Fortnightly Publication Highlighting Latest Insights From IRF Providers

Company Research

Consumer stocks poised for a recovery

Consumer Discretionary

AIR expects a wave of upward revisions from European corporations in the coming months as tariff clouds thin, China stabilises, infrastructure spend ramps up and European rates remain low. The missing piece is consumer confidence, which should rebound quickly if geopolitical tensions ease. Consumer names like Inditex, Stellantis, LVMH, Diageo, Kering, Adidas, Nestle and Unilever look compelling after steep share price declines, with valuations back to decade-lows. Many of these firms are pursuing clear turnaround strategies focused on FCF generation, deep efficiency gains (utilising AI) and renewed focus on core businesses - supported by a trend toward insider CEO appointments, after a decade of appointing outsiders.

Edition: 218

- 22 August, 2025

90% hit rate on Shorts, while Buy calls also continue to outperform

Since the beginning of 2024, AIR has published 41 Short ideas, 37 of which have generated absolute gains. Standout performers include B&M, LEM Holding, Remy Cointreau, STMicroelectronics, Stellantis and Valeo. In Q1 2025, AIR initiated 6 new Short positions, with LVMH leading the pack, and closed 6 positions, including a 54% gain on Aston Martin. On the long side, AIR’s Top 10 Large Cap Best Ideas returned +7.7% in Q1 this year, outperforming the Stoxx 600’s +5.2% gain. Since inception in 2012, the selection has outperformed the index by nearly 300%. Meanwhile, AIR’s Top 10 Mid Cap Best Ideas Selection delivered +17.3% in Q1, far exceeding the +4.3% return from the Stoxx Europe Mid 200 Index.

Edition: 209

- 18 April, 2025

LVMH (MC FP) France

Consumer Discretionary

In the past 20 years, Pierre-Olivier Essig has never seen as many red flags surrounding LVMH as he does today. In addition to terrible 4Q24 numbers, he highlights succession change, brand fatigue, low value retention, supply chain ethics, designer casting mistakes, unjustified pricing, as well as specific issues attached to almost every division. Pierre faced huge resistance from clients 12 months ago when he advised selling LVMH shares at €822, however, that proved to be the correct decision and in Oct, he then upgraded the stock to Buy after it fell through €600. With the share price having recently moved back above €700, Pierre turned bearish once again. He expects Hermes m/cap will exceed LVMH’s within the next year.

Edition: 206

- 07 March, 2025

Healthcare

JEH's high brand value stems from a unique business model that integrates everything from product planning and design to manufacturing, processing and sales. This approach not only differentiates it from other brands but also ensures product quality and craftsmanship, earning the trust of its customers. Yuka Marosek believes JEH’s 19x PE is not only justifiable but expandable with an OP margin of 27%, expected OP growth for 2025 of 35% y/y and ROE at 23%. She considers LVMH to be the closest benchmark due to its focus on high-end concepts and explains why JEH is a beneficiary of inbound tourism with foreign buyers attracted to the company’s glasses produced in Sabae.

Edition: 203

- 24 January, 2025

Multinationals in China: Europe vs. US

Much of what 86Research has heard this earnings season confirms insights they have previously flagged re. the China market, including the strength of Sam's Club, the robust expansion of travel demand and the competitive challenges facing Starbucks and iPhone. More remarkable, however, are the latest moves by several European multinationals, such as Volvo and LVMH, which appear committed to cross-border cooperation in areas relatively insulated from geopolitical pressures. Beneath the broader, probably over-generalised narrative of a multinational exodus, a more nuanced observation points to a potential structural shift in the origins of China-bound investments, with European firms advancing at the expense of their US counterparts.

Edition: 200

- 29 November, 2024

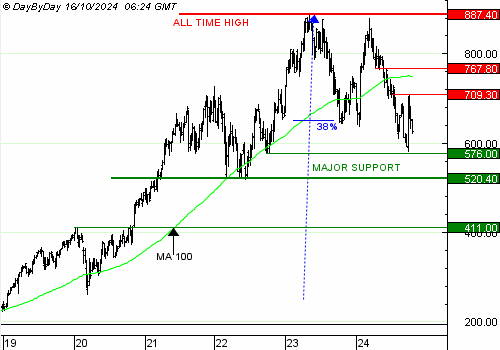

LVMH and ASML drag Europe down

European stocks fell earlier this week as ASML’s guidance cut was compounded by disappointing sales at LVMH. Recent share price action at LVMH (see chart) has resulted in the medium-term trend switching to neutral, but not bearish, meaning buying weakness is still a reasonable strategy. €520/€500 is the level investors should expect to be tested in the near term. Meanwhile, ASML is playing around its major support, the 38% Fibo of the rally since 2020. It had briefly been broken a few weeks ago, hence this new test has a very low probability of re-establishing a rise. Buying will not be an option for a while.

Edition: 197

- 18 October, 2024

Luxury downside

Consumer Discretionary

The MSCI Europe Textiles, Apparel and Luxury Goods Index accelerated to the downside last week - Valérie Gastaldy points out that prices have already fallen below the 38% Fibo since 2022 (at 1325). Should the index correct the rally since 2020, the most reasonable target would be 1207. However, should we be correcting the move since 2009, then the target would be 1020. Re. individual stocks, Hermes is trying to break below its summer lows and the next level where Valérie would consider buying LVMH is at €665. She has set major medium-term support for Moncler at €53.3, but the stock is weaker than the other two and can more easily fall significantly lower if the other two do break equivalent supports.

Edition: 169

- 15 September, 2023

LVMH & Gucci: Monthly Luxury Survey - China

Consumer Discretionary

2023 stands to be a year of resetting for luxury brands and the best hope is that 2024 builds on a moderate comp in a stabilised economy.

LVMH - sales in mainland China are estimated to have declined 5-10% Y/Y in Jul (first month of negative comp YTD). Aug decline has accelerated but could narrow as Chinese V-Day approaches. Macau and HK continue to boom on overseas buying by Chinese tourists.

Gucci - China sales have collapsed and the brand lags peers, likely due to its bold and loud design used to attract entry-level, younger shoppers going out of fashion. Gucci's deep double-digit decline could improve in Q4 as its new designer launches a new season and easy comp kicks in. However, the fundamental issue of losing share in a down market is likely to take time to address.

Edition: 167

- 18 August, 2023

There are two lanes in retail winning right now - momentum and improvement

Consumer Discretionary

Brands with good momentum include Lululemon, Abercrombie, Chico’s, Steve Madden, LVMH, Prada, Ralph Lauren and Macy’s. According to The Retail Tracker, these retailers are entering the back half of the year with the consumer on their side and good assortments. In the improvement lane, they highlight Gap, Target, American Eagle, Bath & Body Works and Nike. They also like the risk:reward in two currently out of favour names - Williams-Sonoma (a high-quality company, with exceptional brands / leadership) and Victoria's Secret (left for dead / trades at a steep discount).

Edition: 166

- 04 August, 2023

France: Europe's high conviction holding

Global equity managers are positioned at their highest ever overweight in French equities - average holding weights have moved towards the top end of the 8-year range at 4.16%, pushing net overweights to a record +1.48% above the iShares ACWI ETF benchmark. Out of the 365 global funds in Copley’s analysis, 64.4% are overweight France compared to the ACWI index. Aggressive Growth and Yield managers have led the charge. On a stock level, LVMH is the most widely held name, while Sanofi and Capgemini have benefited from fund rotation this year.

Edition: 141

- 05 August, 2022

FTSEurofirst 80 Index: Bullish & Bearish Themes

Technical Analysis

Recycling and Renewable Energy stocks such as Umicore, Vestas Wind and Siemens Gamesa are rallying from medium term support. Selective Seafood and Tobacco stocks remain defensive including SalMar, Mowi and Scandinavian Tobacco. Banks are generally rallying in ranges; favours CaixaBank and Sabadell which have already broken out and extend relative bases.

Industrials have broken uptrends and are now losing relative momentum such as Schneider, Atlas Copco and Alfa Laval. Luxury Goods renew their 4-month price and relative tops including Pandora, LVMH, Dior and Hermes. IT Hardware and Semiconductors renew their 5-month price and relative tops; SeSa, BE Semiconductor, Infineon and Nordic Semiconductor are highlighted.

Edition: 136

- 27 May, 2022

Consumer: The recovery engine is reigniting as Covid threats once again wane

Consumer Discretionary

JJK looks for the consumer’s appetite to renew normal living to support upside across PVH, Victoria's Secret, TJX and Ulta Beauty. Demand driven by a return to work, social activities and travel should fuel continued demand strength for apparel, accessories and beauty. With strong evidence from the luxury players including LVMH and Capri Holdings, JJK expects the consumer’s strong demand for these categories to be sustained, with little resistance to elevated pricing.

Edition: 128

- 04 February, 2022

Dufry (DUFN SW) Switzerland

Consumer Discretionary

If public markets don’t realise the value here, DUFN will be acquired by someone like Kering or LVMH - Brian McGough describes the “three stages to getting paid” on this dominant travel retail luxury consolidator. He argues that analysts are asleep on modelling top line recovery to 2025 where Brian is forecasting EPS of CHF 13.37 (over double consensus). With the company hitting new highs in growth, margins and ROIC, it should be hitting new peak multiples of 20-25x earnings. TP CHF 250+ (400%+ upside).

Edition: 123

- 12 November, 2021

Personal Luxury Goods Stocks: Europe's answer to the US tech giants

Consumer Discretionary

In the space of just five years, the share prices of the three French heavyweights, Hermès, Kering and LVMH have more than tripled - this is not far short of FAANG-style performance. However, given the scale of the growth and the return expectations already discounted, Piers Nestler wonders if these stocks are beginning to have a scarcity value themselves. If there is some value for money left, he believes it is most likely to be found in the watches and jewellery segment (highlights Richemont and Swatch), which has at least the potential to surprise on the upside.

Edition: 115

- 23 July, 2021

Apparel Retailers: Store Checks, Promotional Summaries & Key Data Points

Consumer Discretionary

LVMH - less enthusiastic when it comes to pre-Fall product, perhaps too much use of animal prints on classic shapes? Also wondering if the move back to smaller cross body bags creates a lower AUR mix shift for the industry.

Hugo Boss - summer sale tells the story. According to SW Retail’s proprietary data ~60% of total SKUs are on discount this season (US 63%, UK 58%, Germany 58%) vs. 27% for Ralph Lauren and 36% for Tommy Hilfiger.

Burberry - finally serious about promotions being a thing of the past. Recent price increases (Mid to HSD %) have gone largely unnoticed, but handbags continue to disappoint vs. competitors (lack of bright colours).

Edition: 114

- 09 July, 2021