Fortnightly Publication Highlighting Latest Insights From IRF Providers

Company Research

China: Zhongzhi bankruptcy opens door to stimulus

In a pivotal move, a Beijing court accepted Zhongzhi Group's bankruptcy application, a major private financial conglomerate laden with distressed debt and troubled developer projects. Following the nationalisation of Zhongzhi's trust subsidiary in September, a similar fate looms for Evergrande. Onshore investors foresaw these events since their financial licenses were nationalised last September. William Hess sees Zhongzhi's bankruptcy as a positive for property sector policy support, paving the way for broader liquidity injections and demand stimulus for surviving developers. Beijing's shift towards a comprehensive bailout strategy, recognising the inadequacy of selective measures, is noteworthy. Initiatives like Guangzhou's property purchase voucher scheme and Shenzhen's urban village renovation plan aim to de-stock property inventories and rejuvenate construction. William also highlights the PBoC’s commitment to support property sector policies and construction, which – although not directly targeted towards equity markets – will be taken as positive.

Edition: 177

- 12 January, 2024

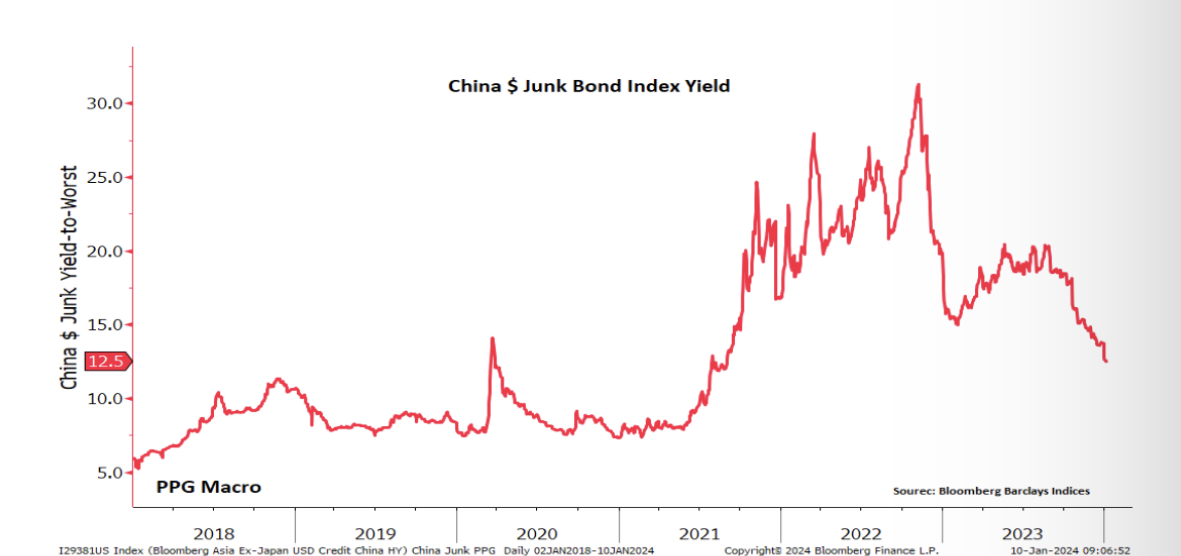

A China surprise?

The China property bust has been a long-running issue – Patrick Perret-Green first wrote about Evergrande back in July 2021. It remains a millstone around the neck of the global economy. Nevertheless, one of the possibilities that’s on Patrick’s radar is that China, relative to expectations, could be an upside surprise. If so, the impact on the global economy and markets could be significant. For all the doom and the gloom, the regime is making progress. One reflection of this is the powerful recovery in Chinese US dollar high yield bonds. There is, however, a big caveat. The fall in yields has been exaggerated by the removal of defaulters from the index, issuance collapsing to non-existent levels and bonds maturing. Over the past year the amount outstanding has fallen from $81.7 billion to $47.4 billion.

Edition: 177

- 12 January, 2024

China: Defaults en route

Warut Promboon is of the opinion that the Chinese regulators are usually reactive rather than proactive, but in the face of Country Garden Holding defaulting on its USD bonds, he believes the government will be looking to rescue more developers. Warut sees no sign of recovery in the property market, a worsening credit crisis before the situation improves and limited refinancing prospects that should deter many international investors from China. The domino effect, starting with Evergrande, is continuing and more defaults will be inevitable. The sector is not investable for the general public and only distressed specialists should endeavor any investments in high-yield property developers. He maintains his underweight recommendation on the COGARD complex despite the attractive offers of c.5 cents on the dollar.

Edition: 173

- 10 November, 2023

Chinese Banks: Focusing on the credit quality challenge

Financials

Galliano's Financials Research

Victor Galliano conducts a credit quality review of eleven Chinese banks in the light of the Evergrande and real estate sector headwinds - he also assesses the banks’ profitability ratios and their capacity to absorb increasing credit losses. Victor considers the best placed banks to be China Merchants Bank and PSBC; the most exposed to further credit quality deterioration are China Minsheng Bank and China CITIC Bank.

Edition: 122

- 29 October, 2021

China: A new and potentially dangerous phase of development

China is embarking on a new phase of development that emphasises stability over growth and signals the growing financialization of the economy. Evergrande marks the dawn of tighter Chinese policy control over credit, with big implications for the future hegemony of US finance. It may end up exposing cracks not only in China’s financial system but in Western finance too; Western policymakers should take heed not to dismiss the China threat!

Edition: 120

- 01 October, 2021

China Credit Chronicle: Hazardous National Anecdote

The fall of HNA Group and others to come is a necessary step of the learning curve for investors in Chinese credits - recent events show us that Chinese mega corporates (i.e. China Huarong and China Evergrande) have enticed international investors (and perhaps rating agencies) to ignore credit fundamentals and believe they will be supported by the local/central government when necessary. The recovery value of HNA-related bonds has become uncertain with asymmetric downside risk to all HNA-related debt, let alone SANYPH 10/21s and HONAIR Perp.

Edition: 116

- 06 August, 2021