Fortnightly Publication Highlighting Latest Insights From IRF Providers

Company Research

Special Sits Idea Forum

MYST’s latest buyside event saw a large group of investors offer a diverse set of ideas spanning various sectors / themes. Stocks highlighted include:

Bayer (BAYN GR) - New management advancing turnaround as litigation resolution approaches. TP €40 (65% upside).

CRH (CRH) - Increased pricing power + Ukraine rebuild opportunity to narrow valuation gap vs. peers. TP $135 (35% upside).

NFI (NFI CN) - Earnings / margins to rebound sharply as production issues ease. TP C$40 (200% upside).

Paramount Global (PARA) - Pending deal approval to trigger “structural bid” from Arbs while streaming business inflects. TP $15 (30% upside).

Parkland (PKI CN) - Substantial SOTP upside amid ongoing strategic alternatives process. TP C$54 (45% upside).

Edition: 207

- 21 March, 2025

Are low rates and a weak CNY really to be feared?

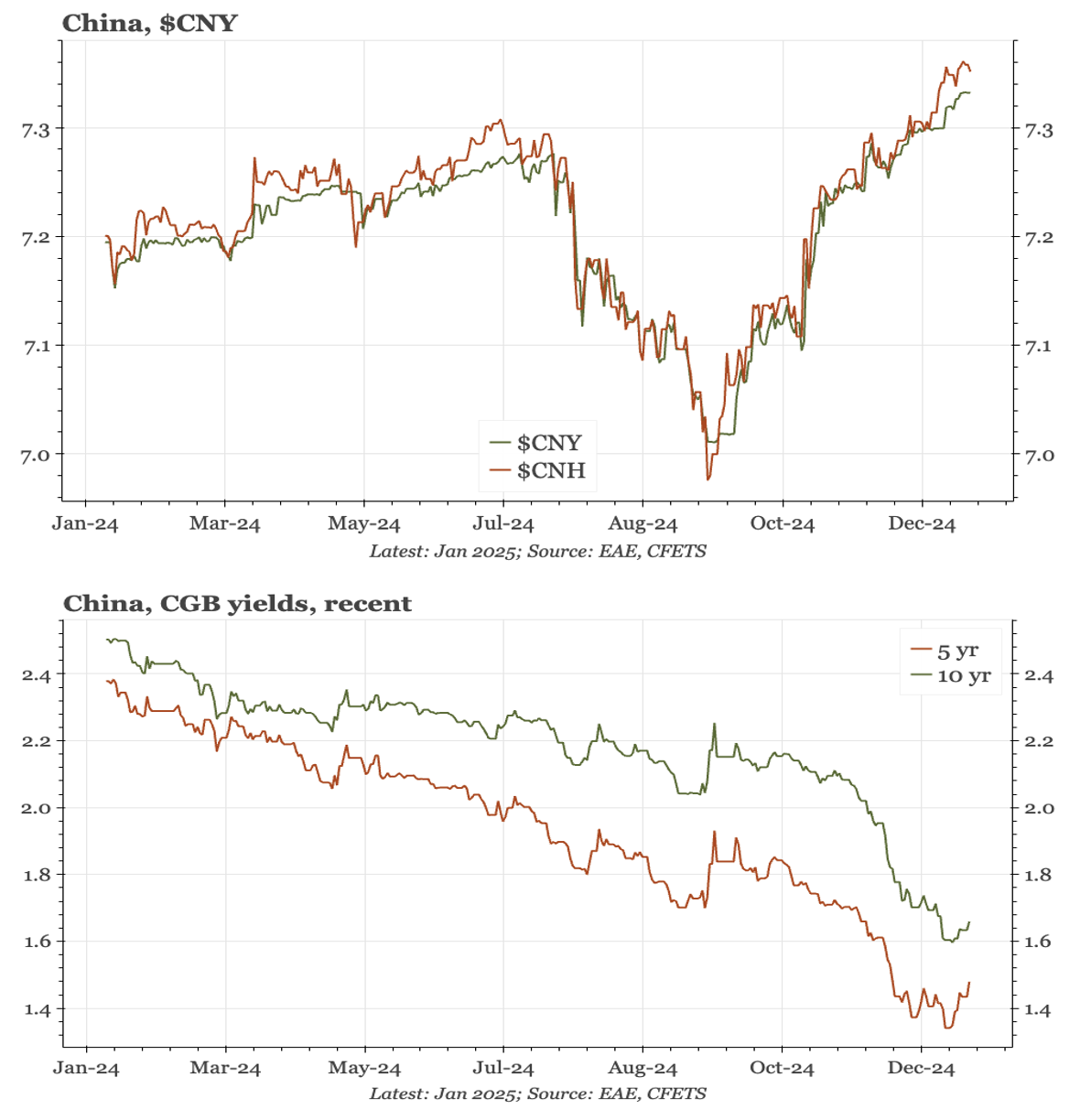

Paul Cavey points out that there are two things happening in China's financial markets that seem to be causing concern. One is the rise in $CNY, which is likely to gain more momentum if Trump imposes another round of big tariffs. The worry is that this encourages capital outflows and so risks the sort of financial stability seen in China in 2015. The second development is the fall in yields. That was indeed sharp in Q424, with rates at the longer-end of the curve in particular falling to all-time lows. The substantive idea is that a 10-year yield of just 1.7% is pricing in a multi-year period of deflation and very slow nominal growth. Paul assumes that management of the cycle is probably the paramount concern in the minds of both policymakers and investors right now. It is only in that context that the continued loosening of domestic monetary conditions is welcome.

Edition: 203

- 24 January, 2025

Consumer Staples

Gordon Haskett Research Advisors

Footfall trends starting around May 20th will be paramount in evaluating the company's recovery in the coming months. Recall that headline issues began to mount for the company around this time last year and persisted throughout most of the Summer months leading to Target's negative 5.3% comp in 2Q23. Recall on monthly phasing… May, June, and July SSS declined approximately 3.0%, 7.0%, and 5.0%, respectively. YOY traffic continues to recover nicely with the 7-day moving average up 15.0% YOY.

Edition: 188

- 14 June, 2024

Communications

The heavy lifting on restructuring is now largely complete (Paramount and Disney are just starting theirs) with expenses down $2.8bn and cash content spending running at ~$4bn/qtr. Studios look likely to recover from 2H23, advertising looks to have bottomed, and the new Max streaming platform has a good mix of content that should be attractive to all viewers meaning top and bottom line should show amelioration from here. Arete forecasts EBITDA of $11.2bn in 2023 and FCF of $4.4bn. For 2024, they expect a further improvement in EBITDA to $13.1bn and FCF to jump to $5.9bn (net debt declines to $36.1bn (2.8x) allowing a buyback to start late in the year). TP $31 (130% upside).

Edition: 162

- 09 June, 2023

Communications

High conviction mis-valuation opportunity only emphasised by Warren Buffet's increased investment in Paramount Global - Robert Sassoon argues Netflix’s woes are company specific (reliance on streaming subscriptions has simply laid bare its vulnerabilities). By contrast, WBD, PARA and Disney have diversified revenue models, backed up with high quality content libraries. WBD’s debt burden is also less onerous than it appears (very attractive fixed rate terms and interest payments will be dwarfed by FCF generation prior to the first repayment dates in 2024). Attributing a PARA-like value multiple to WBD's consensus 2023 EBITDA offers 80%+ upside.

Edition: 136

- 27 May, 2022

Somalia: One extension, please

The Somalian government has requested a three-month extension on two credit lines - equivalent to USD $395m - due to expire on May 17th. The request comes as the country’s presidential election is scheduled for May 15th, with it being unlikely a new government will be installed in time to renew the funding arrangement. Funding from the IMF and other multilateral and bilateral organisations is paramount to maintaining fiscal stability in Somalia. Will the IMF agree to their request?

Edition: 135

- 13 May, 2022

Will Russia invade Ukraine?

Forefront Advisors explores how a Russian invasion, or lack thereof, will transform the geopolitical landscape. Russia is on course to achieve most of its short-term objectives just by credibly threatening an invasion. An attack could see Nord Stream 2 killed, US and EU sanctions and the cementing of Belarus as a hostile state to the EU. An invasion is paramount to Russia’s strategic interests and the conditions for an attack are better than ever.

Edition: 125

- 10 December, 2021