Fortnightly Publication Highlighting Latest Insights From IRF Providers

Company Research

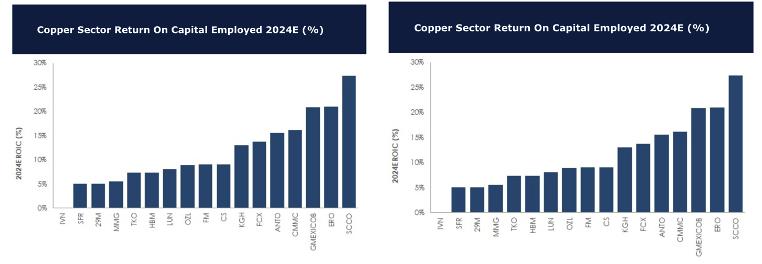

Returns on capital: Copper vs Gold

For 2024, David Radclyffe forecasts copper to enjoy an average ROCE of 11.1%. The standout is Southern Copper Corp, helped by some very low cost and long-lived assets. Relatively new to the market Ero Copper Corp does well, while at the lower end sit Ivanhoe Mines and Sandfire Resources. When it comes to gold, the forecasted average ROCE for 2024 is at 8.3%, with Gold Fields coming out on top and Lundin Gold close behind. The copper sector as a whole continues to generate better real returns on capital than the gold sector, with gold miners continuing to suffer from shorter mine lives and a commitment to M&A to create growth.

Edition: 155

- 03 March, 2023

Miners forced to become green power companies?

David Radclyffe reviews how mines with little access to green electricity will need to build capacity themselves or via a third party in order to meet emissions targets. Some will come under increasing scrutiny; Rio Tinto, South32, Southern Copper Corp, Freeport-McMoRan and Anglo American could all face increased capital/opex exposure. The potential capital costs associated with self-generation are massive, so investors should keep a close eye for opportunities present in the partial or full outsourcing of infrastructure.

Edition: 122

- 29 October, 2021