Fortnightly Publication Highlighting Latest Insights From IRF Providers

Company Research

EM Alpha

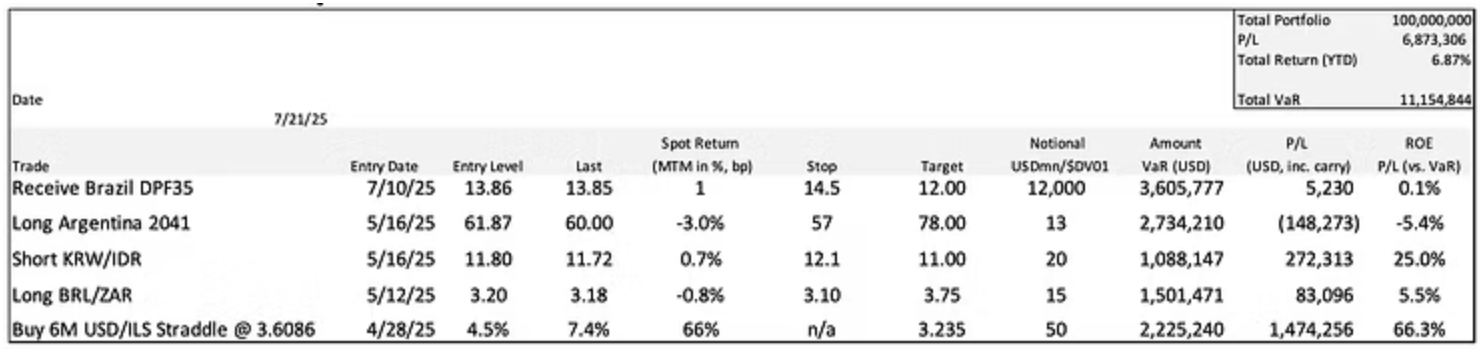

David Woo’s EM Fixed Income Alpha Portfolio is up 6.87% in 2025, 117bp in carry. He has added to the Brazilian rates position at 14% and is looking add more between 14% and 14.25%; he will stop at 14.5%. For long BRL/ZAR his position is up despite a 0.8% drop in spot due to the positive carry, and he is planning to add to this exposure around 3.15. David discusses the counterintuitively optimistic news flowing from South Africa, which he expects to deteriorate in the coming weeks despite the decision to dismiss Minister Nobuhle Nkabane. David also notes the lower-than-expected inflation data from Argentina, which he takes advantage of by adding to his exposure in the 2041 bond, just ahead of the Moody’s upgrade announcement.

Edition: 216

- 25 July, 2025

Japan’s financial sector is nearing a critical turning point

Financials

While BOJ policy normalisation has boosted bank earnings expectations, it has also destabilised the JGB market and raised fears of a sovereign credit downgrade (risks reminiscent of the recent US downgrade by Moody’s). Japanese financials have absorbed nearly 50% of ETF inflows over the past year, but recent outflows suggest sentiment is shifting. Unrealised bond losses and rising fiscal concerns are mounting and the “Japan Premium” for USD funding could return. Neil Newman sees the sector as home to some of the market’s most crowded trades. He highlights Nomura as a short and flags Japan’s three megabanks (MUFG, SMFG, Mizuho Financial Group) as increasingly exposed to reversal risks.

Edition: 213

- 13 June, 2025

TRUMPoline projector

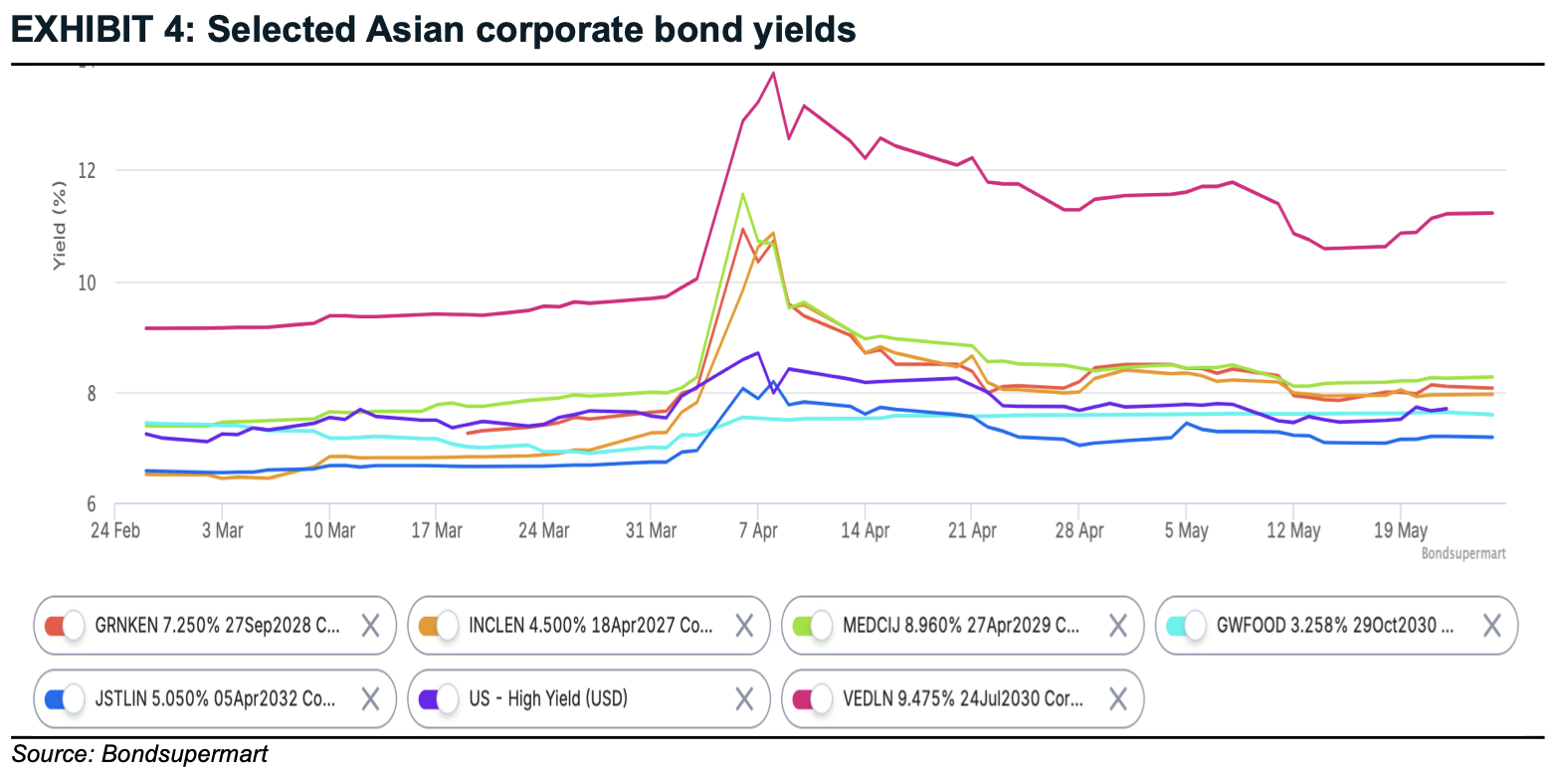

Warut Promboon follows up on his latest report, discussing where the US is towards the unintended recession and where in EM the Trump tariffs will impact the most. In his last report, he reiterated his recommendation to stay on short-dated bonds in addition to precious metals. Since, Moody’s, Fitch and S&P all downgraded the US, which Warut views as spread neutral, since he believes Moody’s simply took the opportunity on the tariff news to move their rating in line with other agencies. Warut sees the US in a stagflation period. Though rising rates are not friendly to fixed rate bonds, he believes Asian high-yield bonds remain a good place to park capital in the near term on their resilience and attractiveness compared to the US high-yield counterpart (see chart). Prefer short duration under 5 years to keep duration low in preparation for an upward pressure on rates in the near term.

Edition: 212

- 30 May, 2025

Financials

Craig Huber sees debt issuance continuing to increase meaningfully over the next several years (on top of record levels in 2024) and MCO should benefit materially including further upside to margins. Short and long term, he likes the stock and fundamentals a lot. His 2025 adjusted EPS estimate is $14.55 (Street high) and $16.50 for 2026. Near-term, his 1Q25 adjusted EPS estimate is $3.65 and for revenue to be up 7.6% Y/Y. Craig maintains his long-held Overweight rating and raises his 12-month TP to $554 based on averaging 23.5x 2026E EBITDA (or 32.0x adjusted EPS) and his 10-year DCF analysis (8.5% WACC, 4.8% long-term FCF growth rate and 27.6x terminal FCF multiple).

Edition: 207

- 21 March, 2025

Tajikistan: The awakening of a forgotten country

After decades of being of little interest to all but adventurous geologists, Tajikistan is now a country of great interest because of an abundance of critical minerals (CRAM) and its potential to be a major supplier of electricity to Central Asia. In his latest 50-page report, Christopher Weafer dives deep into the country. There are some concerns, including security and domestic stability. Yet, positive signs are emerging, with both Moody’s and S&P upgrading their risk assessment based on the more promising growth and investment prospects as well as low debt. Additional opportunities are beginning to appear in consumer sector investors, for healthcare, transport and logistics, and elements of a digital economy—all of which are poorly developed today.

Edition: 199

- 15 November, 2024

Financials

It was a great quarter with MCO beating expectations and raising its FY24 adjusted EPS, but management’s guide still appears conservative vs. Craig Huber's Street-high estimate of $11.60. Heading into the print, he had already increased his 2Q24 and 2024 EPS estimates given ongoing better than expected debt issuance trends in US and Europe. For 2025 and 2026 he estimates EPS of $13.80 and $15.70, respectively. Craig retains his long-held Overweight rating on MCO which is in a long-term secular uptrend in Ratings and Moody’s Analytics. His revised 12-month TP is $500.

Edition: 191

- 26 July, 2024

Colombia and Peru: Credit deterioration

The fiscal stances and institutional qualities have been deteriorating in Colombia and Peru, and Marcos Buscaglia analyses whether this could impact their credit ratings. Running several models, he sees convergence to BB from BB+ for Colombia and expects more downgrades from Moody's. Peru’s S&P rating will remain stable, but Moody’s and Fitch will oversee downgrades, leaving the country on the brink of becoming a fallen angel. On the economic front, Marcos expects Colombia’s GDP growth to outperform consensus at 2% and expects BanRep to deliver another 50bp cut in June. Peru will see similar growth rates, and Marcos forecasts that the BCRP will continue with the easing cycle, with more 25bp reductions and a terminal rate of 4.5%.

Edition: 186

- 17 May, 2024

Emaar Properties (EMAAR UH) United Arab Emirates

Real Estate

EMAAR surfs a 10-year high - Real Estate is seen as a refuge for investors through oil and commodity price volatility. Recent results saw the company's Real Estate revenues fall 18.5%, but this was partly offset by a revival of the other segments with Leasing and retail revenue increasing by 10.6% and Hospitality revenue up 9.7%. Growth was driven by the steady recovery in the tourism industry and strong domestic spending. Margins are also doing well thanks to better operating and financial cost management, while the balance sheet is strong. Finally, AlphaMena flags the recent Credit Ratings upgrade by S&P, Moody’s and Fitch as further proof that the hard times are behind EMAAR.

Edition: 171

- 13 October, 2023

Technology

Post 2Q results, Craig Huber increases his 12-month TP to $389 based on averaging 20.5x 2025E EBITDA (or 26.0x adjusted EPS) and his 10-year DCF analysis (9.0% WACC, 4.5% long-term FCF growth rate and 22.3x terminal FCF multiple). He thinks debt issuance trends are going to improve significantly over the next 2-3 years and MCO should benefit materially and at a time when it is currently tightening its costs to become even more efficient. Street adjusted EPS estimates for 2024-25 look significantly too low; Craig's 2023-25 estimates are $10.25/$12.40/$15.10 vs. consensus forecasts of $10.07/$11.47/$13.20.

Edition: 166

- 04 August, 2023

Technology

Craig Huber thinks the firm's Ratings revenue guidance is far too conservative - for the five years though 2027, Craig’s average Ratings revenue growth estimate is +9.5% vs. management's new guidance of only +2-5%. At this stage the trough for global debt issuance appears to have been 4Q22, 1Q/2Q23 should look sequentially better (but still down y/y), and 2H23 should be up significantly once the Fed is likely done raising interest rates. Craig increases his 12-month TP to $360, based on averaging 21.0x 2024E EBITDA (or 27.2x adjusted EPS) and his 10-year DCF analysis (9.0% WACC, 4.5% long-term FCF growth rate, and 22.1x terminal FCF multiple).

Edition: 154

- 17 February, 2023