Fortnightly Publication Highlighting Latest Insights From IRF Providers

Company Research

Can copper volumes meet big expectations?

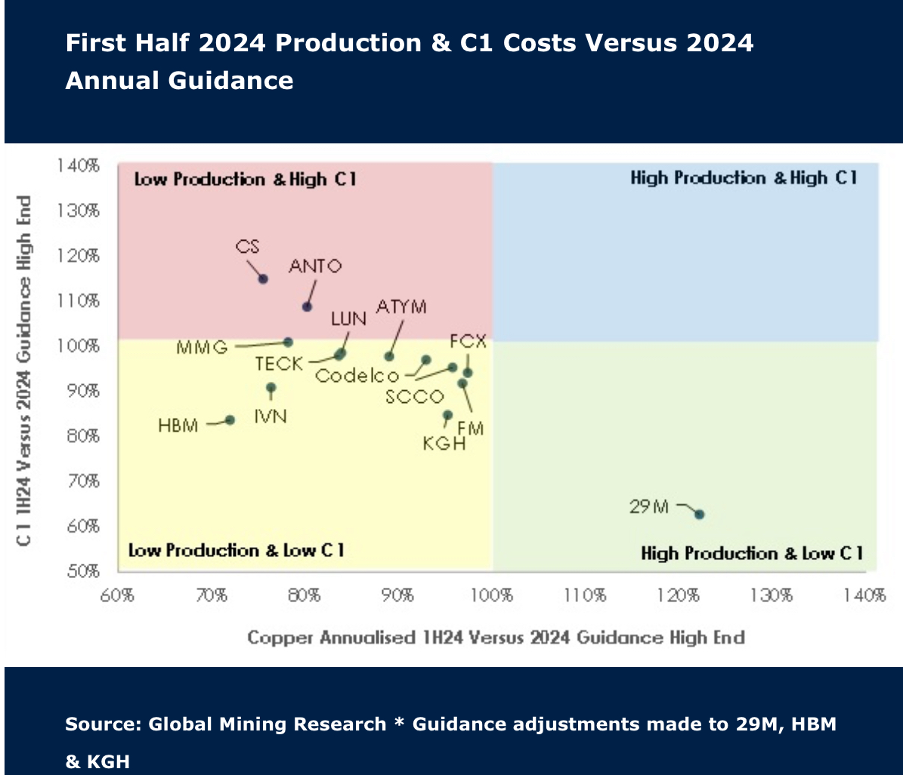

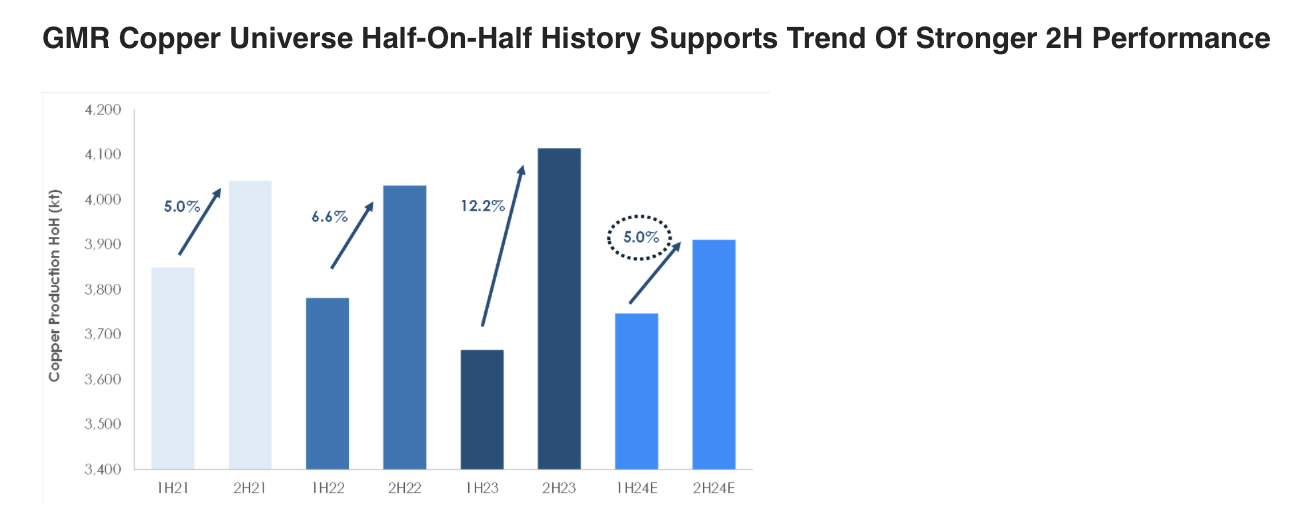

As expected, the first half of the year was met with weaker production, with companies in Global Mining Research’s coverage reporting flat figures of +1.5% and low capex. Costs increased some 4.8%, but this was offset by a ~US$0.60/lb increase in copper prices in the latest quarter. 60% of producers are expecting stronger H2 volumes, but Antofagasta, Ero Copper, Ivanhoe Mines and Capstone Copper are most at risk of missing 2024 guidance. Following the recent pullback and ahead of seasonally stronger Q4 prices, GMR continues to see the sector as attractive. Ratings have been raised for leveraged plays KGHM (to buy) and MMG (to hold).

Edition: 193

- 23 August, 2024

Copper: Risk to the downside

Copper prices had a strong start to the year. David Radclyffe’s review of the Q1/2024 performance versus 2024 guidance for the December year-end stocks helps put the market tightness into perspective. The key takeaway is that, as with gold companies, copper miners are banking on a strong H2/2024 to meet annual guidance figures. The risk is therefore to the downside, with once again copper producers struggling to either meet guidance or increase production appreciably. Only Hudbay Minerals, KGHM, Southern Copper, Freeport-McMoRan and First Quantum Minerals are tracking to 2024 production expectations. David’s preferred copper miners are in the small/mid-cap space on valuation grounds, including Atalaya Mining, Capstone Copper, Sandfire and Hudbay Minerals.

Edition: 187

- 31 May, 2024

Capstone Copper (CS CN) Canada

Materials

A copper growth story with significant optionality within the portfolio to >300kt/yr (vs. 164kt in 2023). After a period of heavy investment, FCF is set to turn positive in 2H24 with production from the Mantoverde sulphides project. The balance sheet is much stronger following the recent equity raising, with Net Debt/EBITDA forecast to fall from 3.8x in 2023 to 1.3x this year. However, near term cash flow is expected to be directed to mines, not the shareholders. CS offers an attractive risk / reward with its exposure to copper, scale, growth upside and a balance sheet expected to rapidly de-lever in the midterm. Growth studies in 2024 are likely to be near-term news catalysts.

Edition: 181

- 08 March, 2024

Increasing overweight position in copper

David Radclyffe recently published on the positive supply outlook for copper, setting out the scene for near- and medium-term market deficits and noted the lack of new projects to fill demand. In addition to the near-term price forecast, the long-term copper price forecast has been lifted to $4.00/lb in 2023 dollar terms. As a result, the sector trades on a prospective 2024 EV/EBITDA of 8.2x, and P/NPV10 of 1.3x. For equities, copper exposure remains in demand and is likely to drive more M&A. Investors may move along the equity risk curve to small caps. Capstone and Sandfire Resources are preferred in the small cap copper stocks, and Antofagasta and Grupo México in the mid/large ones.

Edition: 151

- 06 January, 2023

Sandfire Resources (SFR AU), Capstone Copper (CS CN) Canada

Materials

GMR’s two preferred junior copper names - in addition to offering growth at attractive valuations, their scale, longer mine lives and exploration upside also highlight potential corporate upside as industry peers seek to increase their exposure to copper and the EV materials thematic. The two miners are rapidly evolving businesses; a year ago they each had half the number of producing assets as they do in 2022. SFR is GMR’s cheapest copper stock. It trades at a P/NPV multiple of 0.5x and prospective FY24 FCF yield of 11%. At +200kt/yr from 2023 CS offers scale / leveraged exposure to copper.

Edition: 149

- 25 November, 2022

Summer of disconnect as energy transition stumbles

Industrials

Renewables are the future but the transition is being fumbled - due to the nature of its products Northcoast sees Generac (TP $292; 20% upside) as having the most near-term opportunity and Chart Industries (TP $209; 20% upside) winning as it benefits from the growth in small-scale LNG projects that are often used for utility load management solutions. Looking over the horizon, Bloom Energy (TP $23; 40% upside) and Capstone Green Energy (TP $7; 160% upside) will find success thanks to their unique power generation solutions.

Edition: 136

- 27 May, 2022

Preferred copper mine exposure

With copper trading above US$4.00/lb the ability for copper miners to fund initiatives is strong, providing a boon especially for small capitalisation base metals companies. In such a group, David Radclyffe’s preferred exposure is through BUY-rated Capstone Mining and Sandfire Resources, both offering a blend of value and growth, and which have benefited from M&A accelerated growth. Tony Robson considers Ero Copper after its massive underperformance; it is now more attractively priced and the company is pushing exploration hard, but growth is some time out, so he maintains his HOLD rating.

Edition: 132

- 01 April, 2022

Capstone Mining (CS CN) Canada

Materials

There is a lot to like regarding Capstone's proposed US$1.3bn merger with Mantos Copper - it delivers meaningful scale and makes the new group very much a Chilean-focussed copper producer (Mantos Blancos and Mantoverde projects add ~100kt/yr of copper). There are also clear district level synergies with Mantoverde and the Santo Domingo development project only ~30km apart. The deal appears accretive to NPV (+9%) and 2023E EPS (+19%) and CFPS (+25%). CS at 1.0x P/NPV is attractively priced vs. midcap peers.

Edition: 125

- 10 December, 2021