Fortnightly Publication Highlighting Latest Insights From IRF Providers

Company Research

Technology

Seeing strong growth from expanded product line and improved supply availability. Recent new product launches have boosted revenue and earnings, giving the company flexibility to allocate free cash flow beyond debt reduction. In Q4 results, Ubiquiti increased its dividend and announced a $500 million stock repurchase program. Investment in innovation and a broader portfolio opens opportunities for recurring subscription revenue, strengthening long-term growth prospects. With greater earnings power and shareholder-focused capital allocation BWS raise target price from $440 to $600.

Edition: 219

- 05 September, 2025

Communications Equipment: Earnings quality review

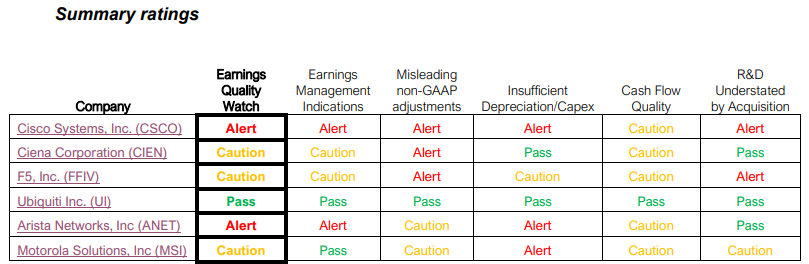

Communications

BTN’s Earnings Quality Watch industry reports provide readers with a quick way to identify the companies that are the most and least exposed to the risk of reporting disappointing results or guidance due to recent results being distorted by unrealistic, accounting-related benefits. Looking at the table above, only Ubiquiti received a ‘Pass’ rating in the Communications Equipment industry, while BTN sees meaningful risk that Arista Networks and Cisco Systems will disappoint on earnings in the next 2 quarters.

Edition: 190

- 12 July, 2024

Technology

Share price is up c.150% since Hamed Khorsand turned bullish (Oct 2019), but he still sees further upside following Q4 results where revenue smashed his expectations (up nearly 24% Q/Q). Enterprise Technology was only $2m away from its highest ever revenue performance, while Service Provider revenue grew by 56% sequentially. Demand remains healthy enough to put UI back on pace for potentially exceeding $500m in revenue in a single quarter. Hamed increases his FY23 revenue estimate to $1.9bn and forecasts net income of $446m. UI should manage to grow EPS by 20%+ (to $7.38) and potentially by as much as 27% in fiscal 2024.

Edition: 144

- 16 September, 2022

Technology

Sales have fallen for three quarters, from a growth rate of 51% last June to -23% in the quarter just ended. Margins have collapsed (gross margins down from 48% to 42% and EBITDA margins from 39% to 31%) and the company has added $1bn of debt since 2017. The share price is only down 13% YTD and is still 10% higher than a year ago. Eric Fernandez believes UI warrants a closer look as a potential short candidate with the stock trading at high multiples of both sales and earnings (46x Jun 22 and 35x 2023 earnings). Other companies flagged in Eric's ‘Breaking Estimates’ model are Nutanix, Upstart and Corsair Gaming.

Edition: 137

- 10 June, 2022