Fortnightly Publication Highlighting Latest Insights From IRF Providers

Company Research

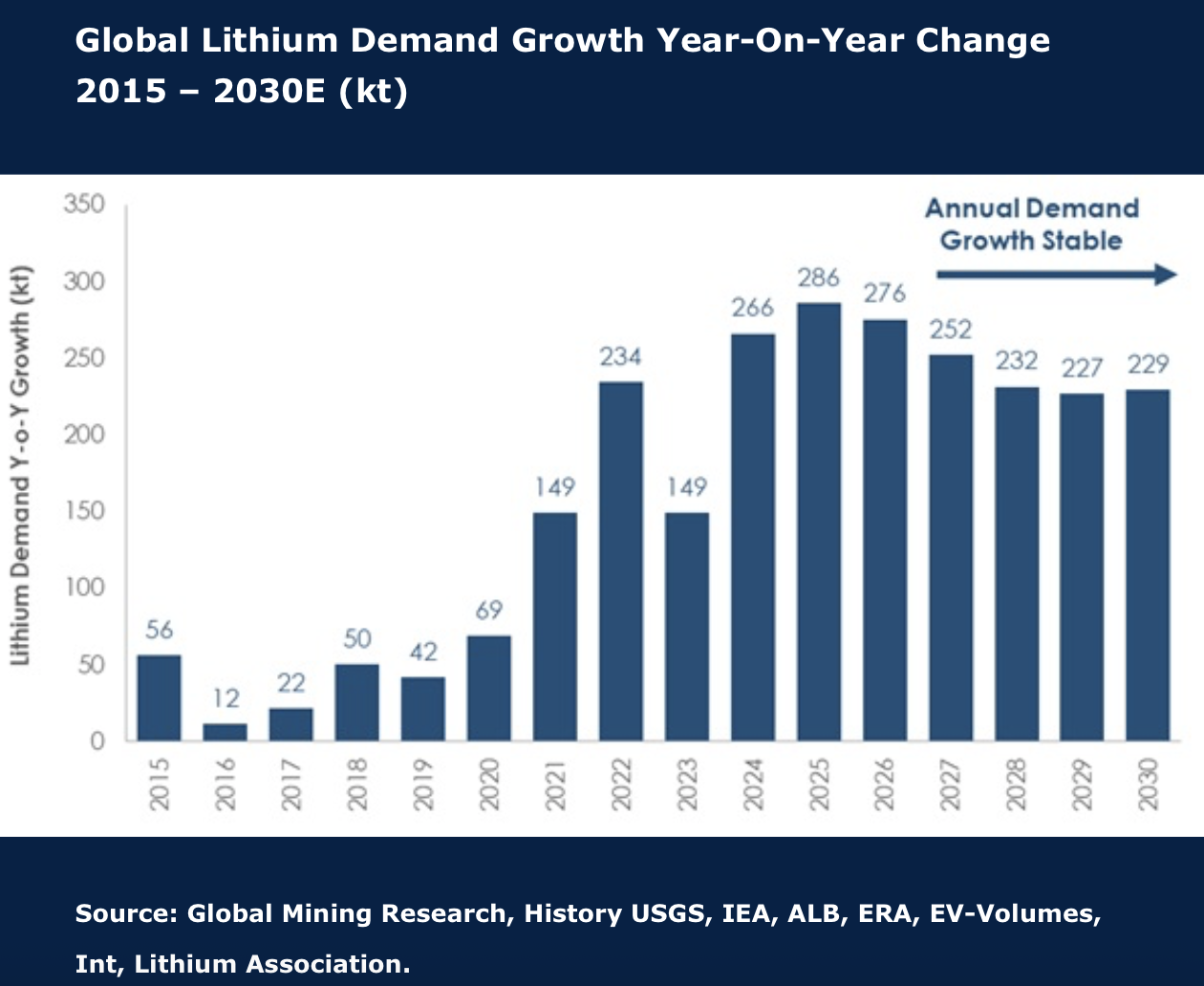

Lithium production to exceed demand to 2030

Lithium, like other minor commodities, is marked by volatile short- to medium-term cycles, with an extraordinary bull market of 2021–2022 followed by a relatively prolonged bear market. This is despite very strong demand growth, due to an equally strong (or greater) advance in production, plus inventory de-stocking. David Radclyffe finds evidence for a continued market surplus out to 2030. Although prices have recently started to turn up, an excess of idled capacity along with significant new projects coming online suggests prices will hover around the top of the cost curve for some time. Of late share prices have moved up ahead of the commodity prices, with equity markets getting more optimistic. Investors should be cautious and favour those already in production or juniors with fully financed projects. David has no Buy-rated stocks dealing in lithium. Pilbara Minerals Ltd has outperformed and, now looking expensive, is downgraded to HOLD. Rio Tinto Plc and Sociedad Química y Minera de Chile SA are rated HOLD, while Albemarle Corp, Energy Resources of Australia Ltd, IGO Ltd and Mineral Resources Ltd are rated SELL.

Edition: 226

- 12 December, 2025

Lithium: Signs of cycle troughing

The last 12 months have marked a complete collapse in lithium pricing from all-time highs. The commodity is marked by short and sharp cycles (see graph) and David Radclyffe sees evidence that investors should increase exposure: product prices are stabilising, production curtailment is underway, EV demand growth is continuing, and seniors are raising equity (like in 2021). Low prices should make Boards more cautious when it comes to adding new capacity. Having been underweight for some time, David now sees opportunity in lithium equities with preferred stocks including Pilbara Minerals and IGO.

Edition: 183

- 05 April, 2024