Fortnightly Publication Highlighting Latest Insights From IRF Providers

Company Research

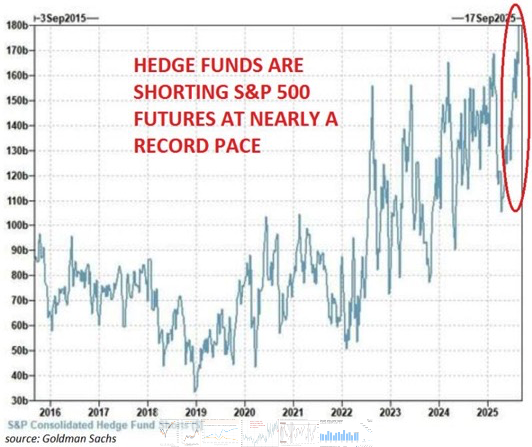

US: It’s not time to be bearish

Forget the argument that this is a new dot.com bubble, argues Gaius King. The top 10 countries in the S&P500 are the ones delivering real growth whilst the remaining 490 and the broader economy are remarkably weak. Ironically, fund managers shorting this market is actually a contrarian indicator. There is little or no seasonality this year, and recall that asset and fund managers remain seriously under invested since the Tariff Tantrum. Actively shorting this market (see chart) in such a low volatility environment is hopium that they will match the index if the market falls. Gaius expects an additional year of market craziness ahead of us, peaking in Q3/2026, and draws remarkable parallels to the 1970s. Investors should buy momentum stocks. If you want a market canary, look at AI’s forward order book.

Edition: 222

- 17 October, 2025

Communications

New CEO Spencer Rascoff is a high-capacity multi-tasker primed to rebuild consumer trust and female engagement. He served as CEO of Zillow from 2010-2020, scaling the business into the leading US online real estate platform. While not a product visionary himself, he is a detail oriented entrepreneurial risk taker who will inculcate a faster paced culture of innovation at MTCH. Rascoff has a knack for emphasising authentic user experience over monetisation (short-term) with an eye towards building a more trusted relationship with customers. Paragon’s analysis includes interviews with 7 former senior executives who worked with Rascoff for more than 85 years combined.

Edition: 210

- 02 May, 2025

Consumer Discretionary

Gordon Haskett Research Advisors

WING shares took a gut punch, falling over 20%, in response to greater-than-expected Q4 SSS moderation. Jeff Farmer thinks the sell-off is materially overdone, highlighting the restaurant company’s fundamental credentials heading into 2025E including 13%+ system unit growth; +MSD% SSS, almost entirely driven by traffic (following +20% SSS in 2024); ~70% cash-on-cash return; 20% EBITDA growth; and 75% FCF conversion. There is no other consumer discretionary company that can match this. Growth investors who have been wanting to add WING to their portfolios, should do so now. Jeff's TP of $370 equates to 38x his 2026E EBITDA estimate of $302m.

Edition: 198

- 01 November, 2024

BoJ and RBA rightly dovish, but still a bit optimistic

Manoj Pradhan comments that being dovish is exactly the right choice for the two central banks, but both were still a bit too optimistic on rising real wages being able to lift consumption. The BoJ has a longer wait before the output gap turns positive and it will need to tread carefully with any rate movements given the role of FX in the economy. The RBA will have to ease by much more than its rhetoric and market pricing suggest, with an outcome similar to the US but without a growth profile to match. Manoj is staying LONG MXNJPY (Banxico will stay hawkish on services inflation and strong growth). He also recommends to stay received Aus 1y1y or 2y1y. For the RBNZ, it is time to recreate a flattener (i.e., add a payer for 2024 to the existing 1y1y receiver).

Edition: 182

- 22 March, 2024

China: Monetary policy is back in fashion

China’s monetary officials aren’t content to sit on the sidelines as the economy limps along. That’s Trivium China’s reading of comments from Zou Lan, director of the central bank’s (PBoC) monetary policy department. In an interview with Xinhua, Zou said the PBoC: “Will strengthen counter-cyclical and cross-cyclical adjustments”. The PBoC will use all its monetary policy tools – including reserve requirements, relending quotas, the medium-term lending facility (MLF), and open market operations – to: “Provide strong support for social financing and the reasonable growth of money and credit”. Until recently the PBoC strove to ensure credit and money supply growth was broadly in line with nominal GDP growth, but it now aspires to match credit and money supply growth with the GDP and inflation targets. This should give credit and monetary growth room to run a little hotter than it has throughout 2023.

Edition: 177

- 12 January, 2024

US: The case for being short bonds (again)

On October 12th Manoj Pradhan took profits on his US positions after a great run, arguing there would be a time to short bonds again – he wasn’t expecting it to come so quickly! He argues there is too little priced into December and for hikes in general; if the Fed does not match the incremental amount of tightening required, then bonds will. He also remarks that the Bank of Canada model is working for the US, commenting on the four elements that forced the BoC to end its April pause and hike in June: labour markets, growth, interest-sensitive spending, and inflation. All of these are highly applicable to the US and point to higher rates – if the Fed doesn’t provide that premium, bond vigilantes will. The Fed is playing with fire and it’s getting burned.

Edition: 172

- 27 October, 2023

Technology

The developer of radio frequency identification chips used in RFID tags benefited when companies were facing supply chain issues which resulted in ordering much more inventory than necessary. Hamed Khorsand thinks it is unrealistic for revenue growth to match last year's strong performance especially since PI is heavily dependent on retail apparel and its largest customer is talking about a challenging environment. He argues the stock is priced for perfection - it currently trades at a price to sales multiple of 8.2 times and a forward PE of 44. Hamed’s TP is $45 (50% downside).

Edition: 164

- 07 July, 2023

Expect a sharp fall in demand for lumber & OSB in 2023

Demand for both lumber and OSB is expected to decline precipitously next year on weaker homebuilding activity. For lumber, overdue capacity closures in British Columbia (BC) should help offset supply growth from the US South, but BC producers can’t solely remove enough supply to match the expected collapse in demand. ERA Forest Products forecast lumber prices cycling either side of BC cash-cost levels, with S-P-F 2x4s averaging $450 on the year, and SYP 2x4s averaging $440. Risks are to the downside. In OSB, declining supply due to a combination of mill conversions, fire-related downtime and a pullback in offshore imports should keep some tension in the market through H1/2023.

Edition: 150

- 09 December, 2022

Swedish Match (SWMA SS) Sweden

Consumer Staples

Philip Morris International will accept all SWMA shares that have been tendered to it despite failing to achieve its 90% minimum stake threshold. PMI must still secure further shares in a voluntary transaction during a new offer period to achieve its goal of utilising compulsory purchases to acquire all remaining stakes in the Swedish company. After PMI raised its public offer in October, the total bid now amounts to SEK176bn ($15.8bn).

Edition: 148

- 11 November, 2022

China is the only 15%+ equity market in the world

Despite the cloudy outlook for zero-Covid China, Manoj Pradhan is optimistic on China on the basis of policy easing. We have the usual suspects that have been in action – rate cuts, infrastructure investment, special bond issuance – but Manoj is drawn by a range of policy measures designed specially to support housing. On the whole, the breadth of policy easing in China will deliver growth that no other economy can match for the next 6-9 months. Investors should stay in developer equities (as per Manoj’s Sept recommendations) and look to add the broader equity market.

Edition: 148

- 11 November, 2022

Communications

New CEO Bernard Kim will rejuvenate Tinder and refocus MTCH’s product roadmap - to reaccelerate growth, Kim will drive better-than-expected payer and revenue-per-payer growth by applying his mobile gaming expertise, introducing new product features, and more efficiently balancing investments in high ROI properties. A forward P/E of 19x, sets up a more compelling risk:reward today than at any point since the stock went public in 2015. Adjusted EPS to increase to $3.83-$4.11 in 2024, which is 14%-22% higher than consensus of $3.37.

Edition: 147

- 28 October, 2022

Canadian Banks: Credit risk playbook for a recession

Financials

The coming credit storm - Nigel D'Souza expects provisions for credit losses in the upcoming cycle to match or potentially exceed PCLs during the GFC. Highlights from Nigel’s report include: 1) Household debt service ratio to set a record high. 2) International exposure to skew PCLs higher during a recession. 3) Real estate secured lending portfolios unlikely to drive material credit losses. 4) Wholesale portfolio credit risk likely to be more idiosyncratic than systemic. 5) Of the Big Six banks, Bank of Montreal would experience the highest peak PCL ratio during a recession (1.20% or 6.0x BMO's pre-pandemic level); National Bank the lowest (0.29%).

Edition: 141

- 05 August, 2022

Indonesia: Lacklustre growth

Andrew Hunt doubts that Indonesia’s economy is growing as rapidly as the official data suggests. It possesses a high level of foreign debt which Andrew suspects it is finding difficult to rollover as the global supply of dollars dries up. With its legacy problems, expect to see further downward pressure on the foreign reserves and the IDR. Given the softness in the domestic economy, the central bank will likely match the Fed instead of enacting aggressive rate hikes, providing that the decline in the rupiah does not become disorderly.

Edition: 140

- 22 July, 2022

UK: A hike into a recession

Carl Weinberg is fully aware of the Bank of England’s price stability mandate, but their latest decision certainly isn’t a wise one. We are living in unusual times with an impaired supply curve heating up inflation, so why would the BoE seek to reduce the demand curve to match this? The MPC is ignoring the obvious problem: energy prices are rising faster than other prices! Carl says a negative or zero interest rate is needed, otherwise the BoE is marching us into recession at an even faster rate than is necessary.

Edition: 135

- 13 May, 2022

GEM Funds Investor Positioning Insights: India maximum divergence

Stephen Holden’s data highlights the growing divide between Value and Aggressive Growth managers in India - while Aggressive Growth investors double down, especially in Financials and Tech, Value managers are finding fewer opportunities to invest, and appear comfortable allowing their underweights to increase. That’s not to say there are no Value opportunities in India, just not enough to match either the benchmark weight, or the weight of their Growth peers. As the world focuses on a potential Growth to Value switch, in EM at least, India will be a key driver of relative performance between the two sets of investors.

Stocks highlighted include HDFC Bank, Housing Development Finance, Indian Oil Corp, Infosys and Tata Consultancy.

Edition: 134

- 29 April, 2022

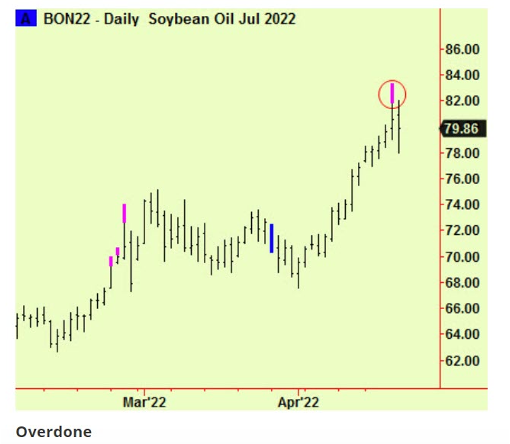

Soybean rally doesn’t match up with the facts

In the face of the huge, stranded harvest problem in Ukraine, soybean oil has been rising like all grain markets. Yet, Richard Edwards believes this move doesn’t reflect reality; Ukraine isn’t a large producer of soybeans. Instead, the rally is largely a result of substitution pricing (Ukraine is a big sunflower oil producer), a sympathy rally, and worries about a shift in planting intention away from soya in the US. None of this is directly attributable to any immediate shortage in soybeans or bean oil, sell SHORT.

Edition: 134

- 29 April, 2022

Big Tobacco’s RRPs showed positive performance in 2021 with promising signs for the future

Consumer Staples

Philip-Morris Int. reported a positive performance of Iqos Iluma in Japan and Switzerland, with significant growth in its heated tobacco portfolio, especially in the Middle East, Africa, South and Southeast Asia. Likewise, Japan Tobacco will prioritise its heated tobacco portfolio by 2027, while British American Tobacco’s revenue from its new products category rose by 42.4%, boosted by higher modern oral products sales. Swedish Match’s sales increased by 11%, driven by the smoke-free product segment, with solid growth in the US and Scandinavia for nicotine pouches and plans to invest further throughout 2022.

Edition: 130

- 04 March, 2022

Technology

Has an appealing proposition for consumers in the emerging BNPL industry, but sellers are not seeing much differentiation among the leading competitors, according to Blueshift’s interviews with merchants, payment industry specialists and payment technology developers. Sources also revealed how the industry is ripe for consolidation (Amazon to acquire AFRM?); how BNPL will continue to grow in the US but won’t match the adoption rate internationally; as well as voicing concerns around credit risk and increased regulation.

Edition: 130

- 04 March, 2022

How to pick a gold stock in 2022

Global Mining Research’s BUY and SELL signals served investors well in 2021 despite some market disconnect between equity price and numerous variables, including dividends. This year, David Radclyffe sees the gold sector shifting more to a growth/scale focus over returns/balance sheets; so, more M&A, growth investment, inflation impacting margins, lower dividends and a focus on ESG. David’s latest report looks for stocks that match the investment themes within the sector. Key picks include Agnico Eagle (new BUY signal), Barrick Gold, Northern Star Resources and Endeavour Mining.

Edition: 129

- 18 February, 2022

Swedish Match (SWMA SS) Sweden

Consumer Staples

A lollapalooza opportunity - where strong growth, pricing power, resilient market share and great allocation all come together. Post spin-off of the cigar business c.95% of EBIT will come from smoke free products, but it is the potential of the company’s ZYN pouch product in the US which Andrew Hollingworth is most excited about. His analysis looks to dispel investor concerns around rivals’ attempts to gain market share by undercutting ZYN's prices. Andrew has also built two models to look at what the future compounding of SWMA might look like - results in 12% and 19% annual returns over the next 7 years.

Edition: 128

- 04 February, 2022

Silver’s shortage: Is it all lies?

In his latest video, Jeffrey Christian discusses the seemingly false narrative around the silver shortage which doesn’t match up with reality. Consequently, the semiconductor shortage isn’t a result of such “shortages” but rather a combination of factors, including demand for specialised chips and an increasingly concentrated industry. Jeffrey also explores the implications for investors and the economic outlook. Click here

Edition: 123

- 12 November, 2021