Fortnightly Publication Highlighting Latest Insights From IRF Providers

Company Research

Lifco (LIFCOB SS) Sweden

Industrials

Karl Redin (Subsidiary CEO) purchased 26,350 shares at SEK 381, spending €920k. This is his eighth purchase and over 10x what he has spent on prior buys; the most recent was in Jul at SEK 367. The purchase occurred on the same day as the stock rose sharply after reporting Q3 earnings. This is an unusual buy, into unusual strength. Martin Linder (Subsidiary Head) also recently purchased shares spending €190k - a large purchase for him. Smart Insider has had a positive rank on this stock since early last year, based on buying from Per Waldemarson (CEO), Anna Hallberg (Director) and Martin Linder (Senior Officer). The stock has moved higher and insider buying has continued. Waldemarson made his most significant purchase in Jul, spending €1.3m and then spent an additional €300k in Sep. This is now the fourth time Smart Insider has renewed their +1 rank since Apr 24.

Edition: 223

- 31 October, 2025

Lundbergforetagen (LUNDB SS) Sweden

Industrials

Sofia Frandberg (Non-Executive since Apr 23) bought 4,000 shares at SEK 474.96, spending €173,000 and doubling her holdings. This is her first purchase since joining the board in Dec 23. Smart Insider ranked this stock +N on Sep 1st based on a €110,000 purchase from Bo Selling (Chairman, joined 2020) at SEK 481. It was a 50% increase in his holdings and his second purchase. His first was in Aug 23 at SEK 448, was part of a +N rank at that time, and proved timely. Now with two interesting purchases, Smart Insider are upgrading the stock further, from +N to +1 (highest rating).

Edition: 219

- 05 September, 2025

EQT (EQT SS) Sweden

Financials

Fighting Financials reiterates their short thesis on EQT and lowers their TP to SEK205 (~30% downside). EQT continues to lose market share, growing FAUM at +7.8% in 1Q25, materially below sector peers. The firm faces structural headwinds - sticky interest rates are reducing prospective IRRs and volatile markets are preventing easy exit opportunities, while LPs also remain overexposed to private assets, making fundraising more difficult. Rising PE portfolio company defaults (especially in France) and increased distressed credit activity further underscore market stress. In this environment, Fighting Financials prefers the more adaptable alternatives specialists like Apollo and as geopolitical tensions rise, the case for investors hiding in the more “anti-fragile”, defensive financials becomes more compelling.

Edition: 214

- 27 June, 2025

H&M (HMB SS) Sweden

Consumer Discretionary

Q1 channel checks reveal weaker-than-expected SSS growth in Europe (+0.35% Y/Y vs. consensus of +2.65%). While 50% of surveyed store managers reported positive Y/Y revenue growth, driven by new seasonal collections and effective in-store promotions, 30% of stores experienced declines due to competitive pressures and adverse weather conditions, particularly in markets like the UK and Czech Republic. 40% of managers noted declining foot traffic as a headwind, particularly in Eastern and Northern Europe. Seasonal inventory challenges were also cited by 20% of respondents, affecting sales performance in some regions, especially in Switzerland and the UK.

Edition: 207

- 21 March, 2025

Husqvarna (HUSQB SS) Sweden

Consumer Discretionary

Another successful short idea from Alumbra Research - Husqvarna's share price declined by 36% while the company was on their Active List (Jun 23-Feb 25) having issued multiple profit warnings and cut its dividend by 67%. In their initiation report, they raised concern that excess inventories combined with intensifying competition in robotic lawnmowers may cause the company to have to slow down production and write down excess stock, thereby pressuring margins. Alumbra also raised concern that Husqvarna’s credit metrics did not meet the threshold to maintain the company’s investment grade credit rating and that this would put the dividend at risk.

Edition: 206

- 07 March, 2025

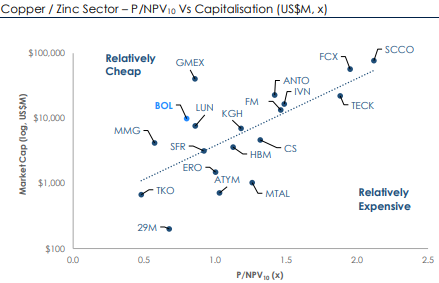

Boliden (BOL SS) Sweden

Materials

GMR continues to favour the outlook for zinc, where BOL is a large player (~0.5Mt/yr) and offers hard to find exposure. It is rare to find a company with several near-term events expected to support the business. These include a forecast recovery in Aitik grades; Tara moving back to full production rates; completion of the Odda expansion; Garpenberg throughput upside from permit revision; as well as plans to acquire Lundin’s Neves Corvo and Zinkgruvan mines. BOL is not expensive trading at 0.8x NPV10 and a prospective 2026E EV/EBITDA of 4.2x and FCF yield of 11%. Gearing is expected to peak in 2025 at ~22%.

Edition: 205

- 21 February, 2025

Evolution (EVO SS) Sweden

Consumer Discretionary

A leader in its industry with strong growth potential and >60% operating margins - regulatory hurdles and scale make it very difficult for operators to compete. The online casino industry has been growing at a 24% CAGR over the last 5 years but still only makes up 22% of the market. There is plenty of growth ahead and market share to win for online casino and EVO, and Ben Jones expects double digit growth to continue for the medium term. He believes EVO can generate far more cash than its current valuation and 12x forward P/E would suggest, and thinks it is a good buy at current levels.

Edition: 203

- 24 January, 2025

Evolution (EVO SS) Sweden

Consumer Discretionary

EVO was one of the ideas pitched at Revelare’s recent Investor Idea Event - the presenter's bear thesis focused on both fundamental and regulatory concerns. Growth is slowing, yet the multiple remains in the high teens. ~60% of the company’s revenues are derived from unregulated markets, but there is a movement afoot to regulate EVO and others like it in China and Japan, which is what is impacting growth. Furthermore, the presenter believes evidence exists that EVO has been receiving compensation from aggregators’ transactions to customers associated with illegal activity and that heavy restrictions will be placed on its business soon. 40%+ downside.

Edition: 201

- 13 December, 2024

Atlas Copco (ATCO SS) Sweden

Industrials

Kenneth Lagerborg (VP Financial Solutions, Group Treasurer) purchased €83,000 of Atlas Copco B shares at SEK159.05, increasing his stake by an estimated 75%. This is the largest of his 5 purchases, the highest price he has paid and his first buy for 4 years. His record to date has been good, according to the analysts at Smart Insider. He last bought stock at SEK91.95 in Dec 2020 and it is notable to see him now buying stock 4 years later at a price more than 70% higher. Furthermore, Vagner Da Silva Rego (CEO since 2024, joined 2014) also recently acquired shares. Smart Insider ranks the stock +1 (highest rating).

Edition: 198

- 01 November, 2024

Lifco (LIFCOB SS) Sweden

Industrials

Per Waldemarson (CEO since 2019, joined 2009) has made another purchase, spending €532k on August 2nd at SEK 307.30 and increasing his holdings by 3% to 758,500 shares. He has developed an excellent record when it comes to acquiring stock, based on 12 prior purchases, and qualifies as a "Smart Buyer". Smart Insider ranked the stock +1 on April 25th based primarily on a €444k purchase from him at SEK 258. The stock is up ~20% since that upgrade and it is interesting to see another large purchase from him.

Edition: 192

- 09 August, 2024

Swedish Orphan Biovitrum (SOBI SS) Sweden

Healthcare

Forensic Alpha’s proprietary machine intelligence performs a detailed forensic analysis of a company’s financial accounts. They continue to categorise SOBI as Very High Risk, with the number of red flags staying consistently high over the past 6 months. The areas of greatest concern are Accounting (including DPO hitting a new high in Q2, +24% Y/Y to 76 days) and Governance (the CEO’s bonus scheme is >50% weighted to revenue which is highly unusual and is likely to encourage a “growth at any cost” mentality; and concerns re. the independence of the Audit Committee members). Forensic Alpha has also identified issues with Earnings Quality, in particular relating to OCF.

Edition: 191

- 26 July, 2024

Securitas (SECUB SS) Sweden

Industrials

Following publication of the company's FY23 annual report, Iron Blue increases their SECUB score from 23/60 to 26/60 (now top quartile / fertile grounds for shorting). This reflects: 1) Sustained elevated stripped out costs. 2) Trade receivables days outstanding compressed at a decade low. 3) One third of debt scheduled to mature during FY24. 4) Sizeable fair value adjustments applied to Stanley Security’s balance sheet. 5) A new contingent liability concerning a US government investigation. 6) Another increase in the rate of employee injuries.

Edition: 191

- 26 July, 2024

Technology

Not only is SSNC trading well below precedent transactions and publicly traded comps, but with its proprietary AI technology its valuation also represents a sizeable discount to most of the other companies that are already capitalising on the AI megatrend. Boyar is also attracted to the firm’s significant recurring revenues, high margins, leading position in its field, less exposure to China, material inside ownership and strong FCF. They believe the earnings slowdown of 2022 and 2023 was a temporary lull in a longer-term growth story and therefore find the current valuation very compelling. Boyar’s intrinsic value estimate of $112 per share, offers ~80% upside.

Edition: 190

- 12 July, 2024

Truecaller (TRUEB SS) Sweden

Technology

Given the underlying weakness in the advertising business, management has been at pains to demonstrate growth from new revenue streams - in particular what they call “recurring revenues” based on selling premium subscriptions and selling to business customers. However, Forensic Alpha highlights a 25% increase in FY23 in Accounts Receivable from business customers with a sharp deterioration in the ageing profile of receivables. If a customer is overdue on their bills by 4 months, they are unlikely to represent a reliable or recurring revenue stream. As a result, they question whether the growth demonstrated by the company is entirely sustainable.

Edition: 186

- 17 May, 2024

Volvo Car (VOLCARB SS) Sweden

Industrials

Inventory of finished goods has grown by 33% y/y (vs. 21% growth in revenues). Based on Q4 COGS, the DSI of finished goods has risen from 33 days at the end of FY22 to 41 days at the end of FY23. This may not seem like a large increase, but in an industry focused on “Just-in-Time” manufacturing, this is a significant move up. Whether this additional product can easily be absorbed into the market will depend on your view of demand in 2024. In any case, Forensic Alpha recommends investors to continue tracking inventory in coming quarters.

Edition: 182

- 22 March, 2024

Elekta (EKTAB SS) Sweden

Healthcare

Median consensus Y3 revenue growth for Willis Welby’s mid cap MedTech coverage remains high at 7.3%, but financial productivity is not generally impressive and with a median implied to Y3 EBITM ratio of 145, expectations are almost all too high. However, EKTAB is one stock that does look particularly attractive. Willis Welby likes the product lines here as well as the financial productivity. And this is a standout cheap share (the implied to Y3 EBITM ratio is in the 50s - significantly below sector peers). Yes, investors should be wary of lumpy orders and delivery, but the positive share price reaction to disappointing numbers recently confirms just how nervous the market is. 50%+ upside.

Edition: 181

- 08 March, 2024

Hexagon (HEXAB SS) Sweden

Technology

Iron Blue initiates coverage on HEXAB with a score of 34/60, which is top decile (fertile ground for shorting). Key areas of accounting focus include 1) Revenue recognition. 2) Stripped out one-off costs, share payments and PPA amortisation. 3) R&D capitalisations and contingent consideration releases. 4) Acquisition disclosures and strategy of buying HEXAB distributors. Regarding governance, they note the auditor lead partner’s relationship with HEXAB’s largest shareholder network, a non-independent board and committees, 2 classes of shares, CEO / CFO internal succession, Greenbridge relationship and unclear CEO annual bonus payout metrics. Iron Blue also flags a fairly large number of areas where disclosure could be improved.

Edition: 179

- 09 February, 2024

Nyfosa (NYF SS) Sweden

Real Estate

Jens Engwall (Director since 2020, CEO 2018-2020) sells 67,743 shares at SEK 95.95. Smart Insider ranked this stock +1 (highest rating) on 2nd Jun 2023 based on purchases from Engwall as well as David Mindus (Director since 2023) around SEK 60 per share. The stock has risen over 50% and this change in sentiment is not surprising but forces them to downgrade the shares to neutral. Engwall's excellent record as both a timely buyer and seller continues to grow. His last sales were in Jan 2023 at SEK 88 and in Aug 2021 at SEK 142, both of which proved timely.

Edition: 177

- 12 January, 2024

Hexatronic (HTRO SS) Sweden

Technology

Vision’s Apr 23 short report on HTRO focused on exposure to boom-bust Tier 2/3 fibre builders, risk of slowdown in key markets and customers, early signs of small customer stress, balance sheet and channel inventory builds, and widespread signs of moderating telecom capex spend. Management updated sales guidance last week and the shares were down over 20%, pushing the total decline since initiation to over 50%. In the past month, Vision has initiated 3 new European shorts: a $20bn+ consumer staple, a $5bn+ consumer/industrial and a $2bn+ industrial.

Edition: 170

- 29 September, 2023

Thule (THULE SS) Sweden

Consumer Discretionary

Past the worse - David Scott first recommended the stock back in 2017, highlighting THULE's global leadership and as a great play on the new leisure age / ageing demographics. While it had a fantastic pandemic, the backwash caught it with excessive levels of high-priced inventory. However, David says the reported numbers are starting to show a classic “Positive Divergence”, where the group’s profits are suppressed by de-stocking but its cashflows are restored in the same process. He believes the deep correction in the share price is over.

Edition: 170

- 29 September, 2023

Sandvik (SAND SS) Sweden

Industrials

Following publication of its 2022 annual report, Iron Blue increase their SAND score to 24/60 from 22/60 to reflect higher stripped out one-off costs (restructuring and wind-down of Russian operations) and changed DB pension liabilities assumptions (higher discount rate, lower salary increase expectations vs. peers). Regarding governance, Iron Blue continues to flag that half of the board could be deemed non-independent and non-audit payments made to PwC are above average.

Edition: 168

- 01 September, 2023

Embracer (EMBRACB SS) Sweden

Communications

Contract Assets have been increasing much faster than sales - it seems strange that there should be such a sharp increase in the balance (from SEK 177m last year to SEK 790m) in the absence of a fundamental change in the business model. There is also an additional amount of SEK 1.2bn Accrued Income for which there is no description. The other interesting piece of disclosure in the accounts is around intangible assets, which highlights the sheer amount of internally generated development costs being capitalised in 2023 (SEK 12bn vs. SEK 3.7bn in 2022). For a company with an adjusted EBIT of SEK 6.4bn, this adjustment would turn the company from profit-making to heavily loss-making.

Edition: 166

- 04 August, 2023

Samhallsbyggnadsbolaget (SBBB SS) Sweden

Real Estate

Stuck in a doom loop - the Swedish real estate group has announced its intention to pause dividend payments on all share classes and cancel the SEK 2.6bn rights issue. The announcement followed S&P’s decision to downgrade SBB to sub-investment grade status. The company’s share price has plunged ~45% as a consequence. SBB (class B/D) equity holders will need to face any one of alternative scenarios ahead. All are fraught with risks.

Edition: 160

- 12 May, 2023

H&M (HMB SS) Sweden

Consumer Discretionary

Downgrades to Short / Sell based on findings from their recent surveys with store managers - Woozle’s H&M channel checks were much more negative than other names in their fashion coverage, many of whom outperformed targets over the Christmas period. Forecasts 1Q23 LFL sales growth of 0% y/y with 24% of respondents reporting that sales are falling below internal targets. This represents a meaningful deterioration in target meeting performances q/q as the latest product releases underwhelm customers. Furthermore, the number of customers trading down to cheaper ranges has increased considerably q/q as the cost-of-living crisis deepens.

Edition: 153

- 03 February, 2023

Swedish Match (SWMA SS) Sweden

Consumer Staples

Philip Morris International will accept all SWMA shares that have been tendered to it despite failing to achieve its 90% minimum stake threshold. PMI must still secure further shares in a voluntary transaction during a new offer period to achieve its goal of utilising compulsory purchases to acquire all remaining stakes in the Swedish company. After PMI raised its public offer in October, the total bid now amounts to SEK176bn ($15.8bn).

Edition: 148

- 11 November, 2022

Samhallsbyggnadsbolaget (SBBB SS) Sweden

Real Estate

Fallen Angel - affiliate-party transactions skews valuations. Green Street NAV is -25% vs. company-reported. Leverage and debt/EBITDA are amongst the highest across Green Street's coverage - rescue rights issue a distinct possibility in the medium term. Issues examined in their 37-page report include complex capital structure; unusual financial engineering; poor management track record; corporate governance issues; disclosure that lacks transparency and obfuscates the market’s ability to derive an accurate valuation.

Edition: 143

- 02 September, 2022

BillerudKorsnas (BILL SS) Sweden

Materials

Refreshed management team has taken bold action to enter North America (via Verso acquisition) and to exit underperforming assets - a leader in several niche markets, this packaging company has limited exposure to skyrocketing European energy prices, while its export options are enhanced with its low energy cost-base as well as the weaker euro. Q2 results were very strong, with sales growth across segments and a consolidated EBITDA margin of 20%. The outlook for Q3 is for price / mix to entirely offset input cost inflation. TP 190 SEK (45% upside).

Edition: 141

- 05 August, 2022

Technology

This defensive compounder offers compelling risk reward - trades at 11x EPS yet has grown EPS at a 25% CAGR for the last decade. With highly predictable earnings, SSNC is relatively well positioned into an economic downturn. Investors shouldn't focus on organic growth, earnings is driven by acquisitions and now is an opportune time with more targets available and at better prices than they have been for ages. TP $85, offers 50% upside, while Abacus Research's bearish scenario sees downside risk of only 12%.

Edition: 139

- 08 July, 2022

Swedish Match (SWMA SS) Sweden

Consumer Staples

A lollapalooza opportunity - where strong growth, pricing power, resilient market share and great allocation all come together. Post spin-off of the cigar business c.95% of EBIT will come from smoke free products, but it is the potential of the company’s ZYN pouch product in the US which Andrew Hollingworth is most excited about. His analysis looks to dispel investor concerns around rivals’ attempts to gain market share by undercutting ZYN's prices. Andrew has also built two models to look at what the future compounding of SWMA might look like - results in 12% and 19% annual returns over the next 7 years.

Edition: 128

- 04 February, 2022

Real Estate

Lars Goran Bäckvall (Non-Executive since 2010) purchases €520k of stock (between Nov 30th-Dec 6th), last paying SEK329 for the shares - Smart Insider had previously turned bullish on NP3 based on purchases Bäckvall made earlier this year at SEK213 and SEK115. He has a good record in the stock, consistently buying into strength. As Bäckvall continues to add at higher prices, Smart Insider are upgrading the stock further, from +N to +1 (highest rating).

Edition: 125

- 10 December, 2021

BICO (BICO SS) Sweden

Healthcare

Share price tanks on disappointing 3Q21 figures - has now fallen 40% since Paul Nagy’s report in early Oct’21. Paul highlighted increased investment in working capital, particularly receivables, that has led to lower CFFO while adjusted EBTIDA has continued to increase. In addition, FCF has been consistently negative. Paul also noted that the pace of acquisitions has increased materially since 2019, raising concerns over integration risk, especially since the market value of BICO implied substantial revenue growth expectations from these acquisitions.

Edition: 124

- 26 November, 2021

Electrolux (ELUXB SS) Sweden

Consumer Discretionary

Consensus estimates need to catch up with fundamentals - this Swedish home appliance manufacturer has benefitted from a Covid-driven pull forward in demand. However, with no replacement cycle for at least 5 years and management’s cost-cutting plan derailed by the fact that nearly all ELUXB’s input costs are at all-time highs, there is no chance that FY22 earnings end up being down only 5% (which follows estimates of an all-time high earnings level in FY21 of up ~40%).

Edition: 120

- 01 October, 2021

Kinnevik AB (KINVB SS) Sweden

Financials

In a major push to focus on its younger, high-growth, unlisted businesses, KINV continues to slim down its portfolio by Spinning off its entire 21% stake in Europe's largest online-only fashion retailer, Zalando. This is not its first Spinoff either - KINV’s last stake distribution (Millicom International Cellular) occurred in 2019 - the stock has since risen 118% (vs. 19% OMX Index). The Edge will analyse and advise on KINV and 8 other global Spinoffs in Q2 2021.

Edition: 108

- 16 April, 2021