Fortnightly Publication Highlighting Latest Insights From IRF Providers

Company Research

Technology

Three weeks ago, with SMCI trading at $21, Lynx rolled out a $45 price target and opined that the odds of delisting were not as high as many thought. Their view was based on belief that the company held a uniquely critical position in the all-important business of installing AI infrastructure. They also argued that the likelihood of Dell taking market share was overblown and called for the run-up in the stock to fade. For the next couple of months, the event-driven volatility is likely to wind down while investors turn their focus to SMCI’s fundamentals. And that is reason enough for Lynx to raise their TP to $60 (based on 20x their FY25 EPS estimate of $2.93).

Edition: 201

- 13 December, 2024

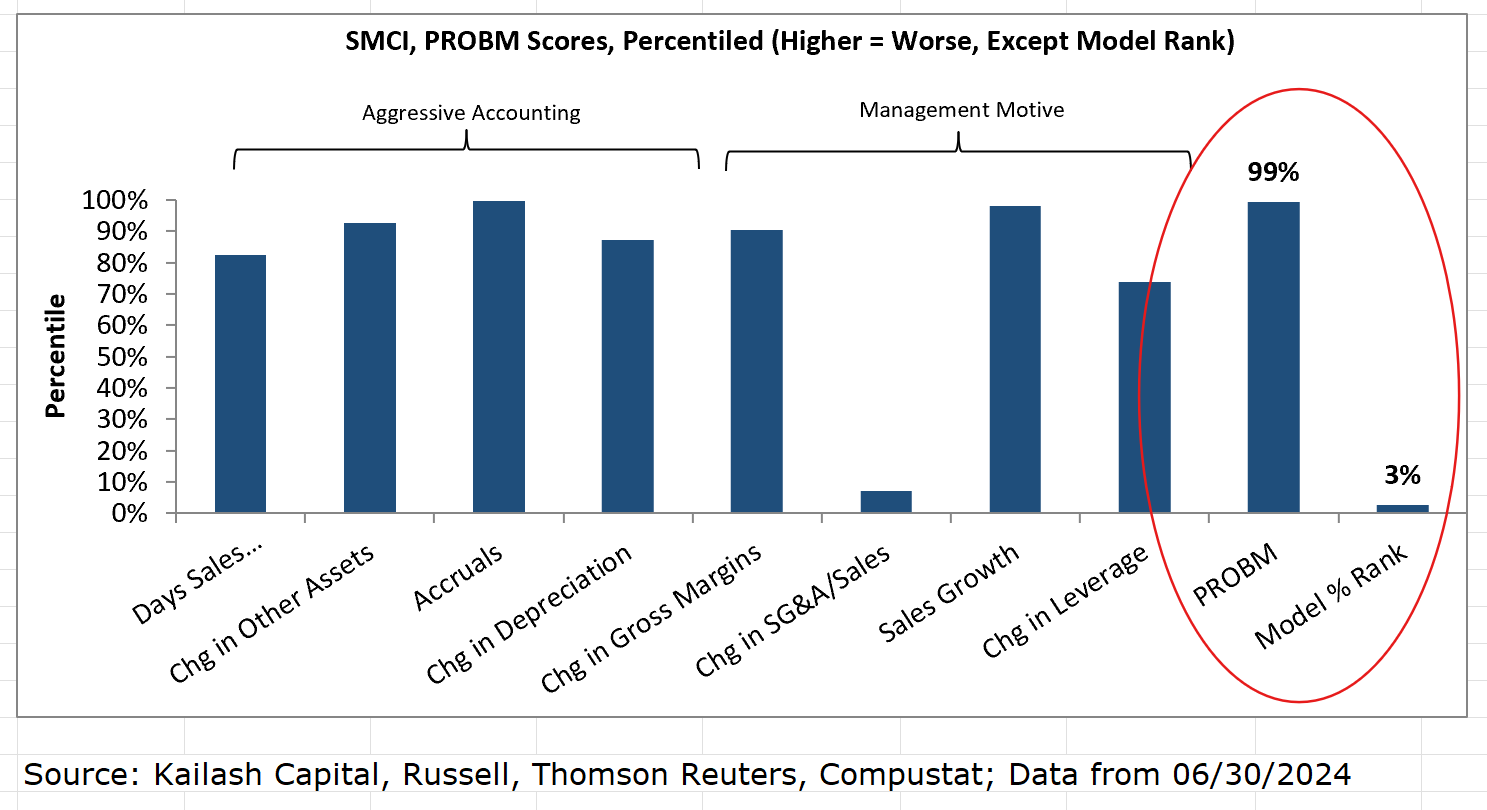

A systematic approach to identifying potential earnings manipulators like SMCI

SMCI shares fell nearly 20% after the company delayed the filing of its annual report and Hindenburg Research alleged “fresh evidence of accounting manipulation”. Interestingly, SMCI features in KCR’s S&P 500 Earnings Manipulator list, which includes stocks in 1) the worst quintile based on academia’s PROBM formula and 2) the bottom 20% of KCR’s ranking methodology. Other companies flagged include Advanced Micro Devices, Tesla, and Xylem, with Block and Emerson Electric added last month. Over the past 14 years, KCR’s Research Short Portfolios have been valuable for spotting potential risk flags and generating short ideas. To access the return summary for these portfolios click here.

Edition: 194

- 06 September, 2024

Technology

SMCI's share price has risen over 300% since AceCamp turned bullish in 2Q23. However, their recent analysis suggests a potential inflection point in the company's trajectory. Intensified H100 server pricing competition could lead SMCI non-GAAP EPS to grow only 17%/4% Y/Y to $27.3/$28.3 in FY24/FY25, 30-40% below consensus estimates. Considering margin pressure and growth headwinds, a contraction from the current elevated multiple to a 10-15x FY25 PE range appears increasingly likely, implying over 50% downside.

Edition: 189

- 28 June, 2024

Should we listen to the central banks?

Investors are growing tired of central bank speak, which James Aitken claims to be performative exactitude peddled as transparency. If you’re in doubt about what’s happening in the world, listen instead to what your best-run portfolio companies are telling you and cross-reference with what you are actually observing. The recent price action – bonds falling more than stocks – could be interpreted as suggesting that despite rising long-end yields, markets are comfortable with strong, perhaps stronger growth to come. That will ensure the best-run companies protect moats & continue to grow earnings in a satisfactory way. Assuming nominal GDP continues to rumble along around 5-6%, bond yields should be higher, with 10yr treasuries soon yielding 5% or more, which will act as headwinds to some stocks that have seen the biggest rallies, such as Super Micro Computer Inc and Nvidia, with marginally profitable, levered businesses struggling. You cannot, however, be out of stocks let alone net bearish: you just need to own different things.

Edition: 184

- 19 April, 2024