Fortnightly Publication Highlighting Latest Insights From IRF Providers

Company Research

The end of Net Zero at any price

As the global energy sector digests the outcome of the 2025 Duke of Edinburgh Future Energy Conference, mainstream financial press like Forbes is reporting a “reluctant consensus” regarding the transition: costs are high, timelines are slipping, and fossil fuels remain dominant. But while the headlines are catching up to the mood, Commodity Intelligence has already defined the mechanism. James Burdass produced a detailed write up on December 2nd, which can be accessed below. While others were observing a general sentiment shift, James was the first to codify this new era as the “Age of Industrial Realism.” By looking beyond the public speeches and tapping into the critical private intelligence exchanges at Mansion House, James helped shape the debate by moving it from vague “macroeconomic concerns” to hard-nosed structural realities.

Click here to read the report.

Edition: 226

- 12 December, 2025

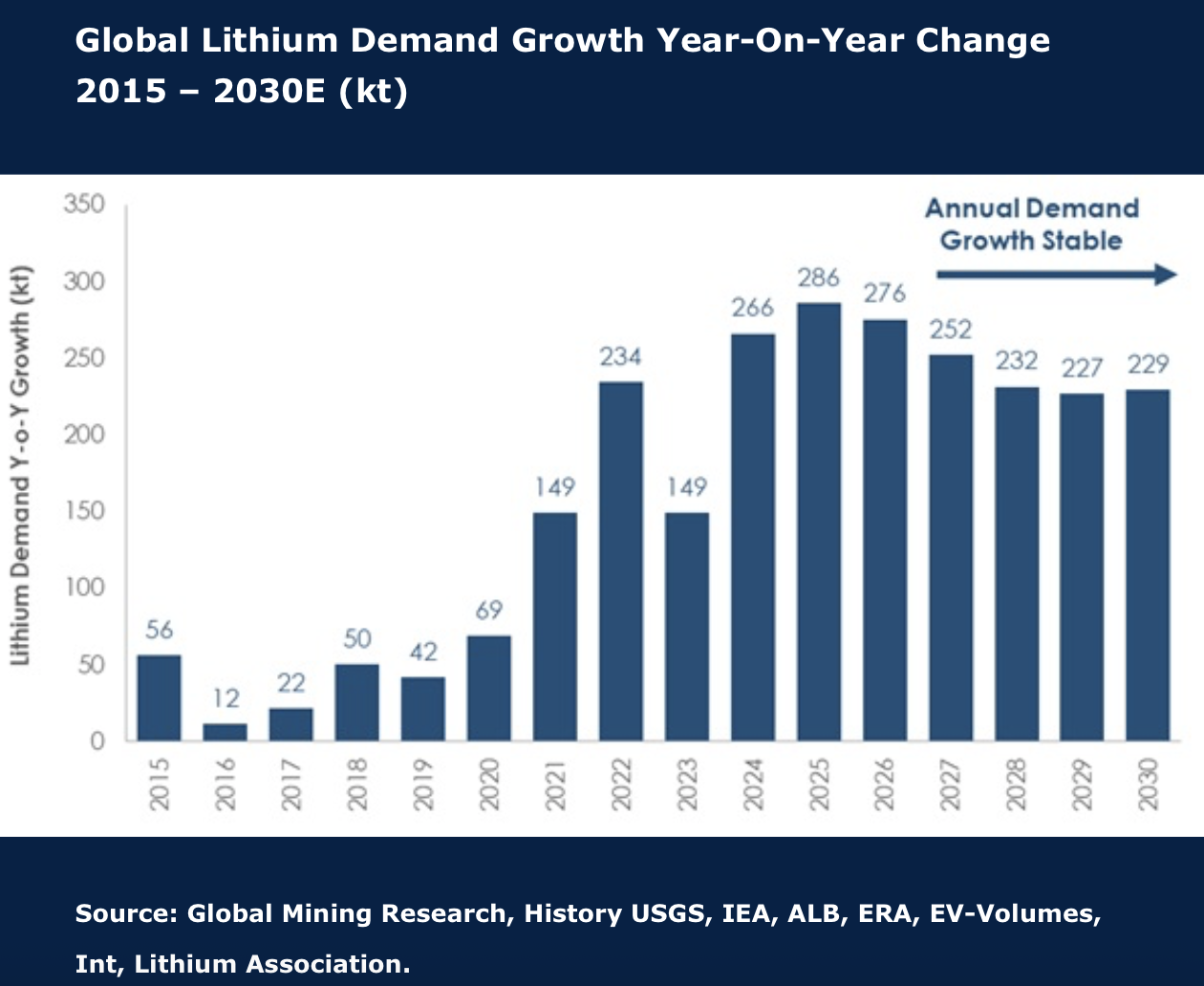

Lithium production to exceed demand to 2030

Lithium, like other minor commodities, is marked by volatile short- to medium-term cycles, with an extraordinary bull market of 2021–2022 followed by a relatively prolonged bear market. This is despite very strong demand growth, due to an equally strong (or greater) advance in production, plus inventory de-stocking. David Radclyffe finds evidence for a continued market surplus out to 2030. Although prices have recently started to turn up, an excess of idled capacity along with significant new projects coming online suggests prices will hover around the top of the cost curve for some time. Of late share prices have moved up ahead of the commodity prices, with equity markets getting more optimistic. Investors should be cautious and favour those already in production or juniors with fully financed projects. David has no Buy-rated stocks dealing in lithium. Pilbara Minerals Ltd has outperformed and, now looking expensive, is downgraded to HOLD. Rio Tinto Plc and Sociedad Química y Minera de Chile SA are rated HOLD, while Albemarle Corp, Energy Resources of Australia Ltd, IGO Ltd and Mineral Resources Ltd are rated SELL.

Edition: 226

- 12 December, 2025

2026 risks being overstimulated

Developed economies enter 2026 with inflation above target, labour markets tight, wage growth solid and governments running gargantuan budget deficits. Yet Gerard Minack points out how markets expect most central banks to ease or keep policy rates steady, Japan (and Canada & Australia) excepted. There are many hard-to-calibrate risks – such as the war in Europe, US trade policy, Fed independence – but the base-case macro-outlook is for at-or-above trend growth that threatens higher inflation and undermines the case for easier monetary policy. Gerard will discuss the implications of this for markets next week. Spoiler alert: two of the biggest issues for investors – the AI equity trade and risks around developed economy sovereign bonds – don’t hinge on the near-term cycle forecast.

Edition: 226

- 12 December, 2025

Communications

Craig Huber downgrades NFLX to Underweight following its $82.7bn agreement to acquire Warner Bros Discovery’s studios, HBO and HBO Max streaming assets - a major strategic shift he views as unnecessarily risky. He argues the deal brings significant regulatory hurdles, adds heavy leverage and could slow NFLX’s organic revenue growth while pressuring margins. Large US media acquisitions rarely succeed and NFLX had excelled for 15+ years without pursuing major M&A. With the deal likely taking 12-18 months to close, Craig expects a prolonged stock overhang. Re. Paramount’s hostile bid, he believes PSKY would need to raise its offer to $32/share to fully entice shareholders away from NFLX’s attractive proposal.

Edition: 226

- 12 December, 2025

Cisco's 800G just hit the same wall GPUs did

Technology

JNK Research indicates CSCO's Silicon One networking roadmap faces the same thermal management bottleneck that constrained Nvidia and AMD GPU production. CSCO is ramping wafer starts 8x - from 1k to 8k annually - at TSMC in 1H26. However, heat spreader suppliers already operate at 85%+ utilisation with capacity concentrated among few Taiwan suppliers. The company is proactively qualifying secondary thermal suppliers and paying for tooling upfront to secure allocation. This mirrors the CoWoS packaging constraints that limited GPU shipments in 2024. Networking ASIC thermal requirements are approaching GPU-level complexity as data centre switches migrate from 400G to 1.6T.

Edition: 226

- 12 December, 2025

Ferrari (RACE IM) Italy

Consumer Discretionary

AlphaValue sees the recent share price correction as a compelling entry point, arguing that RACE’s equity story is unchanged: a scarcity-driven model, limited volume to protect residual values and earnings growth driven by mix, personalisation and pricing. The market’s disappointment with the 2030 targets is misplaced - management has a long track record of beating guidance and the new goals look intentionally conservative. Demand remains exceptionally resilient, supported by a growing collector base, rising UHNW populations and consistently oversubscribed limited series. The stock trades at a discount relative to its historical performance and direct peers, providing a safe haven in the automotive and luxury space, insulated from macroeconomic headwinds, trade disputes and China-related risks. TP offers >40% upside.

Edition: 226

- 12 December, 2025

Communications

Hesham Shaaban argues the Street is underestimating the durability of RBLX’s monetisation surge. Historically sceptical of its Robux-driven model, he now sees clear evidence that incremental traffic is highly monetisable: mid-2025 saw a material surge in traffic (DAUs and Hours) with limited slippage in bookings efficiency, which isn’t typical of a freemium model. Engagement is also “snowballing”: the fact that average hours are even up Y/Y - especially double digits - on a 70% surge in DAU growth suggests engagement is now viral. Hesham sees 4Q25 earnings as the key catalyst - he expects RBLX to produce booking growth more comparable to Q3 results than management's muted guidance triggering a short squeeze.

Edition: 226

- 12 December, 2025

Industrials

Results will not live up to the enormous expectations surrounding this story, as the company shows almost no customer traction beyond Walmart. While SYM is rolling out systems across 42 WMT distribution centres through 2029, new wins have been minimal, leaving a massive revenue gap ahead. In contrast, competitors Knapp and Witron have announced dozens of new customers since 2022 including new business with WMT. Half of the company’s touted $22bn backlog sits in a stalled SoftBank JV (GreenBox), with little evidence of progress. With heavy insider selling, a recent revenue restatement, TAM overstated and the stock trading at ~10x 2027 sales, the bear case sees estimates beginning to be revised down next year and SYM’s valuation potentially halving.

Edition: 226

- 12 December, 2025

Meesho (MEESHO IN) India

Consumer Discretionary

Meesho enters its IPO with strong user and order growth, but Iii flags mounting financial-quality concerns. Despite improving KPIs, the company remains loss-making and faces significant litigation risk, including large tax-related disputes. More troubling, impairments and write-offs are rising sharply: the company has written off INR 223m in bad debts over the past 18 months, its impairment provision has jumped from INR 110m in FY24 to INR 588m in 1H26 and total impairments plus write-offs reached INR 720m in 1H26 alone. Heavy churn in key management roles, new regulations around employee worker costs and recurring audit-trail weaknesses further underscore the risks for investors considering this IPO.

Edition: 226

- 12 December, 2025

South Africa: One notch down, guard up

Krutham (formerly known as Intellidex)

The SARB delivered the unanimous 25bp cut that Peter Montalto expected, but this was no dovish pivot: the CPI path was only nudged slightly lower and the language stayed cautious. The MPC is now comfortable moving into “less restrictive territory”. It means that the country now sits a little above the new neutral range around 6.50%. Looking ahead, Peter remains more conservative than the QPM on both inflation and the policy path. He still sees a stickier non-core wedge and slower expectations pass-through than the model assumes, given the fixed public-sector wage agreement, Nersa’s tariff pipeline and unusual food CPI seasonality, even though the de jure shift to a 3% target pulls the expectations profile down. That keeps Peter above the SARB’s inflation and repo projections: his baseline is no further change for roughly six months, and a clearer next leg down only in H2 2026 to 6.00% end 2026.

Edition: 226

- 12 December, 2025

Materials

Yuka Marosek examines whether ISK can narrow its sizable profitability gap with Nissan Chemical, whose operating margins are more than triple ISK’s. She attributes the gap to ISK’s heavier reliance on lower-margin TiO₂ and inorganic chemicals, while Nissan benefits from higher-value agrochemicals and semiconductor materials. ISK’s mid-term plan aims to shift its portfolio towards higher-value TiO₂, consolidate production under the chloride process, upgrade its functional materials mix and continue disciplined R&D investment. Early signs are constructive: ISK’s Q2 FY3/26 margins have already begun to recover, helped by improving TiO₂ pricing and mix. With further optimisation, new capacity through the MF Material JV and a strengthening agrochemical/vet-pharma pipeline, Yuka sees credible scope for margin expansion and valuation catch-up.

Edition: 226

- 12 December, 2025

Financials

MCAP is emerging with the strongest momentum in Japan’s once-tainted M&A consulting sector. Unlike scandal-hit peers, MCAP avoided reputational damage and is now growing faster than Nihon M&A, generating higher margins and trading on just ~15x FY9/26 earnings despite forecasting >30% Y/Y profit growth (which may well prove conservative). Deal sizes are rising, consultant numbers are compounding 20-25% annually and MCAP’s high-incentive pay model draws top sales talent, keeping churn low. The company’s Recof subsidiary remains a drag, but restructuring should push it towards profitability. With improving industry governance, fears of a “kabarai-style” crackdown fading and cash piling up from strong FCF, the shares are attracting renewed investor interest.

Edition: 226

- 12 December, 2025

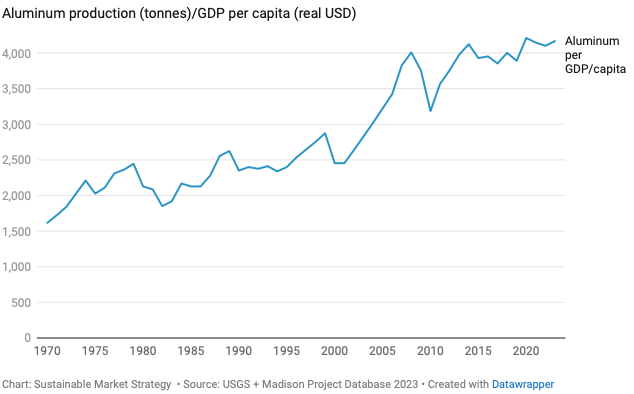

Aluminium in transition: The neglected materials play?

Fossil fuel demand may be falling in the future, but aluminium certainly won’t, driven by demand for EV and solar adoption, the great grid buildout and more aggressive lightweighting. There are no physical constraints to aluminium supply, with bauxite a plentiful resource that can be found near the earth’s surface, yet supply is expected to tighten relative to demand beyond the next three years. China is the main reason, having imposed a national ceiling of 45m tons per year on primary aluminium production. The next big reason lies in electricity constraints; given the amount of electricity required to produce aluminium, the economics of the metal are essentially the economics of power. Competitive advantages are available for producers with sizeable recycling operations, which the team expects to outperform over the next few years. Expect the likes of Constellium, UACJ Corp and Norsk Hydro ASA to be the biggest relative winners.

Edition: 226

- 12 December, 2025

Technology

2Xideas argues OS is tapping into a large, visible market opportunity as enterprises replace outdated software applications and tools. The company continues to gain market share, strengthening its position relative to peers and is on a "winner‑take‑most" path. Furthermore, OS is well‑positioned to integrate emerging AI technologies, benefitting from its role as a trusted governance and compliance layer, which largely insulates it from disruption. 2Xideas forecasts 19% revenue CAGR, driven by new customer wins, strong cross-/up-sell opportunities and international expansion. Over the next 5 years, they expect a total shareholder return of 20.8% p.a., based on an exit NTM EV/Sales multiple of 8.0x.

Edition: 226

- 12 December, 2025

Ivanhoe Mines (IVN CN) Canada

Materials

A 2026 copper turnaround story - IVN is now producing from all 3 of its core and globally significant mining assets. However, this has not been reflected in the share price following the seismicity event at Kakula in May 25. The market is focused on short term risks, but Kakula’s recovery is being managed and 3Q25 volumes (annualised at 285kt/yr) likely marks the bottom. With the 3 operating assets contributing in 2026 and a new smelter set to lower costs, GMR sees next year as the inflection point. IVN also offers major exploration upside - its 100%-owned Makoko district alone has 9.2Mt of copper identified, with additional drilling across Angola, Zambia and Kazakhstan providing further optionality not priced in. Trading at 1.4x P/NPV10, IVN’s growth, scalability and asset quality make the risk/reward compelling.

Edition: 226

- 12 December, 2025

Industrials

BTN views AAON as exhibiting some of the most aggressive revenue-recognition practices in its peer group. The degree to which revenue is pulled forward makes it difficult for the company to sustain momentum from quarter to quarter, resulting in pronounced volatility in reported results and limited visibility into the underlying run rate. Unbilled contract assets remain elevated at 50 days of sales (vs. 27 days a year ago), reflecting AAON’s practice of booking revenue upfront when parts are ordered. Receivables increased $96m sequentially, reaching a new high of 64 days of sales and was the primary driver of the revenue beat. Falling inventory days suggest Q3 was backloaded, consistent with the jump in accounts receivable. OCF remains negative, with BTN sceptical of management’s claims of a swing to positive cashflow in 2025. The company is borrowing and stretching payables to plug the gap.

Edition: 226

- 12 December, 2025

Technology

Jun Lei (Co-Founder) purchased ~ $12.9m worth of stock at HKD 38.58. While modest relative to his 1.9 billion-share stake, the purchase is noteworthy. It is his first open-market acquisition in this stock and also represents the first meaningful insider purchase since the IPO in July 2018 at HKD 17. Despite the recent share price decline, it is interesting to see him making a sizeable purchase shortly after the company released its Q3 earnings. Smart Insider ranks the stock +1 (highest rating).

Edition: 226

- 12 December, 2025

Kroger indicates more price reductions are ahead

Consumer Staples

Scott Mushkin has been highlighting for several months that price discounting would become more aggressive by the end of 2025. His latest findings show Walmart has become increasingly willing to drive down prices and Kroger is gearing up for battle, using a part of its ecommerce rationalisation to lower prices to become more competitive. The increase in competition, unfortunately, will come with further erosion in end demand. This is related to GPL-1 coverage in Medicare and Medicaid, GLP-1 oral compounds coming to market and some additional curtailment in SNAP benefits. At the same time, the continuation of the MAHA trend will remain a headwind. This marks the beginning of what will be a tougher period for the industry, especially those such as Kroger, that have significant overlap with Walmart.

Edition: 226

- 12 December, 2025

Consumer Staples

John Zolidis sees DG’s Q3 results as strengthening both the near- and long-term bull case, with traffic growth and gross margin expansion reinforcing that estimates remain too low. The long-term opportunity is margin recovery: FY24 EBIT margins were 4.7% vs. a 10-yr average of 8.9%, yet DG is targeting 6-7%, far above what the Street has modelled for FY26/27. Near term, analysts were expecting a H2 slowdown, but Q3 comps and margins instead accelerated, suggesting upside - especially as consensus Q4 GM (30%) looks far too conservative vs. 31.2% in H1 and a long history of Q4 outperformance. With execution improving under returning CEO Todd Vasos and profitability still well below historical levels, John sees room for further re-rating.

Edition: 226

- 12 December, 2025

Earnings manipulation, anyone?

Two Rivers has recreated the Beneish model showing the highest potential manipulators and highlighting stocks such as QXO (due to M&A-driven sales spikes for AI supply chain plans), Joby Aviation (high growth amid declining margins), Rivian (rising accruals suggesting expense capitalisation), Alpha Metallurgical Resources (falling gross margins) and Pinterest (rising balance sheet accruals and sales growth). The model's inputs are similar to some that Two Rivers use in their own Stock at Risk's Earnings Quality model - albeit with some additional proprietary “secret sauce”.

Edition: 226

- 12 December, 2025

Shorts continue to deliver impressive alpha

Vision has closed 4 short ideas so far in Q4. Wingstop, initiated in 3Q25 on the view that its rich valuation was unsustainable amid intense competition, category saturation and a disappearing customer cohort benefit, delivered 40%+ alpha. Duolingo, also a 3Q25 initiation, faced a massive influx of AI produced competition at lower cost and some slowing in KPIs, generated 30%+ alpha. Kadant, shorted in 2Q24 as a late-cycle capital goods name with deteriorating fundamentals but a “priced-for-perfection” multiple, added 30%+ alpha. Patrick Industries, initiated in 1Q25 given its peak multiple on overly optimistic estimates and exposure to excess inventory, weak demand and tariff/regulatory risks, generated 5%+ alpha. YTD, Vision has launched 13 new US shorts, 7 European shorts and 5 APAC shorts, with 2-3 more initiations expected before year-end.

Edition: 226

- 12 December, 2025

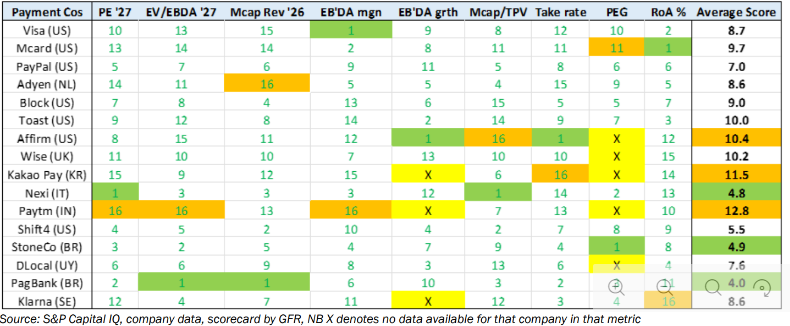

Payment Companies: 1H26 high conviction ideas

Technology

Galliano's Financials Research

Nexi is Victor Galliano’s top pick - it screens as one of the cheapest global payments names on market cap to revenue and market cap to TPV, with expanding EBITDA margins, rising take rate and improving cash opex discipline, all supported by increasing digital-payments penetration in Italy. PagSeguro remains his core LatAm Buy, despite strong YTD performance, valuations are still compelling and it ranks highly on Victor’s proprietary scorecard (see above), with a high net take rate relative to market cap to TPV. Affirm is the key Sell: Klarna’s IPO erodes scarcity value; valuation looks stretched on market cap to TPV and credit quality in its interest-bearing receivables is worsening. Klarna is one to watch - cheaper post-IPO, but BNPL competition and credit risks keep Victor on the sidelines pending a clear catalyst.

Edition: 226

- 12 December, 2025

Wolters Kluwer (WKL NA) Netherlands

Industrials

Concerns that AI threatens WKL are significantly overstated; in reality, AI is reinforcing its competitive position. WKL’s AI-focused analyst teach-in underscored how rapidly the company is evolving into an AI-first, cloud-native software and content provider. Recurring, AI-enabled digital revenues continue to grow strongly, supported by deeply entrenched platforms in tax, legal and healthcare that deliver high customer stickiness and expanding scale efficiencies. Management also highlighted the rising financial burden of US clinical errors (USD 38.5bn in payouts from 2009-18), emphasising the value of WKL’s proprietary evidence-based, longitudinal data in reducing risk and liability. With solutions that deliver far more savings than they cost, the IDEA! maintains a positive stance on the stock.

Edition: 226

- 12 December, 2025

FLSmidth (FLS DC) Denmark

Industrials

Iron Blue initiates coverage on FLS with a score of 29/60, which is top decile and fertile grounds for shorting. They highlight 1) reliance on percentage of completion revenue recognition with an associated rise in FY24 balance sheet contract assets; 2) elevated stripped out restructuring and software/R&D amortisation costs; 3) evidence of deteriorated client payment behaviour; 4) FY24 headline margins supported by Y/Y reductions in inventory and bad debtor impairment expense; 5) DKK1bn headline net debt adjustments from reverse factoring and restricted cash; and 6) many disclosure gaps.

Edition: 226

- 12 December, 2025

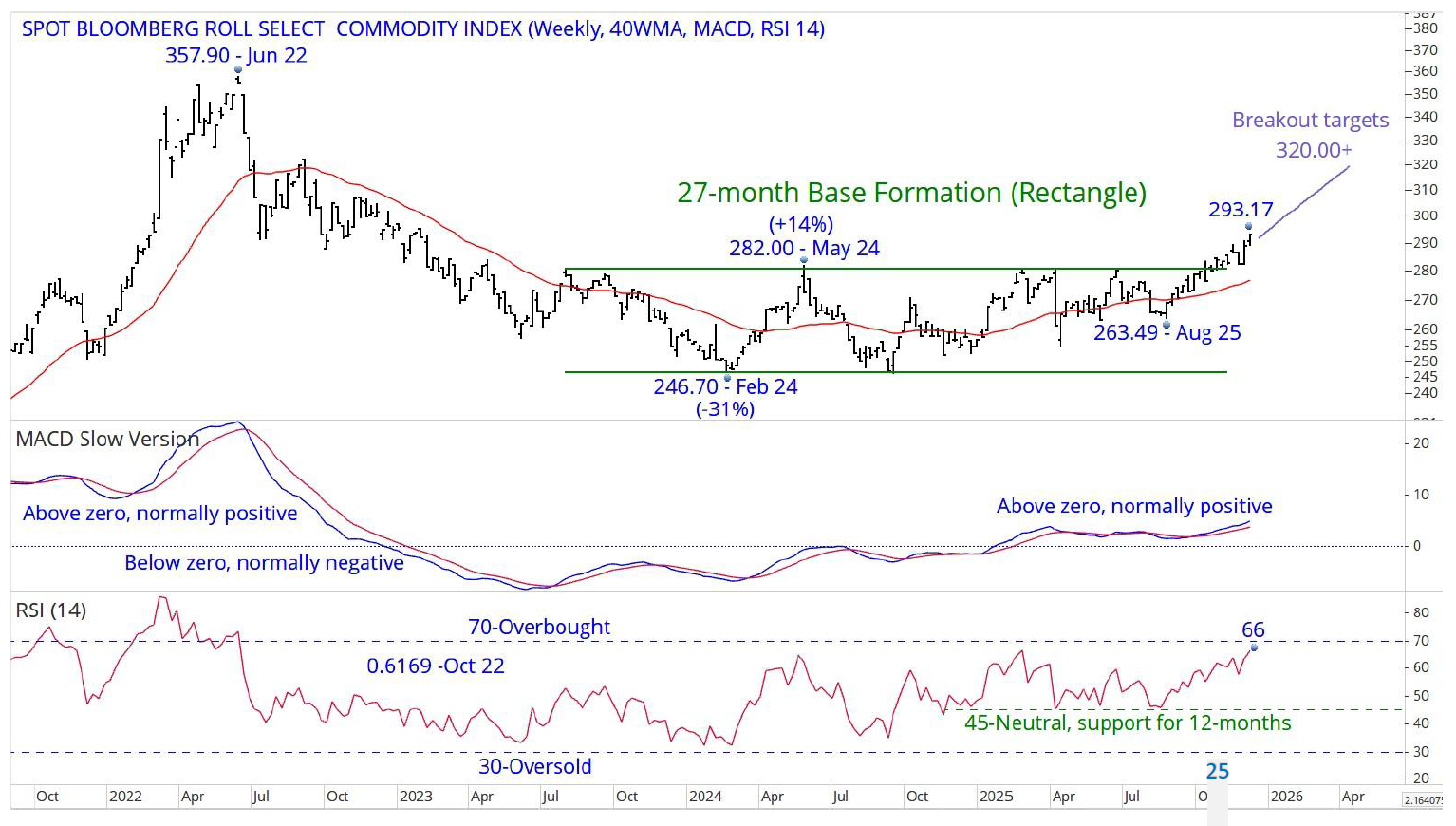

Don’t fall asleep at the wheel, this is a secular bull market

The Spot Bloomberg Roll Select Commodity Index (293.17) is the instrument that Chris Roberts’ newest data provider has, that is just about identical in shape to the Bloomberg Commodity Index that he used to feature. The breakout from the 27-month base formation targets a move to 320.00+, but Chris’s target is a new high above 2022’s 357.90. A secular bear market ended in April 2020 (see next page). The 1st leg of a secular bull market ended in 2022, and following a 30%+ decline and a distracting, time consuming sideways movement, the 2nd leg up is now underway. Indicators have room for further gains.

Edition: 226

- 12 December, 2025

Apple: HBM reallocation adds $4bn to iPhone memory bill

Technology

JNK Supply Chain Research reveals AAPL's iPhone memory costs have doubled as a share of BOM - from 5% to 10% - driven by structural HBM reallocation, not cyclical shortage. iPhone 17 Pro Max memory runs $41-$43 per unit vs. $22 in iPhone 15 Pro Max. Across 225m annual shipments, that is $4bn in incremental cost AAPL absorbs through margin compression, not price increases. HBM production for AI accelerators consumes 3x normal wafer capacity. SK Hynix and Samsung control 95% of DRAM supply with all capacity sold through 2026. AAPL negotiates from a position of weakness and there will no relief until late 2027 when new NAND lines come online. For timing of the resulting GM impact, contact us below. AAPL and other smartphone makers are covered in JNK's Consumer Tracker.

Edition: 225

- 28 November, 2025

Real Estate

JSB is defying Japan’s demographics. Despite the shrinking pool of 18-year-olds, Yuka Marosek argues the student-housing leader continues to compound growth thanks to rising university enrolment, a structural shift away from general rentals toward purpose-built student housing and JSB’s unmatched operational moat. While foreign-student demand adds another tailwind. The company runs ~99,300 units with 18 years of 98%+ occupancy and 11 consecutive years of revenue/profit growth. Valuation-wise, JSB trades at an EV/EBITDA of 8.3x and a P/E of 14.4x - levels that appear low given the group’s ability to deliver steady growth.

Edition: 225

- 28 November, 2025

The Philippines – Protests will not confront Marcos, but the president remains at risk

Major anti-corruption rallies are scheduled throughout the country for 30 November. Civil society groups primarily associated with the middle class — such as the Catholic Church, private universities, professional groups and the business community — are taking the lead. The loose coalition leading this weekend’s protest is critical to political stability, given its prominent role in shaping the broader media narrative and eventually mobilizing the broader population. The consensus view in Manila is that while the broader coalition is calling for accountability and reform, it is still not yet aiming to target President Ferdinand Marcos Jr. directly. Instead, protesters are expected to apply indirect pressure by calling for the president to allow for investigations to continue unimpeded and for the prosecution of high-ranking lower house, senate and executive officials. One key reason for the coalition’s less confrontational stance toward Marcos is that they are less certain that the president himself participated. Driving this consideration is the coalition’s deep unease over the prospect of Vice President Sara Duterte succeeding to the presidency.

Edition: 225

- 28 November, 2025

Emerging leaders in data & AI

Technology

Channel sentiment this quarter shows mixed momentum across data platforms. Elastic saw fewer partners meeting targets amid rising competition and questions about AI-driven sustainability. MongoDB continues to receive more positive views, benefitting from diversified modernisation wins and strong Atlas demand, setting up for a strong Q4. Snowflake is also receiving strong views as they evolve their partner model with new incentives, expand their work with System Integrators and accelerate AI-driven use cases. Box is sharpening its focus on high-value partners and operational AI workflows. Channels see Box benefitting as end users work to manage unstructured data for AI use cases. Click here to access the report.

Edition: 225

- 28 November, 2025

Telefonica (TEF SM) Spain

Communications

The Chair, CEO, CFO and 2 other executives bought a total of €1.3m of stock at ~€3.70 following share price weakness after the earnings release and a dividend cut. Marc Thomas Murtra (Chairman since Jan 25) bought €500k of stock in his first purchase since joining TEF, Emilio Rodríguez (COO since Mar 25, joined 2018) bought €500k worth of stock in his first purchase since he became declarable in 2025 and Laura Abasolo Garcia De Baquedano (CFO since 2017) bought €91k of stock in her first clean purchase. Pablo Antonio De Carvajal Gonzalez (Divisional Director) bought €126k of stock in his largest purchase and his first since 2019. Juan Azcue Vich (CSO since Jan 25) bought €74k of stock in his first purchase since joining. Whilst a likely co-ordinated response to disappointing news, the magnitude of the purchases is notable.

Edition: 225

- 28 November, 2025

Consumer Discretionary

Alibaba’s stepped-up AI investment is pressuring margins, but RFM argues it has now hit critical mass in open-source AI, making it the leading contender in China’s artificial intelligence race. Headline revenue growth in Q2 was only +5% Y/Y, but was +15% adjusting for disposals. The standout was Cloud Intelligence, +34% Y/Y, powered by surging demand for AI services. Qwen now has 180,000+ models on Hugging Face, more than double the No.2 player, giving Alibaba the network-effect scale needed to dominate China’s AI ecosystem. With core e-commerce stabilising and shares far cheaper than Amazon (17x FY26 P/E vs. 29x), RFM sees sentiment turning decisively positive.

Edition: 225

- 28 November, 2025

Healthcare

Tom Tobin thinks there are several secular trends, including AI tailwinds, which makes RDNT a compelling idea even after its share price has rebounded in recent months. Core to Tom’s thesis is his ability to track Diagnostic Radiology staffing at RDNT, monitor turnover, and forecast volume and revenue per clinician. While the current valuation against consensus estimates appears stretched, he can model upside well into 2027 with a number of simultaneous secular tailwinds that justify the premium: 1) continued inpatient-to-outpatient imaging migration; 2) mix shift towards high-margin advanced imaging where demand is being driven by Alzheimer's, Oncology and Cardiology; and 3) AI tailwinds driving incremental revenue and operating leverage.

Edition: 225

- 28 November, 2025

Time to buy Greece

Greece is healing - after a brutal 15-year wait, the country has finally regained its BBB investment-grade rating from Fitch. Despite chronic under-investment in infrastructure, Greek corporates have expanded at home and abroad and now boast strong balance sheets, often with net cash - a rarity in Europe. Ultra-low labour costs and the highest workload in the EU have boosted competitiveness, while political stability since 2019 has restored investor confidence. Yet Greek equities still trade at half their 2008 market capitalisation, leaving substantial upside for companies that are leaner, stronger and more agile than their European peers. AIR’s Buy-rated ideas include Athens International Airport, Motor Oil, National Bank of Greece and Sarantis, each offering 40-100%+ upside.

Edition: 225

- 28 November, 2025

Technology

Arete sees Sony as one of their most compelling ideas, offering structural, multi-year growth outside the AI-bubble debate while still benefiting from AI tailwinds. Their enthusiasm for the stock is based on 1) the ~50% of revenue that is now recurring and 2) rising appreciation for its multiple growth segments (in anime, immersive content, game and music publishing, and image sensors). Sony can be rethought as having two distinct and equally strategic businesses: Content Creation and Enabling Tech/Platforms. FY26 is set to be a banner year - GTA VI, Wolverine, Spiderman, Crunchyroll, and expansion for Image Sensors with Autos wins ramping, Electronics getting cost actions and excess cash piling up. Arete expects mid-teens EPS growth in FY26 & FY27 and even on modest multiples - 12x EV/EBITDA - they get a TP of ¥5,750 (25% upside).

Edition: 225

- 28 November, 2025

Palantir CEO’s defensiveness raises some red flags

Technology

MYST highlights a worrying behavioural shift after analysing CEO Alex Karp’s recent media appearances. Following the stock’s sharp pullback, he has adopted what behavioural economists call “defensive attribution” - a psychological bias where people facing harsh criticism attribute negative outcomes to external factors rather than accepting personal responsibility. Karp’s responses increasingly dismiss critics, question motives and escalate into personal attacks. While MYST are not insinuating PLTR is a fraud or a bad business, his rhetoric mirrors CEOs from some of the biggest corporate scandals.

Edition: 225

- 28 November, 2025

Elekta (EKTAB SS) Sweden

Healthcare

EKTAB delivered a Q2 profitability beat despite tariffs and FX headwinds, while sales were only slightly soft, helping spark a sharp rebound in the shares. Adjusted EBIT came in 6.5% above expectations and margins rose to 10.1%, supported by mix and pricing. Although China and the US weighed on revenue, order intake grew and China’s book-to-bill ratio exceeded 1.3x suggesting a potential recovery ahead. H2 should be stronger, with improving China trends and US approval of Elekta Evo expected. The new CEO’s restructuring plan - cutting ~450 jobs (10%), simplifying the organisation and cancelling low-quality orders - targets SEK500m+ annual savings. With a robust SEK34bn backlog and solid uptake of new products, AlphaValue maintains a positive view as the turnaround gains traction.

Edition: 225

- 28 November, 2025

Technology

The wolf may finally be at the door…Blue Lotus downgrades the stock to Sell. SMIC posted a strong 3Q25 profit beat - mostly driven by volatile G&A associated with fab start-up - while its Q4 revenue guide of 0-2% Q/Q fell well short of Blue Lotus’ +6.8% expectation. They now see rising risk of an air pocket heading into 2026 as Beijing holds back stimulus until after March’s Two Sessions, while headwinds loom across segments that make up 75% of SMIC’s revenue: smartphone weakness from a DRAM shortage, suspension of home appliance trade-in subsidy and slowing NEV growth as tax breaks phase out. While SMIC’s aggressive capacity buildout is positive in the long run, it makes the group vulnerable to demand fluctuations and depreciation is expected to spike to 37% of revenue, leading to a gross margin cut from 26% to 17%. TP HK$51 (25% downside).

Edition: 225

- 28 November, 2025

Technology

ZM delivered a "clean sweep" Q3 that should silence the sceptics. This was not just a beat-and-raise quarter; it was a validation of the company’s structural pivot from a meeting app to an AI-first work platform. With revenue and EPS ahead of forecasts, a raise in FY26 guide and a fresh $1bn buyback authorisation, management is demonstrating immense confidence in the company's capital allocation and operational execution. The real story for investors, however, is the tangible monetisation of AI: usage is up 4x Y/Y and paid AI features are now anchoring 9 out of 10 large CX deals. With the core business stabilising and the AI/CX growth engines firing on all cylinders, ZM offers a rare combination of deep value (trading at ~3.2x EV/Sales vs. peers at 3.7x) and highly profitable growth.

Edition: 225

- 28 November, 2025

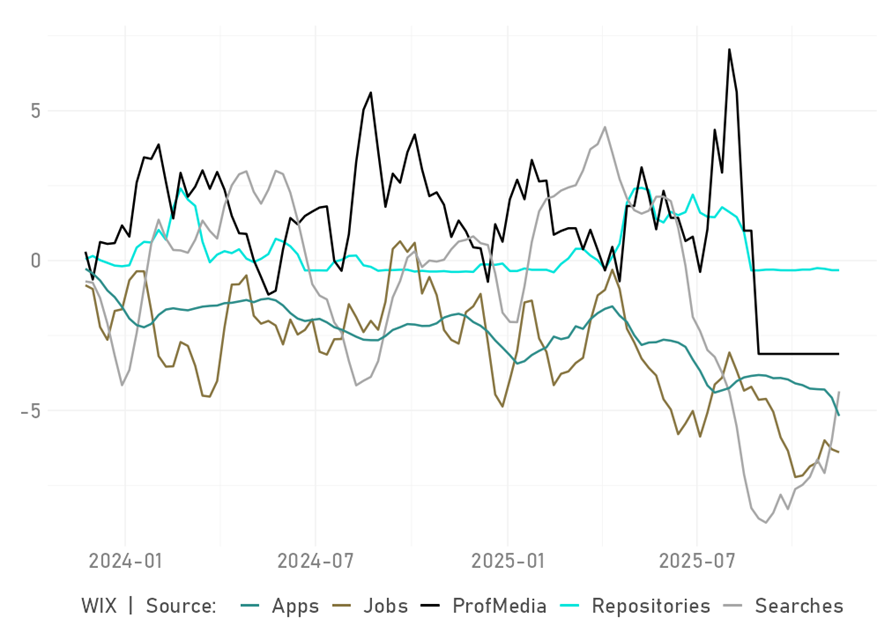

Technology

AnteData flags a sharp deterioration in developer engagement around WIX in 2025, with a TrendRank of just 0.02 - near the bottom of their software universe. GitHub pushes and Stack Overflow discussions are especially weak, signalling that fewer developers are building WIX-related code repositories and that community interest is fading. In contrast, website-building tools Vercel and Webflow show rising coding activity, which indicates a shift in website architecture. WIX holds only ~5% of a market dominated by WordPress (~40%) and Shopify, and AI tools plus social platforms are eroding demand for traditional no-code site builders. The stock has fallen 50% YTD, bringing its Price/Sales ratio down to a moderate 3x. However, the Street still expects DD sales growth. And the stock is not yet priced like low-growth comparables such as GoDaddy or Dropbox, suggesting further downside potential.

Edition: 225

- 28 November, 2025

Anglo Asian Mining (AAZ LN) UK

Materials

Ben Jones reiterates his bullish view with the stock up ~200% since initiation in July 23. AAZ is set to enjoy a dramatic increase in net income as well as FCF which is expected to swing from -$2m (2024) to c.$126m (2026) - a 45% FCF yield on today’s m/cap. He expects AAZ to develop 3 new mines (without raising equity) over the next 5 years which will boost copper production from 2.1kt in 2023 to around 40kt per year from 2028. Ben increases his base case price target from £3.70 to £5.59 (150% upside), assuming long-term copper prices at $4.50/lb, but with optionality to £8.00+ if long-run copper averages $5.50/lb, as forecast by Citi and BAML. Since publication of Ben’s report, AAZ has disclosed it is in preliminary takeover talks - unsurprising given his view that the market continues to undervalue the company’s asset base and growth profile.

Edition: 225

- 28 November, 2025

Consumer Discretionary

Hesham Shaaban argues that EXPE’s strong 3Q25 may be a head fake, with the apparent re-acceleration simply reflecting a return to pre-Covid travel seasonality rather than any revival of “Revenge Travel”. TSA passenger volumes are flat YTD and EXPE’s room-night growth is tracking 2024 levels, suggesting travel demand is merely normalising, not strengthening. Hesham sees EXPE as a useful beta offset to his long ideas, while noting the post-print rally looked like a short squeeze. The key catalyst is 4Q25, where he expects a light 2026 guide - EXPE often sets high Q4 targets only to lower them the next quarter, while consensus estimates leave little room for upside and nothing in the traffic data signals a demand resurgence.

Edition: 225

- 28 November, 2025

Financials

Abacus revisits BN after a 70%+ rise since their Jan 24 write-up, arguing the fundamentals remain as compelling as ever. They still see a 22% IRR over the next 2 years - even assuming a persistent ~30% SOTP discount. BN’s thesis is simple despite its perceived complexity: a longstanding focus on infrastructure positions it as a major beneficiary of US on-shoring and increased infrastructure spending, while structural growth tailwinds support its insurance and wealth platforms (Brookfield Wealth Solutions is highly attractive at ~1x book, given 15% ROE). Although BN is improving its communication, Abacus argues few investors appreciate the value, leaving ~35% upside to their TP of $63.

Edition: 225

- 28 November, 2025

Consumer Discretionary

Paragon Intel is bearish on HOG’s new CEO, Artie Starrs, arguing that while he may mend dealer relations and bring an outsiders’ perspective to the company, he is not equipped to deliver the deep brand turnaround required after two prior CEOs already failed to halt the brand’s decade-long decline. Paragon’s analysis includes interviews with Starrs' former colleagues from Yum! Brands and Topgolf. They found mixed and often critical feedback: he is seen as polarising leader, valued by some sources as a strategic thinker with strong financial acumen, boardroom presence and the ability to drive large-scale initiatives, yet criticised by others as overly numbers-driven, aloof and weak at culture-building.

Edition: 225

- 28 November, 2025

Google locks CoWoS capacity independent of Broadcom

Technology

JNK's research shows GOOG's direct TSM capacity reservations signal a shift away from expensive third-party AVGO design partnerships. The company is now booking advanced packaging without immediate orders, positioning for late 2026 TPU production deployments. TPU 7e progresses with MTK handling I/O integration on roughly 2M unit volumes, while TPU 8p selection between AVGO and AIchip reflects growing design house pricing pressure. This mirrors AWS's trajectory - from external partnerships towards full internal design control. Near-term, Alchip and MTK benefit from current programmes. Longer-term, AVGO faces structural headwinds as hyperscalers internalise capabilities. Click here to access the full note.

Edition: 224

- 14 November, 2025

Financials / Business Services Idea Forum

Financials

Many of the ideas presented at MYST’s buyside event featured a rate sensitivity or credit angle, while a few focused on competitive dynamics and incorporated unique proprietary data to track. It was noteworthy that several of the stocks discussed are either trading near 52-week lows or near recent highs. The most compelling ideas included:

Chime (CHYM) - Trading at substantial discount to peers despite strong member growth potential. TP $31 (65% upside).

Nu Holdings (NU) - Earnings set to inflect as Mexico losses abate while Brazil lending re-accelerates. TP $25 (55% upside).

Kinsale (KNSL) - Combined ratio unsustainable as competition intensifies in softening market. TP $270 (30% downside).

Blue Owl (OWL) - Dividend cut likely amid elevated leverage + margin compression. TP $11 (25% downside).

Edition: 224

- 14 November, 2025

Bharti Airtel (BHARTI IN) India

Communications

New Street turns more positive on Bharti, arguing that focus is likely to shift back to the company itself after Airtel Africa and Singtel materially outperformed over the past year. Bharti has historically rallied ahead of tariff hikes and with price increases expected in H1 next year, momentum should build. Growth is accelerating across Home and Enterprise, AAF continues to perform strongly and capital intensity is now falling, supporting margin expansion and rising ROIC. With fixed wireless access (FWA) adoption gaining traction and scope for meaningful EBITDA beats through FY26-27, New Street raises their TP to INR 2,750 and sees a strong case for re-rating as earnings expectations climb.

Edition: 224

- 14 November, 2025

Technology

PATH has repositioned itself as an “agentic automation” platform riding the AI narrative, but the fundamentals point to slowing growth. Expansion within existing customers is under pressure and the company’s ARR metric - built on future invoice value rather than reported revenue - overstates momentum relative to true performance. Guidance has improved modestly, but it is based almost entirely on FX tailwinds and timing shifts, rather than underlying demand. Deferred revenue and billing trends point towards a normalised growth rate several hundred basis points slower than reported results and management’s increasingly promotional tone around partnerships leaves much to be desired. With federal spending already pressured in the first half and a government shutdown threatening further disruptions to its US federal pipeline, Corto believes that near-term risk is clearly to the downside.

Edition: 224

- 14 November, 2025

Consumer Discretionary

Breaking the value trap - 86Research’s report presents a focused analysis of GenAI-powered commerce, a strategic frontier they believe investors have overlooked. Market attention has remained concentrated on AliCloud’s reacceleration, while continuing to dismiss core commerce as a “value asset” trapped in macro drag. By spotlighting conversational interfaces and AI-enhanced ad tech as emerging structural advantages, 86Research sees a window of opportunity opening. A wave of initiatives has already unfolded in 2H25 and they expect Alibaba to further escalate its efforts in 2026, catalysing a period of positive news flow and re-rating potential.

Edition: 224

- 14 November, 2025

MAER Best Ideas

MAER (The Monitor of Analyst Earnings Revisions) is Mill Street’s long-standing multi-factor quantitative stock selection model and graphical tool. It uses proprietary indicators for earnings estimate revisions, price action and valuation to forecast intermediate-term relative returns for ~6500 stocks globally. With Q3 earnings reports in full swing, the latest monthly MAER updates for the Russell 1000 universe show ~60% of the universe is maintaining positive revisions trends, a relatively high proportion though off its recent peak. While Tech estimates remain quite strong, the sector has had a big move recently and the sector that stands out as a potential contrarian play is Financials, where estimates are still rising but relative returns have lagged lately, improving relative valuations. The list of highest-ranked stocks includes many Financials from multiple industries, including Morgan Stanley, BlackRock, US Bancorp and Chubb.

Edition: 224

- 14 November, 2025

Varonis: Impact of growing competition

Technology

The company’s latest stumble stems from a weakening Federal pipeline and sluggish on-prem renewals, but channel feedback points to deeper challenges from nimble DSPM rivals like Cyera and Concentric.ai to mounting pushback on costly cloud migrations that offer less functionality. With competitive share shifts and customer dissatisfaction surfacing in SPR’s 10/12 panel, it’s clear the DSPM market is heating up fast, fuelled by AI-driven data priorities and VRNS may be losing its footing. SPR’s full note unpacks which vendors are gaining ground, why end users are rethinking their data protection stack and where this market is headed next.

Edition: 224

- 14 November, 2025