Fortnightly Publication Highlighting Latest Insights From IRF Providers

Company Research

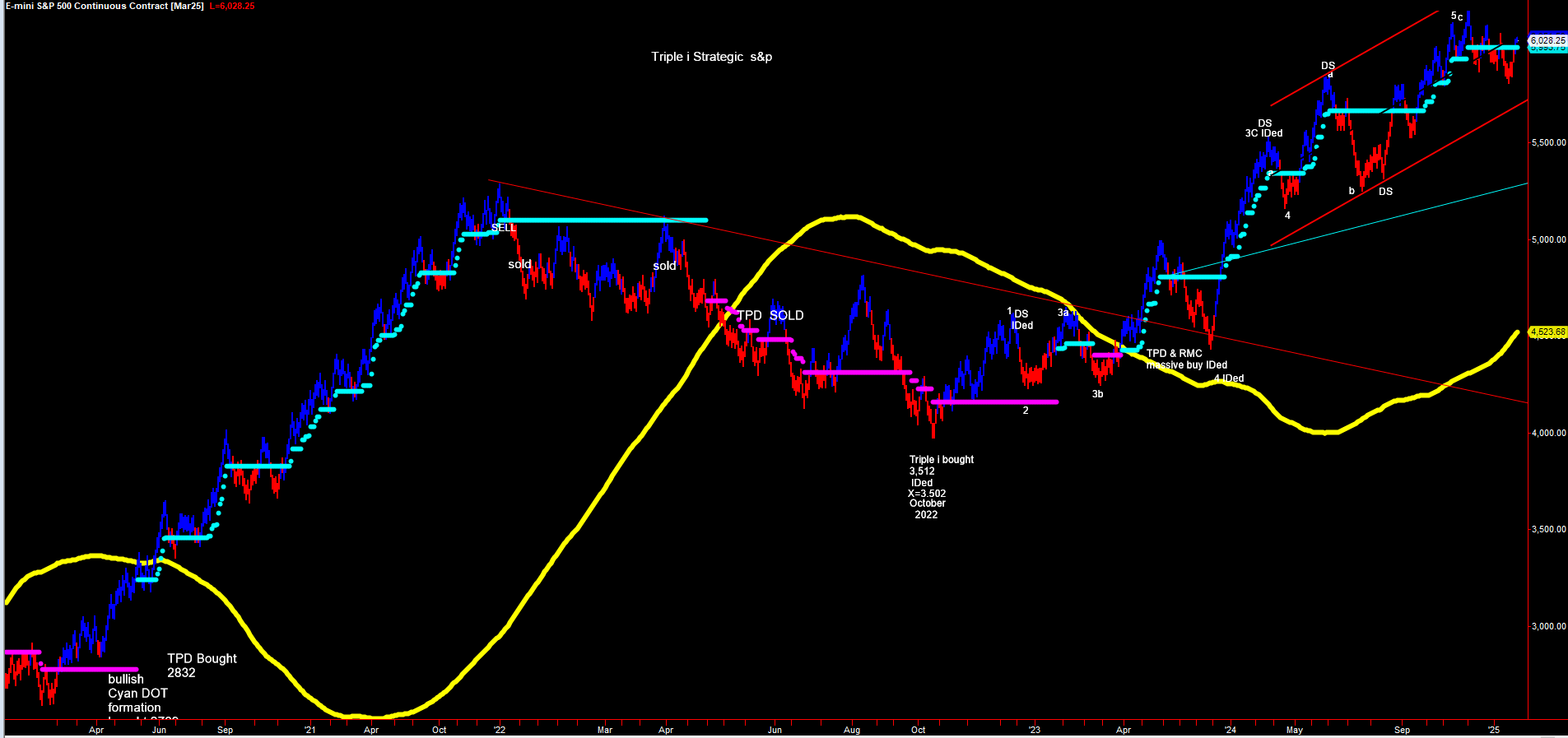

Identifying S&P & Dow Jones volatility trade dynamics

The Fed’s insertion of liquidity to effectuate appreciation since 2020 showcased Triple i’s adroit trade dynamics, identifying trades which are undetectable to traditional methodologies, captured the precise Covid low pre delivering 2194 to square short exposures from 3300 handle. A psychologically bifurcated market which tried to sell at the lows incessantly, up to 3,000, while Triple i clients were provided a major buy signal once 2,350 was traversed, targeting ONLY a break above TPD catalyst 4,458 for continuation was also pre delivered while trading on the lower half of the 3500 handle. What distinguishes Triple i’s exact trade identification from multiple volatility permutations created by market behaviour, is due to the forward-looking volatility calculus provided visually real time to their clients.

Edition: 203

- 24 January, 2025

Austria: Turning (far) right?

Austria may be headed for a government under Herbert Kickl, the leader of the far-right FPÖ. It may be more than three months after the elections, but coalition talks between the conservative ÖVP, the Social Democrats, and the liberal Neos collapsed. Karl Nehammer, former ÖVP chancellor and the lead figure in those talks, resigned. His attempt to keep the FPÖ out of power, even if they won the elections, backfired. Wolfgang Münchau says that there are now two options moving forward: a coalition government between the FPÖ and the ÖVP as a junior partner or new elections. The FPÖ has been rising in the polls to 35% in December and are likely to benefit even further from the current political crisis. So, everyone else apart from the FPÖ has an interest in avoiding elections. After 98 days, Austria is back to square one.

Edition: 202

- 10 January, 2025

The warning sign in US labour

The latest Non-Farm Payroll report showed the US keeps adding jobs at a sustained pace, but Alfonso Peccatiello says this feels weird. It’s hard to square how the US job market can remain so resilient even as rates remain high for long. One of the most reliable long-term indicators of job market weakness is the Sahm Rule: when the 3-month moving average of the unemployment rate exceeds its 12-month low by 0.5%, the recession is here. The latest reading says 0.37%, often cited by bears as a warning sign. If the underlying labour market weakness gets more evident, the Fed needs to react fast. From a long-term asset allocation perspective, one can still remain invested in risk assets here but must be vigilant of surfacing labour market weakness and the Fed reaction function. If they play ball, buying bonds when 10-year Treasuries approach 4.6-4.7% offers great risk/reward.

Edition: 188

- 14 June, 2024

Consumer Discretionary

The stock has meaningfully outperformed local peers, the Hang Seng index, and broader Emerging Markets index in the last 6 months, when Wium Malan argued that VIPS’ valuation multiples had de-rated to levels where it was an attractive takeover target. Trades on a paltry 3.8x forward PE ratio (ex-cash) and looking purely from an infrastructure perspective, trades at a c.50% discount to JD.com on a per square metre basis. Given the recent rebound in Chinese retail / apparel sales growth and the pessimistic expectations from the sell-side, Wium expects the current earnings upgrade cycle to continue.

Edition: 146

- 14 October, 2022

Consumer Staples

How NOT to run a discount retailer - management squanders its pandemic opportunity to capture incremental customers. John Zolidis sees three problems: 1) Chronic underinvestment in infrastructure. This explains the difficulty of dealing with supply chain challenges. 2) Must stop raising prices to protect “merchandise margins”. The value is not there, and that’s why traffic and loyalty members per store are falling. 3) Should staff its stores, rather than using labour as a lever to offset negative comps. Reflecting the reduced labour and service, S,G&A per avg. square foot has not increased in four years, in contrast to industry and competitor trends.

Edition: 132

- 01 April, 2022

UK Industrial REITS: Urban winners

Real Estate

A flurry of inner London transactions in the past four months all points to increasing capital values - marking to where assets could trade today (rather than a valuer’s snail pace recognition of change) results in notable increases to spot NAVs. Buyers are pricing in significant, yet realistic, levels of rent growth (25%+) over the medium-term. As such, one eye should be kept on capital values per square foot, which remains at palatable levels when considering alternative uses such as residential, suburban office or even grocery-led retail. Key recommendation changes include upgrading Segro to Buy.

Edition: 129

- 18 February, 2022

Square Pharmaceuticals (SQUARE BD) Bangladesh

Healthcare

Market leader in the Bangladesh Pharma industry with ~17% market share. It has RoIC of ~40%, net margins above 30% and net cash/M.Cap of 25%. Trades on a forward PE of 10.7x. Square had seen a major derating in its multiple over the last 5 years. However, there has been a clear turnaround with double digit top line growth from 2020-21, which is continuing with latest quarter revenue and EPS growth of 15% and 21% respectively. With the onset of Omicron, Edge Research are expecting a further boost to revenue. Meanwhile, the company has also resolved the management gaps and removed all loans to sister companies. Square looks poised for a multi-year rally.

Edition: 128

- 04 February, 2022

Korean Telcos: Lessons from Japan

Communications

Something is changing in the Korean Telco landscape - buybacks from SK Telecom and KT Corp, increased stock ownership by employees and management, an increased focus on profitability / returns, and more progressive dividend policies all point to a better environment for shareholders going forward. At the same time, post the spin out of SK Square, SKT, which has not historically been a rapid growth company, is now guiding to 50% revenue growth over the next 5 years! Taken together Korean Telcos which have historically traded at a substantial discount to the rest of the EM telecom sector look set to re-rate materially.

Edition: 126

- 07 January, 2022

Technology

Galliano's Financials Research

Victor Galliano questions the eye-watering multiple being paid following news that SQ plans to acquire Australian fintech company Afterpay for $29bn - as SQ enters the BNPL arena, credit risk will need to be managed very carefully, especially in a business experiencing rapid growth. Investors should also expect increased regulatory scrutiny and oversight, especially from financial regulators in the US, who may want to constrain the pace of growth in consumer instalment credit sales. The clear winners are Afterpay shareholders who Victor believes should cash in their SQ shares post exchange.

Edition: 117

- 20 August, 2021

Ceridian (CDAY)

Technology

Underappreciated opportunity - CDAY’s Dayforce Wallet is the company’s first foray into a very different segment of the fintech ecosystem: digital wallets and earned wage access solutions. In this industry primer, Veritas assess the competitive landscape and compare CDAY's offering to products launched by Apple, Alphabet, PayPal, Square, Mastercard, Visa, Tencent and Alibaba. Veritas think the long-term gains of developing a fintech ecosystem are incredibly attractive and CDAY’s unique distribution advantage will help carve itself a piece of the market. Estimates that the module can generate ~US$220m of annual net earnings and be worth US$19 per share.

Edition: 114

- 09 July, 2021