Fortnightly Publication Highlighting Latest Insights From IRF Providers

Company Research

Materials

GMR maintains a Buy rating on NST following their KCGM site visit, reaffirming the mine’s Tier 1 status with a US$6.7bn NPV5 valuation. The A$1.5bn expansion remains the key near-term focus and risk, but appears on track for completion within 12 months. While the market remains concerned about lower near-term FCF and high capex (~A$500m/year), GMR sees KCGM as strategically critical, with meaningful upside from displacing low-grade stockpiles with higher-grade ore, improving mill throughput and ramping up the Fimiston underground. The mine’s long life, production growth potential (to 850-900koz by FY29) and exploration upside through high historical OVMs make it NST's crown jewel, but successful delivery in the near term remains crucial for realising that value.

Edition: 217

- 08 August, 2025

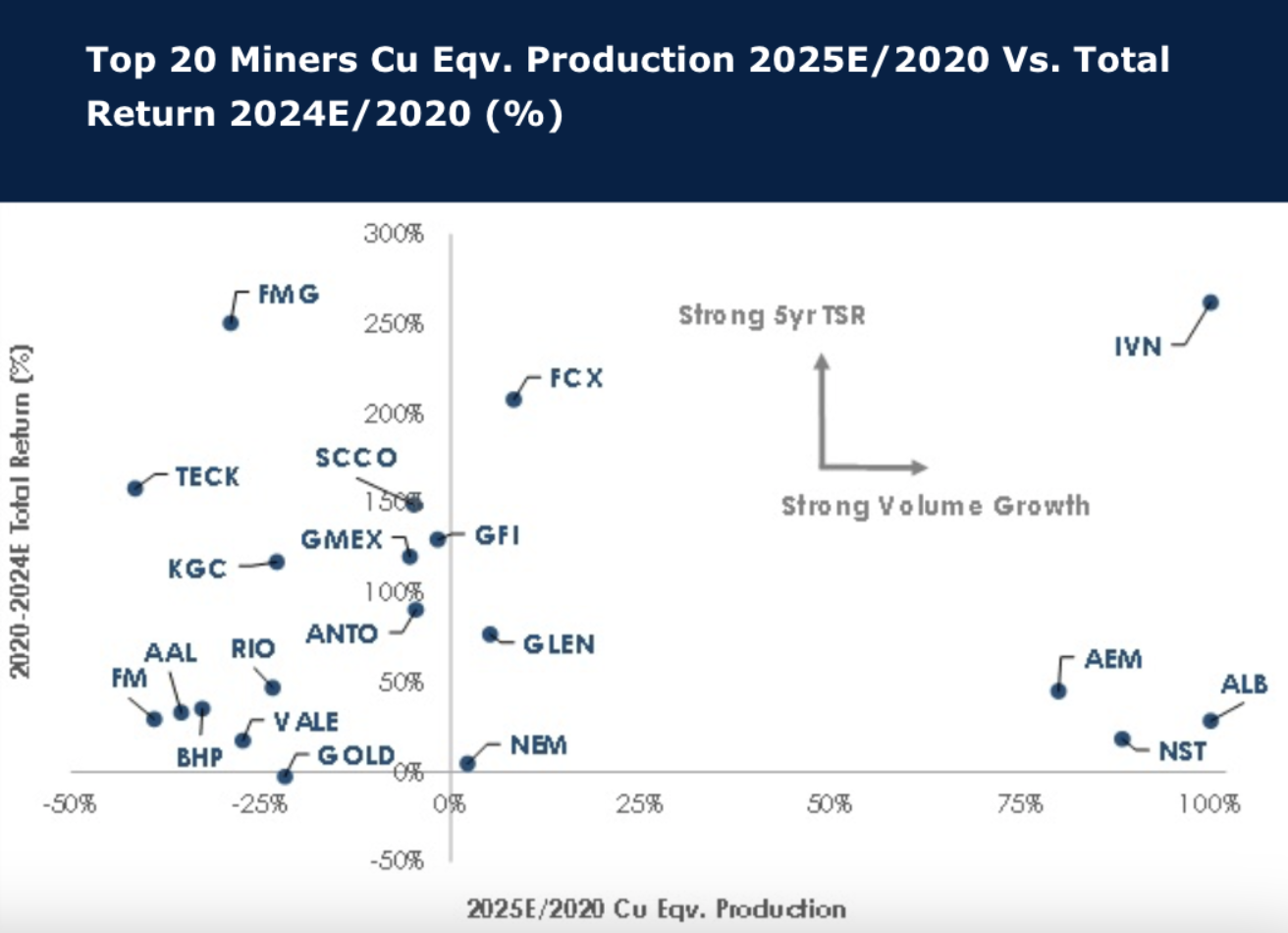

Large cap miners: Performance and growth are not related

As Sellside and Buyside set expectations for 2025, Global Mining Research examines the recent history of the leading miners. Interestingly, only Agnico Eagle Mines Limited, Albemarle Corporation, Ivanhoe Mines Ltd, and Northern Star Resources Limited are estimated to have materially grown through investment and M&A over 2020-2025E. In fact, most miners have shrunk in terms of Cu Eqv. Production, and exiting coal was a clear trend. The copper miners have outperformed, despite iron ore miners clearly returning the most cash to shareholders in dividends. Buybacks should have helped the share price return but there is little evidence this works. For over half the group, a ‘buy and hold’ strategy has not generated a robust return over the period. This reinforces the view that miners are to be traded.

Edition: 202

- 10 January, 2025

How to pick a gold stock in 2022

Global Mining Research’s BUY and SELL signals served investors well in 2021 despite some market disconnect between equity price and numerous variables, including dividends. This year, David Radclyffe sees the gold sector shifting more to a growth/scale focus over returns/balance sheets; so, more M&A, growth investment, inflation impacting margins, lower dividends and a focus on ESG. David’s latest report looks for stocks that match the investment themes within the sector. Key picks include Agnico Eagle (new BUY signal), Barrick Gold, Northern Star Resources and Endeavour Mining.

Edition: 129

- 18 February, 2022

Aussie gold: Recalibrating portfolios, increasing spending

Headwinds from labour shortages and inflation have made 2021 performance lacklustre, but factors that usually favour gold, such as inflation and geopolitical risk, are clearly on the rise. Growth capital expenditure is set to more than double the rates of a few years ago at ~US$375/oz in FY22 in order to satisfy investors. David Radclyffe’s preferred exposure to Aussie gold is through Northern Star Resources and Evolution Mining (recently upgraded to BUY), whilst St Barbara falls in last place as difficult choices lay ahead.

Edition: 128

- 04 February, 2022

Aussie golds spending their dollars

Australian gold companies are heavily reinvesting their cash surpluses. This increased investment indicates companies are becoming more confident in higher prices for the long-term, backed by unleveraged balance sheets. BUY rated Evolution Mining (target $4.80) is expected to reinvest ~US$400/oz in major/growth capital over FY22-FY24E. Northern Star Resources is looking at reinvesting ~US$195/oz but remains the preferred BUY rated Aussie gold with a target price of $14.00.

Edition: 116

- 06 August, 2021