Financials

KTC has moved past its key technical headwinds, with the share overhang from index removal and fears of further stake sales now largely reflected in valuation. Following a sharp sell-off after its removal from the MSCI Global Standard Index in mid-2025, the share price has stabilised, with PBV trading in a tight range. Attention is shifting to fundamentals, where KTC is showing clear improvement: ROE remains attractive and profit after loan-loss provisions as a share of average assets reached a seven-year high in 4Q25. This reflects tighter opex discipline and strengthening credit quality, with a declining cost of risk and a very low NPL ratio vs. Thai peers. Earnings momentum is also improving, with positive EPS revisions accelerating over recent months. KTC is Victor Galliano’s sole Buy-rated Thai financials name.

US: Favour the bears for short-run USD risks

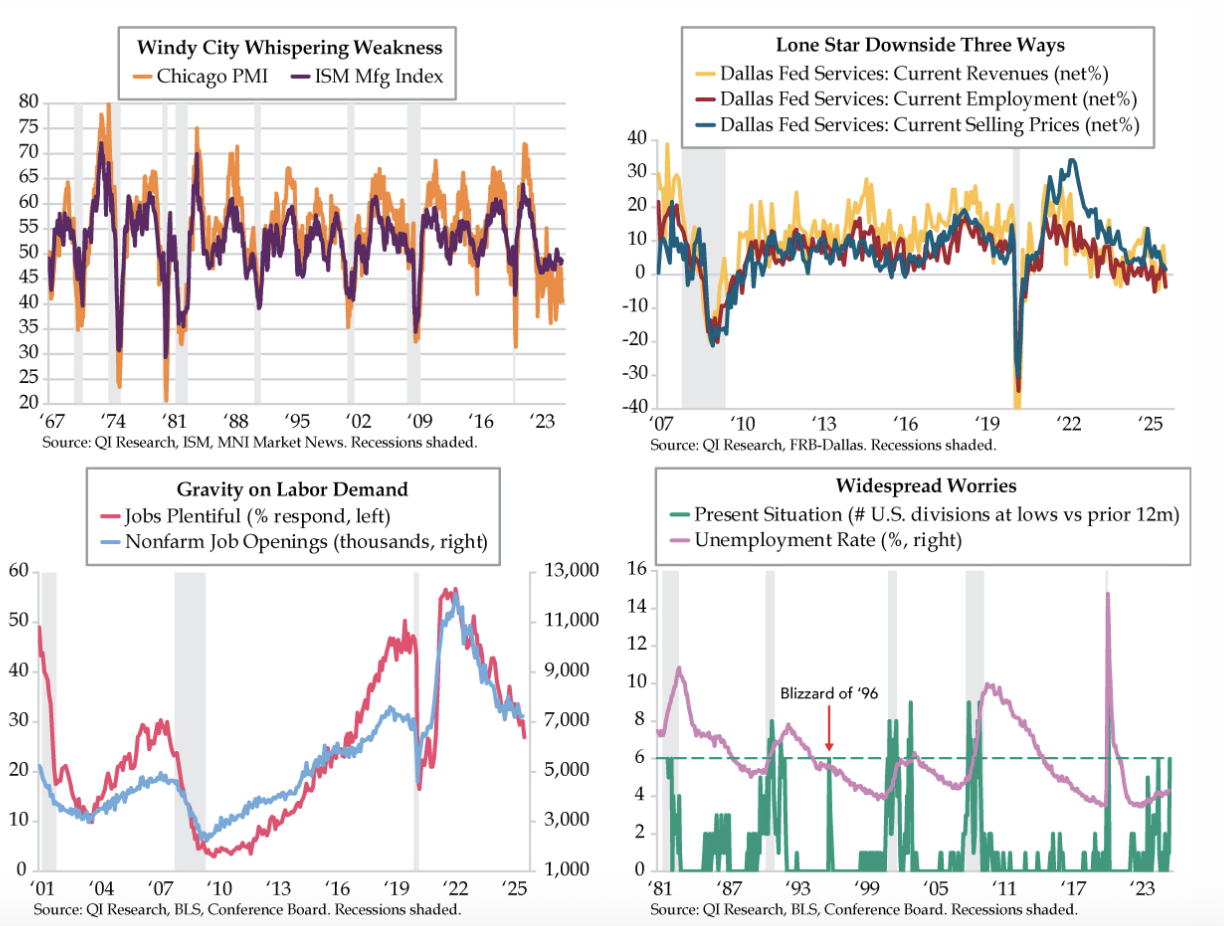

The Chicago manufacturing PMI fell from 41.5 to 40.6 in September, marking 22nd straight months of contraction. It’s streak in the red (below the 50-breakeven) has now extended to seven months. Whilst JOLTS nonfarm job openings surprised to the upside by rising 19,000 to 7.227m, only 9 of 18 industries increased. The Conference Board’s Jobs Plentiful gauge fell to a cycle low of 26.9%, calling into question job openings’ staying power. The forecasting community may have been too sanguine on September’s unemployment rate, after all. Should downside risks of growth, labour and inflation come to fruition, they would bolster the case for Fed easing in both October and December and could push the USD to new lows for the year.

Iron ore: Supply chain shocks and limited upside

SGX 62% Iron Ore futures initially jumped US$3.00/t early last week to seven-month highs of US$107.65/t CFR China, as a result of temporary supply shocks, including in Guinea and Brazil. Meanwhile, more countries have announced anti-dumping duties and tariffs on steel imports, although Atilla Widnell now estimates that they have reached critical mass and gone mainstream. Blocked supply chains will now cause Chinese Steel exports to flow back on itself, exacerbating the domestic supply-demand imbalance and sending Iron Ore futures back down to US$105.50/t CFR China. His medium-term outlook sees limited upside potential, and he maintains his outlook of US$95.70-105.14/t CFR China for Q3/2025.

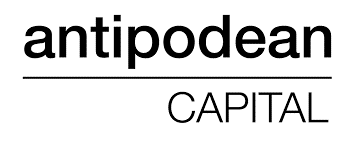

US stocks the most overvalued in 130 years

There is no escaping overvaluation if you are a multi-decade investor. The seven typical valuation measures that Craig Ferguson monitors are now at such an extreme that at nearly a 99th percentile rating the level of US equity market overvaluation is now the highest level seen since 1980 when records pretty much began. The signal is clear: long-term investors should be markedly UW stocks and largely out of US equity markets. This may be against consensus as the globe remains OW equities, but this is at a time when old sage Buffett is raising cash to $35 or more of his portfolio just as he did in the two most recent major overvaluation episodes in 1999 and 1966. Chart 2 shows that large global hedge funds are now nearly as short S&P VIX futures (or volatility) as they were in late 2021, just before the Nasdaq plunged by -38%. This won’t end well for equity markets.

Consumer Discretionary

New CFO Cath Smith has destroyed a total of (192%) alpha at seven different public companies since 2005. Her below-average ManagementTrack Rating of 3.0 is a downgrade to outgoing Rachel Ruggeri's MTR of 4.3 and will lower SBUX's C-Suite Rating despite CEO Brian Niccol's 8.1 MTR. Smith is classified as a: 1) "Capital Returner" Capital Allocator: 59% of career capital allocated towards Dividends and Buybacks. 2) High F.L.A.G. Risk Concern with a "Bad Compliance Record". 3) Inconsistent Guidance Forecaster: beats 35% of guidance given, misses 17%, in-line 48%. 4) Less Evasive on earnings call Q&A: during her Nordstrom tenure, JWN was ~27% evasive vs. SBUX's C-Suite ~33% evasive over the past five years.

The quiet signs of a market top

Bull markets rarely die with fireworks. Instead, remarks Jawad Mian, they fall in a slow, unravelling process. The reason is simple, not all sectors and styles peak at the same time. Looking at thirty bull-market tops since the mid-1920s, the average gap between the first sector peak and the final high has been seven months. A market can stop being a bull market long before the index starts to fall. Jawad recalls the strategy of Jesse Livermore in 1916, who noticed the signs of the market falling one after the other even as the bulls raged around him. A hundred years later, the game–and human nature—remains the same. Investors have been roaring bulls, but, like Livermore, they’re now watching for the shift. And it’s happening.

Potential NTT interest in SBI Sumishin is not far-fetched

Financials

SBI Sumishin Bank shares popped 17% on reports that NTT DOCOMO could be a buyer. Kirk Boodry thinks it is an easy story to believe. DOCOMO has already said it is looking at online banking options to solidify its fintech portfolio. And SBI Holdings essentially has two online banks as recently acquired and privatised SBI Shinsei Bank has a minimal offline footprint. It is encouraging that shares of NTT (rated Buy) were up on the news and while Kirk would like to believe that represents an endorsement of higher fintech exposure, it could also reflect hope that NTT may be steering clear of any involvement in a domestic Seven & i counterbid. The price tag could be somewhat steep with SBI Sumishin valued at ¥514bn, but NTT Group has the balance sheet to support a deal.

India: Adani indictment may prompt domestic and geopolitical ripples

The US Department of Justice has indicted Gautam Adani and seven associates for allegedly orchestrating a USD 265mn bribery scheme, raising concerns over transparency and compliance within India’s corporate sector. Domestically, opposition parties have renewed their criticism of cronyism involving the Adani Group, but political complexities make directly blaming the Bhartiya Janta Party-led government difficult. The indictment and its fallout threaten India’s global economic ambitions and could strain India-US relations, adding to existing tensions over trade and geopolitical alignments.

US: One week to go

With few days remaining until Election Day, the race for the presidency remains deadlocked. Vice President Harris’ lead stands at 1.3 points in 538’s national polling average, down 0.5 points from last week. Such surveys hold little predictive power at this point in the race. Instead, the numbers in the seven battleground states will determine the winner, and these numbers have held fairly steady over the last week. Harris leads by less than a point in polling averages of Michigan, Wisconsin, and Nevada while Trump leads by two points or less in Arizona, Georgia, and North Carolina. Pennsylvania is almost exactly tied. Much of Trump’s gains over the last month have come from his consolidation of undecided Republican voters. There are very few undecided voters remaining. While the presidential race remains little changed over the last few weeks, a number of Senate contests continue to tighten.

Materials

Revelare, who hosts ~40 idea events p.a. where 300+ investment ideas are sourced from institutional investment clients, recently spoke with an investor who is long AZE, the second largest pure play specialty chemical and food ingredient distributor globally after IMCD. The investor is bullish because he sees AZE exiting 2024 with positive total organic growth for the first time in seven quarters, leading to revenue / EBITA acceleration in 2025 and associated multiple expansion. He believes the stock can appreciate to a ~€30 stock price at the end of 2025 (55% upside). He also considers AZE to be a very strategic asset that may be acquired by private equity or Brenntag in the medium / long-term.

Online gaming bucks the trend of weak consumption

Communications

Report by

Blue Lotus Research Institute

Blue Lotus’s research suggests game and online video revenues are holding up better than movie theatres and that Tencent, NetEase and Bilibili’s 2Q24 NI will comfortably beat consensus forecasts. Over the past seven years, they have found an inverse relationship between online game and video with offline movie receipts. Gross billings of China’s gaming industry grew by 2.1% Y/Y in 1H24, reversing a decline since 2022. Online video grew by 1.4%. While smaller developers continue to struggle (economies of scale / large companies benefitting from AI investments and acquisitions), Blue Lotus raises their target prices for NetEase and Bilibili. Tencent remains their top pick.

MENA Chemicals: Street expectations are too demanding

Materials

During 2Q24, the average MENA petrochemical company’s share price declined 4.9%, outperforming the broader market by 1.2%. However, Hassan Ahmed’s analysis suggests that the Street’s estimates for Q2 are too demanding for the majority of these stocks. He expects tepid earnings growth Q/Q for most names and is meaningfully below consensus for Advanced Petrochemical Company and Industries Qatar. Similarly, he believes consensus estimates for FY24 are too optimistic. As a result, he lowers his 2024 earnings estimates for all seven MENA names that he covers and lowers his 2025 EPS estimates for six of the seven stocks.

A rewarding hunt for quality in EM equities

EM equities have not been impressive as of late, generating only a 6% return over the past five years and 13% over the past decade. However, for both EM and China, there are very wide disparities between the top and bottom deciles, with EM countries varying significantly in terms of income, culture, politics and more. EM markets also tend to be more segmented than their European counterparts, increasing the scope for monopolistic conditions. Take a look under the hood and you can find that the top performing stocks in EM and China have in fact outperformed the US; with the top seven performing equity stocks rising by double their S&P equivalents. The potential gains from alpha are substantially greater for EM equities, even if passive index investment strategies may not favour EM.

Utilities

TLNE announces the sale of its zero-carbon data centre campus in Pennsylvania to Amazon Web Services for $650m. The transaction value is more than Hamed Khorsand was expecting and includes a power purchase agreement that would create a minimum of $300m of adjusted EBITDA over the next seven years for TLNE. Moreover, the group has additional assets for sale that could further showcase the underlying value of TLNE's current stock price. Further liquidation of assets could lead to the company being sold in pieces as it would have a small operating footprint to remain public. The share price is up more than 30% since Hamed turned bullish earlier this year.

Consumer Discretionary

Report by

Pernas Research

A globally recognised luxury brand that has existed for over 168 years - BRBY finds itself in the later stages of its brand elevation journey and currently trades at ~12x 2023 earnings. The company has been in the midst of a seven-year transformation aimed at revamping its product offerings and pricing architecture. Although market sentiment is negative towards the stock due to temporary headwinds and brand elevation risks, taking a longer term outlook Pernas Research sees a minimum of 50% upside as BRBY has the right mix of heritage and strategy.

Technology Strategy: Finding short ideas

Investors appear increasingly nervous about the strong price momentum in software and semis. This performance has occurred with average volatility vs. history and with declining volatility over the last six months. Trivariate’s analysis reveals how changes in volatility impact subsequent performance. Specifically, it is software volatility that matters the most. Stocks with the biggest change in volatility Q/Q strongly underperform those with decreases in volatility among the group of tech stocks in the highest tertile of CSR (Trivariate has a proprietary seven-factor model to compute company-specific risk). Short ideas include AppFolio, Vertex, CleanSpark and Alkami.

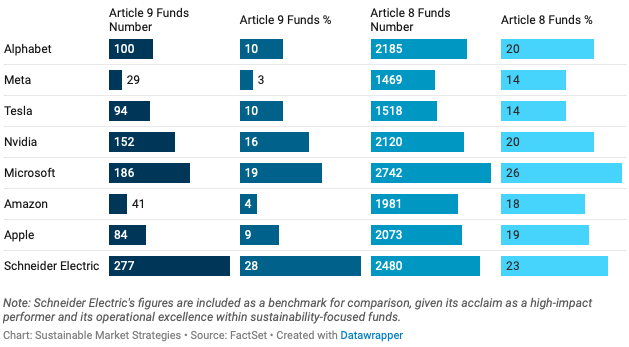

The Magnificent Seven

The impressive growth trajectory of the Mag 7 has been fuelled by AI and cloud computing, as money continues to chase their share prices higher despite pressure from rising bond yields on tech stocks’ long duration and their steep valuations compared to equity benchmarks. As pioneers in innovation, they are increasingly encountering legal challenges, but this has been intensifying as of late. The giants have a noteworthy presence in sustainable investment funds (see chart). However, the Sustainable Market Strategies team see the broad inclusion of these stocks as somewhat dubious. They tout Nvidia and Microsoft as the leaders, although the former is trading on a lot of AI hype and will fall short of growth expectations. Meanwhile, Amazon and Meta should be avoided as long positions in a sustainable strategy.

Markets and the Middle East crises

Following the terrorist attacks on Israel on October 7, U.S. bond prices and Israeli assets weakened while gold and oil rallied. Niall Ferguson analyses seven historical Middle Eastern conflicts involving Israel and finds that most of these conflicts had only limited effects on global markets—with the notable exception of the 1973 Yom Kippur War, which spiked oil prices and led to a crash in equity markets. If the conflict escalates further into a broader conflagration in the Middle East, history suggests there may be larger market moves. However, while Niall urges investors to consider the potential for asset price adjustments comparable with those of fifty years ago, he does not expect an equivalent energy price shock or stock market crash; many of the regional dynamics differ and thus the market reaction is unlikely to be so extreme.

Keeping track of Japan's Retail & Consumer markets

Key stories in this month's issue of JapanConsuming include: 1) Low cost apparel sales keep rising - Shimamura is adapting well despite the competition from platforms like Shein and Temu. 2) Zozo claims the global market for virtual clothes is growing rapidly - and prices suggest it’s probably correct. 3) The next big thing? Seven & I targets first SIP store by Feb. 4) Itochu (and Mizujin) have big plans for Eddie Bauer’s relaunch - hopes to create a major new lifestyle chain for 30s and 40s consumers. 5) Aeon’s new online food store, Green Beans, aims to change shopping habits. 6) Solving the 2024 logistics problem - companies are working hard to come up with solutions to reduce the impact of the new rules re. truck driver working hours.

MENA Chemicals: Earnings misses anticipated

Materials

Relatively weak MENA chemical sector share price performance has resulted from a compression in margins on the back of relatively weak product pricing and higher feedstock costs coupled with investor skittishness around the prospects of a recession across several geographies. Hassan Ahmed’s analysis suggests Street expectations for 3Q23 are too high and has lowered his 2023 and 2024 earnings estimates for all seven MENA names that he covers. SABIC is his top pick, as Hassan believes it offers the best blend of earnings resilience and below-sector average valuation.

Real insight on Japanese Consumer markets

Top stories from this month’s issue of JapanConsuming include: 1) Seven & I has finally sold Sogo Seibu - it will be pleased to have offloaded a loss-making format it never really understood, but at a cost, it will write off ¥90bn+ in loans. 2) Tsuruha is the latest retailer to come under attack from an activist investment fund. 3) ABC Mart expands its lead in footwear. 4) 3Coins, a variety store run by Pal Group, looks to have a strong future. 5) Frozen Foods becoming mainstream. 6) JapanConsuming’s FOCUS article discusses how the country is witnessing the emergence of a new elite group of department stores who are far ahead even of their big city peers.

Peru: Provisional stability carries democratic costs and faces July tests

Seven months into Boluarte's accidental presidency, a new power alignment has formed, bringing relative political calm but eroding democratic safeguards. Congress and the executive have entered a de facto co-existence pact to avoid early elections and secure impunity. However, stability remains fragile. Anti-government protests and a change in congressional leadership in July will test the power balance and Boluarte's political strength. Both Boluarte and Congress face extreme unpopularity. The upcoming protests and leadership election will determine their resilience and the potential for early elections.

Key stories from Japan's retail & consumer markets

Consumer Discretionary / Staples

Highlights from this month’s issue of JapanConsuming include: 1) The great divide: Isetan & Hankyu break records as regional stores close. 2) Rakuten’s Seiyu sell off will boost netsuper business. 3) Authentic Brands to open office in Japan’s “¥3trn brand paradise”. 4) Yaoko: 34 years of record profits. 5) Ecbeing nears ¥1trn in GTVs. 6) Big apparel revival: Onward up again, Sanyo Shokai finally makes a profit. 7) Seven & I CEO survives - just about. 8) Their 'FOCUS' article examines whether today’s ‘normal’ is the same as it was back in 2019: record levels of income, full to bursting savings accounts, alongside subtle signs of a falling propensity to save mean people are out spending again.

Technology

Seven insiders combined to purchase €5.1m worth of stock from April 26th-May 5th at prices ranging from €164-€185. The buyers include four directors, two senior divisional officers and the CEO. Smart Insider ranked this stock +1 on 15th Nov 2022, based on a similar cluster of buying at slightly higher prices (€170-€200). The stock traded as high as €273 in early Feb but has since declined steadily to its current level, below where they ranked it in Nov. It is encouraging to see another solid cluster of buying and so Smart Insider are renewing their +1 rank.

UK Risk Rankings

Paul Hollingworth sifts through ~300 UK companies to ascertain their financial risk. He incorporates seven different Risk Models and scores companies by each model to come up with an aggregate Score. Investors should not be chasing high risk or "a dash for trash" (as we saw in Jan) but should combine classical valuation assessment with low risk opportunities. Companies featured in the top quartile of low risk include Renishaw, Rightmove, Sylvania Platinum, AG Barr, Rotork and Wilmington. Investors should eschew companies such as Wizz Air, Aston Martin, Mitchells & Butlers, Rolls Royce and Ocado. Let alone small caps such as Kromek, Plant Health or Pressure Technologies.

Healthcare

PFE are attempting to move from their successful, but now outdated Prevnar 13 pneumococcal vaccine to Prevnar 20. However, paediatric data suggests it may be slow to achieving noninferiority to old Prevnar 13, and a lack of superiority on the extra seven varieties that Prevnar 20 is meant to prevent in children. Thus, Dr Amit Roy is concerned that it may struggle to position itself as better than already approved alternative MRK’s, Vaxneuvance. He expects most of the $4bn dollar paediatric pneumococcal vaccine market will go to MRK with only $1bn for PFE. Combined with better data in the $1bn adult market, Amit sees $1.6bn for Prevnar 20 overall.

Consumer Staples

Currently trading close to the historical peak FY+2 EV/OP and FY+2 EV/EBITDA, Oshadhi Kumarasiri thinks Seven & i has little to no room for valuation multiple expansion. Earnings also seem to have peaked after reaching an all-time high in the third

quarter. In addition, Oshadhi sees substantial downside risks to 7-Eleven US earnings estimates in the short to medium term with falling gasoline prices (3Q OP beat was mostly driven by an unexpected upside to the retail fuel margin, but this will correct over the next few quarters) and the yen appreciation. 40% downside.

Consumer Staples

Price hikes appeal to investors - Calbee's decision to raise prices across its product range has led to renewed interest among institutional investors for Japan’s largest snacks maker, having fallen out of favour for several years. In fact, after a seven-year fall, the stock is threatening to break its downtrend with the shares up ~37% in the past six months. While investors bet on earnings growth over the long term through regular price revisions, Oshadhi Kumarasiri thinks there could also be short and medium-term gains as operating profit growth turns positive after many years.

Consumer Discretionary

Pre-IPO analysis - Chinese EV maker aims to raise ~US$1.5bn via Hong Kong listing. Leapmotor's revenue has grown by 26.7x (FY19-21) and it aims to launch seven more models over the next few years which should help to prop up growth. However, its linked entity, Dahua Technology, is on US’s entity list which will ward off some investors. In addition, it needs a whole lot of cash to scale up and appears to be lagging its larger peers. In a previous note Aequitas discussed the company’s past performance and PHIP updates. In their latest piece they undertake a peer comparison.

Keep track of Japan's Retail & Consumer markets

JC’s monthly report offers subscribers an easy, fast way to keep up with key trends, deals, marketing ideas, competitor strategies, and all the latest store and consumer data. Top stories from this month's edition include: 1) Seven & I sells Oshman’s to ABC Mart - clear sign that it is beginning to tackle its legacy operations. 2) Aeon Mall looks to experiences to get people into its properties. 3) Workman to open in Ginza; paves way for next big expansion. 4) Omnichannel accelerates in fashion: 40% of eCommerce sales from staff blogging. 5) Subscription retailing goes mainstream.

Consumer Discretionary

Report by

Holland Advisors

HO

The Walmart of the UK pub sector and Tim Martin is its Sam Walton - the power of JDW's financial model is being underestimated according to Andrew Hollingworth. In his latest report, Andrew sets out two scenarios with only one difference between them: the first rebuilds EBIT margins to 10% by the end of the seven-year forecast period. The second assumes no operational gearing at all. The forecasts they produce are for investor IRRs over the next 7 years of 25% p.a. or 16% p.a. JDW is set to offer investors great long-term compounding.

Weakness in Taiwan is concerning

Be wary of Taiwan, claims John Karle. The Taiwan TWSE index has registered seven consecutive lower daily closes coming off a one year high (published Aug 13th) – History warns us that this will be problematic, and investors should expect further volatility over the short-term. Even more crucially, the index is at the very peak of Nautilus’ long-term cycle analysis, reaching the highest point since the 90s.

Industrials Rotation

Industrials

After a multi-year decline, active Asia Ex-Japan fund managers are growing increasingly bullish on the Industrials sector. It is now the 5th most widely held sector, but average weights are fraction of the dominant quartet of IT, Financials, Consumer Discretionary and Communication Services. Steven Copley highlights seven companies likely to feature in the investment decisions of fund managers in the region should the rotation into Industrials continue. These include NARI Technology, Sungrow Power Supply, Voltas, Country Garden Services and CK Hutchison.