Fortnightly Publication Highlighting Latest Insights From IRF Providers

Company Research

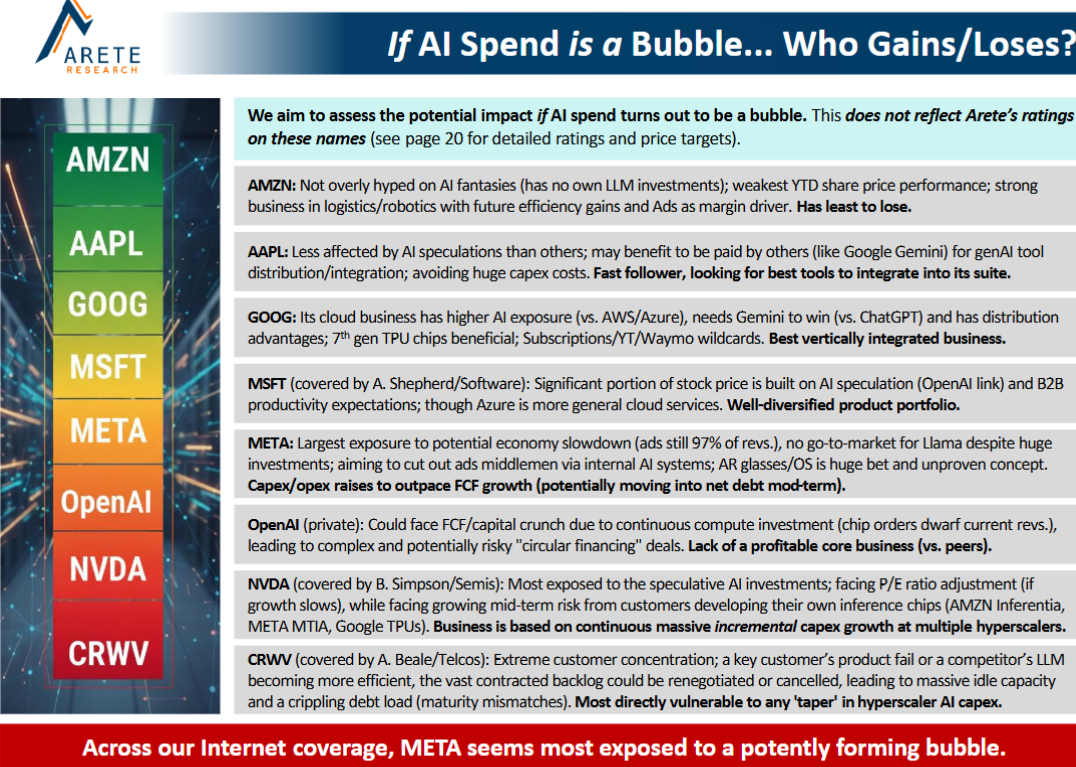

AI & Big Tech: Hunger Games, coming soon

Technology

Arete reviews the surge in Big Tech capex, with their forecasts 20-40% above consensus. They note the mismatch of long-term deals and shortening tech life cycles and accelerated depreciation, believing it will require Big Tech to address new TAMs or target each other’s businesses. Their report weighs whether this spending boom will prove to be a “bubble” and identifies who is most exposed. Arete sees Alphabet, Meta, Apple and Amazon all seeking to “own” a customer interface layer as GenAI products move into mainstream adoption.

Edition: 223

- 31 October, 2025

Fortum (FORTUM FH) Finland

Utilities

Pitched as a long idea at Revelare’s latest investor event, FORTUM operates in Europe’s most attractive market for AI datacentre development. Finland’s grid is mostly hydro and nuclear, with no marginal cost and power prices 60% below mainland Europe, while the cold climate further lowers datacentre cooling needs. All that is required for prices to rise back towards €100/MWh parity is new demand - and that is coming fast. Over 3GW of AI datacentre projects have already been approved, while Google has also bought a huge piece of land in the middle of the country and other hyperscalers are expected to follow. As Finnish power prices increase the company’s earnings should rise from €1 to €3 per share, implying the stock could reach €60 vs. <€20 today.

Edition: 223

- 31 October, 2025

EM Telcos: When does digital drive a re-rating?

Communications

New Street examines when EM Telcos transition from being “Telcos with digital assets” to “Digital-first” companies and when the market begins to re-rate them accordingly. Their analysis of Safaricom and SoftBank Corp suggests that valuation multiples expand once digital revenues reach 15-20% of total sales. New St flags VEON, MTN, Airtel Africa, Vodacom, Kyivstar and Telefonica Brasil as EM operators now approaching this threshold. Digital businesses typically command higher growth, superior ROIC and lower regulatory risk, supporting a valuation premium. Reflecting this view, New Street upgrades their price targets for VEON ($100), Kyivstar ($16.4), Vivo (R$43), AAF (GBP 380), Vodacom (ZAR 200), Safaricom (KES 32) and MTN (ZAR 245).

Edition: 223

- 31 October, 2025

Financials

OWS’s short thesis continues to play out as growth slows and profitability erodes. Total Written Premium (TWP) growth is decelerating, converging toward a long-term low double-digit rate, while management’s talk of 40% growth within five years appears unrealistic. Agent growth has stalled (+3.8% Y/Y vs. +11.1% last quarter) and productivity per agent has essentially been flat for 3 straight quarters. Meanwhile, operating costs per agent continue to rise, leading to margin compression that management expects to persist into 2026. OWS argues that GSHD’s franchise-heavy model is becoming less attractive to experienced agents and increasingly reliant on costly recruitment of new ones, leaving valuation vulnerable to further downside. TP $52 (25% downside).

Edition: 223

- 31 October, 2025

Lifco (LIFCOB SS) Sweden

Industrials

Karl Redin (Subsidiary CEO) purchased 26,350 shares at SEK 381, spending €920k. This is his eighth purchase and over 10x what he has spent on prior buys; the most recent was in Jul at SEK 367. The purchase occurred on the same day as the stock rose sharply after reporting Q3 earnings. This is an unusual buy, into unusual strength. Martin Linder (Subsidiary Head) also recently purchased shares spending €190k - a large purchase for him. Smart Insider has had a positive rank on this stock since early last year, based on buying from Per Waldemarson (CEO), Anna Hallberg (Director) and Martin Linder (Senior Officer). The stock has moved higher and insider buying has continued. Waldemarson made his most significant purchase in Jul, spending €1.3m and then spent an additional €300k in Sep. This is now the fourth time Smart Insider has renewed their +1 rank since Apr 24.

Edition: 223

- 31 October, 2025

Consumer Discretionary

A story riddled with risk - Brian McGough argues DKS is priced for perfection despite mounting structural and cyclical headwinds. Core growth is tapped out and the House of Sport concept – its only unit growth driver - is not working; comping down 20% in year 2 and down again in year 3. Inventory issues, including a Critical Audit Matter on carrying value, and gross margin risks from tariffs on private-label apparel add further pressure. Apparel (40% of sales) has turned deflationary and the Foot Locker merger is seen as immediately margin-destructive, with no strategic merits and likely to strengthen competitors such as Academy and JD Sports. Brian is incrementally of the view that the 5-year CAGR for athletic footwear in the US is -300bp below pandemic-era trends and warns that at 10x EBITDA, a historical peak, DKS is over-owned, over-earning and due for a correction.

Edition: 223

- 31 October, 2025

Saint-Gobain (SGO FP) France

Industrials

Following publication of its FY24 registration document, Iron Blue increases their SGO score to 27/60 (newly top quartile). This principally reflects FY24’s P&L benefit from compression in the expense for inventory and bad debtor impairment provisions, which could provide a tough comp effect in FY25. They also note two new contingent liabilities related to a new Grenfell Tower claim brought against SGO subsidiaries as well as assumed Australia asbestos liabilities with FY24’s CSR acquisition. For the first time the FY24 annual report quantified SGO’s reverse factoring activities (€106m). Iron Blue continues to flag sustained stripped out costs and an elevated gap between PPE capex and the P&L depreciation charge.

Edition: 223

- 31 October, 2025

BLS International (BLSIN IN) India

Industrials

While growth and margins appear strong, Iii’s forensic review of BLS International highlights concerns across the company’s financial reporting with alarm bells ringing especially when it comes to consolidation of accounts, unaudited subsidiaries and the tax stance of the Dubai subsidiary. They also flag an impairment in DSS Gulf Realtors that has surfaced on the balance sheet, in addition to irregularities in cash-flow statements and governance practices. Iii argues these findings highlight gaps in transparency and accounting discipline that investors should monitor closely when assessing the company’s reported results.

Edition: 223

- 31 October, 2025

Adyen (ADYEN NA) Netherlands

Technology

Strong net revenue growth and take rate, were both ahead of expectations for Q3. At constant currencies, net revenue growth amounted to 23%. This is the highest quarterly growth rate this year whilst expectations were that revenue growth would remain flattish in the remainder of the year. Its take rate showed a strong improvement as well, driven by the above average growth of Platforms (up 50.2% and increased take rate to 13.2 from 10.8). Another positive element of Adyen’s quarterly update is that FTE growth (9.0%) lagged net revenue growth again. This will result in a further improvement of its EBITDA margin. Investors can expect more clarity on growth targets at the company's upcoming Capital Markets Day, but based on current momentum and fundamentals, the IDEA! maintains that Adyen remains an attractive investment opportunity.

Edition: 223

- 31 October, 2025

Beneficiaries of US-Japan rare earths deal

Asymmetric Advisors highlights Furukawa and Tadano as potential beneficiaries of the US-Japan initiative to revive American mines, aimed at countering China’s resource dominance. Furukawa’s Rock Drill segment (17% of sales, ~30% of OP), derives over half its overseas sales from North America. The recent acquisition of EarthTechnica should more than double this segment’s sales from FY3/27. The Industrial Machinery division (11% of sales but >20% of OP), which includes belt conveyors used to transport mined materials, provides further exposure. Tadano with ~40% global share in Rough Terrain cranes and ~70% of its US demand tied to resources, also stands to gain. Europe remains its main drag and turning this around is a key factor in any share recovery. The stock trades at 0.78x PBR.

Edition: 223

- 31 October, 2025

Navitas stock surge masks growing execution crisis in AI power market

Technology

JNK Supply Chain Research reveals serious problems hiding beneath the surface as NVTS transitions chip production from TSMC to PSMC. The new factory has lower quality standards and worse yields. Critical 650V GaN devices won't reach mass production until late 2026 or early 2027. Competitor Infineon already ships 800V power solutions to AI data centres. NVTS remains in development while the market moves forward. Big customers like NVIDIA are diversifying suppliers instead of depending on NVTS. The company has few shipping products in hyperscale AI infrastructure. NVTS pioneered GaN technology with 250 million units shipped. But execution matters more than innovation when competitors deliver working products first. NVTS is one of 23 companies JNK tracks in the analog space. Click here for recent results.

Edition: 223

- 31 October, 2025

Materials

EM Spreads initiates coverage on Braskem with an Overweight recommendation. They believe the company’s large domestic footprint, political relevance and partial government ownership make a default event less likely near term, but the credit now hinges less on fundamentals and more on political and strategic decisions involving Petrobras, the federal government and Braskem’s ability to strengthen liquidity. They see asymmetric risk-reward at distressed prices, with outcomes contingent on a secured-liquidity bridge, PRESIQ approval, direct support measures and broader policy backing for Brazil’s petrochemical sector. They favour exposure to the lower-priced bonds within the curve for better downside protection and see greater value in the 2030s at $38.3, 32.1% YTM, 3.1-yr duration.

Edition: 223

- 31 October, 2025

Industrials

Sidoti lifts their target price by 45% following another record-breaking quarter for FIX. 3Q25 EPS and sales beat forecasts by 32% and 16%, respectively, as the company continues to steer its project mix towards the technology sector (mostly data centres). FCF hit $516m (177% of net income) while the order backlog rose 15% sequentially (all organic) and 65% Y/Y (62% organic) to $9.4bn. Expanding modular capacity remains a potential near-term catalyst, while beyond 2026, Sidoti views no shortage of end markets experiencing secular growth (e.g. reshoring, advanced manufacturing, chip plants), or other hyperscalers for that matter, that would like a greater chance to compete for FIX’s services, were current customers to decrease their expenditures. Sidoti now models 2025 EPS of $25.60 (from $22.91), 2026 EPS of $30.34 (from $26.50) and introduces 2027 EPS of $38.50.

Edition: 223

- 31 October, 2025

Consumer Discretionary

PLNT is well positioned in the growing high‑value‑low‑price gym segment with scale and ample runway for growth. New CEO Colleen Keating brings relevant hospitality franchise experience to drive the next phase of growth in the US and internationally. Gen Z is the fastest‑growing membership cohort for the company, supported by initiatives like the “High School Summer Pass”. PLNT continues to refine club formats and contractual terms to improve efficiency and unit economics. 2Xideas expects 2024-31E system‑wide sales CAGR of 11.7%, driven by 6.6% annual net unit growth and 5.0% same‑club sales growth. They forecast an 11.1% EBITDA CAGR and a 44.6% margin in 2031E. European expansion remains an upside not reflected in their forecasts. They see 17.2% annualised total returns based on an exit NTM P/E of 28.0x (17.7x EV/EBITDA).

Edition: 223

- 31 October, 2025

Consumer Discretionary

The Retail Tracker notes continued improvement in URBN’s product assortments, describing the current offering as focused, confident and well-positioned for the holidays with stronger gifting and better alignment to its customer. New leadership is credited with sharper merchandising and more responsive assortments visible across stores, online and social media. Anthropologie and Free People remain strong, attracting younger shoppers while maintaining core customers, with standout accessories, home and active lines. Nuuly, the rental platform, continues to expand rapidly, offering tariff resilience and appealing to younger, price-sensitive consumers. The Retail Tracker has been positive on the name since early in the year and remains so.

Edition: 223

- 31 October, 2025

Communications

Paragon Intel takes a negative view on CEO Sundar Pichai, arguing that his slow, consensus-driven leadership style has left the company “fast following” in an AI race it should be leading. While Pichai’s long-term vision and product instincts built successes like Chrome and Android, and his tenure has delivered impressive financial results, his risk aversion, conflict aversion, reluctance to refresh senior leadership and indecisive response to competitive threats like ChatGPT have led to internal stagnation. Paragon’s analysis includes interviews with 6 former Alphabet executives, who portray him as a thoughtful strategist and capable steward, but ill-suited to the fast, “wartime” pace the AI era demands.

Edition: 223

- 31 October, 2025

Healthcare

Leveraging purchase order data from 450 US facilities, MedMine is closely tracking the rollout of Pulse Field Ablation (PFA), the key driver of BSX’s Electrophysiology growth. The US ablation catheter market for AFib is estimated to be growing about 12% Y/Y. BSX has been growing faster in part due to mix shifting from lower-priced Cryo and RF products to its premium FARAPULSE PFA system. However, BSX is facing increasing competition with its PFA market share now at 80%, 10 percentage points lower than its peak. This raises a key question: will BSX’s next growth phase come from converting the larger RF market or expanding the total patient base estimated at 60m globally? MedMine’s near real-time data helps investors track these shifts in market share, pricing and technology adoption as they unfold.

Edition: 223

- 31 October, 2025

Financials

Abacus sees FIGR as a highly disruptive leader in real-world asset tokenisation - a theme they expect to define the next decade. The company has found a real-world use for blockchain, proving it can reduce the cost and time in HELOC origination by 90% (current 3% market share), with an average production cost per loan of just $730 vs. an industry average of $11,000. Beyond its low-cost origination engine, FIGR operates a marketplace for pooled credit, creating liquidity and transparency in traditionally illiquid markets. Abacus expects this model to scale into other asset classes, underpinned by ~30% operating margins and 80%+ incremental margins, with potential upside of 150% to $115.

Edition: 223

- 31 October, 2025

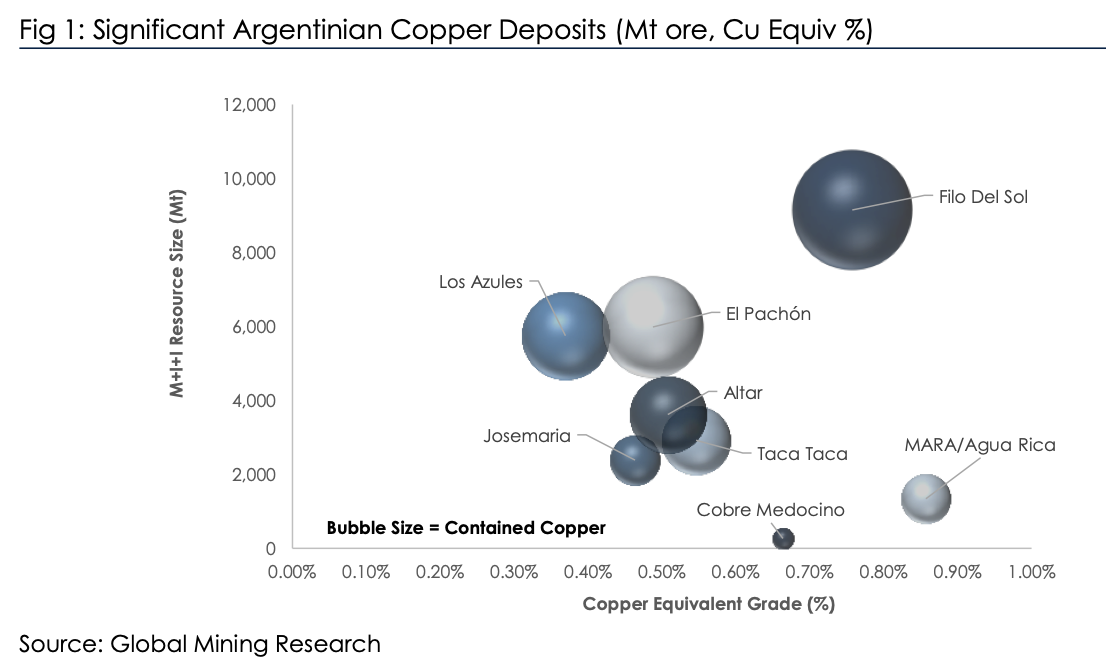

Is Argentina the next big thing?

Argentina has significant copper reserves yet produces no material copper (see chart). The new investment climate (RIGI) in Argentina, spearheaded by libertarian President Milei, is hoping to reverse this. Other volatile countries including DRC have achieved significant growth, so it’s possible. In his latest report, David Radclyffe examines the potential of Argentina copper. He sees potential for the nation to become a 1.0–1.5 Mt per year copper producer (top 10 globally), but comments on the aspirational timelines, with first copper unlikely on this side of 2029. Issues also cannot be discounted, with ESG concerns bubbling alongside a lack of infrastructure and skilled workers. David estimates the total capex at USD $40–50 billion. Lundin Mining has the most leveraged exposure to Argentina in partnership with BHP and is the preferred exposure. There are a few exploration plays, of which NGEx Minerals (non-rated) and its Lunahuasi discovery is the largest.

Edition: 222

- 17 October, 2025

A compelling growth story

AIR highlights Spain as the Eurozone’s standout growth opportunity, further supported by US immigration tightening redirecting talent and labour. The country is benefitting from its strong position in the EU’s €750bn Next Generation EU program, minimal exposure to US tariffs and insulation from Chinese industrial competition. A rapid transition to renewables has driven a 40% decline in wholesale electricity prices over five years, while lower structural taxes and spending continue to support competitiveness. Preferred sector calls include Infrastructure (Acciona, Ferrovial, Sacyr) with robust project pipelines supported by public and private investment; Banking & Insurance (CaixaBank) benefitting from SME exposure and high household savings rates; Real Estate (Merlin, Metrovacesa) poised for catch-up gains vs. other European countries amid supply constraints; and Defence, where Indra Sistemas is well positioned for M&A.

Edition: 222

- 17 October, 2025

Technology

Asymmetric Advisors has turned bearish on Fujikura, having recently closed their long position after what they call a “crazy rerating”. They were “beating the drum” when the stock traded around 15x earnings, but it now sits near 30x FY27, a level they see as unjustified for what remains a largely commodity cable supplier. While earnings surged in recent years on strong demand for its Spider Web Ribbon fibre cables used in AI data centres, capacity constraints and intensifying competition from Corning to Ciena to Furukawa and Sumitomo Electric are likely to cap further upside. Asymmetric now views Fujikura as a suitable short hedge against more attractive technology names in their portfolio.

Edition: 222

- 17 October, 2025

Consumer Discretionary

Brian McGough reiterates his bearish view on FND despite the stock’s ~50% drop since his Apr 24 short call (vs. the S&P +33%). Brian is updating his analysis using his M.A.P.S. (Market Area Performance Study) framework, which tracks store performance by opening cohort. His latest findings suggest that stores opened in 2024 & 2025 are performing even worse than earlier cohorts, reinforcing that FND’s weak comps are structural, not cyclical. New units also show rising market overlap with the likes of Home Depot and Lowe's. While FND is often seen as a housing-recovery play, Brian expects another ~30% downside as earnings, growth guidance and unit expansion continue to disappoint.

Edition: 222

- 17 October, 2025

Nexperia dispute highlights Europe’s semiconductor dilemma

Technology

The escalating dispute between the Dutch government, China and chipmaker Nexperia has become a flashpoint in the global semiconductor power struggle. With parent company Wingtech already on a US trade blacklist and facing tighter restrictions, Nexperia’s plan to separate its Chinese and European operations is now in jeopardy. The export ban poses an immediate risk to Europe’s industrial supply chain, especially in the automotive sector. Finding and certifying alternative suppliers could take months, echoing the chip shortages of 2021/22. Strategically, it spotlights the West’s push for technological sovereignty and the Netherlands’ pivotal role in the China–West tech decoupling. Several (Dutch) companies could be affected including ASML, NXP, Philips and ASM International.

Edition: 222

- 17 October, 2025

Japanese Banks: Taking profits, staying selective

Financials

Galliano's Financials Research

Victor Galliano has lightened positions in Japanese banks, retaining those with larger cross-holdings relative to market cap, which he expects to benefit under an easier-for-longer monetary policy. He argues that managements’ commitment to realise cross-holding value through disposals should be a key near-term driver of share performance. Despite potential delays to further rate hikes, lending rates and net interest margins have continued to rise since the end of NIRP, supported by low delinquency levels. Combined with attractive valuations, these trends should underpin higher medium-term multiples. Among large caps, he keeps Resona and Shizuoka as Buys (downgrading Mizuho to Neutral) and among mid-caps, maintains Buys on Iyogin, Hokuhoku and Hachijuni, while downgrading Hirogin to Neutral.

Edition: 222

- 17 October, 2025

AI insights from China’s Tech giants

Technology

Westlake’s latest reports draw on discussions with AI experts from Tencent, ByteDance and Alibaba, offering fresh perspectives on China’s evolving GPU and ASIC landscape. Tencent’s AI Product Manager detailed the rationale behind increased domestic GPU procurement this year and outlined potential market shifts if B30A and H20 export policies are relaxed. ByteDance’s AI Solution Architect described surging AI compute and token usage and the rapid expansion of AI investments and custom chip development. Alibaba’s AI Project Manager discussed GPU procurement trends, progress in its T-Head ASIC programme and ongoing Qwen model development, including on-device use-cases.

Edition: 222

- 17 October, 2025

Technology

BTN continues to see several areas where OSIS's results may be unsustainable. The company has reduced its bad debt reserve to just 2% of receivables (vs. a 5-7% historical range), adding ~11 cents to Q4 EPS (OSIS only beat Street estimates by 5 cents). The current reserve for bad debts is at least 200 bps too low; if OSIS had to raise it by 100 bps, it would be a 39-cent headwind for EPS. DSOs have surged to 151 days (historically ~90), making Q4's revenue increase more suspect and the $372m forecast for 1Q26 tougher to reach. Warranty expense was cut again (added 3.7 cents to EPS), while OSIS continues to let its PP&E age and is using fully depreciated equipment - saving 29 cents in EPS last year. Finally, FCF remains weak (negative in 5 of the last 8 quarters).

Edition: 222

- 17 October, 2025

Technology

Craig Huber raises his 12-month price target to $2,300 (from $2,100), citing stronger long-term earnings visibility under the company’s new 2026 US mortgage pricing models. The existing Per-Score Model will double to $10 per score, while the new Performance Model combines a $4.95 per score fee with a $33 funding fee on closed loans - boosting mortgage origination revenue by ~130%. Craig lifts his FY26/27 revenue forecasts to $2.54bn / $3.12bn (up 27.5% / 22.7% vs. prior) and expects EBITDA margins of 62.2% and 66.6%, respectively. His adjusted EPS estimates for FY26/27 increase to $43.85 / $60.00 (vs. previous estimates of $36.25 / $45.35). Craig sees limited competitive threat from VantageScore, arguing that FICO’s market dominance and pricing power remains intact.

Edition: 222

- 17 October, 2025

Capital Markets at Risk: Jefferies echoing Bear Stearns

Financials

Charles Peabody believes we are in the mature phase of the capital markets cycle, with revenues likely topping out in 2026, while stocks are expected to turn lower well before then. He recommends selling Morgan Stanley and Goldman Sachs on near-term strength. Credit and liquidity stresses are emerging following the automotive credit, Tricolor and First Brands developments, while syndicated loan offerings are being pulled. He sees echoes of Bear Stearns at JEF, noting that MS and BlackRock have ended relations with Bonita Point, the JEF subsidiary housing First Brands receivables, just as this rapidly growing broker reached top-tier status. Sell Capital Markets, Buy NII - he favours Citi, M&T, Citizens Financial and UBS.

Edition: 222

- 17 October, 2025

Communications

Hesham Shaaban initiates a new tactical long in RBLX, arguing that the recent sell-off following the M Science report has created a “coiled spring” setup ahead of 3Q25 results. His analysis indicates that Concurrent Users have accelerated each month through Q3 and into Oct, contradicting perceptions of a slowdown. He believes the M Science data may not fully capture RBLX’s expanding user base, underestimating bookings growth. If platform activity trends hold, even modest monetisation could yield a double-digit bookings beat for Q3 and stronger Q4 guidance. With the shares up >100% YTD, Hesham expects short exposure to increase into the print, meaning any upside surprise could trigger a sharp rebound if results confirm his thesis.

Edition: 222

- 17 October, 2025

Drug pricing demos as Pharma scrambles

Healthcare

President Trump's drug pricing plans are progressing from the conceptual to a more serious phase. As CMS prepares to issue its most favored nation (MFN) demonstrations and pharma companies attempt to cut pricing and manufacturing deals with the administration, Capital Alpha Partners' Rob Smith and Kim Monk caught up with a former director of the Center for Medicare and Medicaid Innovation (CMMI) on the administration’s advancing Medicare drug pricing agenda. The team sees at least one demo being proposed by the end of the year and implemented by late 2026, though legal challenges remain significant. Physician-administered Part B drugs are the most likely target for a drug model.

Edition: 222

- 17 October, 2025

Technology

TD trades at levels implying investors value its operating business at near zero, reflecting deep scepticism about growth and profitability amid dependence on Samsung and exposure to memory price volatility. While these risks are real, Yuka Marosek argues they are already priced in and TD’s close ties to Samsung Japan and Toyota Tsusho provide stability and long-term relevance. Expansion into automotive and server / storage markets, supported by rising AI-driven demand for memory, offers potential for improved margins and diversification. Toyota Tsusho owns 50.1% of TD and Yuka wonders if Tsusho might eventually absorb the entire company - if Samsung allows it.

Edition: 222

- 17 October, 2025

Technology

Could the stock soar over 100%? KCR argues that CSCO isn’t just cheap vs. AI peers - it is cheap relative to the broader market, trading at roughly the same multiple as Kimberly-Clark despite far stronger growth. Networking product orders have risen 10% Y/Y for 4 consecutive quarters, suggesting investor concerns about a slowdown are unwarranted. Meanwhile, the company’s rapidly growing exposure to AI infrastructure products and shift towards subscription-based revenue both support multiple expansion. CSCO trades at one-third of Arista Networks’ P/E multiple and one-quarter of its EV-to-revenue ratio - even a modest narrowing of the valuation gap would translate into substantial gains for CSCO shares. Finally, a ~5% FCF yield is far too high for a company of CSCO’s quality.

Edition: 222

- 17 October, 2025

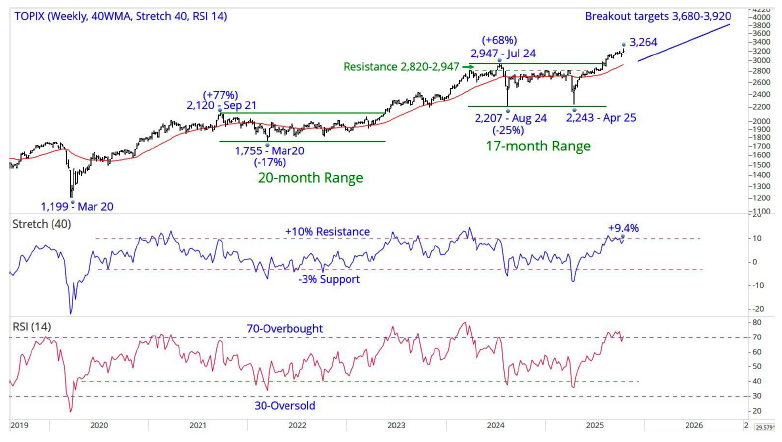

Japan: Hot Topix

The Topix’s (3,198) breakout from the 2,207–2,947, 17-month range targets an advance to 3,680–3,920. The break above the 1,700–1,825, 28-year ceiling in 2021 targets a minimum of 3,400–3,650+. Weekly indicators are either overbought, or close to overbought, but have been higher during this bull market. Chris Roberts remains 50% long from 2,857, with the stop for all longs moving up to a daily close below 2,780 from 2,475. His preferred target is now 3,680+, and he is looking to add to longs. He will add 5% long at 3,178, 5% at 3,168 and 5% at 3,158. If fully executed, he will move to 65% long.

Edition: 222

- 17 October, 2025

DCC (DCC LN) UK

Energy

Following publication of the company's FY25 annual report, Iron Blue increases their DCC rating +3 pts to 27/60 (newly top quartile / fertile grounds for shorting). Key changes vs. FY24: 1) Higher one-off costs: FY25 stripped out restructuring expense increased to 7% of PBT adj, highest in 7 years. DCC also stripped out from headline earnings £74m goodwill impairment. 2) Took £17m profits on disposal of PPE inside underlying profits in FY25, the highest figure in the past decade. 3) P&L expense for inventories write-downs dropped to a decade-low of £5m. 4) DCC continued its strategy of promoting top management from within, with internal promotions to the CFO and newly created COO roles. 5) In its principal risks assessment, DCC highlighted Y/Y risk increases concerning the DCC Technology strategic review and also the impact on its operations from higher tariffs.

Edition: 222

- 17 October, 2025

Tenaris (TEN IM) Italy

Materials

Alejandro Acosta highlights a structural shift in global energy markets, noting that oil and gas exploration has not kept up with production since the 2014-2016 crisis, but is now rebounding as major producers resume investment. Slower-than-expected EV adoption and renewed automaker focus on internal combustion engines support sustained demand, while rising US natural gas consumption - driven by data centre power needs - adds further tailwinds. Alejandro argues these dynamics are not yet priced into TEN, whose improving financials and active share buybacks underscore management confidence. Although potential tariffs pose risks, TEN’s extensive US manufacturing base provides a competitive edge over other foreign suppliers.

Edition: 222

- 17 October, 2025

Siemens Energy (ENR GR) Germany

Industrials

A “backdoor” AI infrastructure play amid growing power bottlenecks from new data centre construction. As data centres cannot rely on intermittent renewables, natural gas turbines are seen as the only viable near-term solution. The market is extremely tight, with projected demand of 80-100GW vs. supply of only ~70GW and consensus likely underestimating both pricing and volume potential. ENR’s Gas business is positioned to deliver 20%+ long-term margins, while its Grid Technologies division should benefit from global electrification and grid modernisation, with revenue expected to exceed €20bn by 2030. Shares could double over the next 3 years, driven by earnings beats and a profit inflection in the Wind segment. The upcoming November Analyst Day is viewed as a major catalyst.

Edition: 222

- 17 October, 2025

Consumer Discretionary

Antedata’s coding activity data points to rising freelance projects related to ETSY, highlighting its strong positioning as an AI beneficiary. Freelancers typically help sellers set up storefronts, optimise search visibility, automate listings and create professional branding. ETSY’s vast, unstructured dataset and its dual role as marketplace and discovery hub make it a prime use case for AI. The company already employs AI in search, personalisation and ad targeting, driving better conversion and marketing efficiency. With operating leverage and discretionary R&D / marketing spend, even modest efficiency gains could meaningfully boost profitability - supporting AnteData’s view that ETSY’s current valuation can be justified by earnings growth potential.

Edition: 222

- 17 October, 2025

AI: Scepticism’s turn

The last week has seen AI sceptics jumping up and down about a coming crash, but Richard Windsor sees them citing data that is misleading. One reason was the MIT study, which claimed that 95% of AI projects failed to yield benefits, but the report also said that great benefits can come when such projects are implemented correctly. So, the sceptics may be wrong, but not nearly as wrong as those who believe superintelligent machines are soon to be among us. Richard sees the idea of $200bn/yr in revenue for OpenAI by 2030 as preposterous, and sees a correction coming, but it won’t be a crash on the scale as the AI sceptics claim. Hyper valued companies burning through money will get into real trouble, but the picks and shovels like Nvidia, Nebius, Micron, SK Hynix, Samsung and Qualcomm and so on are likely to continue to do well. Richard continues to hold the latter two.

Edition: 221

- 03 October, 2025

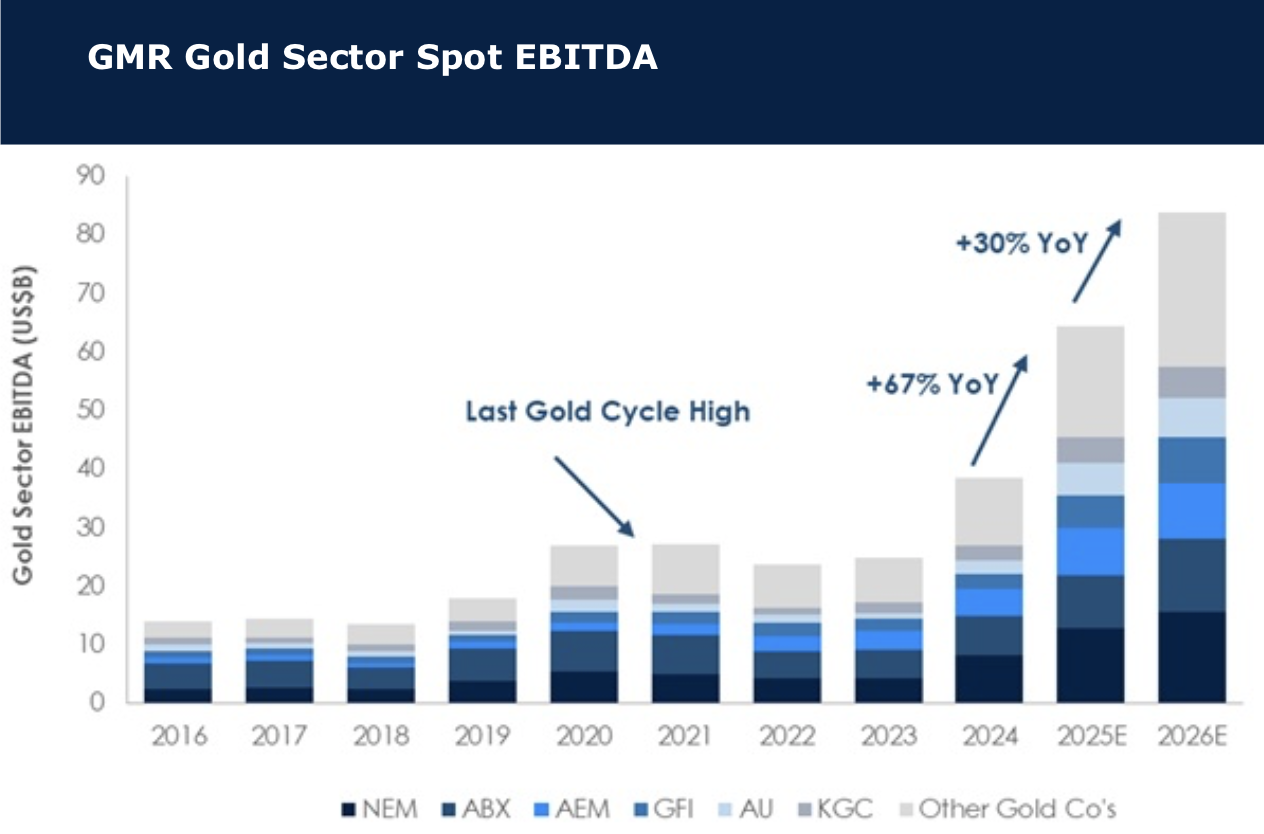

All that glitters is gold

Gold has been setting new highs through 2025 as the best performing major commodity. The music will come to an end, but David Radcliffe says that until that happens, a spot gold price over US$3,800/oz will generate some extraordinary returns. He examines the impact that spot prices could make to a sector that has already benefited from a robust 18 months. The 2026 consensus gold price is ~US$470/oz below spot, implying further upside if prices are maintained. On David’s expectations, spot prices into 2026 could lift sector EBITDA another 30% after an expected 67% lift in 2025. His covered gold stocks trade at a discount with spot P/NPV5 of 0.87x, or an implied gold price of ~US$3,330/oz, a 13% discount. There remains a value argument for gold miners, plus earnings momentum. David’s preferred exposures remain Agnico Eagle, Kinross and Northern Star of the seniors, and IAMGOLD, Equinox and Alamos of the more leveraged intermediates.

Edition: 221

- 03 October, 2025

How will China monetise AI differently?

China will be a close and capable AI follower, focusing on downstream implementation as the US focuses on upstream. This means the two will not run head-to-head encounters right away, and China can lead in the application of AGI in manufacturing and logistics. Its monetisation path will be more complex but can exist. However, as it stands, China is under-monetising AI vs the US. The Blue Lotus team estimate that consumer (2C) AI applications generated $2.0–3.5bn in the US and $0.3–0.5bn in China (excluding AI-enabled advertising and much of video AI). The US monetises AI globally, with global 2C revenues bringing in ~12x that of China. However, the gap will shorten significantly by 2030, in part by taking a lead on robotics+AGI. The team reiterate their top picks of Alibaba, Hesai, CATL and Kuaishou. Baidu stays as a sell.

Edition: 221

- 03 October, 2025

Can a demand sanction on Chinese biotech help US companies?

Healthcare

Blue Lotus examines the early-stage pipelines of 25 Chinese biotech companies (CBT), covering 177 drugs and 278 rival drugs worldwide across 80 biotargets. CBT claims 5 dominant leads, 8 competitive leads and 8 co-leads. Of the remaining 59 biotargets, US biotech companies (USBT) hold leads in 43, of which 31 face "me-better" Chinese competition and 12 "me-too". CBT has been winning by quantity and now increasingly by quality. This raises a dilemma: US demand sanctions could ease competitive pressure for ~49 USBTs (~14% of sector m/cap) but it might also restrict patient access to innovative therapies. Innovent, BeOne, Duality, Junshi and Akeso are highlighted as top early-stage innovators, while 3SBio and SinoBio appear undervalued.

Edition: 221

- 03 October, 2025

Special Sits Idea Forum

The majority of ideas presented at MYST's latest buyside event were industrial-related, with themes including potential takeouts, SOTP simplification stories and power-related names. Stocks highlighted include:

Aptiv (APTV) - “GoodCo vs. BadCo” split to unlock hidden value of Connection Systems business. TP $125 (45% upside).

Bed Bath & Beyond (BBBY) - unappreciated assets create “zero enterprise value” amid positive FCF inflection. TP $28 (180% upside).

DuPont de Nemours (DD) - re-rating tailwinds fuelled by fundamental and technical catalysts. TP $115 (45% upside).

Idaho Strategic Resources (IDR) - enormous upside from potential US government partnership / investment.

Peloton (PTON) - new product launches + subscription price increase to accelerate turnaround.

Ralliant (RAL) - ignored "broken spin” poised for positive revision cycle. TP $60 (35% upside).

Edition: 221

- 03 October, 2025

Ginlong Technologies (300763 CH)

Industrials

It has been three years since the last insider activity in this stock occurred. In Jun 22, the selling was from Finance Director Junqiang Guo and Deputy GM Chan Zhang around CNY 200 per share. The stock rose for a few months but then fell sharply in 2023. Recently, Guo, Zhang and Deputy GM Hefeng Lu made large sales at less than half that price: Guo sold US$862k at CNY 85, Zhang US$515k at CNY 85.06 and Lu US$350k at CNY 87, reducing their holdings by 30%, 30% and 23%, respectively. The stock has nearly doubled from its Apr 25 low but remains flat over the past 12 months and below 2023 levels. Smart Insider are ranking the stock -1 (lowest rating).

Edition: 221

- 03 October, 2025

Technology

AI is fuelling accelerating demand for high-performance compute (HPC) and Bitcoin miners-turned HPC hosting providers have been huge beneficiaries. While the stocks have rallied significantly as multi-billion-dollar contracts become more frequent, Rosenblatt sees a valuation disconnect at WULF due to its perceived smaller power pipeline. They view this as more of a disclosure issue than anything fundamental and expect the power experts at WULF to proactively add new capacity ahead of current market expectations. As such, Rosenblatt reiterates their Buy rating and raises their TP to $14.50, based on 16x their 2027 Adjusted EBITDA estimate.

Edition: 221

- 03 October, 2025

Consumer Discretionary

John Zolidis turns bearish on SBUX heading into Q4. He views domestic store closings and a potential China exit as signs that SBUX is no longer a growth business and valuation should contract to reflect this. Furthermore, traffic remains negative and estimates are too high more than one year after Brian Niccol started as CEO. Last quarter was good for Quo Vadis’ calls with their average Long idea falling 1% compared to an average decline in their Short ideas of 15%. Their (Retail & Restaurants) universe fell 9%, reinforcing that Quo Vadis' approach is identifying winners and losers and creating alpha. Q3 was the fourth consecutive quarter with longs outpacing short ideas.

Edition: 221

- 03 October, 2025

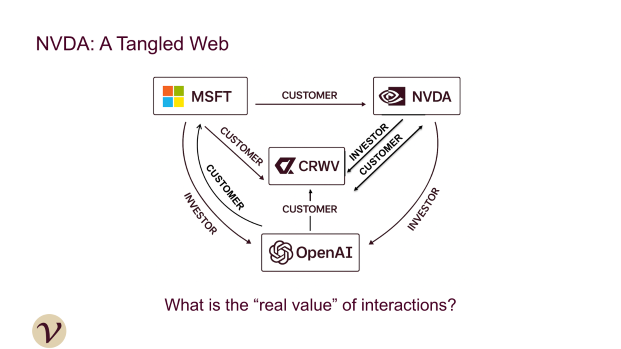

Nvidia's circular financing

Technology

Veritas has been flagging NVDA’s customer financing activities well before they hit the headlines: in 2023, they first highlighted the issue in “Nvidia & The Tech Sector's Circular Cash Flows” and reiterated their concerns earlier this year in “Nvidia’s CoreWeave - A Familiar Story”. Following the Oracle/OpenAI deal, the sell side is now echoing Veritas’ warnings, drawing parallels to the dotcom bubble, when Nortel, Lucent and Cisco extended credit to customers to enable their internet infrastructure buildout. Veritas does not expect this risk to be priced into NVDA's stock until revenue growth slows. If investors doubt customers can generate returns on their chip investments, these large negative cash flow purchases will not be well received.

Edition: 221

- 03 October, 2025

Consumer Discretionary

Hesham Shaaban expects DKNG’s Q3 results to miss consensus, with Periphery’s revenue trackers showing mixed y/y growth in Jul and Aug and their new NFL Upset Tracker pointing to a weak Sep (total upsets down ~33%). He had planned to increase his short into Q4 to capture the downward revision cycle but notes the buyside has already sniffed out the early fallout from the NFL season. Looking ahead, he anticipates management will cut FY25 guidance while going big with their initial 2026 guide to backstop the stock - a pattern seen in both 2024 and 2025. With history likely to repeat, Hesham may still add into the revision cycle but could reduce exposure ahead of the Q3 print.

Edition: 221

- 03 October, 2025

Delhivery (DELHIVER IN) India

Industrials

At first glance, Delhivery’s FY25 results - its first net profit and positive EBITDA margins - suggest the company has finally scaled and matured. However, Iii argues the turnaround is more cosmetic than fundamental. Favourable revenue recognition policies (contract assets equal to ~30 days of sales vs. a 13-day transit cycle), depreciation changes and halved ESOP charges materially flattered reported profits. Capital allocation remains troubling, with Spoton Logistics revenues collapsing >70% since its INR 16bn acquisition, yet losses effectively buried via amalgamation. Rising impairments, questionable subsidiary accounting and elevated executive compensation add to concerns.

Edition: 221

- 03 October, 2025

ASML (ASML NA) Netherlands

Technology

Arete’s report titled "The Capex Conundrum" focuses on: 1) The broader growth backdrop for leading-edge semi demand and the disconnect in ASML and wider WFE estimates into 2026/27. 2) Capex for key customers which should see significant upside over this cycle, boosting EUV demand and delivering above consensus revenues and EPS through 2027E. 3) The ongoing China capex contraction which is now captured in consensus numbers and stock sentiment. 4) Why there has been a disconnect between N2 capacity growth and EUV unit shipments. 5) Risks around the EUV roadmap and the possible move to 3D DRAM and how that might impact unit demand. 6) Valuation risk/reward, especially against the backdrop of recent sell-side downgrades and negative broader investor sentiment towards WFE, looks attractive.

Edition: 221

- 03 October, 2025

Industrials

Under new leadership, Kyodo is accelerating its pivot from the declining paper-printing business towards higher-margin niches such as high-performance packaging materials, flexible packaging and tube products. Margin gains in recent years already reflect this shift and the company’s 10-year plan aims to scale these efforts further. The key question for investors: with DNP and Toppan well ahead in diversification, can Kyodo leverage its niche strengths to establish itself as a viable third player in a consolidating industry. Yuka Marosek argues it can. While Kyodo’s OP recovery appears partially priced in (13.9x P/E vs. DNP at 14x and Toppan at 18.4x), a 4.8% dividend yield should appeal to income investors and with FY26 OP projected +20% y/y and ROE rising to 6.1%, further upside remains possible.

Edition: 221

- 03 October, 2025