Fortnightly Publication Highlighting Latest Insights From IRF Providers

Company Research

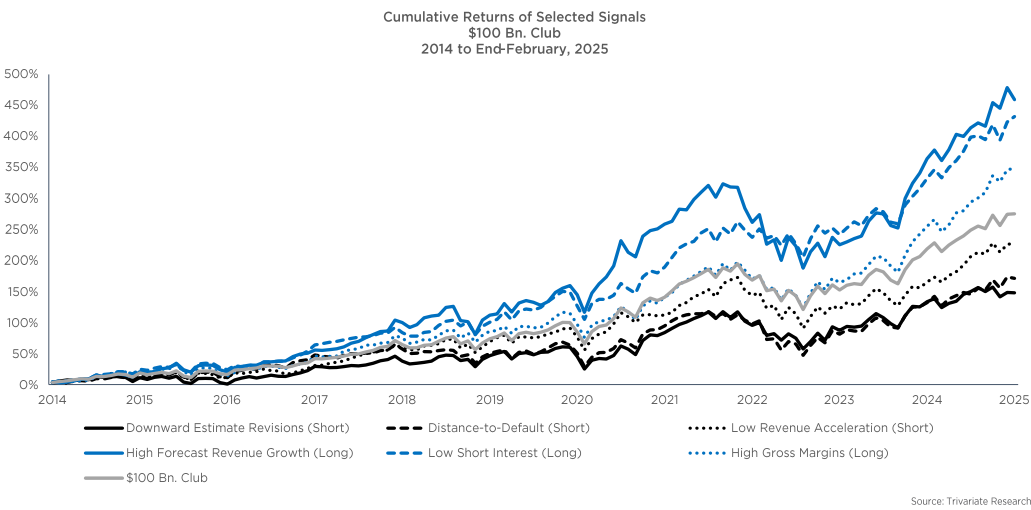

Which stocks >$100bn m/cap are buys now?

With investors searching for value in the current market sell-off and likely looking to buy names among the safer, larger cap universe, Trivariate has assessed the performance of several metrics within the stocks >$100bn m/cap to see if they could systematically pick winners from losers. The best performing signal over the last 10 years, was buying the companies in the top third of forecasted revenue growth, while the second best was buying the one-third of companies with the lowest short interest. The worst performing signals were those in the highest third of leverage and stock volatility (distance-to-default) and those with the worst third of downward earnings revisions. Current long ideas from Trivariate’s $100bn Club Framework include all the Mag 7 (except Tesla), as well as Eli Lilly, Visa and UnitedHealth. Shorts include Goldman Sachs, PepsiCo, Caterpillar and Starbucks.

Edition: 207

- 21 March, 2025

What’s the right beta for your portfolio?

Trivariate analysed the top 500 US equities for five factors beyond the market: size (top 100 vs. 401-500), growth vs. value, high-quality vs. junk, liquidity and momentum. They focused on 3 different portfolios (min-vol, max-Sharpe, max-return) to show a range of outcomes. Over the last 20 years, the “efficient frontier” or optimal beta for a median portfolio appears to be between 0.95 and 1. If you are looking to lower your portfolio beta efficiently, owning high-quality value stocks with relatively low liquidity is a prudent strategy (e.g. Exxon Mobil, Philip Morris, Lowe’s, Medtronic). If you want to take more risk, the optimal factor loadings would be to add to highly liquid growth stocks that are junk quality (e.g. Tesla, Applovin, Micron).

Edition: 204

- 07 February, 2025

Europe’s car industry

The Swedish battery start-up Northvolt has filed for bankruptcy in the US. It is the latest in a series of mishaps to befall Europe’s car industry. Wolfgang Münchau argues that the main problem is not with the new firms like Northvolt, but rather Europe’s dependence on incumbent auto dinosaurs. Compared to Tesla and the panoply of Chinese electric car firms now present, the old incumbent firms are struggling to manage the process. There is also more effective vertical integration, with the new firms building their own batteries instead of relying on smaller new firms. This success stems from a key difference between Europe and both the US & China, the first being more effective capital allocation and the second being a willingness to see new firms pop up, rather than coddling old ones.

Edition: 200

- 29 November, 2024

Consumer Discretionary

Q3 results exceeded expectations, sparking a 21% surge in share price, but the rally overlooks fundamental flaws, especially in TSLA’s robotaxi business. While Elon Musk envisions fares at $1 per mile with low costs of $0.2 per mile, this assumes his company will dominate the market unchallenged. In reality, TSLA faces intense competition, which could push fares down to $0.4 per mile, reducing gross margins to c.20%. The net result is that Musk is overestimating the size of the revenue opportunity by 2 or 3 orders of magnitude and TSLA’s market share by a similar amount. Richard Windsor believes the share price remains substantially overvalued.

Edition: 198

- 01 November, 2024

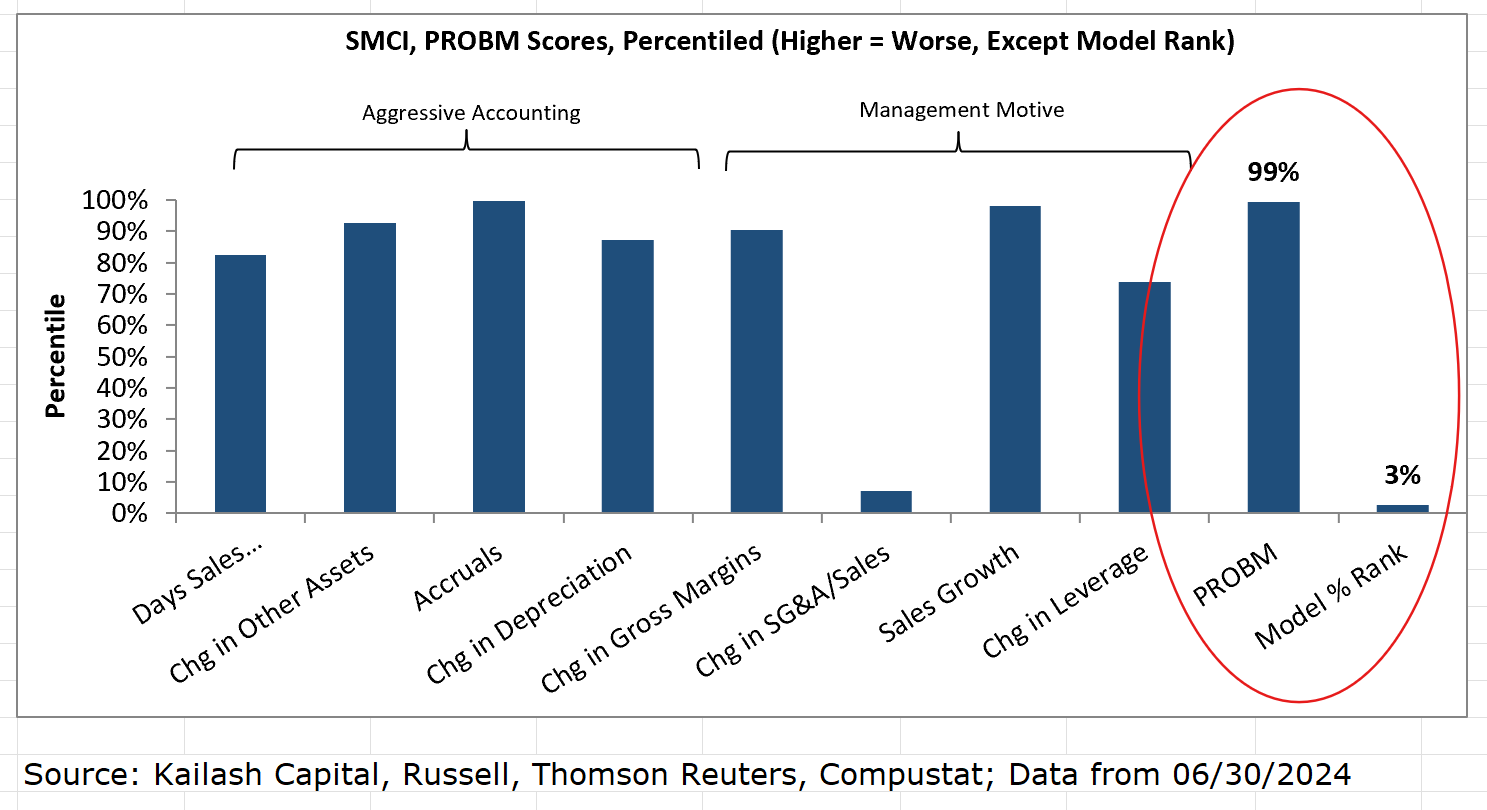

A systematic approach to identifying potential earnings manipulators like SMCI

SMCI shares fell nearly 20% after the company delayed the filing of its annual report and Hindenburg Research alleged “fresh evidence of accounting manipulation”. Interestingly, SMCI features in KCR’s S&P 500 Earnings Manipulator list, which includes stocks in 1) the worst quintile based on academia’s PROBM formula and 2) the bottom 20% of KCR’s ranking methodology. Other companies flagged include Advanced Micro Devices, Tesla, and Xylem, with Block and Emerson Electric added last month. Over the past 14 years, KCR’s Research Short Portfolios have been valuable for spotting potential risk flags and generating short ideas. To access the return summary for these portfolios click here.

Edition: 194

- 06 September, 2024

Crypto: The ultimate Trump trade

In April 2017, Jawad Mian expressed a bullish opinion on Tesla, with the company at the epicentre of Trump’s economic nationalism. This time around, he’s betting on crypto. Trump has made it clear that his administration will support digital currencies, in contrast to the Biden administration’s scepticism. Although crypto assets have performed poorly since the March peak, the legislature appears to be warming up to crypto. New legislation has been passed to provide regulatory clarity for digital asset innovation and the SEC even approved exchange-traded funds for ether. Other positive developments are emerging, including Mastercard’s recent decision to allow users of Binance to make purchases on its network. If Bitcoin is ever going to make a run for $100,000, now is the time.

Edition: 189

- 28 June, 2024

Materials

Ecopro BM is South Korea's largest producer of cathodes for EV batteries. The company is an important supplier to BMW and Tesla and can be viewed as an early indicator to EV market demand. Recently, Ecopro BM reported a major decline in revenue growth, stating 1Q24 Total Revenue (KRW) at -52% Y/Y and below market expectations. Global investors who closely follow Ecopro and the EV market used Sandalwood’s South Korea data to accurately track this trend.

Edition: 186

- 17 May, 2024

The greatest macro trade of all time

Raoul Pal has believed that since 2008, business cycles are largely in sync all around the world, driven by the global debt jubilee when rates were set to zero. When the interest payments inevitably rise, GDP growth falls below the cost of these payments, and a cycle later these payments end up on the balance sheets of central banks, debasing the currency. This has created a near-perfect cyclicity in the global economy hitherto unimaginable. The next step for Raoul’s The Everything Code was for the Fed to go on hold, and next up should be the end of QT and rate cuts in 2024. This is the path of The Everything Code, which if it plays out will be the greatest macro trade of all time. How to take advantage? There’s a lot that investors can do, but Raoul believes that Coinbase and Tesla will both massively outperform next year, and Solana and Ethereum even more.

Edition: 175

- 08 December, 2023

Consumer Discretionary

Li Auto, one of Tesla's top EV rivals in China, beat expectations and set a new monthly record with over 40,000 monthly car deliveries in Oct 23. Soon after this new milestone was announced, Li's stock price popped 15%. The China data (Payments & Auto Insurance) from Sandalwood Advisors helped global investors track Li’s deliveries in real-time, and get an early signal on the strong momentum and better-than-expected results. If you never want to miss an inflection point, Sandalwood launched ‘Alpha Seeker’ which alerts clients to all major +/- trends in Sandalwood data.

Edition: 174

- 24 November, 2023

Where Street earnings are too high & who should miss

Wall Street analysts are too bullish on Q3 expectations for most S&P 500 companies. Although down from record highs set in early 2021, the percentage of companies whose Street EPS exceeds New Constructs’ Core EPS remains high at 71%. Furthermore, 208 companies (>40%) overstate Core Earnings by >10% (Street Earnings are overstated by 24% on average in TTM through 2Q23). New Constructs highlights Bio-Techne as one of the companies most likely to miss Wall Street analysts’ expectations in Q3. Others include Principal Financial Group, T-Mobile, Tesla and Xcel Energy.

Edition: 171

- 13 October, 2023

Renault (RNO FP) France

Consumer Discretionary

Woozle upgrades the stock to Buy following their latest interviews with dealers across Europe and the US - RNO prices are +6% Y/Y in 1Q23 following the launch of several higher margin midsized and compact vehicles in 2022. Volumes are +13% Y/Y (vs. consensus of -8%) driven by a 27% increase in sales in Europe, where RNO has gained market share and its Dacia Spring is now the second most sold EV in Europe, behind Tesla. Elevated raw material / energy prices, rising wage pressure and logistical problems are the main risks to look out for 2023. A lack of truck drivers in Europe was also flagged, but this has mostly impacted Volkswagen and Stellantis.

Edition: 158

- 14 April, 2023

Consumer Discretionary

Poised for recovery - now that the dust has settled on TSLA's Q4 numbers, Ben Z. Rose of Battle Road Research sees good things on the horizon for the company and reaffirms his Buy rating. He considers the most important catalysts to be the impact of the $7,500 federal EV tax credit in the US, expansion of its Austin and Berlin factories, production ramp of the Tesla Semi with an intriguing autonomous driving twist, the launch of the long-awaited Cybertruck, and the potential for a share repurchase. Ben reaffirms his one-year price target of $316, based on a 40x multiple assigned to his 2024 EPS estimate of $7.90.

Edition: 151

- 06 January, 2023

Consumer Discretionary

Chinese clean energy space looks attractive after the recent selloff - BYD is one of Sean Maher’s long-time preferred electrification plays and he is increasingly confident that by mid-late decade it will be worth significantly more than Tesla. BYD set another record month for sales in May and its all-new Seal model offers another revolutionary innovation - a CTB (cell-to-body) structural battery system. The share price is up 80% since Sean added BYD back into his Energy Transition basket (+240% since initiation); constituents added in the last 6 months include Air Liquide, Linde, LG Chem and SK Innovation.

Edition: 137

- 10 June, 2022

China: Lockdown depression

Tesla’s Giga Shanghai plant shut down for 22 days on March 28th and is still running at half capacity. It may be one factory, but Carl Weinberg sees it as a microcosm of a wider Chinese economy being massively unsettled by lockdowns. Since there’s a 1-2 month lag in shipping from China to most destinations, expect to see the effects very soon with the shock to supply chains bringing forth a profound global recession.

Edition: 134

- 29 April, 2022

Communications

The time has come to simplify its confusing sprawl of assets with a series of spin-outs - Tencent Games could replace Activision as the largest global game content stock, worth $150bn, and this excludes its vast portfolio of studios, IP and private stakes. While Tencent will likely be obliged to put Fintech into a standalone Holdco., this creates an opportunity to spin out Cloud & Business Services; potential to be a $10bn business by FY26. Major stakes in Tesla, Meituan, Sea and Kuaishou are not required / should be unwound. Importantly, by taking decisive action, it would make it less threatening to the government and limit the impact of regulation across the group.

Edition: 133

- 14 April, 2022

Consumer Discretionary

Trades at a ~5-turn multiple discount to Avis, with limited Sell-side coverage, and very attractive warrants ($13.80 strike price expiring 2051). This is a “classic bankruptcy re-listing” - strong new management team; B/S restructured with minimal debt; and renegotiated contracts on more favourable terms. Given the ongoing rental car shortage and robust industry backdrop, pricing will remain positive for at least another 18 months. HTZ’s recent order with Tesla for 100k EVs also gives it a first-mover advantage into electrification for rentals vs. peers. TP $35 (35% upside).

Edition: 125

- 10 December, 2021

Consumer Discretionary

Don’t get run over by this IPO - the proposed $80bn valuation is equivalent to the Mkt/Cap of General Motors and implies it will sell 3m vehicles in 2030, nearly four times the number of Tesla vehicles produced over the past 12 months. RIVN has yet to manufacture a meaningful number of vehicles and competes with well-capitalised EV upstarts as well as incumbents which have decades of experience and multi-billion dollar plans to expand EV production. The stock is worth $13bn at best (84% downside).

Edition: 122

- 29 October, 2021

Consumer Discretionary

Tesla China: July registrations dropped to 15-month low (-~70% m/m and -23% y/y). Signs of weakened Model 3 demand increasingly evident. After hitting a high of ~25K units in Mar ’21 (the month prior to when TSLA's controversies escalated in China) Model 3 regs have averaged ~10K over the past four months. Prices have been cut four times since Jan 2020. MIC Model Y regs were down -80% m/m and registered its second lowest monthly deliveries since Jan '21. The Model Y standard variant (newly launched on 8 July) was priced below expectations at 276,000 RMB.

SRR's data tracker for TSLA China includes insurance registrations by model and their proprietary tracking of TSLA's domestic superchargers network, pricing and lead time by model.

Edition: 117

- 20 August, 2021

Tesla (TSLA)

Consumer Discretionary

TSLA China analysis: SRR’s latest checks suggest recent controversies are taking a toll with NIO, XPeng and Volkswagen the main beneficiaries. Feedback from dealers was consistent - there has been a clear increase in cancellations and a decline in foot traffic. Prospective buyers are adopting a ‘wait and see’ approach which increases the risk for a downside surprise in registrations over the coming months. Combined with a significant narrowing of lead times for the Model 3 (1-3 weeks from 2-7) and Model Y (1-3 weeks from 3-9) leaves SRR very bearish on near-term prospects.

Edition: 111

- 28 May, 2021

CarMax (KMX)

Consumer Discretionary

The next General Motors? If GM can compete with Tesla, why can’t KMX compete with Carvana and become the largest online auto retailer? Management has set a goal of delivering $33bn in annual sales in Fiscal 2026 (~2m cars) which Northcoast believe could result in earnings as high as $12 per share. Shares to rerate higher as the benefits of its omni-channel strategy become more fully appreciated.

Edition: 110

- 14 May, 2021

Tesla (TSLA)

Consumer Discretionary

TSLA China analysis - will the recent product quality issues escalate to a level of a long-lasting scandal? Following a barrage of negative headlines at the same time as the Shanghai Auto Show was taking place (one of the most important marketing events for OEMs) the short term outlook is a concern and domestic brands look well placed to benefit. SRR will be closely monitoring the situation; conducting their own channel checks to gauge any material shifts in consumer perceptions over the coming months.

Edition: 109

- 30 April, 2021