Fortnightly Publication Highlighting Latest Insights From IRF Providers

Company Research

Italy: Industrial Devolution

Italy’s industrial production undershot expectations in October, with production falling 1.0% month-on-month, a sharper contraction than the expected 0.3% decline. The pullback was broad-based across key categories: consumer goods output dropped 1.8%, capital goods declined 1.0% and intermediate goods slipped 0.3%. Energy production provided only a modest offset, rising 0.7%. On an annual basis, industrial output fell 0.3%. John Fagan points out that the year-on-year breakdown highlighted persistent structural weaknesses, with significant declines in chemical manufacturing (-6.6%), textiles and apparel (-5.0%), and refined petroleum products (-4.6%). The data reinforce the fragile momentum across Italy’s industrial base, which continues to face a combination of soft external demand, elevated input costs, and sector-specific pressures in chemicals and textiles. The sharp monthly swing also signals that September’s strength was not sustained, raising concerns about the durability of Italy’s manufacturing recovery.

Edition: 226

- 12 December, 2025

Cisco's 800G just hit the same wall GPUs did

Technology

JNK Research indicates CSCO's Silicon One networking roadmap faces the same thermal management bottleneck that constrained Nvidia and AMD GPU production. CSCO is ramping wafer starts 8x - from 1k to 8k annually - at TSMC in 1H26. However, heat spreader suppliers already operate at 85%+ utilisation with capacity concentrated among few Taiwan suppliers. The company is proactively qualifying secondary thermal suppliers and paying for tooling upfront to secure allocation. This mirrors the CoWoS packaging constraints that limited GPU shipments in 2024. Networking ASIC thermal requirements are approaching GPU-level complexity as data centre switches migrate from 400G to 1.6T.

Edition: 226

- 12 December, 2025

Ivanhoe Mines (IVN CN) Canada

Materials

A 2026 copper turnaround story - IVN is now producing from all 3 of its core and globally significant mining assets. However, this has not been reflected in the share price following the seismicity event at Kakula in May 25. The market is focused on short term risks, but Kakula’s recovery is being managed and 3Q25 volumes (annualised at 285kt/yr) likely marks the bottom. With the 3 operating assets contributing in 2026 and a new smelter set to lower costs, GMR sees next year as the inflection point. IVN also offers major exploration upside - its 100%-owned Makoko district alone has 9.2Mt of copper identified, with additional drilling across Angola, Zambia and Kazakhstan providing further optionality not priced in. Trading at 1.4x P/NPV10, IVN’s growth, scalability and asset quality make the risk/reward compelling.

Edition: 226

- 12 December, 2025

Technology

Jun Lei (Co-Founder) purchased ~ $12.9m worth of stock at HKD 38.58. While modest relative to his 1.9 billion-share stake, the purchase is noteworthy. It is his first open-market acquisition in this stock and also represents the first meaningful insider purchase since the IPO in July 2018 at HKD 17. Despite the recent share price decline, it is interesting to see him making a sizeable purchase shortly after the company released its Q3 earnings. Smart Insider ranks the stock +1 (highest rating).

Edition: 226

- 12 December, 2025

Kroger indicates more price reductions are ahead

Consumer Staples

Scott Mushkin has been highlighting for several months that price discounting would become more aggressive by the end of 2025. His latest findings show Walmart has become increasingly willing to drive down prices and Kroger is gearing up for battle, using a part of its ecommerce rationalisation to lower prices to become more competitive. The increase in competition, unfortunately, will come with further erosion in end demand. This is related to GPL-1 coverage in Medicare and Medicaid, GLP-1 oral compounds coming to market and some additional curtailment in SNAP benefits. At the same time, the continuation of the MAHA trend will remain a headwind. This marks the beginning of what will be a tougher period for the industry, especially those such as Kroger, that have significant overlap with Walmart.

Edition: 226

- 12 December, 2025

FLSmidth (FLS DC) Denmark

Industrials

Iron Blue initiates coverage on FLS with a score of 29/60, which is top decile and fertile grounds for shorting. They highlight 1) reliance on percentage of completion revenue recognition with an associated rise in FY24 balance sheet contract assets; 2) elevated stripped out restructuring and software/R&D amortisation costs; 3) evidence of deteriorated client payment behaviour; 4) FY24 headline margins supported by Y/Y reductions in inventory and bad debtor impairment expense; 5) DKK1bn headline net debt adjustments from reverse factoring and restricted cash; and 6) many disclosure gaps.

Edition: 226

- 12 December, 2025

US consumer confidence fell 1% in October

Carl Weinberg notes US consumer confidence was down again in October, with the Conference Board’s headline index continuing its jagged course toward the southeast corner of the chart. Expectations declined, too, and so did the index of current conditions. These confidence indices are very low, well below levels seen just before the Covid lockdowns. Carl says consumers are rattled. The survey indicates that the labour market is tight but jobs have become harder to find in recent months. The inflation expectations index for one year rose, seems to have steadied, but is still extraordinarily high! Carl believes consumer confidence this low will add to the arguments in favour of a rate cut at the FOMC… not a lot, but they do imply a slowdown of consumer spending. Whether or not that might not be a good thing—since the economy is at full employment anyway and cannot produce much more goods or services near term—is a question the FOMC should be debating.

Edition: 225

- 28 November, 2025

Emerging leaders in data & AI

Technology

Channel sentiment this quarter shows mixed momentum across data platforms. Elastic saw fewer partners meeting targets amid rising competition and questions about AI-driven sustainability. MongoDB continues to receive more positive views, benefitting from diversified modernisation wins and strong Atlas demand, setting up for a strong Q4. Snowflake is also receiving strong views as they evolve their partner model with new incentives, expand their work with System Integrators and accelerate AI-driven use cases. Box is sharpening its focus on high-value partners and operational AI workflows. Channels see Box benefitting as end users work to manage unstructured data for AI use cases. Click here to access the report.

Edition: 225

- 28 November, 2025

Argentina – Economy grew 5.0% year-on-year in September

The Argentine economy expanded 0.5% month-on-month in September, much better than Jorge Morgenstern’s expectations, according to the GDP proxy EMAE. Activity grew 5.0% year-over-year. There were significant upward revisions of previous data, with August now 0.9% higher than previous data release and monthly expansions since July. While the economy expanded 5.2% yoy in January-September (5.4% using the seasonally adjusted series), activity in September was 0.2% above February’s peak. As a result, GDP expanded at a seasonally adjusted annual rate of 1.9% in 3Q-2025 following a 0.2% contraction in 2Q-2025, dodging a technical recession.

Edition: 225

- 28 November, 2025

Telefonica (TEF SM) Spain

Communications

The Chair, CEO, CFO and 2 other executives bought a total of €1.3m of stock at ~€3.70 following share price weakness after the earnings release and a dividend cut. Marc Thomas Murtra (Chairman since Jan 25) bought €500k of stock in his first purchase since joining TEF, Emilio Rodríguez (COO since Mar 25, joined 2018) bought €500k worth of stock in his first purchase since he became declarable in 2025 and Laura Abasolo Garcia De Baquedano (CFO since 2017) bought €91k of stock in her first clean purchase. Pablo Antonio De Carvajal Gonzalez (Divisional Director) bought €126k of stock in his largest purchase and his first since 2019. Juan Azcue Vich (CSO since Jan 25) bought €74k of stock in his first purchase since joining. Whilst a likely co-ordinated response to disappointing news, the magnitude of the purchases is notable.

Edition: 225

- 28 November, 2025

Healthcare

Tom Tobin thinks there are several secular trends, including AI tailwinds, which makes RDNT a compelling idea even after its share price has rebounded in recent months. Core to Tom’s thesis is his ability to track Diagnostic Radiology staffing at RDNT, monitor turnover, and forecast volume and revenue per clinician. While the current valuation against consensus estimates appears stretched, he can model upside well into 2027 with a number of simultaneous secular tailwinds that justify the premium: 1) continued inpatient-to-outpatient imaging migration; 2) mix shift towards high-margin advanced imaging where demand is being driven by Alzheimer's, Oncology and Cardiology; and 3) AI tailwinds driving incremental revenue and operating leverage.

Edition: 225

- 28 November, 2025

Identifying stock swaps within your portfolio

Mill Street’s Swap Shop report responds to strong demand from equity portfolio managers seeking to use their MAER model (the Monitor of Analysts’ Earnings Revisions) to identify problematic low-ranked holdings and find high-ranked substitutes that preserve overall portfolio allocations. By leveraging MAER’s powerful intra-sector and intra-industry ranking performance, Mill Street highlights potential swaps within the same benchmark universe and industry, helping managers avoid “portfolio inertia” while keeping sector and style exposures consistent. This month’s screens include global large-cap Value stocks amid the recent rotation from Growth to Value, US Financials and Health Care following Mill Street’s sector allocation changes, and additional screens across the S&P 500 and their European equity universe. Click here to access the report.

Edition: 225

- 28 November, 2025

Technology

Arete sees Sony as one of their most compelling ideas, offering structural, multi-year growth outside the AI-bubble debate while still benefiting from AI tailwinds. Their enthusiasm for the stock is based on 1) the ~50% of revenue that is now recurring and 2) rising appreciation for its multiple growth segments (in anime, immersive content, game and music publishing, and image sensors). Sony can be rethought as having two distinct and equally strategic businesses: Content Creation and Enabling Tech/Platforms. FY26 is set to be a banner year - GTA VI, Wolverine, Spiderman, Crunchyroll, and expansion for Image Sensors with Autos wins ramping, Electronics getting cost actions and excess cash piling up. Arete expects mid-teens EPS growth in FY26 & FY27 and even on modest multiples - 12x EV/EBITDA - they get a TP of ¥5,750 (25% upside).

Edition: 225

- 28 November, 2025

Elekta (EKTAB SS) Sweden

Healthcare

EKTAB delivered a Q2 profitability beat despite tariffs and FX headwinds, while sales were only slightly soft, helping spark a sharp rebound in the shares. Adjusted EBIT came in 6.5% above expectations and margins rose to 10.1%, supported by mix and pricing. Although China and the US weighed on revenue, order intake grew and China’s book-to-bill ratio exceeded 1.3x suggesting a potential recovery ahead. H2 should be stronger, with improving China trends and US approval of Elekta Evo expected. The new CEO’s restructuring plan - cutting ~450 jobs (10%), simplifying the organisation and cancelling low-quality orders - targets SEK500m+ annual savings. With a robust SEK34bn backlog and solid uptake of new products, AlphaValue maintains a positive view as the turnaround gains traction.

Edition: 225

- 28 November, 2025

Google locks CoWoS capacity independent of Broadcom

Technology

JNK's research shows GOOG's direct TSM capacity reservations signal a shift away from expensive third-party AVGO design partnerships. The company is now booking advanced packaging without immediate orders, positioning for late 2026 TPU production deployments. TPU 7e progresses with MTK handling I/O integration on roughly 2M unit volumes, while TPU 8p selection between AVGO and AIchip reflects growing design house pricing pressure. This mirrors AWS's trajectory - from external partnerships towards full internal design control. Near-term, Alchip and MTK benefit from current programmes. Longer-term, AVGO faces structural headwinds as hyperscalers internalise capabilities. Click here to access the full note.

Edition: 224

- 14 November, 2025

Why investors keep buying silver

In his latest video, Jeffrey Christian of CPM Group discusses recent developments in gold, silver, platinum, and palladium prices, and their consolidation following October’s sharp rise. He also looks at the factors that could determine the next breakout for the metals, and whether the next price move might be higher or lower. Jeff takes an in-depth look at the physical silver market and addresses several misconceptions about physical supply, fabrication demand, investment demand, and inventories. He looks at mine production, secondary recovery, fabrication demand, inventory levels, and investor activity, explaining how the market remains well supplied even as investment demand has risen sharply in recent months. Jeff also discusses ETF flows, coin sales, premiums for 1,000-ounce bars, and why talk of a “silver shortage” is misleading.

Click here to watch.

Edition: 224

- 14 November, 2025

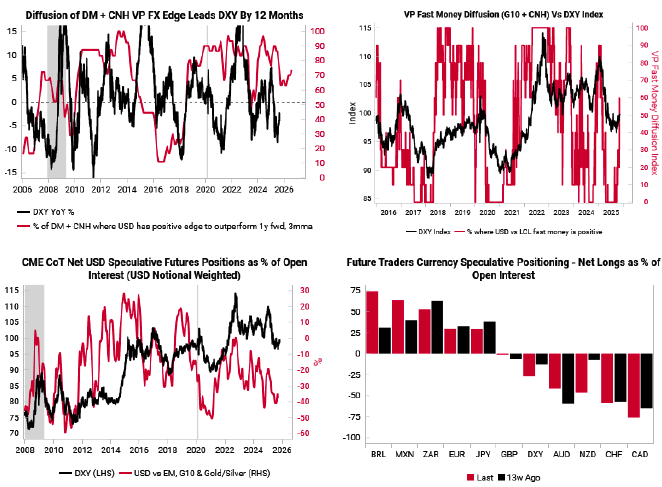

USD short squeeze thesis playing out

The Variant Perception team’s cyclical and tactical indicators still point to a rebound in the USD through year-end as markets are now pricing in less easing from the Fed and net positioning remains short USD. On a cyclical basis, their fundamentals-based FX edge model still shows the USD has a positive expected 1-year total return against most G10 currencies (top left chart). Meanwhile, most tactical indicators we monitor suggest the dollar is bottoming out. Their Fast Money diffusion index – a measure of speculative activity – has risen from 0% to over 50%, which has marked the start of dollar rebounds over the past decade (top right chart). To add to this, short positioning against the dollar remains stretched (bottom two charts): aggregate positioning is near multi-year lows, much of which is concentrated in longs for EUR, JPY and high-carry EM currencies. Their preferred expressions for a tactical dollar bounce remain long USD/KRW and short EUR/USD.

Edition: 224

- 14 November, 2025

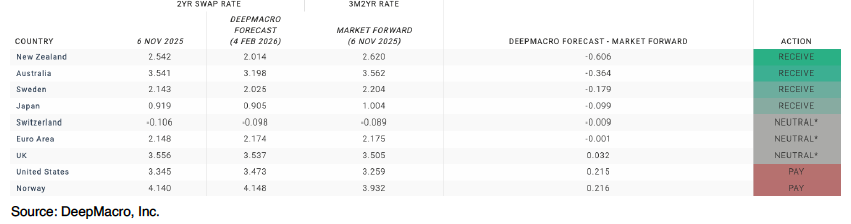

Short-Term Rates-1 Model

DeepMacro’s STR-1 is a short-term rates model, providing forecasts of 2yr swap rates for the G10 countries over the next three months. The team choose 2yr swap rates because they are an estimate of the market's expectation for monetary policy over the medium term, which they recognise as a function of economic growth and inflation. STR-1 generates receive/pay recommendations based on the difference between model forecasts, and market forward interest rates. The inputs to the model are the DeepMacro growth and inflation factors, including "Big Data", and DeepMacro's automated, machine-driven analysis of central banks. Currently, the model expects rates to rise in the US, but the market forwards expect rates to decline. In Europe the model forecasts rates to rise but by less than market forwards, and in UK it expects rates to decline but by less than market forwards, but both gaps are not large enough to recommend a trade. Please get in touch to find out more.

Edition: 224

- 14 November, 2025

How to beat the S&P500 - the Q&A that matter

Trivariate examines six core issues for long-only managers benchmarked to the S&P500: 1) Beta: despite long-term data favouring sub-1.0 beta portfolios, this is currently nearly impossible given the high-beta “Great 8”. 2) Alpha vs. Risk: ~75% of holdings should be for risk management. 3) Diversification: run both a broad risk book and a concentrated alpha book - essentially two portfolios in one; holding a higher number of stocks vs. history. 4) Position Sizing: take large, conviction-weighted bets in names with high company-specific risk / hard to replicate (e.g. Healthcare). 5) Blow-up Avoidance: avoid large exposures to bottom-decile FCF converters, large increases in inventory-to-sales, large intangible accruals and extreme valuations. 6) Macro: portfolio managers must consider what set of macro conditions are best for their portfolio performance.

Edition: 224

- 14 November, 2025

Russia: Close to recession

Christopher Weafer notes that the Russian economy is close to recession. Economic growth has accelerated on the back of big fiscal stimulus and an upswing in the domestic demand – but GDP growth could fall into a negative territory in 4Q25. Industrial output is expected to be near zero, while other segments, such as retail sales and agriculture, could help the economy escape a contraction. However, the growth dynamic will become far less certain in early 2026 with the introduction of higher VAT and inflationary pressures. In 9M25, GDP increased by just 1% YoY (0.9% YoY in September), which puts Christopher’s 2025 growth forecast of 1.2% more on the optimistic side. Over the next 2-3 quarters, the economy will balance at close to zero. Christopher expects that it will be no earlier than mid-2026 when credit conditions could start to improve, thus offering support to a gradual rise in consumer demand and corporate investments.

Edition: 224

- 14 November, 2025

Constellation Software (CSU CN) Canada

Technology

Value in the volatility - concerns around AI disruption and Mark Leonard's departure, which have driven CSU shares down >30% since the start of Jul, are more sentiment-driven than reflective of any fundamental deterioration. On AI disruption risk, CSU is well positioned to serve as the distribution layer for AI solutions, given 1) its existing customer relationships, 2) proprietary industry knowledge and 3) in some cases, the ability to leverage data. In addition, CSU can continue to thrive despite Mark Leonard being less involved because of its decentralised structure, which pushes agency to the edges and fosters an entrepreneurial culture in both capital allocation and operations. Veritas maintains their Buy rating and intrinsic value of $5,500/share (70% upside).

Edition: 224

- 14 November, 2025

AI driven 10Q / 10K text analysis

Since there are always reasons when companies change the wording in their financial filings, being alerted to these changes allows investors to realise potential risk factors and opportunities before they are reflected in the market. Recent alerts include: 1) Akamai - ongoing competition, pricing pressure, DIY, alternative sourcing strategies. 2) Align - increased competition? Customs investigations? 3) Arista Networks - more benign competitive and market conditions. 4) Bruker - covenant concerns. 5) Celanese - greater than usual year-end destocking in Q4. 6) Jazz Pharmaceuticals - caution on ability to maintain or increase sales.

Edition: 224

- 14 November, 2025

Pemex: Debt strategy extends support, spreads tighten vs. Mexico

Energy

Mexico’s comprehensive debt strategy highlights extraordinary sovereign support for Pemex, easing refinancing pressures and compressing spreads relative to the sovereign. Still, EM Spreads thinks further tightening will hinge on Pemex’s fundamentals, as investors are likely to increasingly focus on its operational profile. At current spread levels and with a steeper curve, they continue to recommend the PEMEX 6.700% 2032s (6.7% YTM, 4.3-yr duration) as offering best value in the belly. For higher duration appetite, they see the PEMEX 7.690% 2050s (8.6% YTM, 10.1-yr duration, $82 price) as most attractive on the long end, with compelling carry and upside potential.

Edition: 224

- 14 November, 2025

Fortum (FORTUM FH) Finland

Utilities

Pitched as a long idea at Revelare’s latest investor event, FORTUM operates in Europe’s most attractive market for AI datacentre development. Finland’s grid is mostly hydro and nuclear, with no marginal cost and power prices 60% below mainland Europe, while the cold climate further lowers datacentre cooling needs. All that is required for prices to rise back towards €100/MWh parity is new demand - and that is coming fast. Over 3GW of AI datacentre projects have already been approved, while Google has also bought a huge piece of land in the middle of the country and other hyperscalers are expected to follow. As Finnish power prices increase the company’s earnings should rise from €1 to €3 per share, implying the stock could reach €60 vs. <€20 today.

Edition: 223

- 31 October, 2025

Blow-up avoidance guide - how are you dealing with the S&P500 being an AI factor bet?

While there are plenty of high-quality AI-exposed stocks to own, the challenge is that many non-Tech names have also become correlated to the AI trade. Trivariate screened for stocks with low correlation (<0.2) to their AI Semiconductors basket, that are up >10% in the past 6 months, top-half quality and beta <1 - identifying 28 stocks with a m/cap >$50bn. Given the recent huge moves in speculative names, Trivariate also advises preparing a sell/short list for a potential market rollover. They highlight 24 stocks ($1bn+ m/cap) that are up >100% in 6 months, in the most expensive EV/sales decile and the bottom half of their quality model, companies with high short interest and lower 2026 EPS estimates than at the start of the year, meaning the recent big moves in stock prices are despite a deteriorating nearer-term fundamental outlook.

Edition: 223

- 31 October, 2025

Financials

OWS’s short thesis continues to play out as growth slows and profitability erodes. Total Written Premium (TWP) growth is decelerating, converging toward a long-term low double-digit rate, while management’s talk of 40% growth within five years appears unrealistic. Agent growth has stalled (+3.8% Y/Y vs. +11.1% last quarter) and productivity per agent has essentially been flat for 3 straight quarters. Meanwhile, operating costs per agent continue to rise, leading to margin compression that management expects to persist into 2026. OWS argues that GSHD’s franchise-heavy model is becoming less attractive to experienced agents and increasingly reliant on costly recruitment of new ones, leaving valuation vulnerable to further downside. TP $52 (25% downside).

Edition: 223

- 31 October, 2025

Lifco (LIFCOB SS) Sweden

Industrials

Karl Redin (Subsidiary CEO) purchased 26,350 shares at SEK 381, spending €920k. This is his eighth purchase and over 10x what he has spent on prior buys; the most recent was in Jul at SEK 367. The purchase occurred on the same day as the stock rose sharply after reporting Q3 earnings. This is an unusual buy, into unusual strength. Martin Linder (Subsidiary Head) also recently purchased shares spending €190k - a large purchase for him. Smart Insider has had a positive rank on this stock since early last year, based on buying from Per Waldemarson (CEO), Anna Hallberg (Director) and Martin Linder (Senior Officer). The stock has moved higher and insider buying has continued. Waldemarson made his most significant purchase in Jul, spending €1.3m and then spent an additional €300k in Sep. This is now the fourth time Smart Insider has renewed their +1 rank since Apr 24.

Edition: 223

- 31 October, 2025

Navitas stock surge masks growing execution crisis in AI power market

Technology

JNK Supply Chain Research reveals serious problems hiding beneath the surface as NVTS transitions chip production from TSMC to PSMC. The new factory has lower quality standards and worse yields. Critical 650V GaN devices won't reach mass production until late 2026 or early 2027. Competitor Infineon already ships 800V power solutions to AI data centres. NVTS remains in development while the market moves forward. Big customers like NVIDIA are diversifying suppliers instead of depending on NVTS. The company has few shipping products in hyperscale AI infrastructure. NVTS pioneered GaN technology with 250 million units shipped. But execution matters more than innovation when competitors deliver working products first. NVTS is one of 23 companies JNK tracks in the analog space. Click here for recent results.

Edition: 223

- 31 October, 2025

Materials

EM Spreads initiates coverage on Braskem with an Overweight recommendation. They believe the company’s large domestic footprint, political relevance and partial government ownership make a default event less likely near term, but the credit now hinges less on fundamentals and more on political and strategic decisions involving Petrobras, the federal government and Braskem’s ability to strengthen liquidity. They see asymmetric risk-reward at distressed prices, with outcomes contingent on a secured-liquidity bridge, PRESIQ approval, direct support measures and broader policy backing for Brazil’s petrochemical sector. They favour exposure to the lower-priced bonds within the curve for better downside protection and see greater value in the 2030s at $38.3, 32.1% YTM, 3.1-yr duration.

Edition: 223

- 31 October, 2025

Consumer Discretionary

PLNT is well positioned in the growing high‑value‑low‑price gym segment with scale and ample runway for growth. New CEO Colleen Keating brings relevant hospitality franchise experience to drive the next phase of growth in the US and internationally. Gen Z is the fastest‑growing membership cohort for the company, supported by initiatives like the “High School Summer Pass”. PLNT continues to refine club formats and contractual terms to improve efficiency and unit economics. 2Xideas expects 2024-31E system‑wide sales CAGR of 11.7%, driven by 6.6% annual net unit growth and 5.0% same‑club sales growth. They forecast an 11.1% EBITDA CAGR and a 44.6% margin in 2031E. European expansion remains an upside not reflected in their forecasts. They see 17.2% annualised total returns based on an exit NTM P/E of 28.0x (17.7x EV/EBITDA).

Edition: 223

- 31 October, 2025

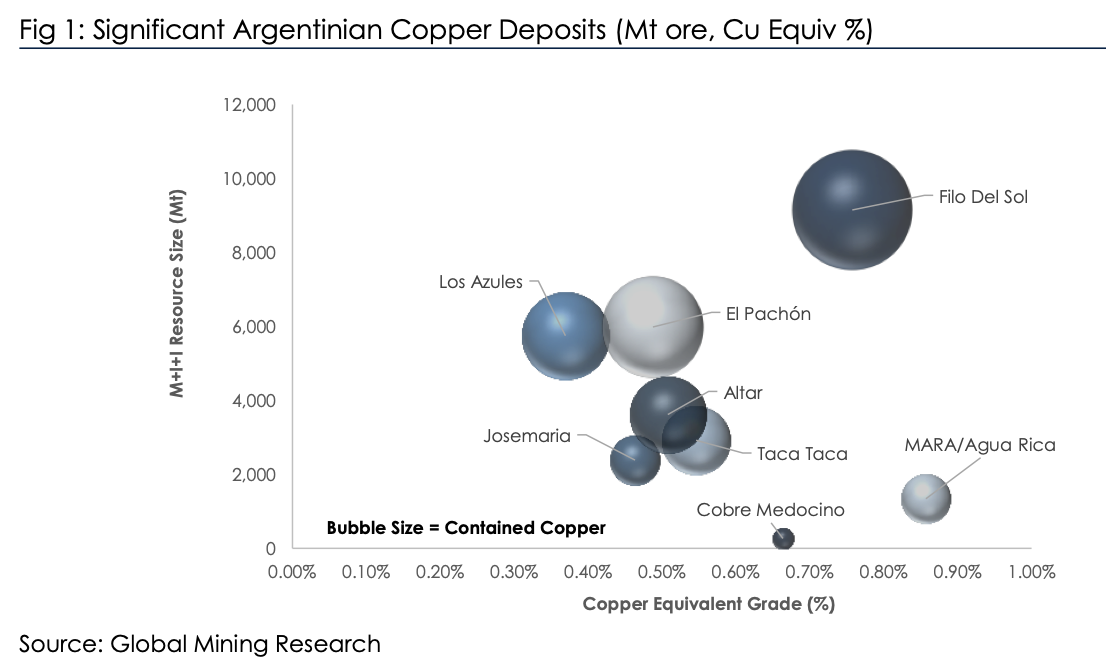

Is Argentina the next big thing?

Argentina has significant copper reserves yet produces no material copper (see chart). The new investment climate (RIGI) in Argentina, spearheaded by libertarian President Milei, is hoping to reverse this. Other volatile countries including DRC have achieved significant growth, so it’s possible. In his latest report, David Radclyffe examines the potential of Argentina copper. He sees potential for the nation to become a 1.0–1.5 Mt per year copper producer (top 10 globally), but comments on the aspirational timelines, with first copper unlikely on this side of 2029. Issues also cannot be discounted, with ESG concerns bubbling alongside a lack of infrastructure and skilled workers. David estimates the total capex at USD $40–50 billion. Lundin Mining has the most leveraged exposure to Argentina in partnership with BHP and is the preferred exposure. There are a few exploration plays, of which NGEx Minerals (non-rated) and its Lunahuasi discovery is the largest.

Edition: 222

- 17 October, 2025

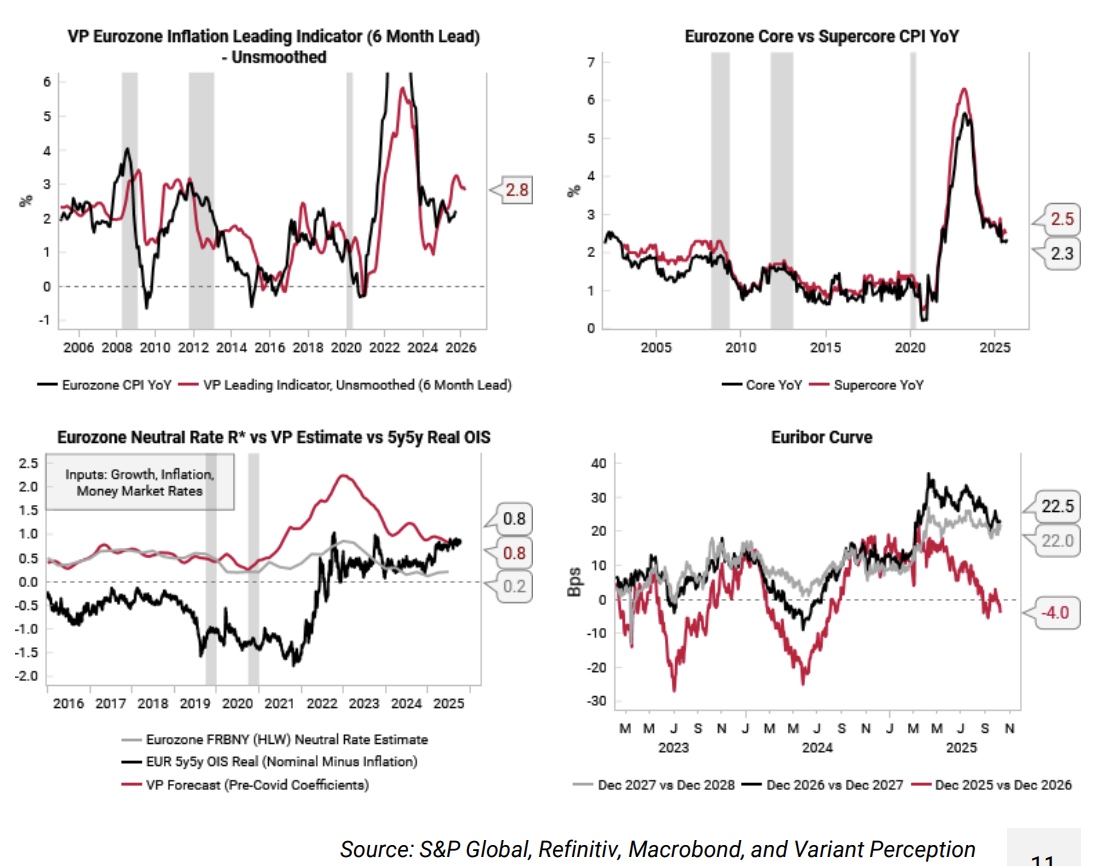

Eurozone: Consensus too optimistic on disinflation

Consensus expectations see 2026 eurozone headline CPI at 1.8% and core CPI at 2%. The Variant Perception team suspects that inflation risks are tilted to the upside from here given the recovery in their eurozone growth leading indicators and the ECB rate cuts so far this year. Their main inflation leading indicator is rolling over from a high level, but the point estimate remains elevated at 2.8% (top left chart). Core and supercore CPI have also been slower to fall, still at 2.3 to 2.5% YoY (top right). The team put the real neutral rate (R*) for the eurozone at 0.8%, which is also where the 5y5y EUR real OIS is trading (bottom left). With headline CPI at 2%, there is good chance that ECB policy is already stimulatory, potentially creating inflation upside in 2026. The team take profits on their SOFR vs Euribor Dec 25/26 convergence trade established last month.

Edition: 222

- 17 October, 2025

Access to proprietary short-availability data

As many quantitative researchers know, reliable historical short-availability data, especially intra-day, is notoriously difficult to obtain. Recognising this gap and leveraging the accessibility of real-time market feeds, Capital Systems began recording real-time short-availability data for all US equities in Aug 23 and for all USDC-denominated cryptocurrencies on the Binance exchange in Jun 24. The data is of particular use in two areas: 1) Reducing assumption bias in short-selling strategies, especially for hard-to-borrow securities. 2) Alpha capture. Why would Capital Systems share such an edge? The firm trades only a small fraction of the markets it monitors, allowing them to offer this unique dataset on a limited basis to select clients.

Edition: 222

- 17 October, 2025

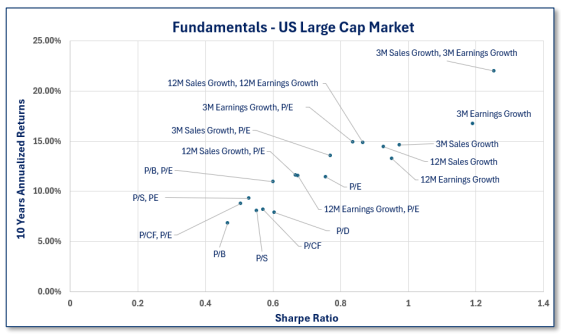

What’s really driving alpha

Trendrating’s latest analysis provides data-driven insights into the fundamental parameters that have historically generated the most alpha across US sectors. Their report identifies and ranks the combinations of metrics most rewarded by the market, offering investors a factual framework for factor-based decision-making. In US Large Caps, the combination of Highest 3-Month Sales Growth and Highest 3-Month Earnings Growth has delivered the strongest returns over both 3- and 10-year periods, while Lowest Price/Book and Lowest Price/Dividend generated the weakest returns. Their report also includes results for specific sectors including Consumer Discretionary, Financials, Industrials and Technology - click here to access.

Edition: 222

- 17 October, 2025

Technology

TD trades at levels implying investors value its operating business at near zero, reflecting deep scepticism about growth and profitability amid dependence on Samsung and exposure to memory price volatility. While these risks are real, Yuka Marosek argues they are already priced in and TD’s close ties to Samsung Japan and Toyota Tsusho provide stability and long-term relevance. Expansion into automotive and server / storage markets, supported by rising AI-driven demand for memory, offers potential for improved margins and diversification. Toyota Tsusho owns 50.1% of TD and Yuka wonders if Tsusho might eventually absorb the entire company - if Samsung allows it.

Edition: 222

- 17 October, 2025

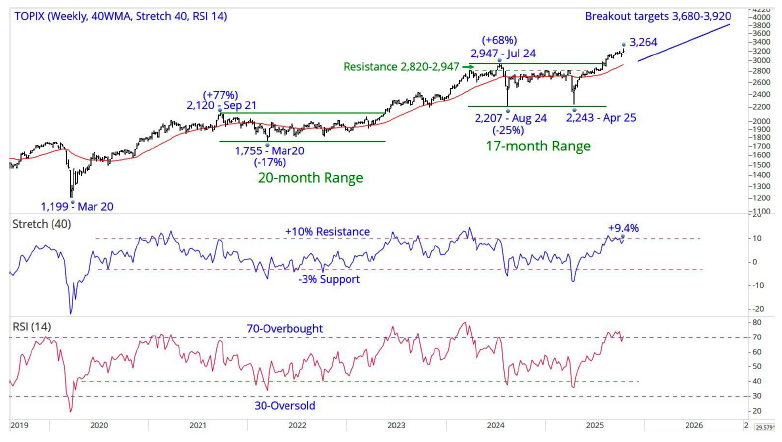

Japan: Hot Topix

The Topix’s (3,198) breakout from the 2,207–2,947, 17-month range targets an advance to 3,680–3,920. The break above the 1,700–1,825, 28-year ceiling in 2021 targets a minimum of 3,400–3,650+. Weekly indicators are either overbought, or close to overbought, but have been higher during this bull market. Chris Roberts remains 50% long from 2,857, with the stop for all longs moving up to a daily close below 2,780 from 2,475. His preferred target is now 3,680+, and he is looking to add to longs. He will add 5% long at 3,178, 5% at 3,168 and 5% at 3,158. If fully executed, he will move to 65% long.

Edition: 222

- 17 October, 2025

DCC (DCC LN) UK

Energy

Following publication of the company's FY25 annual report, Iron Blue increases their DCC rating +3 pts to 27/60 (newly top quartile / fertile grounds for shorting). Key changes vs. FY24: 1) Higher one-off costs: FY25 stripped out restructuring expense increased to 7% of PBT adj, highest in 7 years. DCC also stripped out from headline earnings £74m goodwill impairment. 2) Took £17m profits on disposal of PPE inside underlying profits in FY25, the highest figure in the past decade. 3) P&L expense for inventories write-downs dropped to a decade-low of £5m. 4) DCC continued its strategy of promoting top management from within, with internal promotions to the CFO and newly created COO roles. 5) In its principal risks assessment, DCC highlighted Y/Y risk increases concerning the DCC Technology strategic review and also the impact on its operations from higher tariffs.

Edition: 222

- 17 October, 2025

Ginlong Technologies (300763 CH)

Industrials

It has been three years since the last insider activity in this stock occurred. In Jun 22, the selling was from Finance Director Junqiang Guo and Deputy GM Chan Zhang around CNY 200 per share. The stock rose for a few months but then fell sharply in 2023. Recently, Guo, Zhang and Deputy GM Hefeng Lu made large sales at less than half that price: Guo sold US$862k at CNY 85, Zhang US$515k at CNY 85.06 and Lu US$350k at CNY 87, reducing their holdings by 30%, 30% and 23%, respectively. The stock has nearly doubled from its Apr 25 low but remains flat over the past 12 months and below 2023 levels. Smart Insider are ranking the stock -1 (lowest rating).

Edition: 221

- 03 October, 2025

Consumer Discretionary

John Zolidis turns bearish on SBUX heading into Q4. He views domestic store closings and a potential China exit as signs that SBUX is no longer a growth business and valuation should contract to reflect this. Furthermore, traffic remains negative and estimates are too high more than one year after Brian Niccol started as CEO. Last quarter was good for Quo Vadis’ calls with their average Long idea falling 1% compared to an average decline in their Short ideas of 15%. Their (Retail & Restaurants) universe fell 9%, reinforcing that Quo Vadis' approach is identifying winners and losers and creating alpha. Q3 was the fourth consecutive quarter with longs outpacing short ideas.

Edition: 221

- 03 October, 2025

Argentina tries… orthodoxy

From a muddle-through approach fraught with renewed peso and inflation risk, to more classically orthodox measures, Jonathan remarks just how much the policy stance has changed in the past three months. This is the best chance of getting money growth and inflation back down into low double and ideally single digits, at the cost of keeping the economy in recession. In the face of the country’s anaemic export economy, the only hope for external stabilisation is to keep overall demand and import spending weak. Even if Argentina holds course, it doesn’t guarantee a stable peso, and the needs to give up the USDARS 1,500 "ceiling" and let the exchange rate find its level without endless borrowing support. The recent backup in dollar yields has opened tactical value, but not necessarily a structural buying opportunity; there's a big difference between successfully stabilizing the macro position and finding an exit strategy for external indebtedness.

Edition: 221

- 03 October, 2025

ASML (ASML NA) Netherlands

Technology

Arete’s report titled "The Capex Conundrum" focuses on: 1) The broader growth backdrop for leading-edge semi demand and the disconnect in ASML and wider WFE estimates into 2026/27. 2) Capex for key customers which should see significant upside over this cycle, boosting EUV demand and delivering above consensus revenues and EPS through 2027E. 3) The ongoing China capex contraction which is now captured in consensus numbers and stock sentiment. 4) Why there has been a disconnect between N2 capacity growth and EUV unit shipments. 5) Risks around the EUV roadmap and the possible move to 3D DRAM and how that might impact unit demand. 6) Valuation risk/reward, especially against the backdrop of recent sell-side downgrades and negative broader investor sentiment towards WFE, looks attractive.

Edition: 221

- 03 October, 2025

Industrials

Under new leadership, Kyodo is accelerating its pivot from the declining paper-printing business towards higher-margin niches such as high-performance packaging materials, flexible packaging and tube products. Margin gains in recent years already reflect this shift and the company’s 10-year plan aims to scale these efforts further. The key question for investors: with DNP and Toppan well ahead in diversification, can Kyodo leverage its niche strengths to establish itself as a viable third player in a consolidating industry. Yuka Marosek argues it can. While Kyodo’s OP recovery appears partially priced in (13.9x P/E vs. DNP at 14x and Toppan at 18.4x), a 4.8% dividend yield should appeal to income investors and with FY26 OP projected +20% y/y and ROE rising to 6.1%, further upside remains possible.

Edition: 221

- 03 October, 2025

Retail Cross Currents: 4 key themes & top stock ideas

Consumer

Gordon Haskett Research Advisors

GHRA highlights an unusually volatile retail backdrop through late 2025 and early 2026, noting multiple “cross currents” affecting both consumers and retailers. Recent rating changes include downgrades for Dollar Tree (Reduce) and BJ's Wholesale Club (Hold), while upgrades cover Williams-Sonoma (Buy), Wayfair (Accumulate), Kohl's (Accumulate) and Dick's Sporting Goods (Hold). GHRA’s key investment themes emphasise: 1) stocks offering both EPS upside and multiple expansion (Five Below, Ross Stores, Burlington); 2) underappreciated turnaround stories (Kohl's, Dollar General); 3) selective “rate-trade” exposure favouring home furnishings over home improvement (Williams-Sonoma, Wayfair, Tractor Supply); and 4) secular winners / “Coffee Can” stocks (Walmart, Costco, TJX, Ollie's Bargain Outlet, Casey's).

Edition: 221

- 03 October, 2025

Cellnex (CLNX SM) Spain

Industrials

Robert Crimes views CLNX’s sharp de-rating since 2022 as highly unjustified. Prop. EBITDaL has grown 36%, from €1.8bn in 2022 to €2.4bn in 2025E, yet the share price has declined 26%, massively underperforming the Eurofirst 300. The stock trades on 2025E EV/EBITDaL of 16.7x, a 29% discount to the 22.9x average of its recent disposals. Robert believes CLNX could attract a buyout from a large consortium, such as American Tower, as it offers a non-replicable pan-European network, ranking first or second in eight of the ten countries it operates in. His TP of €69, implies ~135% upside, with CLNX ranking 3rd of 23 on Insight’s Stock Ranking System.

Edition: 221

- 03 October, 2025

Making it easier to beat the benchmarks

Delivering investment performance remains a challenge for active managers. Most funds underperform their respective benchmarks over 3, 5 and 10-year periods. Conventional tools and datasets often fail to deliver alpha, leaving investors in need of fact-based, testable intelligence that can measurably impact returns. That’s what 300+ institutions access through Trendrating’s platform. In this document (click here to access), you will find valuable insights into the performance ranking of various fundamental parameters in the US market. Trendrating's system now includes expanded analytics and an advanced AI assistant. Contact us below to access an exclusive demo and free trial to explore its insights, including top-performing parameter combinations YTD.

Edition: 220

- 19 September, 2025

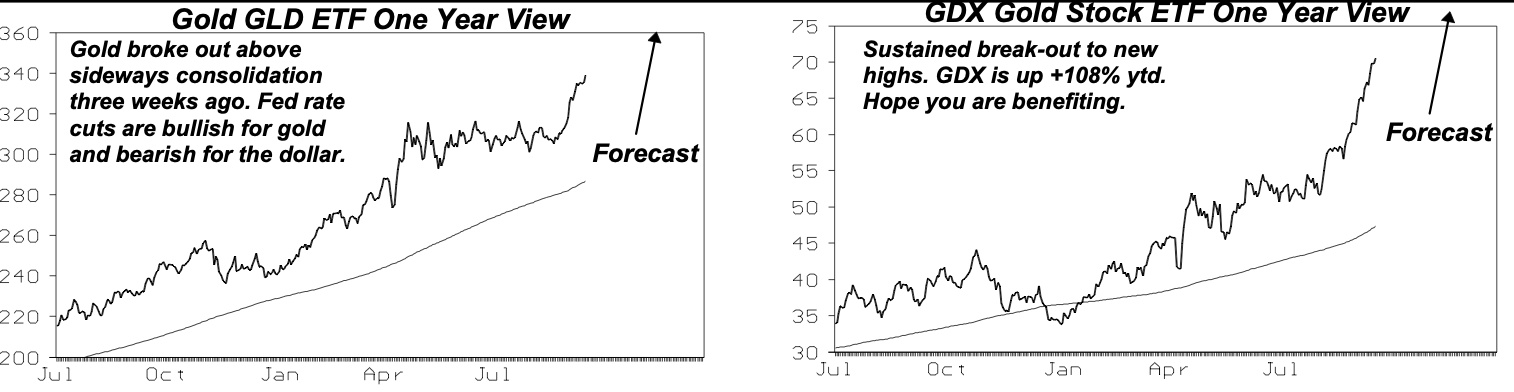

Don’t miss out on the gold rally

Gold stocks have been the top recommendation on Michael Belkin’s US industry group/stock page all year. The VanEck Gold Miners ETF (GDX) is now up +108% ytd after just 1.5 months of inflows, six times as much as the MAG7 +18% ytd gain. The fundamentals remain positive. The Fed’s policy shift waves a green flag toward gold prices, with central banks continuing to accumulate gold as they shift reserves out of the USD. The fundamental attraction for gold miners is finally being recognised, but we are only 1.5 months into the change in perception. GDX has only US$19bn of assets at this point, and the five largest stocks clock in at US$275bn, indicating that it is large enough to accommodate industrial buying, which could dramatically expand the market cap of related stocks as the rally continues. Michael’s recommendations include small-cap stocks that have lagged the GDX advance, including Galiano Gold, McEwen, Seabridge Gold and Equinox Gold.

Edition: 220

- 19 September, 2025

Brazil: Selic rate may go down sooner than expected

The recent adjustment in the Fed Funds trajectory has direct implications for the exchange rate, and with US monetary policy in a loosening phase the Buysidebrazil team project a weaker dollar, with the DXY falling to 97 points. In Brazil, the risk perception remains relatively stable, and the team have calibrated their CDS forecast to 140 points, leading them to revise the exchange rate to BRL 5.50. This brings positive effects for inflation dynamics, especially in the industrial goods segment; the team have adjusted their PRCA forecasts to 4.6% in 2025 and 4.1% in 2026 (previously 4.7% and 4.2%). Now, with a more stable exchange rate, a slowing economy, an inflation risk balance skewed downward, and inflation expectations in the process of re-anchoring, the conditions are favourable for the central bank to start the rate-cutting cycle as early as December 2025.

Edition: 220

- 19 September, 2025

South Africa: Duller and calmer, with eyes on the prize

Krutham (formerly known as Intellidex)

The SARB kept rates unchanged in a 4-2 vote – which Peter Montalto expected would be a close call – but it remains a bit of a surprise given that this week’s CPI and expectations data could have opened a sliver of space. The QPM model moved up the repo path by removing one cut at the end of this year and the coming two, while the inflation track was marked up. Growth for 2025 was revised up to 1.2%, now in line with Peter’s view. Overall, the statement largely sidestepped this week’s CPI and gave inflation expectations only a passing nod; a signal possibly that the MPC wants a broader medium-run, firmer, re-anchoring before moving again. Peter’s baseline is an extended hold of ~10 months, with the next leg down only after a formal target change by Budget 2026, trending towards 5.50% terminal rates into 2028. There is a small risk of one more cut in November, but the bar is high.

Edition: 220

- 19 September, 2025

Overlooked opportunities in YWR’s QARV rankings

Why do China, shipping, iron ore, hardware, Brazil… all stand out if you screen high ROE’s with low valuation? Erik@YWR sees it as scepticism about global growth on which he is taking a contrarian view. Following this month’s review of YWR’s QARV rankings key themes include: 1) A massive China bull market has only just begun. 2) Opportunities in iron ore, where Fortescue, Rio Tinto and Kumba are delivering ~20% ROEs at <12x P/E despite China’s property crash. 3) The Taiwanese semiconductor supply chain stands out as highly profitable and undervalued. Everyone focuses on Nvidia and the datacentre buildout but misses the whole Taiwanese supply chain behind this. Tokyo Electron and ASML also screen well. 4) Brazil is overlooked, with names like Itau, Vale, Ambev and B3 all screening well. 5) Container shipping - supply-chain diversification could sustain tighter freight rates than investors expect.

Edition: 220

- 19 September, 2025

Industrials

Kyocera is attracting investor attention, fuelled by hopes of unlocking value from its overcapitalised balance sheet and complex business structure, rather than faith in management. While the first steps on asset divestment and business restructuring have now been decided, Asymmetric Advisors suspects the external pressure from activist investors, backed by TSE reforms, will force a more rapid pace of change than the “not so drastic” change management are presently outlining. Trading at 0.88x PBR with ¥1.6trn net cash, recent announcements - a ¥200bn buyback and partial KDDI stake sale worth ~¥250bn - highlight the scale of latent value.

Edition: 220

- 19 September, 2025