Fortnightly Publication Highlighting Latest Insights From IRF Providers

Company Research

Communications

NBIS announced its first hyperscaler contract - a 5-year deal with Microsoft worth up to $19.4bn, which will consume nearly the entire capacity of its New Jersey facility. The agreement marks a major validation of NBIS’s model, significantly de-risking its capacity buildout plans as it targets 1GW across the US in the coming years. Hamed Khorsand thinks the deal provides unprecedented clarity on the company's long-term revenue potential and opens the door to further hyperscaler partnerships. Following the news, the shares surged ~50% and are now up 170% since he turned bullish in Jan 25, however, Hamed continues to see significant upside raising his TP from $90 to $130.

Edition: 220

- 19 September, 2025

South Africa: One small cut, one big implicit signal

Krutham (formerly known as Intellidex)

The SARB’s recent rate cut, while long anticipated, marks a shift in tone as risks are now seen as balanced and a 3% inflation target scenario was introduced, suggesting a preference for anchoring inflation at the lower end of the target range. However, Peter Montalto finds this scenario implausible, since it assumes a smooth and immediate re-anchoring of inflation with little macro cost. Despite lower CPI and growth forecasts, the baseline suggests a gradual rate path with the QPM-implied repo rate dropping to 6.93% by end-2025. A July cut is seen as 40% likely, with future moves dependent on global conditions and SARB communication. The next MPC meetings are set for July, Sept and Nov, with cuts unlikely beyond July without further data shifts. Peter sees the official target only being changed next year.

Edition: 212

- 30 May, 2025

Jumbo (BELA GA) Greece

Consumer Discretionary

ResearchGreece flags growing competitive risks as Dutch retailer, Action, reveals plans to open its first store in Romania later this year. This marks the first time a similar, yet more aggressive, retail chain is entering into one of Jumbo’s markets (Romania contributes 22% to group sales). Action offers 6,000 products across 14 categories that compete with Jumbo's, with about two-thirds of these items priced under €2.00. Furthermore, investors should not rule out the possibility that Action may choose to enter Greece, where Jumbo operates 53 out of its 89 stores, given Action has identified existing and potential markets with the capacity to add an additional 4,700 stores.

Edition: 208

- 04 April, 2025

South Africa: 25bp of comfort blanket

Krutham (formerly known as Intellidex)

The SARB’s MPC kept rates unchanged at 7.50%, as expected. While this move aligns with Peter Montalto’s expectations, he believes the MPC missed an opportunity to cut, given the (very) benign inflation outlook in both the short and medium term. The MPC overemphasises global geopolitical and trade risks versus the realised downside risks. Still, it is quite clear they are remaining highly risk averse and want to keep a 25bp buffer vs neutral – for now - by sitting at the top end of the neutral range. The key question now is whether this marks the end of the cutting cycle. Peter reckons that it does. He maintains his longstanding view that if any further easing were to happen, it would likely be limited to just one more cut to bring rates to neutral. The baseline for now to be clear is no further cut.

Edition: 207

- 21 March, 2025

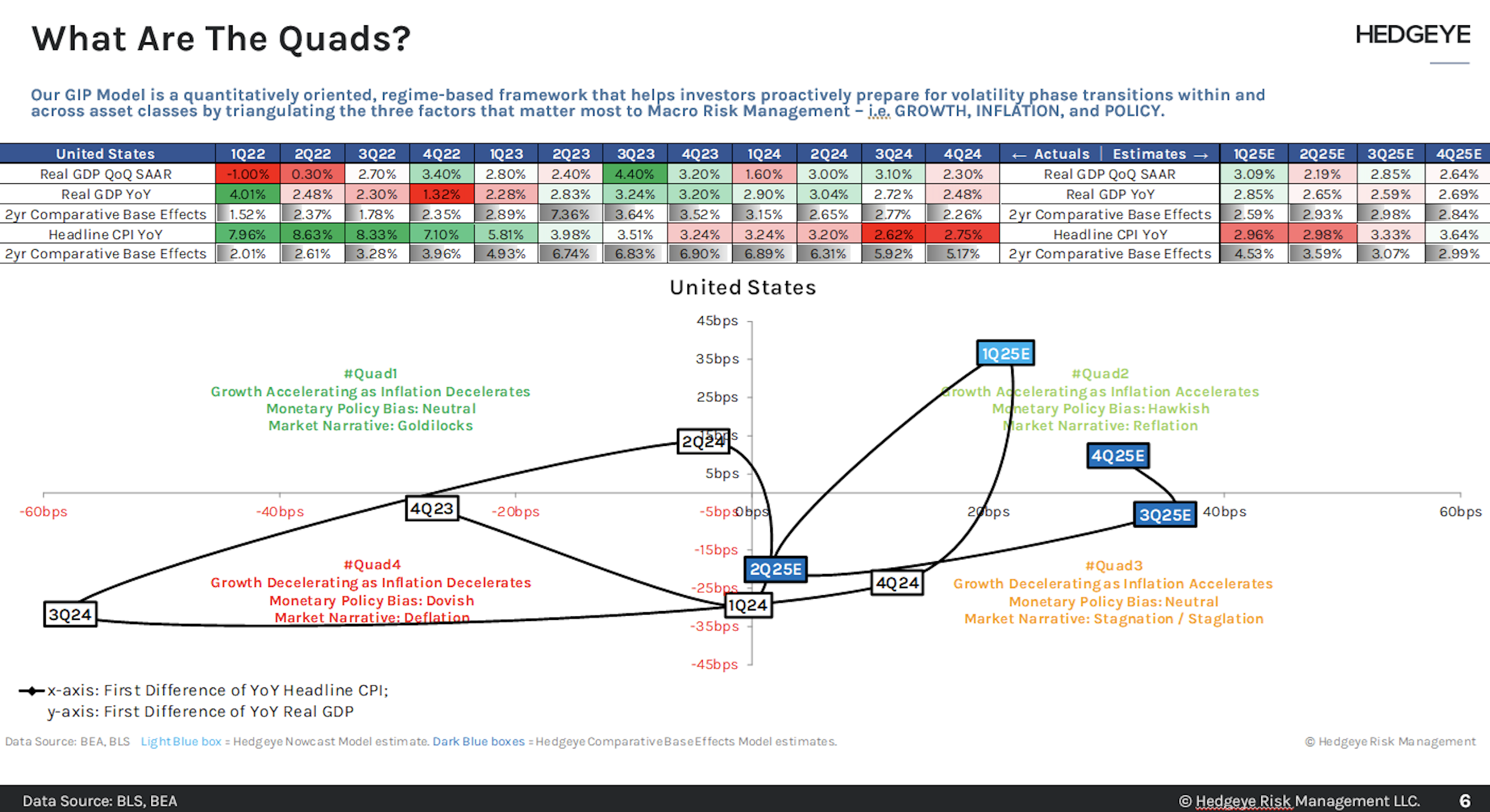

US: Growth forecast for the year ahead

Q4 2024 Real GDP growth of 2.48% Y/Y (2.23% Q/Q SAAR) was a -24bps deceleration from Q3 2024’s real GDP growth of 2.72% (3.04% Q/Q SAAR). The Hedgeye team generally regard ~25bps delta change as the cutoff point for what they consider “shallow” GDP deceleration, putting Q4’s decel just inside the shallow cutoff. Their current Nowcast estimate for Q1 Real GDP growth of +2.85% growth Y/Y marks a healthy RoC acceleration from Q4’s 2.48% growth and equates to 3.05% Q/Q SAAR. Coupled with their estimate for accelerating inflation on a full-quarter basis, this suggests Quad 2 is most likely for Q1 (see graph). Their Q2 and Q3 Real GDP growth forecast estimates call for growth of 2.65% and 2.59%, suggesting Quad 3 is most likely for both Q2 and Q3. Finally, looking forward to Q4, expect growth to reaccelerate to 2.69%, and increase of +10bps in RoC terms. Coupled with expectations for accelerating Q4 inflation, this suggests that Q4 will be Quad 2.

Edition: 204

- 07 February, 2025

The green agenda hits a red wall

The re-election of Trump marks a significant shift for sustainability-focused investors. Anticipated regime changes include higher bond yields and resurging inflation, and some changes to the fiscal tailwinds coming from the soon-to-be defunct Inflation Reduction Act. The fundamentals tied to the energy transition remain unchanged: demand for power is growing fast, and clean energy is cheaper and quicker to build than fossil fuel power plants. The recent devaluation of green equities creates opportunities for savvy investors and the Sustainable Market Strategies team suggest investors take a back seat for now and look for opportunities to acquire undervalued stocks. In the short run, they should look for companies with a limited exposure to the US and who still have strong businesses outside the country. Over the medium term, they could also look into re-entering into renewable companies with a strong business pipeline in the US given the current trends in the country’s power demand.

Edition: 199

- 15 November, 2024

FTSE 100 Technical Review

Messels' weekly Stocks & Sectors report highlights continued improvement in Services, Media and Banks, while reducing exposure to Consumer sectors. New Buys include Ashtead (broken out of 2-year price and relative ranges) and Barclays (renews the uptrend and has broken out of 8-year price and relative ranges). They have also closed longs in Whitbread (lacks momentum in the short term), Imperial Brands (maintains the uptrend but is reaching the top of the relative range), Howden Joinery (lost momentum and developed short term price and relative tops) and Marks & Spencer (reaching medium term price and relative resistance). Following these changes, Messels’ FTSE 100 Momentum portfolio now consists of 16 stocks.

Edition: 199

- 15 November, 2024

US: A boost in capex?

In this week’s note Barry Knapp reviews the inflation and economic data in detail, marks the monetary policy outlook to market ahead of the Jackson Hole Economic Policy Symposium, offers his thoughts on the evolving political policy outlook and updates his sector and asset allocation views. Broadly, Barry’s medium-term outlook is for a strong capital spending cycle like the ‘60s or ‘90s enhanced by accelerated technology innovation adoption diffusing across a range of sectors, notably healthcare. This secular trend in turn would overcome excessive government spending and deficits as well as Fed intervention into a part of the market they have no business being involved in, namely the setting of longer-term rates. In the near-term, however, Barry has a negative bias because of his concerns about government interventions to stabilise ‘market failings’, mostly making things worse.

Edition: 193

- 23 August, 2024

FTSE 100 stocks & sector review

Messels currently has 19 long positions in their FTSE 100 Momentum portfolio having closed their position in Rio Tinto after it pulled back in the five-year range and broke medium term relative support. They remain overweight Retail and in particular, Howden, Tesco and Marks & Spencer which maintain uptrends and JD Sports and Kingfisher which renew base formations. Other stocks highlighted in their technical review this week include Informa, which has rallied back to the highs and rallies from relative uptrend support; while M&G finds 18-month uptrend support and develops a base at the bottom of the relative range.

Edition: 191

- 26 July, 2024

bpost (BPOST BB) Belgium

Industrials

Quality comes at a price - while the size and valuation of the recently proposed Staci acquisition has some analysts and investors concerned, it marks a first credible step aimed at accelerating the transformation of BPOST into a company with a bigger exposure to growth activities and higher margins. Analysts at the IDEA! think the process BPOST is going through shows some parallels with that of the three largest Dutch publishers in the late 1980s and 1990s. In view of the current valuation of the shares (just over 2x EV/adj. EBITDA) they feel that this is beginning to turn into an increasingly compelling investment case.

Edition: 184

- 19 April, 2024

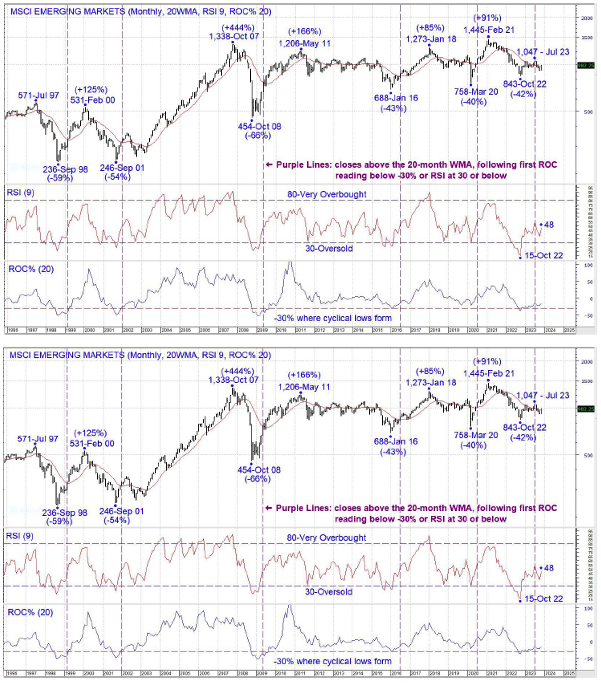

MSCI EM: Time to break free?

Writing about the MSCI EM Index in 2023 feels a bit like a DJ playing a new Earth, Wind and Fire single, but the collective EM is still a thing and looks like it may get more interesting in 2024. The monthly chart shows a peak in October 2007 of 1,338, that is no longer the all-time high but that level marks the beginning of a now 16-year ceiling for the index. On a positive note, the 2008 low of 454 has been followed by a series of rising cyclical lows in 2016, 2020 and 2022. The weekly chart shows an initial 26% rally from the important 2022 low, and the index has now been rangebound for 9 months, forming a potential rectangle. A breakout from the range would signal another cyclical advance, perhaps driven by some improvement in Chinese equities.

Edition: 174

- 24 November, 2023

Israel/Palestine: The wars around us

Hamas' attack on Israel raises a number of important questions for the rest of the world, the most of important of which being whether the conflict will spread. One likely long-term consequence is greater global fragmentation, a trend that has been under way for some time, which accelerated with the Russia-Ukraine war. Wolfgang Münchau makes the observation that many events of the 2020s are the results of unsustainable policies and decisions in the previous decade. This is not a time for analysis and answers but a time for questions. Two key questions that stand out are whether Hamas' incursion marks the beginning of a wider conflict in the Eurasian continent, and whether it will reduce western support for Ukraine as attention turns elsewhere. Attention in Washington will now almost surely shift to the Middle East.

Edition: 171

- 13 October, 2023

China: Trade, not own

The breakup of Alibaba Group marks the grasp of Xi Jinping’s common prosperity agenda. Investors can be rich, but not too rich. Companies can innovate but with Beijing first. The government is taking it too far, sapping the culture of innovation that was a driver of China’s technology rise since 2012. Its tech influence is now restricted within Asia. Its geopolitical realm is diminished greatly – the Belt and Road Initiative is now barely mentioned outside of debt renegotiations. To structurally invest in this market is to believe an intervention can support equity multiples. Paul Krake notes this can be true in some cases, such as climate infrastructure, but there is a big difference between government support and interference. Chinese equities remain a trade and nothing more.

Edition: 157

- 31 March, 2023

UK: Not the Northern Ireland Protocol

Helen Thomas discusses how PM Sunak has played a significant role in the recent Windsor Framework agreement between the UK and EU, seeking to neutralise the impact of the Northern Ireland Protocol. Sunak’s consensual approach, which matches the EU’s desire to de-escalate the irritation of Brexit, has led to a more cooperative relationship between the two sides. Sunak's main goal is to ensure that his party accepts him as their true leader, and the agreement reflects a shift away from the weaponisation of the Irish Border and a commitment to working together to help each other. Indeed, Helen claims, this marks the end of the beginning of the Brexit negotiations.

Edition: 155

- 03 March, 2023

Technology

Jeff Lawson (Co-Founder, Chairman & CEO) purchases 158k shares at $63.26, spending $10m - this marks a reversal from a series of sales, most recently at $264 (Jan 2022). His only previous buy was at $23.43 in May 2017. Donna Dubinsky (Non-Exec since 2018) purchased $251k on the same day. This is her first time buying shares in TWLO and a reversal from sells at higher prices. She didn't acquire any shares at either of her previous Non-Exec roles. These purchases follow recently posted year-end results along with a workforce reduction and $1bn buyback.

Edition: 155

- 03 March, 2023

Financials

2Q22 results mask $1bn in additional earnings power as fortress balance sheet is strengthened - JPM reported $2.76 EPS but core earnings power was closer to Charles Peabody’s $3.00 estimate after backing out marks and other adjustments. While the market was disappointed by the suspension of stock buybacks, Charles’ analysis suggests JPM can raise the dividend and resume buybacks very soon while still building CET1 to 13% levels by 1Q23. The stock is very attractive at current levels.

Edition: 140

- 22 July, 2022

Colombia: Petro elected as country’s first left-wing president

Petro’s victory marks a historic shift for Colombia. Whilst he has repeatedly insisted that he is not as radical as his critics make out, his pledges to redistribute wealth, end fossil fuel extraction and implement a wide-ranging land reform mark a significant departure from the incumbent president. Petro also faces the challenges of reassuring better-off Colombians that he is not seeking to expropriate their wealth. However, lacking a majority in congress may force him to tone down some of his more radical proposals once he takes office.

Edition: 138

- 24 June, 2022

China: A new and potentially dangerous phase of development

China is embarking on a new phase of development that emphasises stability over growth and signals the growing financialization of the economy. Evergrande marks the dawn of tighter Chinese policy control over credit, with big implications for the future hegemony of US finance. It may end up exposing cracks not only in China’s financial system but in Western finance too; Western policymakers should take heed not to dismiss the China threat!

Edition: 120

- 01 October, 2021

What China’s economic slowdown really means?

In sharp contrast to the 2007/08 GFC, China is lagging policy actions and has been deliberately inactive since the Lunar New Year. Michael Howell believes this marks a new phase in Chinese economic development, away from growth and towards stability, evidenced by the more stable Yuan exchange rate. This is bullish for Chinese financial assets long-term, but comes at an obvious cost to the rest of the world through slower growth.

Edition: 119

- 17 September, 2021

Risky Business: China’s Tech Crackdown & How to Navigate it

While the official ban on the most lucrative activities in the after-school tutoring sector marks a new low in the regulatory crackdown, RedTech maintain that China is not trying to strangle the golden goose. A handful of big losers will be offset by a majority of companies that are well positioned for growth in a tighter regulatory environment. The less risky (Tencent) are being dragged down with the more risky (Didi), creating lucrative, long-term investing opportunities. Other companies mentioned include Alibaba, Ant Group, ByteDance, Douyu, Huya, JD, Meituan, Pinduoduo, Sogou and TAL.

Edition: 116

- 06 August, 2021

NRDC positioning for China to import more coal

In preparation for robust consumption this summer, China’s National Development and Reform Commission has started directing customs authorities to release more import quotas to boost coal imports. Jeffrey Landsberg comments that this marks a stark reversal from Beijing’s earlier stance and is increasingly bullish for Chinese coal import prospects for the near term.

Edition: 109

- 30 April, 2021