Fortnightly Publication Highlighting Latest Insights From IRF Providers

Company Research

China: From trade war to tech war

Don Ma has distilled the latest US-China escalations into actionable insights. The shift from trade to tech war amplifies trends like self-reliance and friend-shoring, reinforcing long-term investment themes rather than disrupting them. In the short term, rising risks in market sentiment, supply chains, countermeasures, and geopolitics could trigger a 10%+ adjustment, eroding momentum strategies. Rare earth disruptions pose real threats to global tech production. Over the medium-term, expect supply chain redundancy builds, accelerated Chinese outbound manufacturing, and stronger domestic substitution. Trump's negotiation leverage may weaken due to legislative roots, prolonging tensions. Over a longer horizon, systemic distrust will entrench friend-shore/near-shore economies, benefiting ASEAN hubs and amplifying US’s structural inflation vs China’s deflation. Hedge with long gold/short crude. Compared to prior rounds, the recent conflicts are more strategic and entrenched, with lower compromise odds mid-term but enhanced supply chain rebuilding long-term.

Edition: 222

- 17 October, 2025

Healthcare

BTN raises concerns about DGX's reliance on acquisitions for growth, questioning its sustainability given rising debt (3.0x EBITDA) and acquisition spending that regularly exceeds FCF post-dividends and buybacks. They also highlight earnings quality issues: over half of Q1’s EPS beat came from an unexpectedly low tax rate; receivables are rising without a corresponding increase in bad debt allowance; and more than $2.00 per share in acquisition-related expenses are not being recognised, which is over 20% of the company’s expected 2025 non-GAAP EPS forecast.

Edition: 212

- 30 May, 2025

Consumer Discretionary

John Zolidis removes DKS from his LONG list, following the group's proposed takeover of Foot Locker. He argues that the deal undermines the rationale for assigning DKS a premium multiple, which had been supported by its consistent performance and structurally superior margins. John is deeply sceptical that management can succeed where respected executive Mary Dillon failed. The acquisition threatens to create even more banner conflict, overlapping real estate, greater reliance on Nike and adds significant operational complexity. Crucially, FL lacks unit growth - the one element DKS was missing. While some cost synergies and FCF may eventually be realised, it will take a long time to recoup the $2.5bn price tag.

Edition: 211

- 16 May, 2025

Communications

Andrew Freedman sees Google’s AI Overviews as a critical and underappreciated threat to RDDT’s business model, with RDDT content already pushed lower in search results vs. 2024. This validates his earlier view that the company’s heavy reliance on Google traffic is a key risk. Marketer feedback from 1Q25 also points to sharp declines in organic traffic, hitting both user growth and monetisation. While global user numbers may appear encouraging, they are largely driven by new translation features in international markets like India. These markets, however, monetise poorly and are unlikely to contribute meaningfully to revenue or profit growth. Looking ahead, Andrew anticipates increasingly volatile advertiser and user behaviour going into 2H25. He forecasts a faster-than-anticipated deceleration in revenue growth and a stock that is 40% lower over the next 12-months.

Edition: 211

- 16 May, 2025

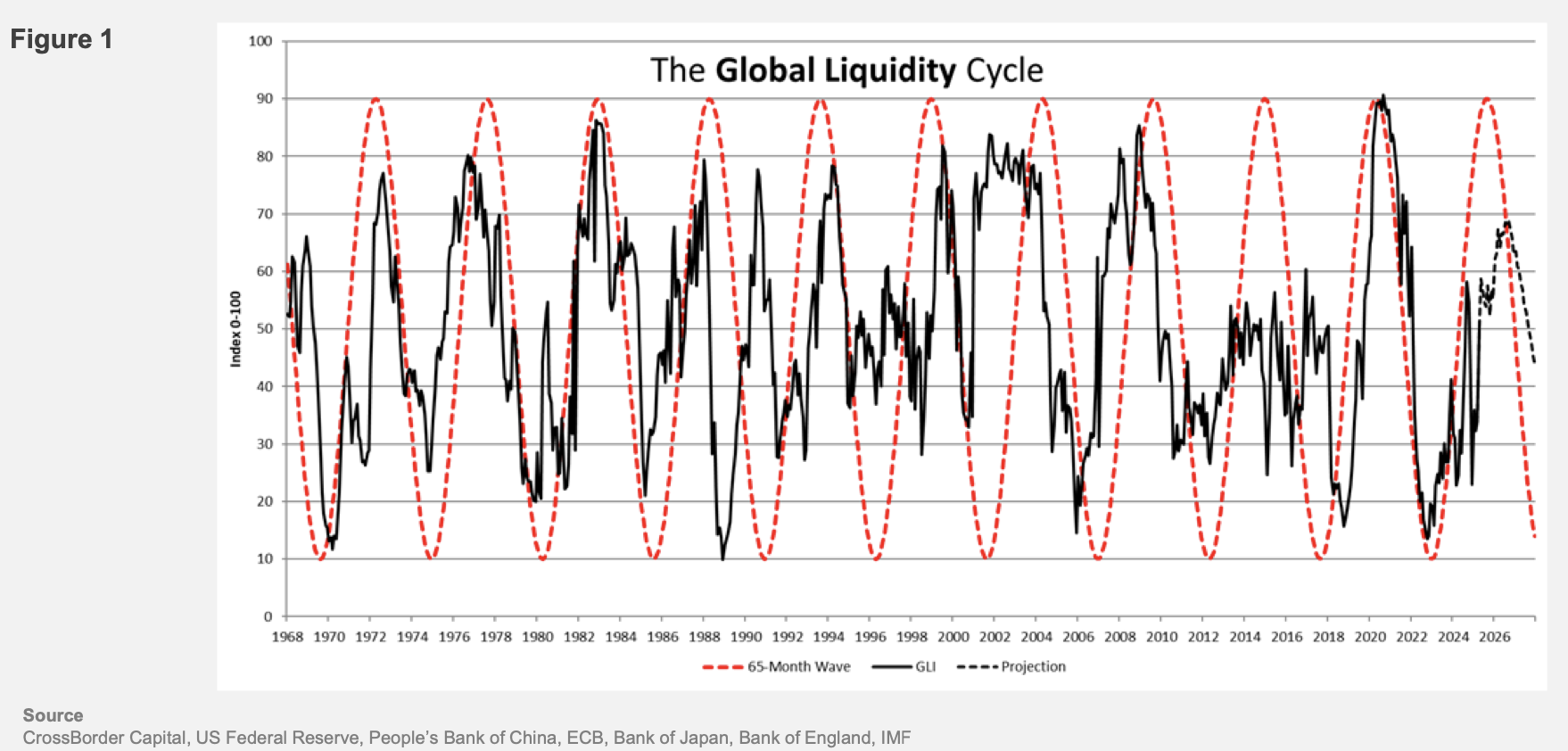

A looming recession

Global liquidity is edging higher, driven largely by China's aggressive monetary easing to avoid recession amid trade tensions. But, alongside, the US faces tighter future liquidity conditions due to declining private sector cash flows, shrinking bank reserves and collateral shortages exacerbated by the debt ceiling standoff. The modern financial system’s reliance on US Treasury collateral — now paradoxically in short supply — has heightened repo market stress, with key indicators like the SOFR-Fed funds spread and MOVE index flashing several warnings. Despite superficial Fed liquidity gains from TGA inflows and seasonal factors, Michael Howell comments that underlying pressures point to deflationary risks, compounded by the Fed’s reluctance to ease amid sticky inflation and political constraints. This divergence sets the stage for potential liquidity shocks, with China propping up global markets as the US grapples with a fragile debt-refinancing mechanism and the spectre of 1930s-style demand collapse. Investors are reducing risk exposure.

Edition: 211

- 16 May, 2025

Communications

META is doubling down on AI infrastructure, raising its 2025 capex forecast to $64–72bn as it accelerates data centre construction amid rising costs. CEO Mark Zuckerberg is committed to making META a leading AI platform and insists on building in-house capacity to avoid reliance on others. While the AI strategy (centred on open source) is progressing well, it comes with a steep price tag, notably the ongoing $4bn+ quarterly burn at Reality Labs. Richard Windsor sees a growing risk of AI infrastructure overbuild, with META, Google, Microsoft and Amazon all ramping up spend - setting the stage for a painful correction. Despite this, META’s core business remains solid, with strong Q1 performance and improved operational efficiency via AI. At 23.5x FY25 PER, META is reasonably valued, but Richard prefers Google, where AI disruption risks from players like OpenAI are, in his view, overstated.

Edition: 210

- 02 May, 2025

US: Cash is king

Despite a much hyped and universally expected decline in the TGA, Andrew Hunt’s measures of financial liquidity are in general weak. Surging R/P lending activity may be a sign of rising strains within the financial sector. Credit quality may be deteriorating. It is early days, but these signs deserve close monitoring. The rate of tightening in fiscal policy has slackened as DOGE has lost momentum. It seems that rising credit demand in the real economy has left banks with “less money” to lend to the financial sector. Rather than “crowding out” the real economy – as has frequently been the case over recent years - the financial sector could be being crowded out by rising credit demand from the real sector. This de-financialization could leave asset markets vulnerable. US banks are retreating aggressively from foreign markets. Andrew is negative the USD on a six-month view given the US’s reliance on foreign inflows.

Edition: 207

- 21 March, 2025

Kone (KNEBV FH) Finland

Industrials

Iron Blue initiates coverage on the stock with a score of 27/60, which is top quartile (fertile grounds for shorting) and their equal highest score in the Capital Goods sector. They highlight 1) Reliance on percentage-of-completion revenue recognition. 2) Sustained stripped out restructuring charges. 3) An ageing debtor book (China construction). 4) Widened gap between capex and depreciation. They also note governance out of line with best practice (elevated non-audit fees, non-independent chair, board & remuneration committee and narrow CEO variable compensation payout metrics) as well as many areas of imperfect disclosure.

Edition: 201

- 13 December, 2024

Nigeria: What could go wrong with the latest local crude-for-fuel swap deal?

State-owned Nigerian National Petroleum Company Limited (NNPCL) has notified the Nigerian Upstream and Downstream Petroleum Regulatory Authority (NMDPRA) that it will no longer import petroleum products from 1 October “if local pricing is competitive”. Given the country’s historical reliance on fuel imports and its negative impact on foreign exchange, the development is potentially game changing for Nigeria. However, recent public spats between NNPCL and the local crude refinery (the expected main supplier for the market), including over pricing modalities, operational risks and logistical challenges, risk undermining any potential benefits.

Edition: 195

- 20 September, 2024

Technology

ETR conducted a CRWD focused flash survey of 100 IT decision makers on the day of the global IT outage to capture the initial impact and reaction to what was unfolding. Nearly 75% of respondents were from large organisations, including 25% from Global 2000 firms. While 56% of respondents were very unlikely or somewhat unlikely to replace CRWD, a similar amount were reconsidering their reliance on the company and expressed disappointment in its testing and response, urging better QA processes and improvement in communication. Since publishing their findings, ETR has gathered CRWD customers who can share how the outage affected their organisations and discuss how it will influence their relationship with the cybersecurity firm moving forward.

Edition: 192

- 09 August, 2024

Ukraine: Debt restructuring deal is ambitious

Ukraine’s preliminary sovereign debt restructuring deal balances short-term downside risk protection for creditors against substantial debt relief for Kyiv. However, the restructuring is also clearly ambitious given its reliance on unrealistic IMF growth and debt sustainability forecasts, setting the stage for a potential second restructuring around 2027/2028. Max Hess continues to consider the GDP warrants effectively worthless - a view reinforced by the fact that the deal removed cross-default provisions to those warrants. Meanwhile, Russian forces continue to make creeping advances on the front across Ukraine’s Donetsk region, particularly in its south. Max believes that it is likely that Russian forces will control almost the entirety of the Donetsk region for the first time ever by year’s end if the current pace of Russian advances continues.

Edition: 191

- 26 July, 2024

US/EU: Further across the pond

With Biden goes the last of the great US trans-Atlanticists – Wolfgang Münchau points out that there are no more Democrats who will follow in the same tradition. The EU needs to prepare for the shifting US political landscape on both the Republican and Democrat sides. Interests are diverging, and as fiscal constraints kick in, the US will be even more reluctant to engage in international ventures that carry no domestic political pay-off. The discussion about Europe’s self-sufficiency often narrows down to defence spending, which is certainly important, but Wolfgang believes Europe’s reliance on US technology and the fragmentation of economic policy, including capital markets and services, is far more critical.

Edition: 191

- 26 July, 2024

The fault at the heart of China’s strategy

China’s dominance in the broader renewables supply chain is clear, achieved with smart subsidies early on. However, debt has risen as a share of GDP, and property woes subsist. Growth in the three key sectors – EVs, solar, batteries – is providing an offset to the country’s these woes, but overinvestment in renewables threatens further downward pressure on prices and a profits squeeze. This will lead to a retaliatory backlash from nations struggling to compete with China, stoking trade tensions. It is not possible for China to grow at its current pace and maintain its manufacturing output without increasing its share of global trade. This is the fault line at the heart of China’s strategy, remarks Graham Turner: Western governments want to reduce their reliance on Chinese imports, not increase it.

Edition: 178

- 26 January, 2024

Gold ESG Focus 2023

Metals Focus recently published their latest gold mining ESG report, covering 17 of the biggest gold miners from 2014-22. It revealed that combined scope 1 and 2 greenhouse gas emissions fell by 2% y/y in 2022, partly a result of company initiatives to cut emissions and reliance on fossil fuels. The total combined emissions for the gold mining industry as a whole are estimated at 0.3% of global emissions. Water withdrawals fell 7% and water consumption by 3%, but miners need to further improve water management, especially in regions of water scarcity. Spending on community projects rose markedly, seeing a 37% improvement.

Edition: 169

- 15 September, 2023

Materials

After several years of market speculation TECK is set to spin off its coal business. The Canadian mining group plans to create via a complex scheme of arrangement the jettisoning met coal on the one hand and keeping the cash flow on the other. Financial markets and media are split. Clearly, some have called the move a positive one, while others use terms like “climate placebo” and “greenwashing” and “have your cake and eat it”. Having examined the proposal in detail, GMR is not in favour of the move. If anything, it simply brings to the fore TECK’s reliance on coal. That aside, as a base metal play TECK isn’t cheap vs. peers.

Edition: 157

- 31 March, 2023

Materials

Gradient's 17-page initiation report highlights a variety of fundamental concerns and earnings quality issues: 1) Increasing reliance on pricing to drive revenue growth and looming Performance Chemicals weakness. 2) Surging receivables suggest declining revenue quality. 3) Inventory levels have diverged from near-term demand estimates and appear at odds with expectations of gross margin expansion. 4) Facing margin headwinds from its accrued liability and prepaid expense accounts. 5) Analysts may be underestimating FY23 depreciation. 6) Trades at a massive premium to peers across a wide array of both trailing and forward-looking valuation metrics.

Edition: 153

- 03 February, 2023

Consumer Discretionary

Rakuten expanded its Mobile segment disclosure at Q3 which is great for investors but the message is not very positive as roaming costs remain elevated and hopes for a recovery are now being pinned to the receipt of platinum band spectrum but that is years away even if the regulatory outlook is improving. With a continued reliance on KDDI for roaming and the associated costs that come with it which are higher than total service revenue, Rakuten is unlikely to step up its customer acquisition efforts and that is great news for incumbents but market expectations that mobile is value destructive are unlikely to change.

Edition: 150

- 09 December, 2022

Cybersecurity: Beat-and-raise being replaced by marginal-beat-and-cautious-outlook

Technology

Inflection Point Research, LLC

Economic woes impacting cybersecurity vendors - security projects are being delayed / cancelled at a rate not seen for several years. Following recent earnings, IPR questions whether Tenable will be able to sustain its surprisingly impressive momentum over the next couple quarters. Varonis’ lowered guidance is consistent with IPR’s belief that their offering has shifted to being a like-to-have technology. Qualys and Rapid7’s reliance on vulnerability management must be considered a negative. Meanwhile, Check Point's results underscore IRP's hypothesis that vendor consolidation trends are strong and becoming stronger.

Edition: 148

- 11 November, 2022

Materials

Earnings miss underscores Hamed Khorsand’s ongoing concerns - his short thesis is based upon slower demand for WDFC’s products and rising inventory levels. The group’s reliance on price increases will lead to further earnings misses as input costs remain elevated at a time when customers could experience sticker shock as further price hikes are rolled out this quarter. WDFC generated negative FCF in fiscal 2022 and there is no assurance FCF will turn positive in fiscal 2023. TP $88 (45% downside).

Edition: 147

- 28 October, 2022

Jio (RELIANCE IN) India

Communications

It is rare for a single company to be able to change the direction of an industry globally, but New Street thinks that is what happened at Reliance Industries AGM where Mukesh Ambani, the Chairman of RIL and founder of Reliance Jio announced a target of 100m 5G FWA subscribers in India in coming years. For context, New Street estimates there are currently around 2-3m FWA subscribers globally. Jio’s announcement on its own therefore turbocharges the entire FWA industry. FWA in EM today is analogous to 2G mobile in 2000, with outsized returns likely given modest market expectations and strong underlying demand.

Edition: 144

- 16 September, 2022

Communications

High conviction mis-valuation opportunity only emphasised by Warren Buffet's increased investment in Paramount Global - Robert Sassoon argues Netflix’s woes are company specific (reliance on streaming subscriptions has simply laid bare its vulnerabilities). By contrast, WBD, PARA and Disney have diversified revenue models, backed up with high quality content libraries. WBD’s debt burden is also less onerous than it appears (very attractive fixed rate terms and interest payments will be dwarfed by FCF generation prior to the first repayment dates in 2024). Attributing a PARA-like value multiple to WBD's consensus 2023 EBITDA offers 80%+ upside.

Edition: 136

- 27 May, 2022

Poor EM performance

EMs are effectively short dollars, directly via USD borrowings and/or indirectly via a reliance on commodities. Given the commodity rally, EM performance has been remarkably poor. Brian McCarthy doesn’t see much improvement ahead and recommends long S&P vs EEM - the trade has moved a lot recently but still has plenty more room to run!

Edition: 126

- 07 January, 2022

Lukoil (LKOH RM) & Reliance Industries (RIL IN) India

Energy

Both stocks already have an investor base among both EM Aggressive Growth and Growth funds, whilst also appealing to Value investors. As such, Copley would expect both to be on the shortlist of the many underweights and non-investors looking to ramp up allocations in the Energy sector.

Edition: 121

- 15 October, 2021

German DAX: Heavily owned and vulnerable

The increasing reliance on equities in the last couple of months has been unstoppable, but the equity market’s assumption that the Fed’s hawkish pivot was a ‘good tightening’ worries Julian Brigden. Right now, the charts are ugly. In particular, he mentions that DAX is heavily owned and vulnerable to Europe’s premature reopening. Julian recommends selling half a risk of unit here (see graph) with a stop above the all-time highs of 15,850. Add the rest on a move below 14,800 with a trailing stop. The initial target is 13,100 and then 12,000.

Edition: 115

- 23 July, 2021