Fortnightly Publication Highlighting Latest Insights From IRF Providers

Company Research

US equities: The case for value

Tian Yang is changing his long-held bias against value stocks and recommending a shift to overweight value vs growth. He points out that he is finally seeing alignment across A) market behaviour, B) the macro-outlook, and C) bottom-up fundamentals. On his indicators, today's set up is as good as it has been since the GFC for value to outperform. US earnings estimate revisions have broadened since Liberation Day, which has historically been indicative of value vs growth outperformance over the next 12 months (first chart below). At the same time, he notes a sharp fall in the correlation of the Russell 1000 market cap weighted index vs the equal weighted index. As the second chart shows, this correlation collapse has often marked a low in the value-to-growth ratio historically. Tian is also seeing evidence of a rotation into value stocks over the past couple of months.

Edition: 223

- 31 October, 2025

Ready for the contrarian gold trade?

Cam Hui has been bullish on gold, but point-and-figure charts of gold and gold miners now show that they are either very near or have outrun their measured price objectives. Tactically, the contrarian trade would be to sell gold and buy bonds. However, a cycle analysis leads Cam to conclude that the market is undergoing a shift to a hard asset price leadership cycle. Cam’s base case calls for a multi-month correction and consolidation in the manner of the 2004–2006 experience, followed by a second rally to an ultimate top at much higher gold prices. It is within this context that a long-term point and figure objective of 9,800 is achievable in the next 3–5 years.

Edition: 223

- 31 October, 2025

Consumer Discretionary

PLNT is well positioned in the growing high‑value‑low‑price gym segment with scale and ample runway for growth. New CEO Colleen Keating brings relevant hospitality franchise experience to drive the next phase of growth in the US and internationally. Gen Z is the fastest‑growing membership cohort for the company, supported by initiatives like the “High School Summer Pass”. PLNT continues to refine club formats and contractual terms to improve efficiency and unit economics. 2Xideas expects 2024-31E system‑wide sales CAGR of 11.7%, driven by 6.6% annual net unit growth and 5.0% same‑club sales growth. They forecast an 11.1% EBITDA CAGR and a 44.6% margin in 2031E. European expansion remains an upside not reflected in their forecasts. They see 17.2% annualised total returns based on an exit NTM P/E of 28.0x (17.7x EV/EBITDA).

Edition: 223

- 31 October, 2025

Healthcare

Leveraging purchase order data from 450 US facilities, MedMine is closely tracking the rollout of Pulse Field Ablation (PFA), the key driver of BSX’s Electrophysiology growth. The US ablation catheter market for AFib is estimated to be growing about 12% Y/Y. BSX has been growing faster in part due to mix shifting from lower-priced Cryo and RF products to its premium FARAPULSE PFA system. However, BSX is facing increasing competition with its PFA market share now at 80%, 10 percentage points lower than its peak. This raises a key question: will BSX’s next growth phase come from converting the larger RF market or expanding the total patient base estimated at 60m globally? MedMine’s near real-time data helps investors track these shifts in market share, pricing and technology adoption as they unfold.

Edition: 223

- 31 October, 2025

Financials

Abacus sees FIGR as a highly disruptive leader in real-world asset tokenisation - a theme they expect to define the next decade. The company has found a real-world use for blockchain, proving it can reduce the cost and time in HELOC origination by 90% (current 3% market share), with an average production cost per loan of just $730 vs. an industry average of $11,000. Beyond its low-cost origination engine, FIGR operates a marketplace for pooled credit, creating liquidity and transparency in traditionally illiquid markets. Abacus expects this model to scale into other asset classes, underpinned by ~30% operating margins and 80%+ incremental margins, with potential upside of 150% to $115.

Edition: 223

- 31 October, 2025

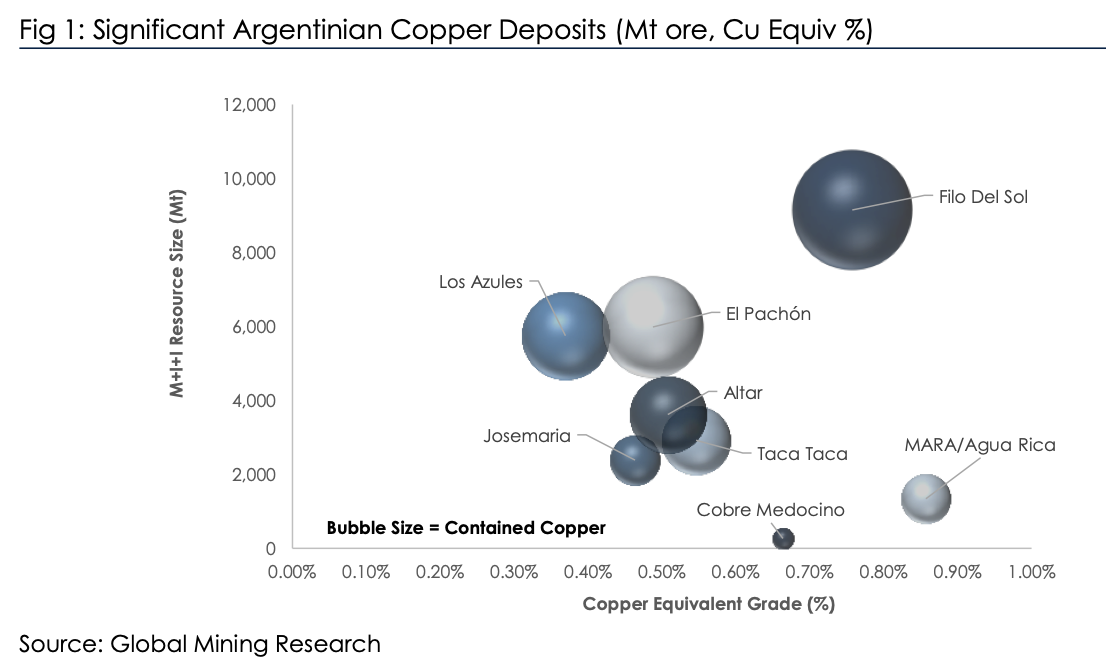

Is Argentina the next big thing?

Argentina has significant copper reserves yet produces no material copper (see chart). The new investment climate (RIGI) in Argentina, spearheaded by libertarian President Milei, is hoping to reverse this. Other volatile countries including DRC have achieved significant growth, so it’s possible. In his latest report, David Radclyffe examines the potential of Argentina copper. He sees potential for the nation to become a 1.0–1.5 Mt per year copper producer (top 10 globally), but comments on the aspirational timelines, with first copper unlikely on this side of 2029. Issues also cannot be discounted, with ESG concerns bubbling alongside a lack of infrastructure and skilled workers. David estimates the total capex at USD $40–50 billion. Lundin Mining has the most leveraged exposure to Argentina in partnership with BHP and is the preferred exposure. There are a few exploration plays, of which NGEx Minerals (non-rated) and its Lunahuasi discovery is the largest.

Edition: 222

- 17 October, 2025

A compelling growth story

AIR highlights Spain as the Eurozone’s standout growth opportunity, further supported by US immigration tightening redirecting talent and labour. The country is benefitting from its strong position in the EU’s €750bn Next Generation EU program, minimal exposure to US tariffs and insulation from Chinese industrial competition. A rapid transition to renewables has driven a 40% decline in wholesale electricity prices over five years, while lower structural taxes and spending continue to support competitiveness. Preferred sector calls include Infrastructure (Acciona, Ferrovial, Sacyr) with robust project pipelines supported by public and private investment; Banking & Insurance (CaixaBank) benefitting from SME exposure and high household savings rates; Real Estate (Merlin, Metrovacesa) poised for catch-up gains vs. other European countries amid supply constraints; and Defence, where Indra Sistemas is well positioned for M&A.

Edition: 222

- 17 October, 2025

China: Xi-Trump summit still possible despite tariff threats

William Hess comments that the tumultuous week for US-China highlights the latter’s position: China is happy to drag out negotiations for as long as possible. The backdrop to successive negotiations is a situation of fundamental distrust and geopolitical realignment that Beijing is in no hurry to slow down. These developments set the stage for markets to blow off some steam after recent rallies appear overextended. In terms of activity levels, William’s proprietary indicator for China is showing activity that is moderating but in line with cyclical expectations and far from collapsing. This is consistent with his expectations for Q3 GDP growth that is a tick above the consensus of 4.7%. More important for market expectations will be the Fourth Plenum next week, which should be Beijing’s attempt to improve the macro narrative with structural reform plans.

Edition: 222

- 17 October, 2025

Chile: Policy rate should stabilise at ~4.5%

Igal Magendzo points out that the market — which in recent weeks had been converging toward a scenario with a policy rate somewhat higher than the Central Bank’s baseline projection — has slightly adjusted the timing of the final cuts expected in this cycle. Specifically, the highest probability of a rate cut shifted from next January to this December, in line with the medians of both the Economic Expectations Survey and the Financial Operators Survey, and consistent with Igal’s baseline scenario. Regarding the final cut, although the probability of a 25-basis-point move remains only around 50%, the market brought its expectation forward from October to June (compared with last week). Igal continues to maintain his view that the policy rate is close to neutral and should stabilise around 4.5%.

Edition: 222

- 17 October, 2025

Siemens Energy (ENR GR) Germany

Industrials

A “backdoor” AI infrastructure play amid growing power bottlenecks from new data centre construction. As data centres cannot rely on intermittent renewables, natural gas turbines are seen as the only viable near-term solution. The market is extremely tight, with projected demand of 80-100GW vs. supply of only ~70GW and consensus likely underestimating both pricing and volume potential. ENR’s Gas business is positioned to deliver 20%+ long-term margins, while its Grid Technologies division should benefit from global electrification and grid modernisation, with revenue expected to exceed €20bn by 2030. Shares could double over the next 3 years, driven by earnings beats and a profit inflection in the Wind segment. The upcoming November Analyst Day is viewed as a major catalyst.

Edition: 222

- 17 October, 2025

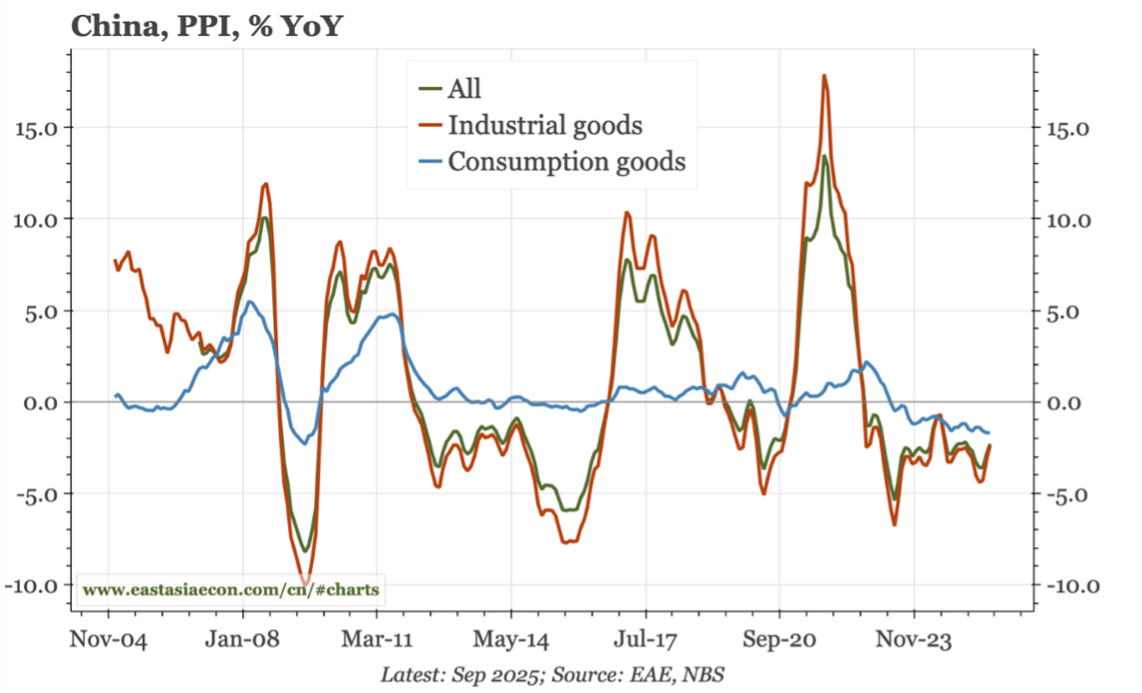

China: A fragile improvement in PPI

For the first time in more than a year, in level terms, the producer price index (PPI) has stopped falling; however, in year-on-year terms it was down 2.3%y-o-y (versus -2.9% y-o-y in August). That is an improvement, but one that looks fragile. Prices in auto manufacturing – one of the sectors targeted by the anti-involution drive – are falling more quickly than ever, and the "consumption" sector of the PPI in general shows no turnaround. Building material prices continue to be dragged down by the problems in the property market. The stabilisation in PPI is being driven by prices for "industrial" products, namely mining and energy. The short-term leads don't suggest much change in PPI in the next couple of months. But there is some upside risk coming from the YoY rise in global commodity prices (in CNY terms). Paul Cavey remarks that this would be more powerful for China if the construction cycle really finds a floor, allowing building materials prices to do the same.

Edition: 222

- 17 October, 2025

Germany: Angela Merz

Four months in and Chancellor Merz’s government has a mixed record, and Niall Ferguson says that doubts over the coalition lasting until 2029 are justified. However, media forecasts for a near term breakdown are unlikely to be founded, and Niall expects the coalition to survive beyond November of next year. Even if the AfD secures victories in state-level elections, Merz and Vice-Chancellor Klingbeil will be able to use the argument that time must be given for economic recovery before the electorate rushes to the polls for another party. Russia’s antics in testing NATO should bolster the coalition’s cohesion. Niall is positive on German equities and continues to be constructive on German growth, which will in turn boost Europe as a whole.

Edition: 221

- 03 October, 2025

Japan: Give me capex

The quality of Japan’s growth is outstanding, Manoj Pradhan comments on how capex is the dominant trend alongside base pay growth. Additionally, the composition of inflation is not convincing, with goods and rice prices forming the biggest component. Thankfully, the combination of labour shortages and services producer price inflation suggests that capex may be playing a critical role. Pulled together, these point to productivity creating the virtuous cycle of income-spending, a more sustainable likelihood of the wage-services price drift that the BoJ desires, and an economy that can handle any rate rises as the underlying rate of return in the economy is rising. The productivity dynamic points to equity upside not just today but for the next 2-3 years. Balassa-Samuelson should mean medium-term Yen upside, with Manoj claiming EUR/JPY as the better choice for Yen bulls whilst USD improves.

Edition: 221

- 03 October, 2025

Further misery for beleaguered Canadian lumber producers

Materials

ERA continues to urge caution on all lumber-leveraged names and sees risk as downside-weighted in the near-term from sluggish demand. While the timber REITs are better positioned over the long-term, weak wood products markets will be a headwind for them too. Q3 earnings will be terrible and with an incremental 10% tariff being introduced shortly, prospects for Q4 remain extremely bleak. Lumber names are generally beaten up and there will be plenty of upside runway for survivors when markets eventually begin their next upcycle. However, ERA recommends waiting a quarter or two before building long positions.

Edition: 221

- 03 October, 2025

Healthcare

GH has two new liquid biopsy products that are ramping quickly and are well positioned. There is a massive TAM to go after: $100bn vs. current industry revenues of ~$3-5bn. Abacus believes Shield, one of the new products, could transform GH, with revenues growing from $60m this year to $700m in 2028, with further upside if Shield evolves into a multi-cancer screening platform. GH’s first-mover advantage is significant, provided the company demonstrates strong commercial execution. Abacus does not anticipate the need for additional capital, though a modest equity raise in 2026/27 to support growth would not be surprising. They target ~150% upside over the next 3-4 years.

Edition: 221

- 03 October, 2025

Bios scores big on 89bio, rotates to new opportunities

Healthcare

Bios Research’s long call on 89bio has paid off handsomely: since turning bullish in Apr 25, the shares have climbed ~120%, culminating in Roche’s announced takeover at $14.50/share plus a $6 CVR. With conviction now removed, Bios suggests rotating into SMID-cap biotech to capture what they see as the early stages of a new bull cycle. On the short side, the team has just launched a new idea with 30-50% expected downside over the next 6 months. Their track record is strong: 15 of 22 shorts over the past 18 months have generated absolute returns (~72% alpha-adjusted hit rate), with notable successful conviction removals including Apellis, Butterfly Network, Geron and Inspire Medical.

Edition: 221

- 03 October, 2025

The ailing world

The global economy is weakening and looks recession-bound, claims Andrew Hunt, who expects markets to be surprised by the extent of the economic weakness over the coming weeks. The bond sell off may have run its course for now. US equities are in a bubble that has been fuelled by continued aggressive debt monetisation in the G7 and China. Many are worried that the bubble could end as global economic growth slows, but Andrew suspects that the World has already entered an easing cycle – particularly in quantity terms which he regards as very much more important than simple rates. Andrew expects that easier monetary conditions will sustain markets in Q4. Next year, Andrew expects to see the inflationary consequences of the current easing cycle and for that reason he expects that higher inflation and the prospect of higher rates will then represent a clear threat to the system’s ability to sustain the bubble next year.

Edition: 220

- 19 September, 2025

France: Rising debt, rising instability

According to Brunello Rosa, the resignation of PM Bayrou after a no-confidence vote makes the approval of restrictive fiscal measures even less likely. Once again President Macron chose a loyalist, Sébastien Lecornu, as the replacement. But the likelihood of forming a coalition that could vote through the next budget is very slim, and so Macron may be forced to dissolve parliament. However, the result of new elections may be as inconclusive as the previous two, with three blocks of similar size unwilling to compromise and coalesce amongst themselves. France needs a serious and prolonged period of fiscal consolidation and reform, but this will make Macron even more unpopular, in turn favouring the rise of extreme parties on the far right and the left. If Macron dissolves parliament, he may end up in a cohabitation with an extreme party, which may pave the way for the RN’s victory in the next election.

Edition: 220

- 19 September, 2025

Europe: The Art of War

It’s been a rough summer for Europeans. The EU-US trade deal is highly unpopular, yet European leaders had little choice if they wanted to keep President Trump on their side in Ukraine. Niall Ferguson expects the European Parliament to ratify the deal. At the same time, EC President von der Leyen is looking to diversify trade deals, and Niall expects one with Mercosur countries to be ratified by year’s end. The EC will also walk back commitments under the Green Deal, including softening emissions targets for the auto industry, which will provide businesses with much needed breathing room. Niall expects frozen Russian assets and higher bilateral support from member states to support Ukraine, with defence-only EU bonds materialising next year. He remains bullish on European defence and dual-use tech.

Edition: 220

- 19 September, 2025

South Africa: Duller and calmer, with eyes on the prize

Krutham (formerly known as Intellidex)

The SARB kept rates unchanged in a 4-2 vote – which Peter Montalto expected would be a close call – but it remains a bit of a surprise given that this week’s CPI and expectations data could have opened a sliver of space. The QPM model moved up the repo path by removing one cut at the end of this year and the coming two, while the inflation track was marked up. Growth for 2025 was revised up to 1.2%, now in line with Peter’s view. Overall, the statement largely sidestepped this week’s CPI and gave inflation expectations only a passing nod; a signal possibly that the MPC wants a broader medium-run, firmer, re-anchoring before moving again. Peter’s baseline is an extended hold of ~10 months, with the next leg down only after a formal target change by Budget 2026, trending towards 5.50% terminal rates into 2028. There is a small risk of one more cut in November, but the bar is high.

Edition: 220

- 19 September, 2025

TKH Group (TWEKA NA) Netherlands

Technology

At its upcoming CMD, TKH is expected to set new mid-term targets to 2029: turnover >€2bn, EBITA margin >18%, ROCE 22-25% and net debt to EBITDA / leverage ratio <2x. While broadly consistent with prior goals, the updated plan is likely to emphasise organic growth. Crucially, with its investment cycle complete and working capital set to normalise, TKH is forecast to generate €600-650m in FCF in the next couple of years. This underpins scope for materially larger share buybacks - potentially €300m, or ~20% of current m/cap - alongside dividends and bolt-on M&A. the IDEA!’s DCF points to fair value of €51.30/share, implying ~50% upside.

Edition: 220

- 19 September, 2025

China: A new drive

William Hess notes that this past week saw the proliferation of annual industry “stable growth plans”. These are consistent with the objectives outlined recently which themselves are consistent with expected top-down emphasis on optimising the economic layout and capacity in the next batch of five-year plans. According to comments from MIIT, the weight of stable growth plans will focus on ten industries: the steel, non-ferrous, petrochemical, chemical, building materials, machinery, automobiles, power equipment, light industry, and electronic information manufacturing industries. These are cited as key forces to stabilize the industrial and national economy. As is the case for the steel sector, William sees the latest annual stable work plans as outlines for pending five-year plans to be released in 2026, focusing on improving high-quality supply capacity, optimizing the industry’s development environment, and promoting the effective improvement of quality and reasonable growth of the industry. It’s all part of Xi’s quality productivity drive.

Edition: 220

- 19 September, 2025

Technology

TWLO is positioned as a leader in the expanding CXaaS market, fuelled by its unique integration of communications, data and AI capabilities, which no competitor matches. The company’s disciplined shift to a unified platform is unlocking deep cross-sell opportunities among its vast customer base (63% of 349k+ customers still use only one product) and driving margin expansion, while accelerating revenue growth and robust FCF ($3bn+ cumulative by 2027) support an explicit capital return strategy (50% payout target via buybacks). Anchored by strong partnerships in the AI ecosystem and a proven go-to-market overhaul, TWLO’s compelling risk/reward profile is underpinned by durable profitability targets and margin stability, making it highly attractive for those seeking exposure to next-generation customer engagement infrastructure. TP $140 (35% upside).

Edition: 220

- 19 September, 2025

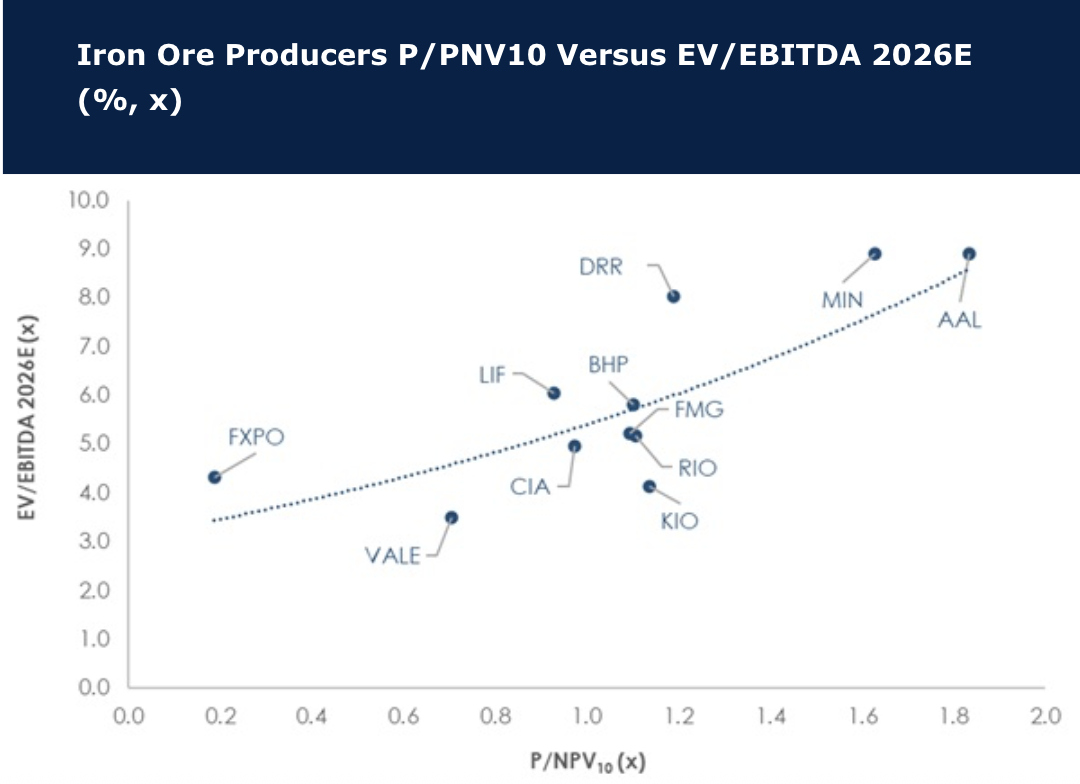

Iron ore is too big to ignore, but headwinds prevail

Iron ore seaborne supply is increasing at a time when steel demand is ailing, and David Radclyffe points out that this rightly makes investors nervous. However, the spot iron ore price has proven to be quite resilient this year at ~US$100/t. The headwinds may have dissuaded some investors, but at $378bn the iron ore market is simply too big to ignore in mining. As demand rolls the cost curve is key to sustaining volumes, and David assesses the LT price at US$95/t (US$101/t). Iron ore pure plays and diversified miners trade at 1.1x P/NPV10, and a prospective next two years average EV/EBITDA of ~5.8x and dividend yield of ~4.4%. Relative to other sectors this is reasonable, but high compared to historic levels. In the diversified iron ore-rich miners David prefers buy-rated BHP, then Vale, while in the pure plays it is Labrador Iron Ore Royalty. Overall, he remains underweight iron ore, with sells on key pure plays. Herein, Champion Iron is upgraded from sell to hold.

Edition: 219

- 05 September, 2025

How do you Identify Compounders?

In a market where investors increasingly seek long-term “compounders” to ride out volatility, Trivariate’s research shows that out of the four factors tested (revenue, gross margin, net margin, and price momentum), consistent gross margin expansion has been the most reliable signal of future stock outperformance. This is a rare but powerful cohort with only 39 companies having expanded gross margins for 12 consecutive quarters; 22 are expected to continue doing so next quarter. Actionable names include AMZN, T, ETN, APH, and TDG, among others.

Edition: 219

- 05 September, 2025

France: Instability ahead

The country is entering another period of political turbulence over next year’s budget. Niall Ferguson sees Beyrou’s days as prime minister as numbered, expecting him to lose the confidence vote on September 8th. This will put President Macron back into the driver’s seat, and Niall expects him to nominate another minority government that can secure a 2026 budget with PS cooperation. Yet such a budget would reduce the deficit only marginally. The other scenario is parliamentary snap elections in autumn, which would raise the risk of a victory for RN. In any case, Niall expects the risk premium on French sovereign bonds to rise in the coming weeks, with Frech political instability a major European theme for 2H/2025.

Edition: 219

- 05 September, 2025

ECB: Expect the circumspect

In line with Dimitris Valatsas’s expectations, the European consumer is showing signs of life: June retail sales came in at 3.1% y-o-y. But across the EU, growth remains slow and non-mortgage lending subdued. Demand for mortgages and consumer credit fell in Q2 and credit to EA companies stays very low. Spain remains Europe’s economic steamroller—2Q25 consumption grew by 3.5% y-o-y, while GFCF grew by 5.6% y-o-y. Dimitris views the trade truce with the US as a derisking factor—though he expects some of the deflationary effects of the global trade war to remain. Dimitris says the ECB has settled here; policymakers are too scared to get ahead of the economy, so he now expects them to hold for at least the next two meetings. 2Q26 forward rate expectations still seem too hawkish. The French and Spanish governments are increasingly fragile, though only the French situation presents a major threat to policy continuity.

Edition: 218

- 22 August, 2025

Technology

According to Systems Integrators who work with SNOW, they saw strong 2Q25 momentum driven by rapid partner expansion and AI innovation. The company now has over 10,000 partners worldwide reflecting heavy investment in programs that broaden global reach. New AI-driven tools, including Cortex AI, Iceberg tables, and adaptive compute capabilities, enable enterprises to interact with data in natural language and automate pipelines, and are driving revenue. Strategic acquisitions, such as Crunchy Data, further enhance Postgres capabilities and enterprise appeal. To sustain momentum, SNOW is leaning heavily on system integrators, hyperscalers and resellers to drive adoption of next-gen AI offerings.

Edition: 218

- 22 August, 2025

Financials

The Genius Act has changed America’s relationship with crypto, making it the most attractive country in the world for stablecoins. Abacus’ latest report notes that while the pace of adoption is still unclear, long-term disruption of financial incumbents appears inevitable. CRCL’s model is attractive if USDC can scale, though Abacus estimates ~10x growth is needed to deliver a reasonable IRR - a challenging hurdle. Blockchains are expected to replace legacy infrastructure, with SWIFT the first casualty. Visa and Mastercard face limited near-term risk, but crypto is the primary long-term threat to their duopoly. Stablecoins have the potential to reach >$2trn m/cap in the next few years vs. $260bn today. Abacus sees CRCL as a compelling risk/reward play, with upside potential of 195% outweighing downside risk of 50%.

Edition: 218

- 22 August, 2025

Japan’s space capabilities are rapidly expanding

Investor enthusiasm in the country’s space sector is accelerating, underpinned by several IPOs expected in the next couple of years. At SPEXA 2025, this enthusiasm was on full display, led by Toyota’s backing of Interstellar Technologies, which plans a listing and aims to capture the growing low-Earth-orbit launch market. Japan is also positioning itself at the forefront of space-debris removal working with Astroscale and JSAT, targeting an international regulatory framework by 2026. Meanwhile, government ambitions include doubling the space industry to ¥8trn, achieving 30 annual rocket launches by the early 2030s and deepening NASA collaboration, including a Toyota-built lunar rover. Neil Newman sees Japan’s space industry as an increasingly attractive investment theme.

Edition: 218

- 22 August, 2025

Markets at a crossroad as dollar recovery stalls

As highlighted in previous reports, Taha Bin Sohail notes that the US dollar was poised for a short-term recovery after overshooting to levels near its post-COVID lows. The 96.0 DXY level has consistently acted as a critical technical support, and recent market action confirmed its importance. Below this zone, the dollar risks sharp declines, while the 100.0 level remains the key upside resistance. In line with Taha’s projections, the DXY tested the upper bound but quickly retraced following the weaker-than-expected non-farm payrolls (NFP), signalling that labour market concerns are now front and centre for investors. Technically and fundamentally, the DXY is trapped between 96.0 and 100.0. ABCG Research currently maintains a wait-and-see approach, with the next decisive move likely to depend on trade deal outcomes. A breakout in either direction will set the tone for the dollar’s trajectory into the next quarter.

Edition: 217

- 08 August, 2025

Consumer Staples

Scott Mushkin downgrades DG to Sell, citing widening price gaps with competitors, which threaten margins and volume share gains over the next 12-18 months. R5’s latest fieldwork shows a total basket premium of 9% vs. Walmart - well above the typical 3-7% range. Scott now sees pressure from WMT starting to impact the back half of 2025; while Amazon’s push to speed up delivery times in rural areas, coupled with its low pricing for everyday essentials also appears be gaining momentum. At the same time, Dollar Tree is making inroads into DG’s core markets. Finally, regulatory risks from SNAP eligibility changes and the MAHA movement targeting sugary foods are expected to negatively impact sales.

Edition: 217

- 08 August, 2025

Quantum computing primer unveils two new Buy ideas

Technology

Rosenblatt initiates coverage on D-Wave (Buy, $30 TP) and IonQ (Buy, $70 TP), identifying them as differentiated, high-conviction ideas in the rapidly expanding quantum computing market. QBTS offers unique exposure to quantum annealing - particularly suited for optimisation workloads - and is expected to grow revenues at a +66% CAGR from 2025-2030. IONQ, a leader in trapped-ion architectures, is positioned to exceed $1bn in revenue within the next few years, with significant upside from its product roadmap and ecosystem development. These initiations are framed by Rosenblatt’s comprehensive quantum computing primer, which outlines the core principles, architectures and commercialisation pathways shaping the industry’s next era and underpins the firm’s bullish stance on both names.

Edition: 217

- 08 August, 2025

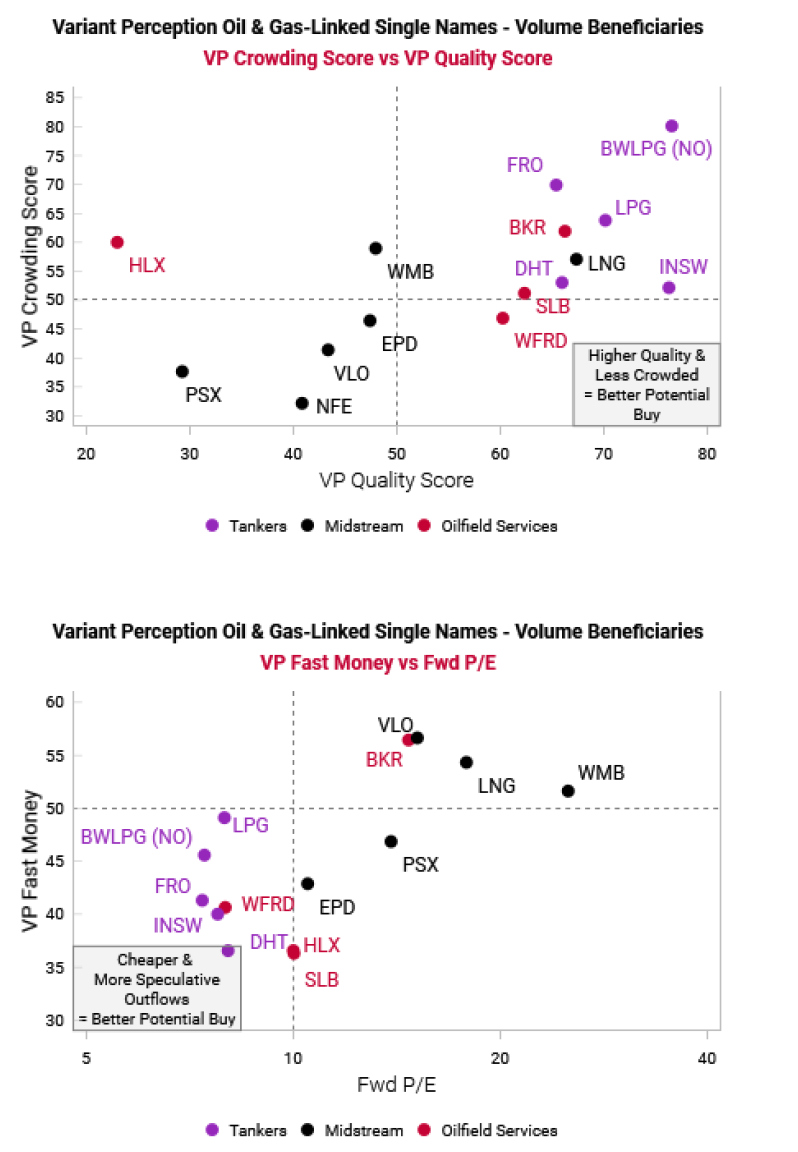

Pockets of value emerging in energy-linked single stocks

Variant Perception’s team suggest that underperformance in the energy market may continue, but they still see an opportunity for select single names if/when their tactical models turn bullish. They examine the market for single stocks that have favourable business models that benefit from higher volumes for oil and gas, and that screen well on VP metrics like capital cycle, crowding, and quality. Oilfield services, midstream and tankers are well suited, US-listed oilfield services are not. Despite appealing valuations, some midstream names still offer reasonable upside and volatility. However, among tankers, the team are highly cautious on LNG and product tankers as these have a glut of new builds coming online in the next few years relative to the existing fleets. Potential plays include Schlumberger, Baker Hughes, Enterprise Products Partners, Frontline and DHT.

Edition: 216

- 25 July, 2025

The trade war is dead, long live the trade war!

Despite all of the dire headlines about the imposition of a 25% tariff rate on Canada and 30% on Mexico and the European Union, Cam Hui says the only trade war that matters is effectively over. China has won. In the short run, economic policy uncertainty is receding but it’s not fully normalized. According to Cam, it’s time to adopt a risk-on posture. US equities lagged most during the trade war panic, and they are recovering and should be the leadership in the short term. In the long run however, Trump’s America First policies of continuing trade wars and efforts to reshore low value-added industries are likely to erode U.S. productivity and competitiveness. The S&P 500 is already trading at a highly elevated forward P/E of 22.2. Cam believes that equity investors should not expect US equities to continue to outperform global stocks in the next expansion cycle.

Edition: 216

- 25 July, 2025

Europe vs China: The battle for automotive dominance

Wolfgang Münchau points out how China is far ahead of Europe in all the categories that will determine the competitiveness of next generation cars – batteries, rare-earth magnets, AI software, and key components of electric engines. In fact, the country has left the EU behind in virtually all dimensions of 21st century technology, even in clean tech which was previously touted as a valuable opportunity to carve out a niche. Wolfgang says a role as junior partner of China is what the EU should hope for, but the likelihood is that they cut themselves off through non-tariff barriers and protectionist policies. Germany’s economic decline is a failure of the corporate sector to invest in 21st century technologies, and a failure of the government to create an efficient capital market that penalises such situations. They’re not even talking about it.

Edition: 216

- 25 July, 2025

Forecasting 2yr swap rates

DeepMacro’s Short Term Rates-1 (STR-1) model provides forecasts of 2yr swap rates for the G10 countries over the next three months. Jeffrey Young chooses 2yr swap rates because they are an estimate of the market's expectation for monetary policy over the medium term, which he believes is usually a function of economic growth and inflation. It generates receive/pay recommendations based on the difference between model forecasts, and market forward interest rates. The inputs to the model are the DeepMacro growth and inflation factors, including "Big Data", and DeepMacro's automated, machine-driven analysis of central banks. Currently, in the US Jeffrey expects rates to rise but market forwards expect the opposite. For the EUR, Jeffrey is also going against the market, with expectations of rate declines vs market expectations of a rise. In the UK, both agree on rate declines, but Jeffrey sees them falling more than market forwards.

Edition: 216

- 25 July, 2025

Top large cap picks for 2H25

Following a strong H1, AIR remains focused on companies that can continue gaining market share through exceptional management, innovation and cost discipline - all driving rising operating margins and FCF, even in challenging environments. The following names pass all 45 of AIR’s proprietary filters (3 layers of 15 valuation and quality criteria) and are expected to significantly outperform over the next 12 months: 1) Adidas - ranked No.1 in AIR’s quantitative system, with accelerating EBIT, margin gains and surging FCF. 2) Aena - best-in-class margins, strong traffic growth and a robust balance sheet. 3) Prysmian - a key player in energy transition and digital infrastructure with a record €40.3bn order book. AIR rates all three stocks as Strong Buys, with 50-100% upside potential.

Edition: 216

- 25 July, 2025

US: Claims about claims

Some investors watch the weekly fluctuations in initial claims for unemployment insurance benefits as if they are the secret to calling the next turn of the labour market or business cycle. Yet, the relationship has only a 0.34 correlation, and Carl Weinberg says attempts to ascertain a greater fit in the data fails. There are three factors that can make the unemployment rate rise or fall: a recession or fears of an impending one. Employees quitting without a new position to go into (which signals confidence in the labour market), and immigration. What we are seeing week-to-week is more noise than signal, and investors should instead pay attention to the monthly JOLTS data.

Edition: 216

- 25 July, 2025

Super Copper

Craig Ferguson points out that US tariffs uncertainty remains with 50% tariffs on copper imports spiking the metal to new all-time highs. He expects a supply deficit from next year, one that will last for years as electrification and the transition to renewables unfolds. Countries like the US will now build copper strategic reserves, so Craig would not fade this price spike. This may be the start of a major run higher in the commodity and inflation cycle with copper (and gold, uranium and platinum) already leading the way. This may suggest a new super cycle in commodities has begun. This would suggest a super cycle in big ASX miners and the AUD also has begun (be OW both). However, it also is inflationary and would complicate things for global central banks, bond yields and stock markets. Craig is surprised that both BHP and the AUD are not higher as both should be on this news.

Edition: 215

- 11 July, 2025

Litigation Watch: Top focus names for Q3

MDC follows significant legal disputes to provide clients with actionable investment ideas. Focus List situations that they believe may be among the most actionable during Q3 include Burford Capital, Reckitt Benckiser and Bayer. Burford is a UK based litigation funder that has already been awarded a Judgment totalling $16,099,788,293. Now, the challenge is to collect from the Republic of Argentina! Reckitt along with Abbott Laboratories are facing product liability lawsuits in the US regarding baby formula products causing NEC. The next bellwether trial will be in the Diggs Case scheduled to start on Aug 8th. As if Bayer hasn't faced enough toxic tort litigation regarding its Roundup weed killer product, it now faces potential liability for Polychlorinated Biphenyls. The next PCB Trial is scheduled to commence on Sep 8th.

Edition: 215

- 11 July, 2025

US Healthcare: What's next from DC

Healthcare

With President Trump signing the OBBB into law, Washington will now turn to other regulatory priorities and states will begin work on implementing the Medicaid reforms. Aldis Institutional's policy-focused events provide investors with timely and actionable insights into the DC landscape. This differentiated platform combines small group conversations with key stakeholders and policymakers, with real-time market commentary from Aldis' senior team. Recent and upcoming event topics include the change to the ACA exchanges and impacts on insurers (Centene, Molina Healthcare), Medicaid reform implementation - including work requirements and provider tax changes, and the outlook for home health and DME/CGMs after CMS's recent proposed rule.

Edition: 215

- 11 July, 2025

The secular bull market for Banks gets a midyear tailwind

Financials

US bank stocks can continue to hit new highs and assume a leadership role in the market, according to Charles Peabody. Fundamentals are excellent, balance sheets are strong and capital is abundant. Meanwhile, the next 12-18 months will likely include a reduction in capital requirements as part of the deregulation process. Reducing the CET1 ratio by 1% can add double digit earnings growth to banks either through buybacks or growing earning assets. Deregulation can also reduce expenses by 1-3% annually. While this process is in place, investors have become accustomed to one way headaches from regulators, and thus, deregulation is only reflected in stock prices after it happens. Charles' top picks are Citigroup, M&T Bank and Citizens Financial.

Edition: 215

- 11 July, 2025

Is liquor the next luxury?

Consumer Staples

David Scott argues that luxury liquor companies are facing the same structural challenges confronting luxury apparel. While pandemic-era demand and post-Covid inflation masked underlying weaknesses, those issues are re-emerging. Key headwinds include shifting demographics and declining alcohol consumption among younger generations, as well as industry overpopulation and fragmentation. Liquor companies are experiencing falling asset turns but margins have not risen to compensate and the operating leverage effects will be "very vicious" as a result. David also sees the rising use of weight-loss drugs like Ozempic as a further negative catalyst. Companies discussed include Diageo, Pernod Ricard, Brown-Forman, Kweichow Moutai and Wuliangye Yibin.

Edition: 213

- 13 June, 2025

Communications

Andrew Freedman initiates a short on RBLX, contending the market is underestimating structural headwinds that will pressure the stock over the next 12-18 months. His proprietary Metaverse Tracker shows strong 2Q25 DAU trends - driven primarily by the success of Grow a Garden and favourable calendar dynamics - marking what he views as peak growth. However, Andrew’s analysis points to limited runway for sustained user acquisition at current growth rates, a more challenging competitive landscape and increasingly difficult comps. He expects a sharp deceleration in growth and monetisation, diverging meaningfully from consensus. At ~$95, he sees limited upside ($10-15) and significant downside risk ($30-40).

Edition: 213

- 13 June, 2025

Vista Energy (VISTAA MM) Mexico

Energy

EM Spreads recommends buying Vista’s new 2033 bonds, citing an attractive 8.5% yield and shorter duration relative to the 7.625% 2035 notes (yielding 8.3%). The bonds offer a more compelling return within Vista’s debt capital structure and screen wide relative to the broader EM BB and LatAm BB curves. Strong execution on well tie-ins and midstream expansion supports the group's ambitious EBITDA and production targets. EM Spreads views Vista as a top credit pick for exposure to Argentina’s energy sector, with relative insulation from sovereign risk. They believe operational momentum and an improving macro backdrop, including easing capital controls, could drive bond outperformance over the next 9-12 months.

Edition: 213

- 13 June, 2025

Communications

A high-quality business with a sustainable competitive advantage, underpinned by strong FCF generation, limited debt, low stock-based compensation dilution and 70%+ EBITDA margins (with incremental margins over 90%). Its proven dominance in gaming advertising through advanced AI engineering is now being leveraged to expand into new verticals like direct-to-consumer ecommerce, where Abacus sees a high probability of success. The 2Q25 launch of self-service tools could further accelerate growth, supporting a bullish outlook for this year and next. Abacus expects rapid FCF growth through 2027, which the market has yet to fully price in. Their TP of $635 offers 65% upside.

Edition: 213

- 13 June, 2025

Trumping the agenda

According to Helen Thomas, the BoJ, the Fed and the BoE will all be unchanged next week. The first two want to wait and see what happens to tariffs, whilst the BoE remains split over how soon to deliver the next interest rate cut. The BoE can't even rely on data as their guide, not that the data really matters right now, with political decisions the driver of the economy. Fiscal policy, trade and tariffs will be right back in focus before Congress breaks up for summer after Independence Day, with President Trump hoping the Big Beautiful Bill has become law, that the pause in reciprocal tariffs has yielded big beautiful trading partnerships and the NATO Summit has the whole western world, rather than just America, tooled up and ready for war. Expect a ramping up of threats, intimidation, handshakes and back slapping, all at once.

Edition: 213

- 13 June, 2025

A transition tipping point

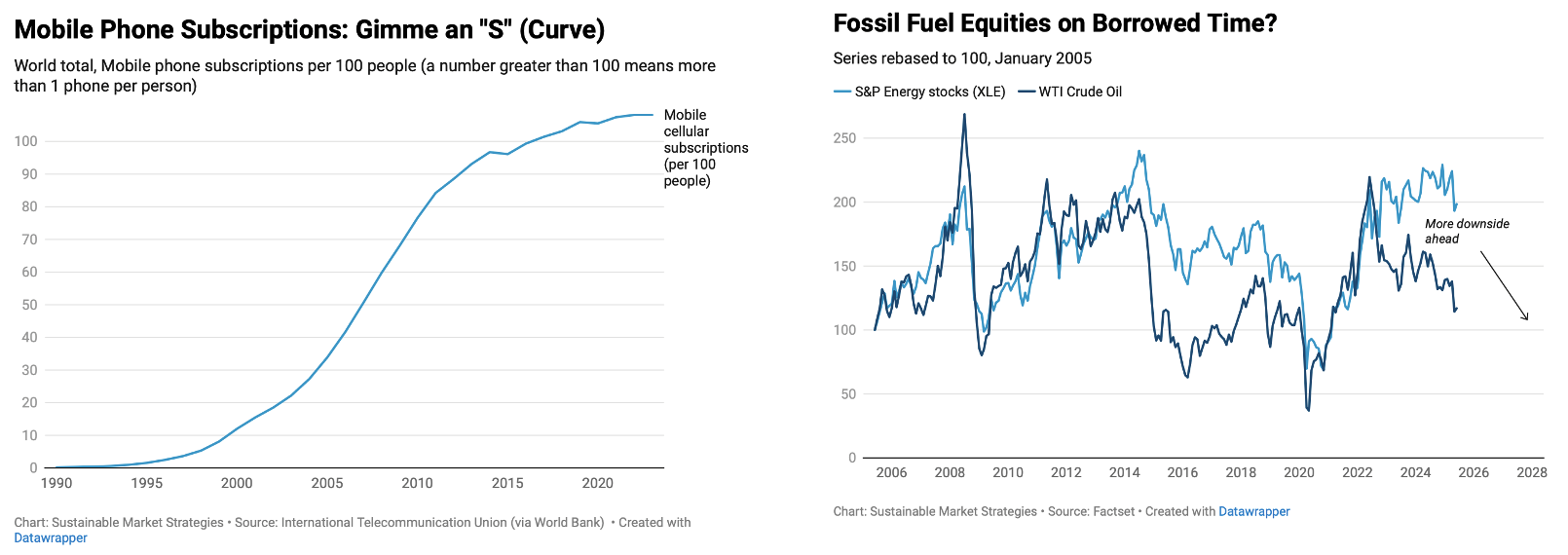

Renewable energy technologies may be entering the most exciting phase of the S-curve when it comes to aggressive gains in market share relative to incumbent fossil fuel sources. Just like mobile phone subscriptions (see chart), the S-curve demonstrates that investors must think about timing instead of assuming liner growth in order to obtain the best returns. EV sales in countries like Norway have already reached the end of their curve, and fossil fuels such as coal are seeing an inverted S-curve at play. Fossil fuel equities may be living on borrowed time (chart 2), and investors that have not yet diversified away from conventional energy assets should do so before the next wave of imminent write downs of stranded assets begins. The window is closing rapidly; act quickly.

Edition: 212

- 30 May, 2025

Recombinant Collagen: China’s next Beauty growth engine

Consumer Staples

Recombinant collagen is emerging as a transformative force in China’s beauty and aesthetics sector, poised to replace traditional hyaluronic acid and animal-based collagen in both medical and skincare applications. On the clinical side, Jinbo Bio stands out as the only company with Class III approval for injectable collagen, expanding its product lineup and expected to grow revenue by over 50% in 2025. In the skincare space, Giant Biogene leads with strong brand equity and broad channel reach, using collagen innovation to power new launches and deepen consumer engagement. With rising demand for safe, science-backed ingredients, recombinant collagen is becoming a structural growth story to watch.

Edition: 212

- 30 May, 2025