Fortnightly Publication Highlighting Latest Insights From IRF Providers

Company Research

Consumer Discretionary

John Zolidis turns bearish on SBUX heading into Q4. He views domestic store closings and a potential China exit as signs that SBUX is no longer a growth business and valuation should contract to reflect this. Furthermore, traffic remains negative and estimates are too high more than one year after Brian Niccol started as CEO. Last quarter was good for Quo Vadis’ calls with their average Long idea falling 1% compared to an average decline in their Short ideas of 15%. Their (Retail & Restaurants) universe fell 9%, reinforcing that Quo Vadis' approach is identifying winners and losers and creating alpha. Q3 was the fourth consecutive quarter with longs outpacing short ideas.

Edition: 221

- 03 October, 2025

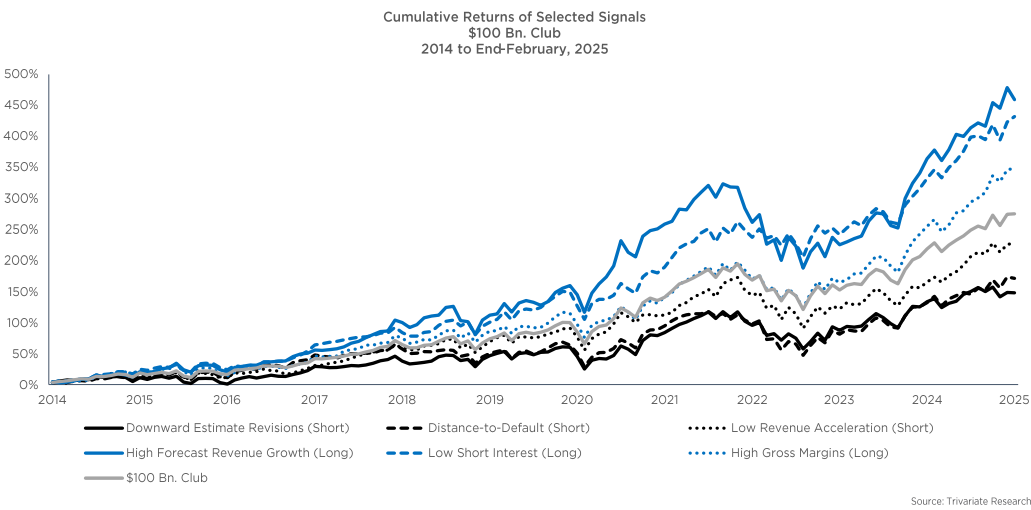

Which stocks >$100bn m/cap are buys now?

With investors searching for value in the current market sell-off and likely looking to buy names among the safer, larger cap universe, Trivariate has assessed the performance of several metrics within the stocks >$100bn m/cap to see if they could systematically pick winners from losers. The best performing signal over the last 10 years, was buying the companies in the top third of forecasted revenue growth, while the second best was buying the one-third of companies with the lowest short interest. The worst performing signals were those in the highest third of leverage and stock volatility (distance-to-default) and those with the worst third of downward earnings revisions. Current long ideas from Trivariate’s $100bn Club Framework include all the Mag 7 (except Tesla), as well as Eli Lilly, Visa and UnitedHealth. Shorts include Goldman Sachs, PepsiCo, Caterpillar and Starbucks.

Edition: 207

- 21 March, 2025

Consumer Discretionary

New CFO Cath Smith has destroyed a total of (192%) alpha at seven different public companies since 2005. Her below-average ManagementTrack Rating of 3.0 is a downgrade to outgoing Rachel Ruggeri's MTR of 4.3 and will lower SBUX's C-Suite Rating despite CEO Brian Niccol's 8.1 MTR. Smith is classified as a: 1) "Capital Returner" Capital Allocator: 59% of career capital allocated towards Dividends and Buybacks. 2) High F.L.A.G. Risk Concern with a "Bad Compliance Record". 3) Inconsistent Guidance Forecaster: beats 35% of guidance given, misses 17%, in-line 48%. 4) Less Evasive on earnings call Q&A: during her Nordstrom tenure, JWN was ~27% evasive vs. SBUX's C-Suite ~33% evasive over the past five years.

Edition: 206

- 07 March, 2025

Multinationals in China: Europe vs. US

Much of what 86Research has heard this earnings season confirms insights they have previously flagged re. the China market, including the strength of Sam's Club, the robust expansion of travel demand and the competitive challenges facing Starbucks and iPhone. More remarkable, however, are the latest moves by several European multinationals, such as Volvo and LVMH, which appear committed to cross-border cooperation in areas relatively insulated from geopolitical pressures. Beneath the broader, probably over-generalised narrative of a multinational exodus, a more nuanced observation points to a potential structural shift in the origins of China-bound investments, with European firms advancing at the expense of their US counterparts.

Edition: 200

- 29 November, 2024

Bear’s Den Idea Forum

Common themes from MYST's latest buy-side event focused on cyclicals / companies trading at peak, potential “Trump losers” and companies facing inventory headwinds. The most compelling ideas include:

Bentley Systems (BSY) - Mining / renewables weakness to curb ARR growth; Trump could threaten IIJA tailwind.

Powell Industries (POWL) - Absurdly valued, highly cyclical business with peaking fundamentals & large insider selling.

Starbucks (SBUX) - Litany of earnings headwinds not fully appreciated under “abysmal” new CEO.

Toro (TTC) - Recent FY24 guidance a “Hail Mary” amid rising DSO’s / Inventory Days.

Edition: 182

- 22 March, 2024

Consumer Discretionary

Decision to hire Laxman Narasimhan as the new CEO could be a mistake - Paragon’s previous diligence report includes interviews with 18 former colleagues, all of whom found him to be arrogant, self-centred, insecure, and abrasive. As a result, he destroys company culture and is not well-liked. Furthermore, he lacks the ability to execute on a long-term strategy. At Reckitt he underperformed as CEO (destroyed 17% alpha for shareholders), performance they believe stems from a "lack of deep understanding of the business”. Paragon will be supplementing their previous work on Narasimhan with interviews with former colleagues at Reckitt.

Edition: 144

- 16 September, 2022

DoorDash (DASH)

Communications

Clear case to be made that DASH can rise from an upstart restaurant ordering/delivery company into an empire spanning Restaurants, Convenience, Grocery and other CPG categories. Hedgeye believe that the company can easily exceed $70bn in Marketplace GOV in FY24, up over 80% from $37bn in FY21. Their bullish thesis also includes DASH’s opportunity to monetise DashPass (compares it to Amazon Prime/Starbucks Rewards) and its potential to capture substantial market share in the digital advertising space.

Edition: 113

- 25 June, 2021