Fortnightly Publication Highlighting Latest Insights From IRF Providers

Company Research

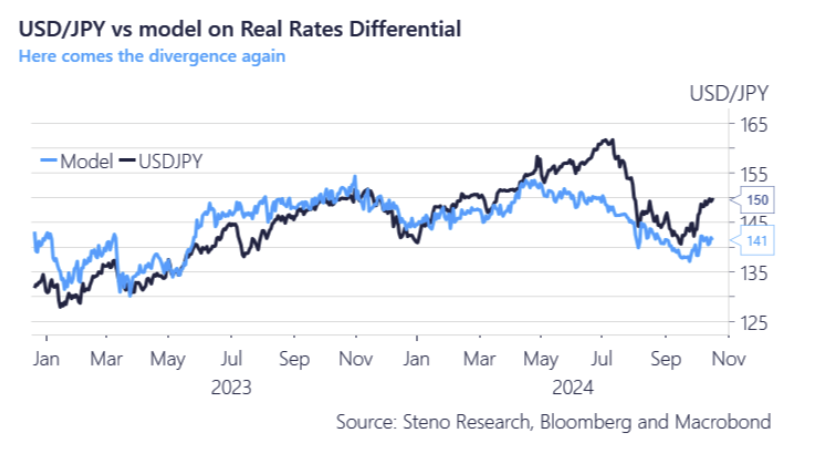

USD/JPY: Trading far north of fair values

USD/JPY has seen significant moves over the past few weeks, initially in tandem with USD rates being priced higher. However, Andreas Steno believes that the moves over the past couple of days have been truly out of sync with fundamentals and his real-rate differential model still points towards fair value being around 140-141. The moves he is seeing rhyme decently with the narrative in late 2022 and 2023, where no news = buy, and markets are likely celebrating that USD real rates have started to flatline. USDJPY still offers very decent carry, so as long as there are no visible moves in real rate spreads, there might be idiosyncratic reasons to expect USDJPY to go higher.

Edition: 197

- 18 October, 2024

Healthcare

PODD is on the cusp of a new product cycle for Omnipod 5 for diabetes 2 patients which will drive upside to 2H24 and 2025 consensus estimates. Abacus also argues the market’s GLP-1 fears are overplayed (impact will be negligible over the next decade / have no impact on type 1 diabetes, PODD's core customer). If this is proven, the multiple should expand. Although competitors Medtronic and Tandem will launch new products over next few years, their success is not guaranteed. For now, Omnipod has a first mover advantage. Abacus sees a path to $3.6bn in 2027 revenues (2023-27 CAGR of 21%) and an EPS of $6.50 (25% CAGR).

Edition: 195

- 20 September, 2024

Technology Spending Intentions Survey

ETR’s July 24 TSIS saw participation from 1768 IT Decision-Makers, including 293 Fortune 500 and 419 Global 2000 organisations. Highlighted vendors include:

Equinix (EQIX) - rising sector and vendor-level spending intent places EQIX in a dominant position among peers, as the vendor seems well-aligned with broader IT spending and ML/AI trends, warranting ETR’s first-ever positive outlook on the data set.

Salesforce (CRM) - souring spend intent for its core Enterprise Apps business, in tandem with overall Net Score in Cloud Computing registering sharp declines, warrants a negative outlook.

Varonis (VRNS) - Negative outlook. ETR has observed a clear declining trend in spending intentions for two years, with an even lower Net Score among the Global 2000 and a sharp rise in Replacement intentions among existing customers.

Edition: 191

- 26 July, 2024

Has the ECB killed the golden goose?

If the Fed has a new paradigm of low inflation and sustained growth, Europe has discovered low inflation and no growth. The result is a structurally weak Euro. David Roche is now SHORT again. Among his secular themes in his February report, central banks figured largely. The report analysed why the Fed may benefit from a new paradigm. That is sustained growth and low(ish) inflation without incurring a recession or massive layoffs. If so, that would be due to a new relationship between job openings and unemployment. In short, job openings and wage increases could fall in tandem without a massive rise in unemployment. That would avoid hitting household income and risking a recession. And for the nerds, it put a kink in the Beveridge Curve and killed the Phillips Curve dead.

Edition: 181

- 08 March, 2024

China: Cyclical fundamentals not as bad, policy creeping in

Manoj Pradhan has long been a bear on China, arguing for years that the country’s economy would go sideways at best. Without fundamentals working in tandem, China equities have little upside. Cyclical fundamentals, however, aren’t as bad as markets think. As a result, a massive equity stimulus isn’t necessary to get the economy back to a somewhat sound footing and the steady stream of measures we are now beginning to see should work. Stay LONG China equities as the market still remains oversold. Keep LONG USD/CNH, but switch CNH’s role to a hedge after a superb run from a change in the China view from May.

Edition: 169

- 15 September, 2023