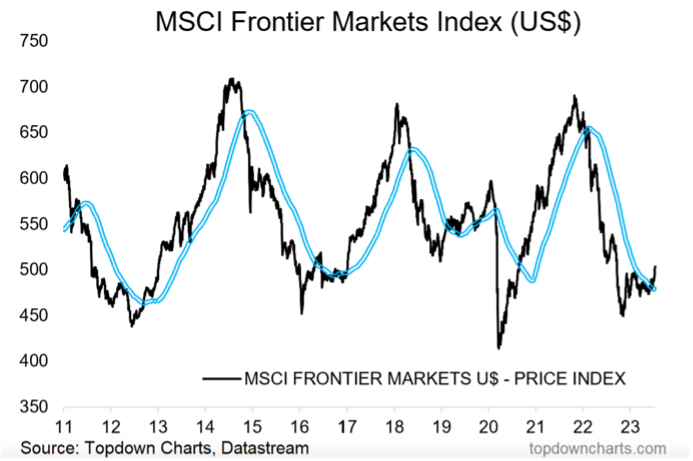

Frontier market equity technicals are looking up as the MSCI FM index notches up a new high and pushed above its 200-day MA (see chart). Callum Thomas believes the strategic case for frontier markets is intriguing and mostly overlooked. FM equities sit at the top of the expected return table, have historically traded on lower correlations vs other major chunks of global equities and lower historical volatility than EM equities. The FX situation is also consistent with the bullish technicals and strategic outlook, with FM FX trading at record cheap valuations and FM FX breadth trending up.

Edition: 165

- 21 July, 2023

China Consumer Staples: Conviction overweight

Consumer Staples

Steven Holden reports how active MSCI China funds are positioned for the outperformance of the Consumer Staples sector - overweights are near record levels at +3.97% above the benchmark. Today’s 7 most widely held stocks in the sector join a prized group of just 15 companies that have ever been owned by more than 20% of funds at any one time. Dubbed the 20% Club, 8 of these stocks have since left, with Luzhou Laojiao the most recent entrant. The remaining 6 stocks are Kweichow Moutai (the highest conviction holding), China Mengniu Dairy, China Resources Beer, Wuliangye Yibin, Inner Mongolia Yibin and Tsingtao Brewery.

Edition: 163

- 23 June, 2023

Opportunities in the EM landscape

MSCI EM (EEM-US) has continued to hold above Vermilion Research’s $37-$37.50 line-in-the-sand, meaning they are constructive from a price perspective. That being said, RS has been neutral at best, and they have maintained an underweight to emerging markets. There are still plenty of attractive countries and sectors within the EM landscape. Top country overweights continue to be Taiwan (TAIEX), India (S&P BSE SENSEX), South Africa (FTSE JSE All Share) and Mexico (S&P/BMV IPC). MSCI EM Technology continues to be an overweight, and MSCI EM Energy and Financials have been upgraded to overweight too.

Edition: 161

- 26 May, 2023

Will investors return to India soon?

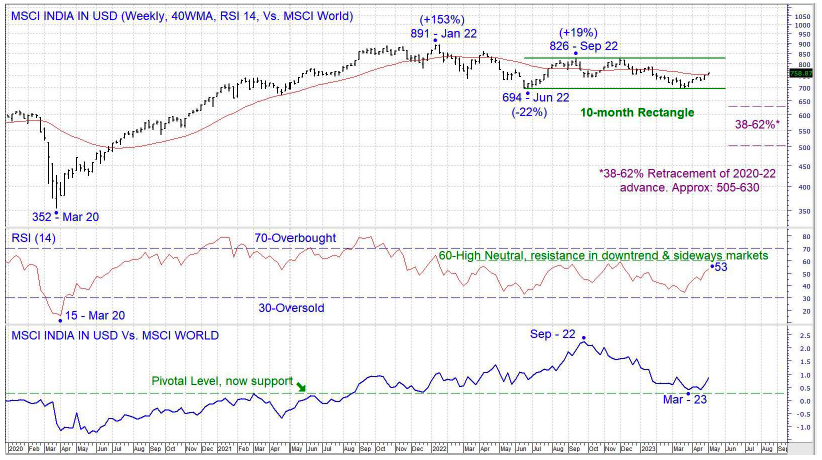

The MSCI India in USD has been rangebound for 10 months, following a very shallow retracement of the 2020-22 bull market. The shallow correction, combined with the relative performance vs the MSCI World, show what an investor favourite this market was post the Covid-19 bear market lows. An upside breakout from the 10-month range would likely trigger investment flows from global investors again.

Edition: 160

- 12 May, 2023

China A-Share Financials: Out of love

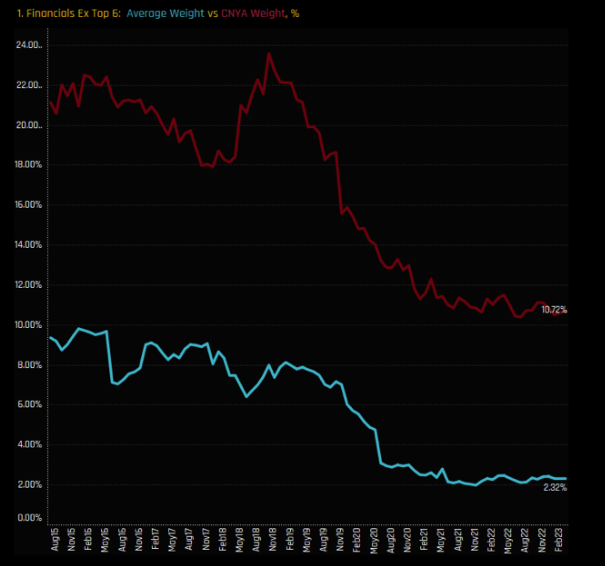

Ownership levels in the China A-Share Financials sector are at their lowest ebb, driven by lack of confidence. The top 6 most widely held Financial stocks make up 5.5% of the average active A-share fund and 5.75% in the iShares MSCI China A-Share ETF, but it’s outside of this where the divergence between active and benchmark occurs. Across 83 companies, active A-Share funds have allocated just 2.32% whereas the iShares MSCI China A-Share ETF has allocated 10.72%. The message is clear – stick to the top 6 and avoid the long tail.

Edition: 159

- 28 April, 2023

Technology

New Street takes advantage of recent share price weakness post WISE's 4Q23 update to upgrade the stock to Buy - whilst TPV was a touch light, they think the market's focus should be firmly on the new steer for NII which drives material upgrades to EBITDA (40% in fiscal 2025). The market has been contorting itself to keep near-term EBITDA margins at ~20% (as per mid-term guide) when in reality it will be nigh on impossible to reinvest a significant portion of NII gains on any sort of near-term basis. Along with street upgrades, potential MSCI inclusion (May) is another catalyst. TP increases to £6.75.

Edition: 159

- 28 April, 2023

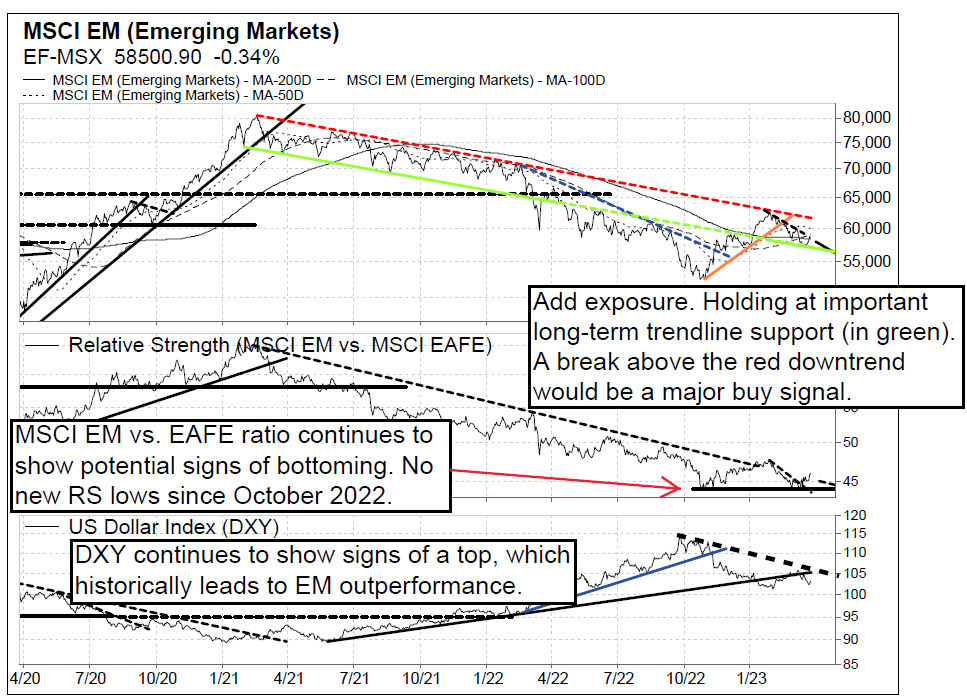

MSCI EM 2-month downtrend reversal at support

In Vermilion Research’s February EM Strategy, the team mentioned they were buyers of the MSCI EM (EEM-US) on a pullback to the 50-day MA. The pullback went a bit deeper but managed to hold at their $37.50 line-in-the-sand. The EEM-US now displays a bullish 2-month downtrend reversal -- add exposure. Additionally, the MSCI EM index (local currency) is holding at an important long-term support level (see chart, green trendline). Signs continue to point to a topping U.S. dollar (DXY), and a declining DXY has historically resulted in EM outperformance relative to EAFE. As long as the DXY remains below $105.50, the team expects to see the MSCI EM form a relative strength bottom (vs. EAFE).

Edition: 157

- 31 March, 2023

Mexican allocations continue to surge higher

Over the past 6 months there has been some aggressive country repositioning among active EM managers - Mexico is now the largest country overweight position (vs. the benchmark iShares MSCI EM ETF). Despite this sentiment shift, Steven Holden says allocations look far from stretched (avg. weights among active EM funds: 3.4% today vs. nearly 5% in 2015). On a Style basis, Yield managers have increased weights the most. On a stock level, Grupo Financiero Banorte and Wal-Mart de Mexico have been instrumental in Mexico’s rise up the ranks.

Edition: 147

- 28 October, 2022

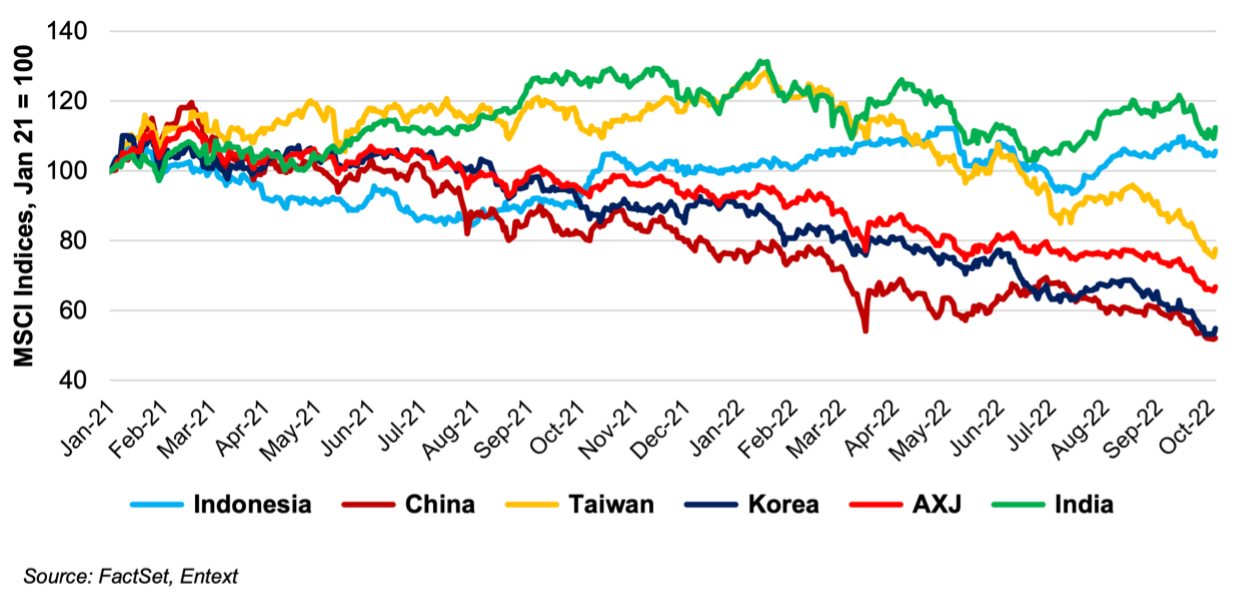

India has become a momentum trade comfort blanket

Sean Maher believes that Indian stocks are now trading on a historically expensive premium versus wider EM, propped up in part by the ‘India as the next China’ soundbite (see graph). The country is attempting to embark on the China path but lacks the ingredients. As stimulus rises in China and the pro-growth Li faction in the ascendant, Sean has opened up a LONG MSCI China versus India position in anticipation of a mean reversion over the next few months.

Edition: 146

- 14 October, 2022

Asia ex-Japan Q3 performance was challenging for active managers

Steven Holden examines Q3 performance among the Asia ex-Japan active funds, breaking down this quarter’s performance relative to the iShares MSCI Asia Ex-Japan ETF (AAXJ). The last quarter was a challenging one for active Asia Ex-Japan managers. The return distribution shows the managers losing between -18% and -14% over the period. Aggressive growth and value managers were the only Style groups to outperform over the period, driven by stronger returns from the Small/Midcap end of the spectrum.

Edition: 146

- 14 October, 2022

After 15 terrible years, when will things look up for Europe?

With the MSCI Europe index almost 30% below its 2007 peak (in US$), it’s fair to say European equities have done poorly. The near-term outlook doesn’t look much good either, yet Gerard Minack is more upbeat on a medium-term view (3+ years). He argues that the next cycle will suit Europe; an investment-led cycle that will benefit sectors that produce tangible outputs. Also, European valuations look cheap relative to their expensive American counterparts. A cheap Euro will also help. Look past the near-future and things are looking up.

Edition: 143

- 02 September, 2022

China Tourism Group Duty Free (1880 HK)

Consumer Discretionary

Is looking to sell up to 118.176m shares to raise up to US$2.5bn - pricing at HK$143.5-165.5/share is a 38.6%-29.2% discount to China Tourism Group Duty Free (601888 CH). Brian Freitas believes the stock could be added to MSCI China Index in November and to the FTSE All-World and FTSE China 50 indices in March. Southbound Stock Connect could come online on 19 September providing opportunities to trade the A/H spread.

Edition: 142

- 19 August, 2022

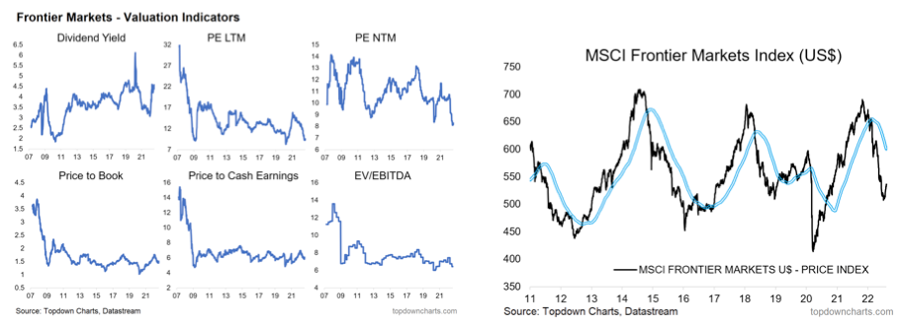

Moving bullish on frontier markets

After a -26% drop, Callum Thomas claims frontier market (FM) equity valuations are much improved, looking cheap on a number of metrics (see charts). Technicals are also improving, with breadth metrics tentatively turning up after going oversold, and the MSCI Frontier Markets index bouncing off support. Callum also comments on EM FX, with recent EM currency weakness pushing the valuation indicator into extreme cheap territory. With the highest expected returns, Callum is bullish FM equities.

Edition: 142

- 19 August, 2022

GCL Technology Holdings (3800 HK)

Energy

Double index inclusion and huge passive inflows - after being deleted from major global indices last year due to prolonged suspension, Brian Freitas expects GCL will be added to the MSCI China Index and the FTSE All-World Index over the next few months. This will require passive trackers to buy over US$1.1bn of GCL stock. Even after the recent rally, GCL trades cheaper than its peers on EV/EBITDA, forward PE and price to book.

Edition: 139

- 08 July, 2022

Stay long China tech

Back in March, the MSCI China Index saw its valuation halve in a year to about 9x 12mth forward earnings, vs the 5yr average of 12.6x. However, the sector is now a remarkably cheap leveraged play on a diplomatic resolution to the Russo-Ukrainian conflict, belated regulatory stability and a surge in buybacks and even PE deals among the smaller players. If China is perceived to be creating distance from Russia, and so avoiding sanctions risk, the rally in mainland tech names will accelerate in Q2.

Edition: 133

- 14 April, 2022

An extensive EM view

Crystal Shore Dashboards generates weekly buy/sell risk scores on all 34 individual emerging countries and on a staggering 1,200 single stocks falling under MSCI Emerging Markets, virtually the entire universe of the ETF. In addition to this extensive view, Crystal Shore Dashboards also offers six defined strategies for investing in EMs through either single stocks or ETFs, all easy to manage and execute. To find out more, please get in touch.

Edition: 132

- 01 April, 2022

China is risking an ESG embargo over Russian support and Xinjiang

Is China facing a selling pressure based on governance? Paul Krake argues we could see a longer-term move towards private sector covert sanctions and investment embargos as major firms divest from Chinese assets (US pensions in particular). Currently, global allocations to Chinese stocks and bonds fall short of its economic might (MSCI has a 6% allocation despite China accounting for 17% of global output). The structural bull scenario was that this gap would be closed, but Russia and Xinjiang make it highly unlikely in the years to come.

Edition: 131

- 18 March, 2022

Technology

Can the stellar share price performance continue? This is a high-quality fabless semiconductor company, with significant revenue growth, generating returns well above its cost of capital, a net cash balance sheet, and an attractive sustainable dividend. Although current valuation levels are above historical average levels, Wium Malan expects a continuation of the earnings upgrade cycle to provide a positive share price catalyst. The stock is also likely to see large passive inflows following the MSCI November Semi-Annual Index Review.

Edition: 122

- 29 October, 2021

Lack of clarity on company emissions

Curation Corp comments that companies have a long way to go when it comes to clarity from organisations on emission disclosures. To keep within the 1.5C emissions target of 61.4 gigatons of CO2 equivalent, drastic cuts are required; right now, the budget is on course to run out in six years according to the MSCI Net-zero tracker. An international framework requiring firms to disclose climate risks may soon be reality, and it’s needed.

Edition: 116

- 06 August, 2021