Fortnightly Publication Highlighting Latest Insights From IRF Providers

Company Research

Flutter Entertainment (FLTR LN) UK

Consumer Discretionary

UK tax raid rumours create a buying opportunity - FLTR will be able to weather the impacts through market share gains and cost containment measures. Hedgeye sees the blended tax rate going to ~35% starting next year. The market size will be lower as will the profit pool, but FLTR’s piece of the pie will be bigger in the long term. Anyway, it is not the UK growth story that matters (it will represent <20% of EBITDA by 2026 and well below 20% on a long-term basis) as Hedgeye makes the case that the group’s US business alone is worth nearly $200 / share. On revised figures out to 2027, they see a $300+ stock.

Edition: 197

- 18 October, 2024

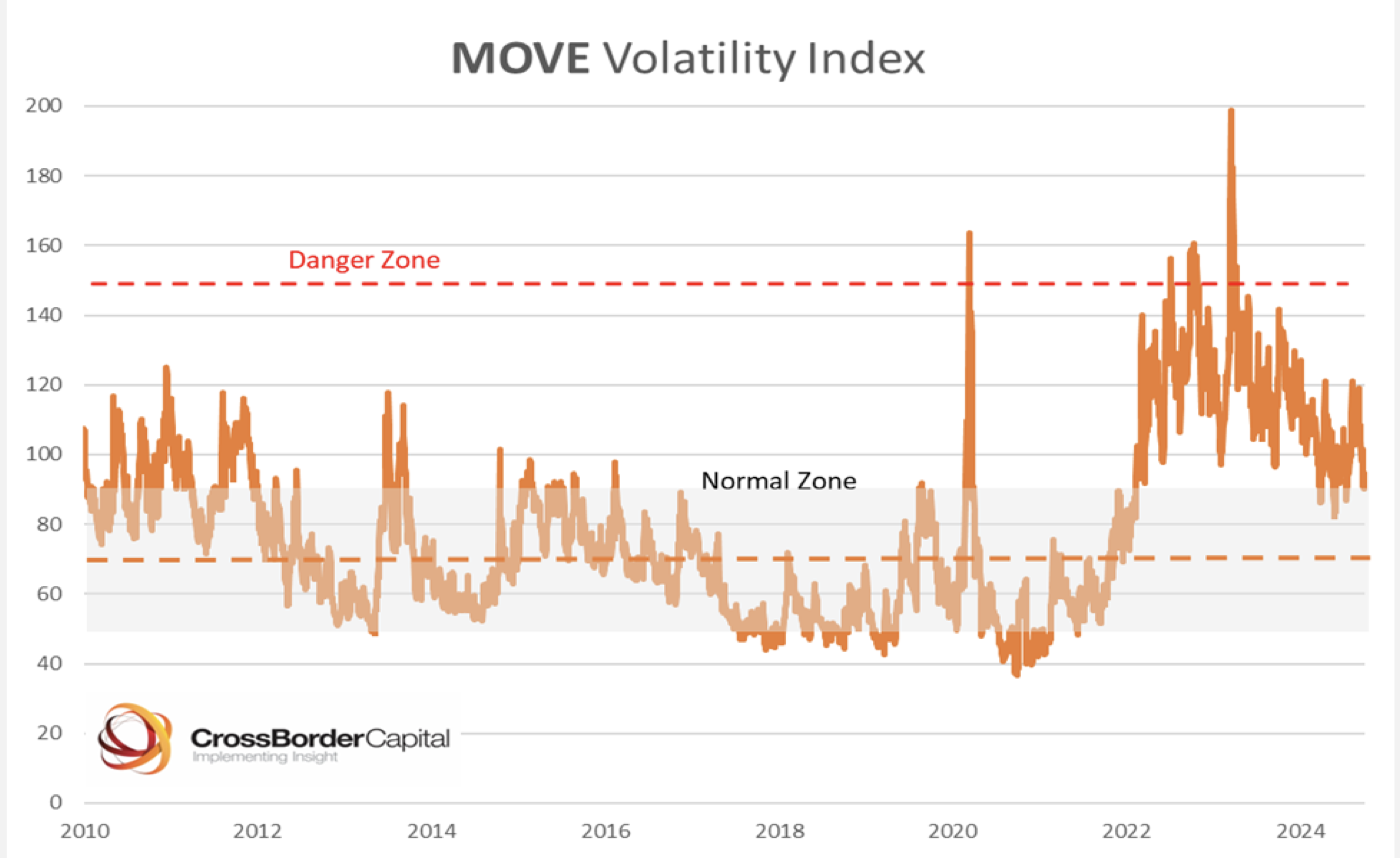

The hidden driver of global liquidity

Michael Howell’s latest report examines another important source of Global Liquidity, where an increasing multiplier pushes up an expanding collateral pool. He argues that the size of this multiplier is closely tied to falling bond market volatility. Thus, more Global Liquidity drives down the MOVE index of bond volatility, which in turn generates more Global Liquidity in a self-reinforcing loop. Maybe the MOVE index is more important to investors in risk assets than the more popular VIX index?

Edition: 196

- 04 October, 2024

No free lunch for the Fed

Frank Shostak suggests that the US Fed does not determine interest rates, but instead only distorts the market interest rates set by individuals’ time preferences. The entire guessing game regarding the Fed’s rate stance is erroneous. What is required is to ascertain the damage that the interest rate policy inflicts on the pool of real savings. When money out of “thin air” is injected into the economy, this creates an exchange of nothing for something. The receivers of the injected money can now divert to themselves consumer goods from the producers. When the central bank attempts to counter the rising interest rate trend by means of injecting money supply, this can make the rising trend steeper because the increase in the money supply creates an exchange of nothing for something, thereby weakening the pool of real savings.

Edition: 186

- 17 May, 2024

Building Product Distributors still offer plenty of upside

Industrials

Many market participants are looking for a way to play housing and it would be easy to look at building product distributors and write them off as being overvalued and that you’ve missed out. However, TRG believes this is faulty logic. Builders FirstSource, Beacon Roofing and GMS (as well as others) have margin profiles that have risen to comparable or superior levels in relation to the “premium-valued group” (SiteOne, Pool, Leslie's, Core & Main and Ferguson), but have EV/EBITDA multiples (avg. 10.6x) well below these stocks (avg. >20x). If they gain a more appropriate multiple (for strong SF starts and better margins) on higher EBITDA, then all three companies still offer significant (~70%) upside.

Edition: 183

- 05 April, 2024

US: What drives the economy?

Rather than looking at many economic indicators to establish the state of the economy, it is going to be more effective to establish the key factor that drives the economy. Frank Shostak suggests that this is the pool of real savings. With respect to the Fed’s monetary policies, the market is starting to sense that the US central bank is likely to ease its interest rate stance in a few months’ time. For the time being, the ongoing Fed’s tampering is continuing to distort the economy. This undermines the process of real savings formation. Because of the time lag from changes in money supply and its effect on economic activity and prices, Frank is of the view that the strong decline in the momentum of money is likely to dominate the economic scene in the months ahead.

Edition: 178

- 26 January, 2024

Japan: Mrs Watanabe’s threat to world bond markets

Michael Howell argues that Japan’s shifting YCC policy is far from the greatest threat to global bond markets from Asia. A bigger issue is the stability of Japan’s huge household savings pool; the impact of Asian savings has been forgotten but is still meaningful. Currently invested in low yielding deposits, the savings are anchoring low world interest rates, which Michael says may help to explain the tight correlation between the bond term premia across the US, UK, Germany and Japan. However, faster Japanese inflation (already higher than many investors believe) and/or a rapid economic rebound across the Asian economies, could lead to a significant asset shift away from global bonds.

Edition: 174

- 24 November, 2023

Defence Insight: European security of supply

Industrials

War in Ukraine has provided Europe, specifically the EU, with a much-needed reality check and opportunity to reform how it handles defence, starting with cooperation. While one of its weaknesses is integrating a group of 27 individual member-states into a coherent entity, it also represents a strength that it should capitalise on. This should start with further integration of Nordic states into EU projects to pool greater resources together and help improve supply chain resilience. However, to do this, the EU must do better - moving away from solely financial-based incentives and enhancing the value of its initiatives to enhancing the value of its initiatives to member states and other partners.

Edition: 161

- 26 May, 2023

US: Beware the Fiscal Cliffers!

Concerns that the US is approaching a fiscal cliff are misplaced. Fiscal policy won’t be a drag in 2022 and will in fact still be providing stimulus to the economy. It’s crucial to note that government transfers to the private sector are not directly counted in GDP, but rather only when the funds are actually spent. The huge pool of household savings sitting in cash will be spent over time as consumers feel more confident and spur greater investment and consumption with a long lag.

Edition: 118

- 03 September, 2021

Lack of customer expertise hurts Enterprise IT sales

Technology

Blueshift primary research finds the effectiveness of cloud-based applications is swiftly diminishing the need to retain in-house IT staff, leaving a dwindling pool of experienced workers clinging to familiar last-generation technologies, instead of staying current on newer IT capabilities. Hence, enterprise technology sales are likely to miss a hoped for rebound in H2 to the direct benefit of the public cloud operators. Positive: Amazon, Datadog, Microsoft. Negative: Cisco, IBM, Snowflake.

Edition: 111

- 28 May, 2021

Securities Filings Analysis: Pinterest (PINS), Pool Corp (POOL) & Prestige Consumer Healthcare (PBH)

280first is a technology powered service that rapidly extracts actionable insights from 10-Q / 10-K text discussions through quantitative and qualitative inputs. Recent alerts include:

PINS - user engagement concerns? Added a reference to its Q1 10Q re. ‘new content and new forms of content that may not have as much relevancy as prior content…Pinner engagement may decline...’

POOL - tough times ahead? No mention of ‘expectations to gain market share…’ that was present in its 2020 10K.

PBH - management increasingly bullish / shareholders to be rewarded? Removed the risk factor re. ‘no intention of paying dividends…’

Edition: 110

- 14 May, 2021