Fortnightly Publication Highlighting Latest Insights From IRF Providers

Company Research

Ready for the contrarian gold trade?

Cam Hui has been bullish on gold, but point-and-figure charts of gold and gold miners now show that they are either very near or have outrun their measured price objectives. Tactically, the contrarian trade would be to sell gold and buy bonds. However, a cycle analysis leads Cam to conclude that the market is undergoing a shift to a hard asset price leadership cycle. Cam’s base case calls for a multi-month correction and consolidation in the manner of the 2004–2006 experience, followed by a second rally to an ultimate top at much higher gold prices. It is within this context that a long-term point and figure objective of 9,800 is achievable in the next 3–5 years.

Edition: 223

- 31 October, 2025

Financials

OWS’s short thesis continues to play out as growth slows and profitability erodes. Total Written Premium (TWP) growth is decelerating, converging toward a long-term low double-digit rate, while management’s talk of 40% growth within five years appears unrealistic. Agent growth has stalled (+3.8% Y/Y vs. +11.1% last quarter) and productivity per agent has essentially been flat for 3 straight quarters. Meanwhile, operating costs per agent continue to rise, leading to margin compression that management expects to persist into 2026. OWS argues that GSHD’s franchise-heavy model is becoming less attractive to experienced agents and increasingly reliant on costly recruitment of new ones, leaving valuation vulnerable to further downside. TP $52 (25% downside).

Edition: 223

- 31 October, 2025

UK: Anatomy of a rolling fiscal crisis

Helen Thomas says that the totemic Caerphilly Senedd by-election loss for Labour coupled with the inevitable cost-free, protest-vote election of Lucy Powell for Deputy Leader could not have come at a worse moment for budget preparations and for PM Starmer. After the OBR delivers its final pre-measures forecast, Reeves will know what number is required to meet the fiscal rules. By Nov 10th, the OBR will deliver its initial post-measures forecast - essentially a judgement on whether Reeves's shopping list of measures will pass muster. If not, there will be more HMT/OBR back and forth until it does. Except the shifting political landscape means that this is no longer just an optimisation problem between two economic institutions. Helen says that for the embattled prime minister the situation looks terminal, and Starmer will be gone within months, as a result of challenge to his leadership by those in the Labour Party who now oppose him.

Edition: 223

- 31 October, 2025

Materials

EM Spreads initiates coverage on Braskem with an Overweight recommendation. They believe the company’s large domestic footprint, political relevance and partial government ownership make a default event less likely near term, but the credit now hinges less on fundamentals and more on political and strategic decisions involving Petrobras, the federal government and Braskem’s ability to strengthen liquidity. They see asymmetric risk-reward at distressed prices, with outcomes contingent on a secured-liquidity bridge, PRESIQ approval, direct support measures and broader policy backing for Brazil’s petrochemical sector. They favour exposure to the lower-priced bonds within the curve for better downside protection and see greater value in the 2030s at $38.3, 32.1% YTM, 3.1-yr duration.

Edition: 223

- 31 October, 2025

Debt Risk Monitor

TT has launched their first Debt Risk Monitor, highlighting 53 companies across Europe and the Americas, that have been flagged by their proprietary tool as potential debt risks. Previously integrated within TT’s accounting risk framework, the new monitor flags firms where debt concerns exist regardless of whether they see any other accounting issues (i.e. earnings manipulation). The tool detects signs of hidden on- and off-balance-sheet debt, an approach that previously identified Steinhoff and NMC Health ahead of their collapses. Similar to the accounting risk score, the higher TT’s debt risk score, the more indication they have that companies have hidden debts. Clients can access the full monitor, covering 7,500+ listed companies, via TT’s website, alongside historical data, background reports and ongoing monthly updates.

Edition: 223

- 31 October, 2025

DCC (DCC LN) UK

Energy

Following publication of the company's FY25 annual report, Iron Blue increases their DCC rating +3 pts to 27/60 (newly top quartile / fertile grounds for shorting). Key changes vs. FY24: 1) Higher one-off costs: FY25 stripped out restructuring expense increased to 7% of PBT adj, highest in 7 years. DCC also stripped out from headline earnings £74m goodwill impairment. 2) Took £17m profits on disposal of PPE inside underlying profits in FY25, the highest figure in the past decade. 3) P&L expense for inventories write-downs dropped to a decade-low of £5m. 4) DCC continued its strategy of promoting top management from within, with internal promotions to the CFO and newly created COO roles. 5) In its principal risks assessment, DCC highlighted Y/Y risk increases concerning the DCC Technology strategic review and also the impact on its operations from higher tariffs.

Edition: 222

- 17 October, 2025

UK: A governing party in denial

Helen Thomas sums up the Labour Party Conference with one word: denial. Denial about the scale of the economic challenge, the breadth of discontent within the party and the country, and what must be done to resolve the situation. The message of the conference was that we are in "a fight for the soul of our country", with Starmer pitching himself against Farage. Despite Andy Burnham rowing back on his ambitious coup attempt, everyone is discussing who the replacement for Starmer will be. Meanwhile, Chancellor Reeves is fighting the Gilt market daily for her political life, but she is in denial about what is required. Helen says that we remain in a hiatus ahead of the budget, where even the Chancellor doesn't know yet what will be in it on 26th November, in part because she does not yet know how the Office of Budget Responsibility (OBR) will model her choices.

Edition: 221

- 03 October, 2025

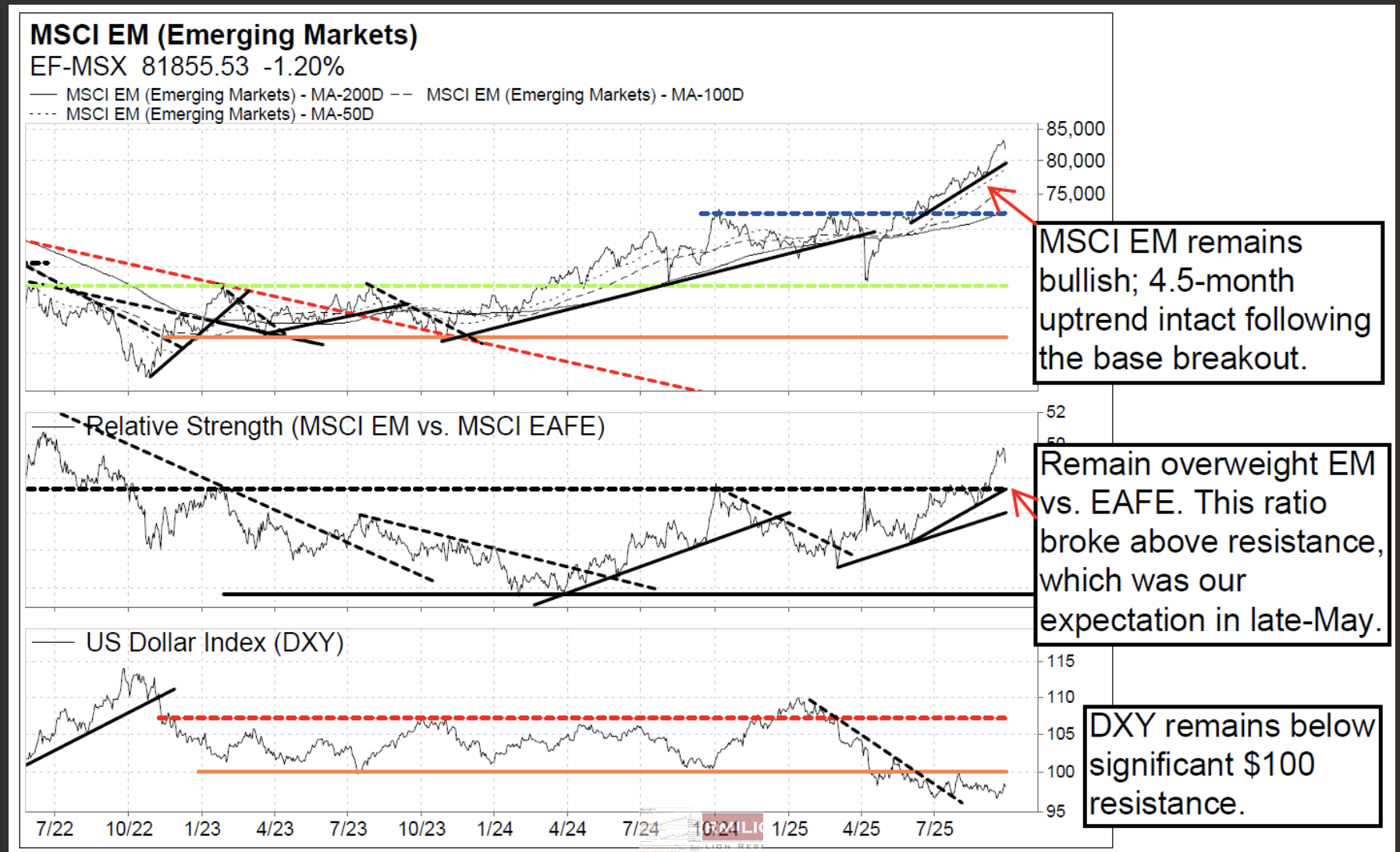

Remain overweight Taiwan, China and Korea

According to David Nicoski, the MSCI Emerging Markets index (local currency) and EEM-US (USD) are both trading within 4.5-month uptrends, and he remains bullish. David expects support at the uptrend, which also coincides with the 50-day MA and $50.65 horizontal support on EEM-US. He would view any pullback to $48 support on EEM-US as a buying opportunity. For EM countries, while price remains attractive, he is downgrading Greece to market weight due to RS deterioration. EM countries where he remains overweight include Taiwan, China, and South Korea. Additional leadership countries include Vietnam, Romania, and Pakistan. For EM sectors, defensive EM sectors (staples and utilities) continue to underperform and are at YTD RS lows; underperformance has continued, as expected -- avoid. Meanwhile, attractive EM sectors where David expects outperformance include: MSCI EM technology, consumer discretionary, materials, and communications. He is also monitoring for a RS bottom on EM health care.

Edition: 221

- 03 October, 2025

Deutsche Boerse integrates social media intelligence in market surveillance software

While Deutsche Boerse has been an early adopter of social media monitoring for years, they have now taken the critical step of integrating Stockpulse's social analytics directly into their core Scila surveillance system. This integration provides comprehensive monitoring of 70,000+ global equities and cryptocurrencies with real-time social sentiment analysis, buzz metrics and seamless workflow integration within their mission-critical market oversight platform. This signals a broader trend toward holistic market surveillance encompassing trading data, news feeds and social sentiment. As social media increasingly shapes market dynamics, similar integrations are likely to follow globally. For investors, Stockpulse's insights into social sentiment, help spot emerging risks and opportunities before they hit the market. Contact us for a free trial / demo.

Edition: 221

- 03 October, 2025

US: Shutdown

With just over two weeks left until the US government runs out of funding, the odds of a government shutdown are rising. Unlike recent funding cliffs, both sides are facing competing political incentives to push the funding debate to the brink. At the heart of the issue is the backlash within the Democrats over the last government funding fight. Senate Minority Leader Schumer and a handful of Democratic senators ultimately supported the bill, believing that staving off a shutdown was the least bad option, resulting in weeks of backlash over his decision. Although government shutdowns are often averted at the last moment, there are reasons to believe a last-minute deal won’t materialize this time around. In this case, Democrats believe their healthcare-focused message is a political winner while the GOP believes that offering Democrats a clean funding bill and letting them vote it down will put the blame for the shutdown squarely on them.

Edition: 220

- 19 September, 2025

Compounding at the curb

Industrials

The waste sector has proven to be one of the most durable compounders in the industrials sector. Essential services support stable cash flow across the cycle, reinforced by pricing discipline and steady volumes. Growth is amplified through ongoing consolidation and optionality in RNG and EPR. Within this backdrop, Veritas sees diverging investment cases for Waste Connections and GFL. WCN, with modest leverage, FCF conversion returning to 50% post-RNG build and balanced capital returns, offers steady compounding. Attractive end-market exposure and visibility to double-digit FCF growth support a premium valuation and Veritas’ Buy rating. By contrast, GFL has ~70% more FCF growth priced in than peers, while longer-term margin and FCF convergence remain uncertain, particularly vs. a structurally advantaged peer like WCN. Accounting adjustments add complexity and LFL comparisons highlight its shortfall vs. larger peers.

Edition: 220

- 19 September, 2025

DR Congo: Murmurs in the military

The military prosecutor indicated that the state has sought prison sentences ranging from three to 15 years for 40 military officers accused of plotting a coup. The military officers were arrested in April, after being filmed at a hotel declaring an end to President Felix Tshisekedi’s governance and stating that they would seize power. The development comes on the back of scores of arrests of military officers in recent months for various alleged infractions. While the risk of a coup in the near term is considered low, the risk will escalate to moderate over the longer term, particularly as the 2028 elections approach. If Tshisekedi fails to resolve the M23 conflict, it will likely worsen lingering public grievances with the statesman. This could undermine Tshisekedi’s position within the ruling Sacred Union coalition and the military, and may even lead to elections being cancelled.

Edition: 219

- 05 September, 2025

UK: Under the weather

Mark Bathgate’s exceptional level of dialogue and understanding of Westminster/Gilt markets has allowed him to accurately call changes over the past few tumultuous months. Mark warned clients through May and June that Labour MPs were unwilling to accept any curbs on welfare spending, and hence a much larger deficit, gilt funding needs and tax cuts would be the main political and market talking points for the second half of the year. He sees the upcoming Autumn budget being dominated by an internal debate within Labour over which taxes to hike, which will play out via media leaks until a last-minute resolution. There is little reason to expect a change from the story of excess inflation, overshoots in borrowing needs, higher taxes and weak household real income growth and spending. Hence, the market trend to higher long term gilt yields and underperformance of other DM sovereign bond markets is well founded, and investors should expect no reason for change.

Edition: 218

- 22 August, 2025

Communications

Blue Lotus expects Tencent to beat 2Q25 revenue, IFRS operating profit and net income forecasts, supported by success in the extraction shooter genre, which has exploded in popularity within the Chinese market recently. Tencent’s Delta Force has surged from ~5m MAUs in Jan to 38m in July, making it the company’s 3rd largest game. Arena Breakout is also proving to be extremely popular. While both Tencent and NetEase have blockbuster titles in development, the former appears to be moving faster - likely due to its generative modelling strengths. With upside to valuation and near-term catalysts, Blue Lotus names Tencent as their Top Pick in the gaming sector.

Edition: 217

- 08 August, 2025

Quantum computing primer unveils two new Buy ideas

Technology

Rosenblatt initiates coverage on D-Wave (Buy, $30 TP) and IonQ (Buy, $70 TP), identifying them as differentiated, high-conviction ideas in the rapidly expanding quantum computing market. QBTS offers unique exposure to quantum annealing - particularly suited for optimisation workloads - and is expected to grow revenues at a +66% CAGR from 2025-2030. IONQ, a leader in trapped-ion architectures, is positioned to exceed $1bn in revenue within the next few years, with significant upside from its product roadmap and ecosystem development. These initiations are framed by Rosenblatt’s comprehensive quantum computing primer, which outlines the core principles, architectures and commercialisation pathways shaping the industry’s next era and underpins the firm’s bullish stance on both names.

Edition: 217

- 08 August, 2025

Materials

GMR maintains a Buy rating on NST following their KCGM site visit, reaffirming the mine’s Tier 1 status with a US$6.7bn NPV5 valuation. The A$1.5bn expansion remains the key near-term focus and risk, but appears on track for completion within 12 months. While the market remains concerned about lower near-term FCF and high capex (~A$500m/year), GMR sees KCGM as strategically critical, with meaningful upside from displacing low-grade stockpiles with higher-grade ore, improving mill throughput and ramping up the Fimiston underground. The mine’s long life, production growth potential (to 850-900koz by FY29) and exploration upside through high historical OVMs make it NST's crown jewel, but successful delivery in the near term remains crucial for realising that value.

Edition: 217

- 08 August, 2025

Technology

Despite a solid Q3 beat and raise, MU shares fell on misplaced concerns over HBM oversupply. Arete sees strong FY26 growth, with HBM projected to reach ~40% of DRAM sales by late 2026, reinforcing MU’s status as an essential yet still undervalued AI stock. Nvidia continues to request additional HBM and potential resumption of H20E (with HBM3E-8Hi) sales could act as a catalyst for further global supply tightening. MU must demonstrate HBM4 competitiveness (16-layer stacking capability) within 6-8 months to ease investor concerns. Arete also expects MU to gain eSSD market share at the expense of Samsung and SK Hynix. A combination of stable traditional DRAM pricing and rising HBM mix to drive a 63% Y/Y rise in FY26 EPS to $12.78. TP increased to $150 (35% upside).

Edition: 216

- 25 July, 2025

Technology

Forensic Alpha has raised PAYX’s risk score to the highest level (10/10), citing a sharply rising trend in DSO as a key flag in the company’s latest 10-K. The increase stems from significant growth in “Purchased Receivables” tied to PAYX’s Funding Solutions business, which provides non-recourse payroll advances to staffing agencies. These receivables rose 23% Y/Y to $1.2bn, now ranking among the largest items on the balance sheet. Given its growth and size, Forensic Alpha was surprised there is only one passing reference to it within the investor presentation and no mention of it on the Q4 earnings call. Changes in cash flow presentation and more optimistic revenue recognition assumptions further raise concerns about transparency and earnings quality.

Edition: 216

- 25 July, 2025

Iron Ore: Higher prices, but still within medium-term trading range

Recently SGX 62% iron ore futures initially traded to lows of US$98.00/t CFR China in response to the release of a plethora of disappointing macroeconomic data. That said, there were several indications that some policy measures would be introduced soon to cut back overcapacity. Although the government's intentions will have a negative impact on China's iron ore consumption, the positive impact on Steel margins has counterintuitively dragged iron ore prices kicking & screaming higher. Accordingly, Atilla Widnell has updated his short-term target to US$100.14-101.55/t CFR China. As to the medium-term outlook, markets are entering a period of seasonably tighter iron ore supply through the third quarter. Atilla can't see how 62% iron ore futures trade outside of the current range unless there's a material black swan event. As such, he is only tightening the upper boundary given that he feels the upside potential is relatively limited, maintaining his medium-term outlook to US$95.70-105.15/t CFR China for Q3 2025.

Edition: 216

- 25 July, 2025

Orsted (ORSTED DC) Denmark

Utilities

Tom Beevers of Forensic Alpha pitched ORSTED as a short at our latest Best Equity Short Ideas Conference, arguing that the company’s balance sheet is materially weaker than the market appreciates, with true leverage significantly higher than reported and free cash flow overstated. The stock scores a maximum 10/10 risk rating on Forensic Alpha’s platform, which leverages proprietary machine intelligence to detect red flags buried within financial statements and governance disclosures, across 35 risk categories. Click here to listen to Tom's presentation and here to access the slides.

Edition: 215

- 11 July, 2025

Industrials

CAT ranks among Two Rivers’ top short ideas within its Declining Business Model framework. Despite deteriorating fundamentals, the stock trades at historically high multiples - over 20x 2025 earnings. Sales have declined for multiple quarters (-9.8% in Q1), estimate revisions remain deeply negative and margins are rolling over from peak levels. Working capital is rising. Finished goods are slowing. Forecasts project cash balances to dwindle on large maturity payments leaving the company with a negative cash position without refinancings. At the last earnings release, CAT missed on the sales, EBITDA and earnings lines.

Edition: 215

- 11 July, 2025

China: The RMB’s implicit trading range

William Hess points out that under PBoC’s rigid dollar peg the path for USD/CNY has increasingly resembled that for USD/HKD, with upper and lower trading bands. William expects renewed USD weakening, given that the ongoing trade talks are not sufficient for PBoC to abandon its current target range. His team predict that the Bank will likely allow +/- 2% movement in USD/CNY relative to its daily fixing. Elevated trade tensions and external uncertainty will only reinforce PBOC’s commitment to defending this trading band. Moreover, PBoC’s management of moves to USD/CNY within this trading band appears to be asymmetric. The Bank appears to be more stringent with defending the trading band and daily fixing when the RMB is under greater pressure to depreciate. Against this backdrop, William believes the PBoC will continue to confine USD/CNY to the 7.05-7.35 range for the rest of this year while the RMB depreciates against the CFETS currency basket ~10% by year end.

Edition: 213

- 13 June, 2025

Vista Energy (VISTAA MM) Mexico

Energy

EM Spreads recommends buying Vista’s new 2033 bonds, citing an attractive 8.5% yield and shorter duration relative to the 7.625% 2035 notes (yielding 8.3%). The bonds offer a more compelling return within Vista’s debt capital structure and screen wide relative to the broader EM BB and LatAm BB curves. Strong execution on well tie-ins and midstream expansion supports the group's ambitious EBITDA and production targets. EM Spreads views Vista as a top credit pick for exposure to Argentina’s energy sector, with relative insulation from sovereign risk. They believe operational momentum and an improving macro backdrop, including easing capital controls, could drive bond outperformance over the next 9-12 months.

Edition: 213

- 13 June, 2025

Technology

Trivariate flags PLTR as one of the most compelling short ideas ahead of the June 2025 index rebalance. Having surged nearly 5x since mid-2024, PLTR now trades at a $291bn m/cap and an eye-watering 73x EV-to-forward sales - making it the second most expensive US non-biotech stock with over $50m in revenue. Historically, stocks trading above 30x EV/sales fall to 18x within a year and underperform the market by an average of 22.5%. With PLTR comprising over 8% of the mid-cap growth index, a shift into the large-cap universe will likely trigger major selling pressure. Unless you believe PLTR can grow faster and longer than any company has ever grown, selling now and shorting near June 30th is the logical strategy.

Edition: 212

- 30 May, 2025

Chemicals: Is the worst behind us?

Materials

Frank Mitsch sees early signs of stabilisation in the chemicals sector, despite short interest sitting at 52-week (or longer) highs and persistent investor concerns around potential dividend cuts. While he remains cautious on Tronox and Huntsman’s payouts, he considers dividends from Dow and LyondellBasell to be safe. Roughly 60% of 1Q results landed within 4% of his expectations, with Olin, Corteva, FMC and Celanese leading on beats vs. the Street. Westlake was the notable miss, due to underperformance in its PEM segment, partly from unplanned downtime. After over two years of sector underperformance, exacerbated by the overreaction to Liberation Day, Frank believes the worst may be behind us; hence his recent upgrades (to Buy) on DOW, LYB and PPG. He has also been heartened by how the credit markets have been open to companies such as CE and OLN.

Edition: 212

- 30 May, 2025

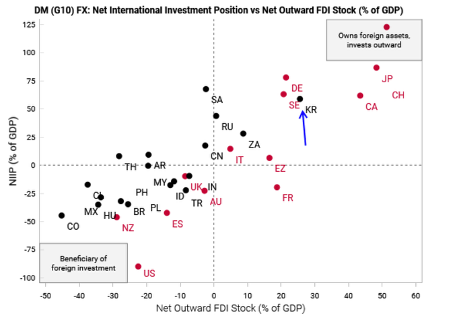

Korea: Taking the long view

South Korea is a less extreme version of Taiwan, where current account surpluses have also been recycled into US assets. Despite persistent current account and basic balance surpluses, the KRW real effective exchange rate is very weak, making Korea an outlier within EM. The country’s net international investment position is very large relative to GDP at 60%+, which is also reflected in the balance sheet. Similar to Taiwan, the BoK has been accumulating foreign assets and partially sterilising since the GFC, and just like Taiwan, the KRW may appreciate as these decade long structural imbalances start to normalise. To help control for the carry of a long KRW position, the Variant Perception team like shorting CNH against a long KRW position.

Edition: 211

- 16 May, 2025

Communications

SoftBank to invest up to $40bn in OpenAI starting with a $10bn tranche this month of which it will fund 75% itself. It will source the funds from Mizuho Bank although the group has sufficient cash on hand already. SoftBank's LTV ratio increases from 12.9% at Q3 end to c.17%. It should be able to raise up to $46bn in funding through asset-backed finance and borrowing up to the 25% LTV level relative to commitments of c.$47bn (OpenAI, Ampere, Aug payment to SVF for ARM and the initial Stargate push). SoftBank will probably lose money this quarter but not so much it doesn’t end the year in the black. Vision Fund was down $1.1bn, largely on India weakness (-$1.2bn across its four public investments) with the rest of the portfolio moving sideways. The discount to NAV has widened slightly to 55% but remains well within the recent trading range. TP ¥11,000 (65% upside).

Edition: 208

- 04 April, 2025

US: Liberation Day

The swathe of tariffs was worse than expected, and Gerard Minack says that lower tariffs must be negotiated within the next few weeks to prevent a serious knock to growth. Whilst a recession is possible, it’s not yet Gerard’s base case, and markets are wrong to expect Fed intervention otherwise. He also expects double-digit percentage declines in both US and non-US equity markets. As is to be expected, treasuries will rally as equities fall, but the gains may not persist. If inflation concerns limit the Fed’s ability to ease, long-end rates will start to rise as short-rate markets take out the cuts that are now priced. Moreover, treasuries will have to cope with large ongoing deficits. Just as equity investors are now realising that the strike on the Trump put is lower than they expected, treasury market investors may also recognise that any Bessent put is almost as worthless.

Edition: 208

- 04 April, 2025

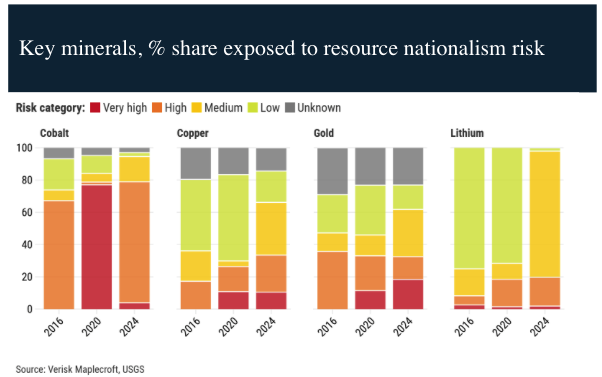

EM: Taking control

Emerging markets are home to a swathe of critical miners, including cobalt, copper, gold and lithium. According to Verisk Maplecroft’s Resource Nationalism Index (RNI), which measures government control of economic activity within mining and energy, 47 EM countries have registered a significant increase in the last five years. If this momentum continues, disruption to the supply of critical minerals for the renewables, tech and defence industries is probable. Some EMs will attempt to leverage their reserves in the wake of increasing geopolitical competition, implementing a wide range of measures including tax and rent hikes. Over the next few years, expect an increasing of number of related policy announcements in both producer and demand countries.

Edition: 208

- 04 April, 2025

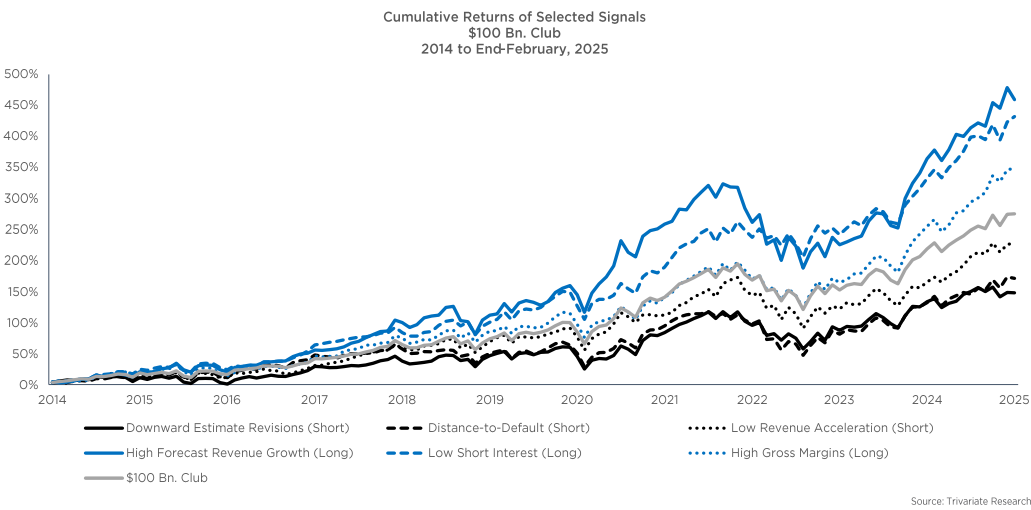

Which stocks >$100bn m/cap are buys now?

With investors searching for value in the current market sell-off and likely looking to buy names among the safer, larger cap universe, Trivariate has assessed the performance of several metrics within the stocks >$100bn m/cap to see if they could systematically pick winners from losers. The best performing signal over the last 10 years, was buying the companies in the top third of forecasted revenue growth, while the second best was buying the one-third of companies with the lowest short interest. The worst performing signals were those in the highest third of leverage and stock volatility (distance-to-default) and those with the worst third of downward earnings revisions. Current long ideas from Trivariate’s $100bn Club Framework include all the Mag 7 (except Tesla), as well as Eli Lilly, Visa and UnitedHealth. Shorts include Goldman Sachs, PepsiCo, Caterpillar and Starbucks.

Edition: 207

- 21 March, 2025

US: Cash is king

Despite a much hyped and universally expected decline in the TGA, Andrew Hunt’s measures of financial liquidity are in general weak. Surging R/P lending activity may be a sign of rising strains within the financial sector. Credit quality may be deteriorating. It is early days, but these signs deserve close monitoring. The rate of tightening in fiscal policy has slackened as DOGE has lost momentum. It seems that rising credit demand in the real economy has left banks with “less money” to lend to the financial sector. Rather than “crowding out” the real economy – as has frequently been the case over recent years - the financial sector could be being crowded out by rising credit demand from the real sector. This de-financialization could leave asset markets vulnerable. US banks are retreating aggressively from foreign markets. Andrew is negative the USD on a six-month view given the US’s reliance on foreign inflows.

Edition: 207

- 21 March, 2025

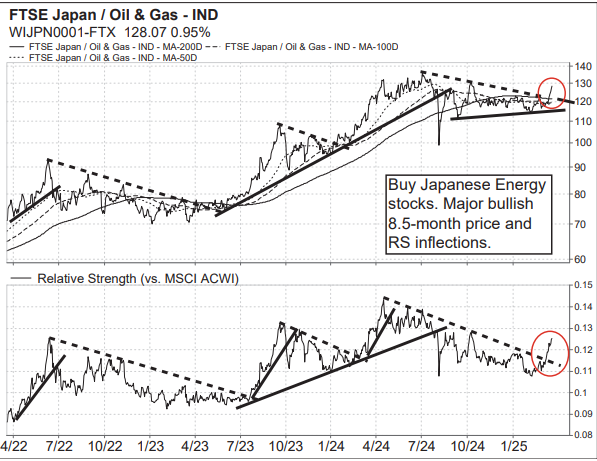

Japan is breaking out: Buy Energy stocks

Energy

The TOPIX and Japan Hedged Equity ETF are breaking out following 5+ months of consolidation. Japanese Financials have been the leading sector in Japan for quite some time; Vermilion has been bullish for nearly a year and it has been the only Japanese Sector that they have been widely recommending ever since the TOPIX breakdown in Jul/Aug 24. However, over the past 1.5 months, the Energy Sector within Japan has also been leading the charge higher and outperforming. The FTSE Japan Oil & Gas Sector now displays bullish 8.5-month price and relative strength inflections. Actionable names include Idemitsu Kosan, JAPEX, INPEX and ENEOS.

Edition: 207

- 21 March, 2025

LVMH (MC FP) France

Consumer Discretionary

In the past 20 years, Pierre-Olivier Essig has never seen as many red flags surrounding LVMH as he does today. In addition to terrible 4Q24 numbers, he highlights succession change, brand fatigue, low value retention, supply chain ethics, designer casting mistakes, unjustified pricing, as well as specific issues attached to almost every division. Pierre faced huge resistance from clients 12 months ago when he advised selling LVMH shares at €822, however, that proved to be the correct decision and in Oct, he then upgraded the stock to Buy after it fell through €600. With the share price having recently moved back above €700, Pierre turned bearish once again. He expects Hermes m/cap will exceed LVMH’s within the next year.

Edition: 206

- 07 March, 2025

Intercontinental Exchange (ICE)

Financials

2Xideas publishes deep-dive research on compounding stocks that have the potential to double within 5-7 years. Their latest report focuses on ICE, which has the following key opportunities to drive continued growth and operating leverage: 1) To win share of institutional client workflows as fully automated trading proliferates. 2) Drive growth across its energy franchise with products such as Environmental Futures or Dutch TTF Natural Gas contracts, while continuing to innovate around new products such as carbon allowance credits. 3) Drive a digital‑to‑analog shift in the mortgage origination process, consolidating the mortgage value chain and building marketable mortgage trading and data products in the process. In aggregate, 2Xideas forecasts a 5.3% revenue CAGR and 11.5% adjusted EPS CAGR through 2030E on an NTM P/E of 20x.

Edition: 206

- 07 March, 2025

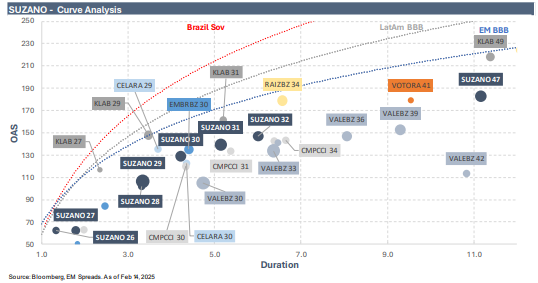

Materials

Despite additional industry supply, tight market conditions persist due to low stock levels, maintenance-related production cuts and operational disruptions. Healthy pulp prices, higher sales volumes, controlled costs and a focus on deleveraging should support Suzano’s cash generation and credit profile in 2025, with this trend likely continuing as no major new supply is expected. Within Suzano’s capital structure, EM Spreads prefers the 3.750% 2031 and 3.125% 2032 bonds, which compare favourably to select regional peers, the broader EM BBB Index, and the US BBB Index. Additionally, these notes trade below par at $90.1 and $84.6, respectively, while most of Suzano’s curve remains priced above par.

Edition: 205

- 21 February, 2025

Can Bitcoin reach $160,000?

Bitcoin prices have surged $50,000 since the BTC ETF launch, putting it on track to potentially reach the $140,000 - $160,000 target by the end of 2025. Markus Thielen points out that $142 billion has flowed into the crypto market, demonstrating how feasible this price movement is. However, despite bullish narratives around a potential strategic Bitcoin reserve or sovereign wealth fund acquisitions, Bitcoin’s upside remains tied to capital inflows. Matching this level of liquidity in 2025 will be challenging, which may limit BTC’s price trajectory within this range. Markus also calculates the Bitcoin Terminal Price at $190,847, advising investors to take profits should it reach this level.

Edition: 205

- 21 February, 2025

Healthcare & Trade Tariffs: Rising costs, disrupted supply and industry response

Healthcare

The trade tariffs imposed by the Trump Administration are expected to raise healthcare costs, disrupt the supply chain and make care less affordable for patients. Companies are trying to mitigate these issues through initiatives such as on-shoring manufacturing and sourcing from unaffected countries; however, these measures face regulatory challenges and will require time to implement. Within the medical devices and hospital supply sector, the impact of these tariffs varies among companies. For instance, Johnson & Johnson, Medtronic and Intuitive Surgical have manufacturing exposure in China and Mexico, whereas Boston Scientific and Edwards Lifesciences do not. MedMine monitors spending on medical devices and hospital supplies at ~3,000 hospitals and related healthcare providers across the US, providing valuable insights into the effects of these tariffs.

Edition: 204

- 07 February, 2025

Oil: Pressure on all fronts

Oil prices rallied above $80 in the last fortnight after news of a major US sanctions package targeting Russian oil plus expectations of disruption to Iranian supply. Niall Ferguson believes that the impact on Russia is material, taking around 400,000 barrels per day (bpd) off the market, although he expects Russian flows to normalise gradually as workarounds are found. The US is also likely to take ~500,000 bpd of Iranian exports offline. Nonetheless, as the Russian and Iranian oil affected represents less than 1% of global oil demand, Niall thinks oil prices will still trend downwards throughout 2025, given the weak demand growth outlook, strong non-OPEC supply and the increasing risk of a price war launched from within OPEC.

Edition: 203

- 24 January, 2025

Short Attacks: Carvana (CVNA) & FTAI Aviation (FTAI)

Forensic Alpha’s analysis finds an overlap of several issues highlighted in Hindenburg Research’s meaty report on CVNA “A Father-Son Accounting Grift for the Ages” - in particular related-party transactions with DriveTime and off-balance sheet risk. Commenting on Muddy Waters' new short report on FTAI, they note that using transfers to inflate profits within a “prize division” is a common shenanigan - Forensic Alpha recently raised similar concerns around CRH and Volkswagen. Their own analysis of FTAI classifies the stock as “High Risk”.

Edition: 203

- 24 January, 2025

The story for 2025

Last week, Andrew Hunt noted that inflationary pressures within the non-traded goods sectors remain elevated, largely a result of the huge cyclically-adjusted budget deficits that many governments continue to run. These deficits also imply that net public debt issuance will exceed household saving by a considerable margin this year. If governments cannot embrace growth-sapping austerity, they will need to either accept higher yields to attract foreign savings / crowd out domestic investment, or return to some form of de facto QE and yield curve control. Ultimately, Andrew expects the latter to occur but not before a further rise in bond yields over the next 3 – 6 months that tips the Global Economy into a recession, while also undermining equity and credit valuations. He then expects a panicked and aggressive easing of global monetary policy in H2/2025.

Edition: 202

- 10 January, 2025

Nigeria is showing signs of life & Banks are 2x earnings

Financials

Recent progress within the country has been helped by two Eurobond sales last month (the first in nearly three years) for a combined US$2.2bn, stable interest rates and - shockingly - a rebound in the currency. If/when the devaluation stops, the entire economy can explode higher in USD terms via the natural equilibration of street prices back up to normal levels in real terms. Mike Churchill has been running the rule over some of the Nigerian banks and insurers including the likes of Access Bank, United Bank for Africa and Zenith Bank, with each one offering massive upside as well as double digit dividends.

Edition: 202

- 10 January, 2025

Gold: Rangebound in a consolidation phase

According to Sohail Yousaf gold continues to exhibit range-bound behaviour, with critical resistance at $2,660 and support firmly positioned at $2,630. A breakdown below $2,630 could trigger a deeper correction, targeting $2,560 as the next major support zone. The broader bearish outlook remains intact, particularly as gold trades below the descending trendline, highlighting the persistent downward pressure. As Sohail forecast earlier, the $2,450-$2,480 level could be a key area for accumulation before another potential bullish leg upward. Price action within this range suggests a cautious approach until a breakout occurs. Alternatively, a selling opportunity can be considered from the current price level, but with a strict stop-loss just above the descending trendline. This strategy ensures protection against potential breakouts while allowing for participation in the prevailing bearish momentum. Patience is key.

Edition: 201

- 13 December, 2024

Kerry Group (KYGA ID) Ireland

Consumer Staples

Iron Blue initiates coverage on KYGA with a score of 28/60, which is top quartile and fertile grounds for shorting. Accounting concerns highlighted include: 1) A significant increase in stripped out restructuring expense over the past three years. 2) FY23 PPE capex exceeded depreciation by 9% of PBT adj. 3) 12.6% tax rate is lower than suggested by the geographic profit split and could see risk from Pillar Two. 4) Discount rates for pension liabilities and the goodwill impairment test both seem less conservative than average. Re. governance, they note a 21-year average KYGA career within the leadership team, a nationality mismatch with the group’s geographic mix and a CFO who previously was lead auditor on KYGA.

Edition: 200

- 29 November, 2024

Playing the Trump card

The outcome of the US election creates a tough backdrop for ESG strategies, but it is far from being the death knell. Indeed, Trump’s first term was an excellent time for many thematic sustainability funds and many equity sectors moved contrary to consensus expectations – this trend could repeat over the next four years. Companies that have benefitted from deglobalisation, such as those involved in building domestic supply chains, will continue to thrive in the years ahead. Sustainability-focused investors should look for industrial companies that generate most of their revenues within the US and support resource efficiency, climate adaptation and automation, as these will be in high demand (see table for some examples).

Edition: 200

- 29 November, 2024

India: Adani indictment may prompt domestic and geopolitical ripples

The US Department of Justice has indicted Gautam Adani and seven associates for allegedly orchestrating a USD 265mn bribery scheme, raising concerns over transparency and compliance within India’s corporate sector. Domestically, opposition parties have renewed their criticism of cronyism involving the Adani Group, but political complexities make directly blaming the Bhartiya Janta Party-led government difficult. The indictment and its fallout threaten India’s global economic ambitions and could strain India-US relations, adding to existing tensions over trade and geopolitical alignments.

Edition: 200

- 29 November, 2024

The South-South trade

The share of South-South trade has risen steadily over the past two decades, now exceeding 50% of total trade turnover in the EM universe. However, Jonathan Anderson points out that this is all due to China. If the country is excluded, the internal share of trade between the rest of EM has actually fallen. Jonathan claims that China is a coloniser, not a leader. It likes to portray itself as a partner for mutual growth, but the opposite is true. Its relationship with the rest of EM is marked by a rapidly increasing surplus within the South and an overwhelming level of purchases for raw materials while selling higher volumes of industrial products – effectively using the South as a “vent for surplus”.

Edition: 199

- 15 November, 2024

Cemex (CEMEXCPO MM) Mexico

Materials

EM Spreads downgrades Cemex to Market Perform - weaker than expected 3Q24 results, alongside macroeconomic uncertainties in Mexico, dependency on uncertain US-Mexico relations and foreign exchange risk add pressure to the credit story. For EM investors, EM Spreads prefers Cemex 5.20% 2030 bonds, as they are trading wide to the Mexican Sovereign and the EM BBB Index. However, they do not anticipate these notes will outperform in the near term. For US investors, compared to the broader US market and peers within the cement industry, Cemex’s bonds no longer appear compelling at currently tight spread levels.

Edition: 198

- 01 November, 2024

Communications

“Contract Assets” have continued their trend upwards, jumping from 41 days to 45 days of sales. “Unbilled fees and costs and contract assets” have seen a huge increase, rising by 50% to $1,017m in the last 9 months. This is a sizeable balance of "unbilled" revenue sitting on the balance sheet and compares to "Advertising and Media" total revenues of c.$2bn in the last quarter. This seems unusual, particularly in the context of the company's claim that “substantially all unbilled fees and costs will be billed within the next 30 days”. Forensic Alpha considers this one of their more important flags in terms of identifying aggressive accounting and it is particularly concerning for OMC given that revenue recognition was one of the "Critical Audit Matters" raised by its auditor.

Edition: 198

- 01 November, 2024

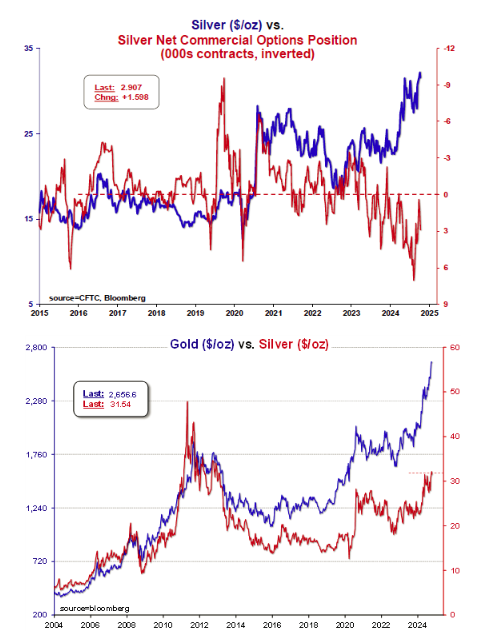

Gold & Silver: Breakout likely to arrive soon

Gold recovered from a stumble earlier in the week, finishing at its second highest weekly close on record and $16 shy of its record daily high. Silver also stumbled yet managed to recover to $31.54/oz and remains within striking distance of the $32.50 breakout zone. Eric Pomboy suspects the 'narrative change' following the stronger than expected Payroll report (which, as he has noted, was not necessarily a great report due to seasonal factors) will soon fade, dragging the dollar and yields lower once again. As ever, all eyes are on a silver breakout to confirm the next leg higher. In recent weeks, the precious metals have proved quite resilient, quickly recovering from a number of intraday selloffs. Eric says that the upside pressure is building and a real breakout is likely to arrive sooner than later.

Edition: 197

- 18 October, 2024

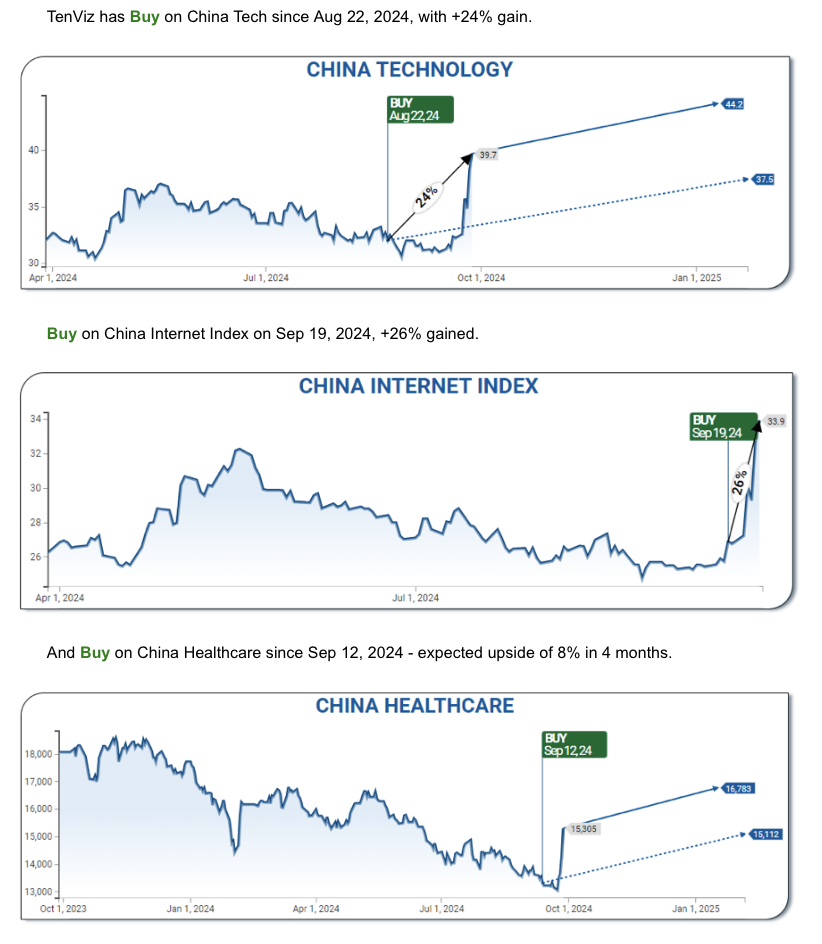

China: Unexpected positive developments

Rate cuts and liquidity injections preceded a massive 32% rally within a week. However, Konstantin Fominykh mentions that Chinese stocks were essentially priced for an economic collapse, and capital inflows signaled a turn before the policy shift: BUY on China tech since Aug 22; BUY on China Internet Index since Sep 19; BUY on China Healthcare since Sep 12. Institutional money is flowing not only into major tech names but also into sectors like auto-tech and green energy, highlighting broader market recovery. The rally started within the context of oversold emerging markets. Consistent with a weakening US$, SELL on the trade-weighted USD. Inflows into China align with BUYS on crude oil, uranium ETF, rare earth metals ETF and European luxury stocks.

Edition: 196

- 04 October, 2024