Fortnightly Publication Highlighting Latest Insights From IRF Providers

Company Research

Venture Capital: Turning today’s dreams into tomorrow’s write-downs

KCR warns that today’s most speculative, unprofitable tech start-ups are hidden in private venture capital portfolios, not public markets. With VC valuations ballooning from $1.7trn in 2020 to $4trn today, they argue this mirrors the dot-com bubble - only this time, the risks are obscured. Many VC-backed companies can’t IPO because their valuations far exceed what the public market will bear. Worse, KCR highlights a surge in venture debt - often issued to unprofitable firms without equity backing. This debt-fueled demand props up Big Tech profits, echoing past financial manias. If failure rates hit the historical 75-90%, these holdings could implode, triggering ripple effects across tech markets. Click here to access the report.

Edition: 211

- 16 May, 2025

A secular bull market story

The Bloomberg Commodity Index’s weekly chart features a 20-month Rectangle that started forming some 15-month after the index peaked at 140.58. The BCOM fell 34% between 2022 and 2024, and Chris Roberts continues to view the rectangle as a base that will be followed by the resumption of the secular bull market that started in 2020. The monthly MACD has finally started to turn up. A number of commodities have set new all-time highs in recent months, including cocoa, coffee, copper and gold. Chris already has long positions in the latter two and is patiently monitoring other markets looking for buy set-ups. He is adding to spot silver longs this week. If the BCOM breaks out from the Rectangle, the measured move target is around 126.00.

Edition: 208

- 04 April, 2025

AI: The race to the bottom

One would have expected Anthropic’s latest innovation to be part of its premium tier, but the fact it is free is a sign that the race to the bottom, kicked off by Meta, is already underway. Richard Windsor sees it as a sign that the company is struggling to attract users to its platform in an already competitive environment. There are still no signs of the promised superintelligence on the horizon. Current expectations and valuations are unrealistic, and we will likely see the reset begin in the venture capital space as start-ups fail to meet their targets and go back to their backers for more money. Against this backdrop, everyone is going to take a hit, but the least pain is likely to be felt by Nvidia and TSMC. Richard prefers adjacencies of inference at the edge and nuclear power as the best way to get exposure to AI.

Edition: 194

- 06 September, 2024

InterContinental Hotels Group (IHG LN) UK

Consumer Discretionary

Willis Welby remains of the view that the UK has plenty of interesting and growing businesses. IHG features in their latest large cap growth screen - it has great financial productivity and is clearly winning market share. Dollar weakness does not help but the implied to Y3 EBITM ratio is just 84. It is too low. Hilton and Marriott are on 135 and 114, respectively. IHG would make sense GBP20 higher than it is now. Other stocks highlighted include QinetiQ (there is a good fundamental story here alongside some very cautious expectations. Despite a Q2 rerating, the implied to Y3 EBITM ratio is still only 65) and GlobalData (the disposal of part of the Health franchise may prove seminal. Management is talking organic growth >10%, margins drifting higher and accretive roll-ups).

Edition: 194

- 06 September, 2024

Consumer Discretionary

BABA’s transformation from China’s eBay to China’s Microsoft continues - the group’s AI strategy involves both the development of its open-source LLM model (Qwen), which has performed well on benchmarks in China, and investment in Chinese AI startups. This strategy has already proven successful with Moonshot and MiniMax developing popular AI applications. BABA provides these start-ups with credits that can be used for training or inference, which has driven growing demand for AI services on AliCloud. Although GPU supply is a constraint, Blue Lotus sees domestic breakthroughs in semiconductor equipment providing BABA with an avenue to expand its supply of AI compute and expects the group (and Tencent) to reinvent China’s software industry.

Edition: 193

- 23 August, 2024

Tracking the mutual funds tax selling

Quantitative Partners with Phil Erlanger Research

Geoff Garbacz thinks this might be the most important data point to follow to determine if we continue to see a stock market rally. Stocks vulnerable to tax selling include Boeing, Intel, Rio Tinto, Stellantis and UPS. Click here to watch the video which also includes the key levels to monitor on the S&P 500.

Edition: 193

- 23 August, 2024

Technology

Survey data suggests more friction converting customers to SaaS - ETR’s Technology Spending Intention Survey (TSIS) results have shown a 28-point Net Score decline over the past two years and preliminary July Net Score data puts VRNS as the second lowest among publicly traded security vendors. The company has executed its first SaaS transition phase well, but ETR’s data reflects declining spending intentions among existing customers it aims to convert. AI adoption is expected to grow the volume and complexity of enterprise data use, but ETR sees increasing competition from Microsoft, large security platform companies and AI-focused security start-ups.

Edition: 189

- 28 June, 2024

Discount Stores & Warehouse Clubs: Reading the prints

Consumer Staples

Gordon Haskett Research Advisors

In terms of set-ups and expectations, GHRA remains most bullish on Target and least optimistic on BJ's Wholesale Club at current levels. For TGT, they increase their 1Q24 SSS view to negative 3.5% and EPS to $2.00 with GHRA’s eyes focused squarely on comp cadence along with category trends in General Merchandise. Conversely, they lower their 1Q24 core SSS view on BJ's to negative 1.0%. They think the Street's $0.83 EPS forecast is too optimistic given that gas profitability has deteriorated, which alongside continued Capital One headwinds could weigh on profits. Looking ahead, they expect BJ's to back its FY24 EPS guidance of $3.75-$4.00, but management could indicate that the lower-band is more appropriate given some of the softness YTD.

Edition: 186

- 17 May, 2024

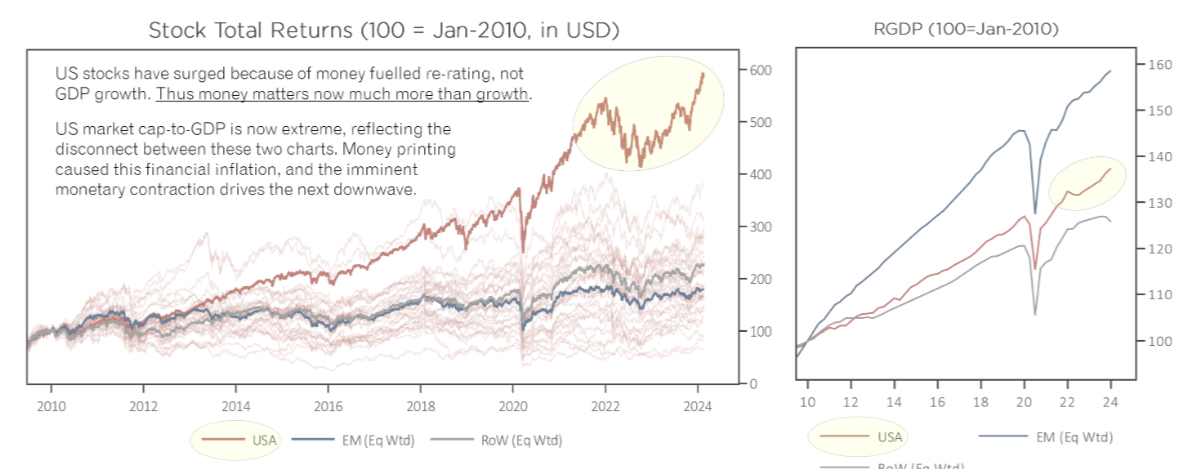

US: The next downwave

Whitney Baker comments on how 25yrs of central bank pricing in US and China drove once-in-a-generation bubbles in both place. The result is that assets have become tethered to central bank flows, rather than economic outcomes, and the huge size of the bubbles mean that central banks must slowly withdraw liquidity to avoid asset collapse. The market action through the unwind follows violent ups and downs, just like in 2020, but Whitney warns that this no-return volatility provides a smokescreen that hides a sideways lost decade or so for real returns on dollar assets, as economic cashflows inflate into them. This brings us to the US right now, where the pace of the Fed’s money creation is slowing fast and will start to contract in 2Q24, ushering in the next downwave in US assets. The most important thing is not US growth, it’s US liquidity, because that money disconnected asset caps from the economy and is alone sufficient to lead to a tactical bearish inflection.

Edition: 180

- 23 February, 2024

Artificial Intelligence: Lifecycle of a bubble

Technology

As more and more models are released by companies, start-ups and open source, the harder they will have to work to attract users, resulting in falling prices. The current mantra (and what companies seem to be raising money on) is that $20 per user/month is the benchmark and at this price, a lot of money will be made. However, Richard Windsor suspects the real price will be no more than $20 per user/year. This means that in 12 months when these new companies need to raise more money, they will have badly missed their targets and the long-term outlook will be lower. This is what pricks the valuation bubble and causes expectations and valuations to reset to reality.

Edition: 173

- 10 November, 2023

Artificial intelligence: Countdown to winter

The current exuberance around AI is simply not going to last, exclaims Richard Windsor. We’re in the 4th AI hype cycle, with the others occurring in the 1960s, 1980s and 2017-19, with each cycle represented by unrealistic expectations, FOMO, and the eventual collapsing valuations. Money is being thrown at start-ups with valuation and fundamentals being an afterthought. LLM models are popping up all over the place, which will put current services such as Chat-GPT under relentless pressure when it comes to their pricing models. Richard only has one AI investment in Palantir, and won’t touch anything else.

Edition: 164

- 07 July, 2023

Into the Minefield - Will private equity blow up in 2024?

Stephen Clapham has taken a look at private equity as he thinks that its meteoric rise over the last 20 years has largely been a product of falling rates and rising valuations. The next 10-15 years will prove a very different environment. He expects that there will be some big blow-ups in the PE space in the next 18-24 months, with mark to market becoming a contentious issue. As a result, private equity will find the going much tougher and pension funds with high allocations will suffer remorse.

Edition: 163

- 23 June, 2023

Technology

Inflection Point Research, LLC

NVDA's dominance in AI workloads, both in cloud computing infrastructure and other implementations, remains very much intact - Michael Fox believes the bevy of current start-ups will have a steep uphill climb to get any traction in high volume AI deployments (i.e. cloud), and while Advanced Micro Devices and Intel have competing solutions that look good on paper, both fall short in ecosystem and support. Ultimately, Michael expects the real competition for NVDA’s dominance will come from internal chip developments at the hyperscalers. Fortunately for NVDA, any true competition is years down the road.

Edition: 149

- 25 November, 2022

Space-based Earth Observation industry projected to be $27bn market by 2025

The inaugural edition of Quilty Analytics’ Earth Observation & Geospatial Quarterly Briefing series is kicking off with a report on the space-based EO industry followed by a deep dive into the expanding Synthetic Aperture Radar (SAR) imaging sensor market and the $500m+ in new capital it has seen since 2019 from start-ups including Capella Space, Iceye, iQPS, Synspective, Predasar and Umbra.

Edition: 127

- 21 January, 2022

Short Ideas: MYST’s clients generate impressive alpha

MYST hosted 23 Formal Events in 2021 which yielded 73 short ideas - 83% of these calls yielded positive alpha with ~21% average alpha over a 3-month period (12-month figs: 77% generated positive alpha with 21% avg. alpha). Ideas that remain compelling include:

United Parcel Service (UPS) - Multi-yr headwinds from increased competition, wage inflation and airfreight rate normalisation.

Elanco Animal Health (ELAN) - Questionable M&A strategy, bloated balance sheet and SEC probe to pressure results.

IPG Photonics (IPGP) - Anticipate precipitous ASP declines due to low-cost Chinese competitors.

Edition: 126

- 07 January, 2022

TFI International (TFII)

Industrials

With a string of acquisitions under its belt, management seems to have hit on a gamechanger in buying the UPS Freight Business. Q2 gave investors the first look at the operational improvements management can make to the assets and there is a lot more to come (highlights real estate potential / excess capacity can be used to create additional value). An underfollowed and underappreciated stock that bounced around for years, TFII was trading at ~US$39 when Veritas turned bullish last year, the stock now trades at $110, but plenty of upside remains.

Edition: 116

- 06 August, 2021