Fortnightly Publication Highlighting Latest Insights From IRF Providers

Company Research

Energy

A large-cap trading at just ~11x earnings, with a ~12% FCF yield and will pay owners a 10% yield in the very near future. The Coterra deal markedly increases DVN’s stature and shale production in the Delaware Basin without incremental acquisition debt, adding ~4,600 high-return drilling locations, nearly half with sub-$40/bbl breakevens. The combined company expects $1bn+ in annual synergies and plans a $5bn buyback, materially lifting FCF/share and NAV/share. Nevertheless, investors have yet to adequately reflect DVN’s improved fundamentals in its share price, with it continuing to trade at a sharp discount to other E&P players in terms of both P/OCF and at a high required FCF yield. For each 0.5x improvement in its P/OCF multiple or a 1pp decrease in its FCF yield, DVN’s share price will rise by ~$5.

Edition: 231

- 06 March, 2026

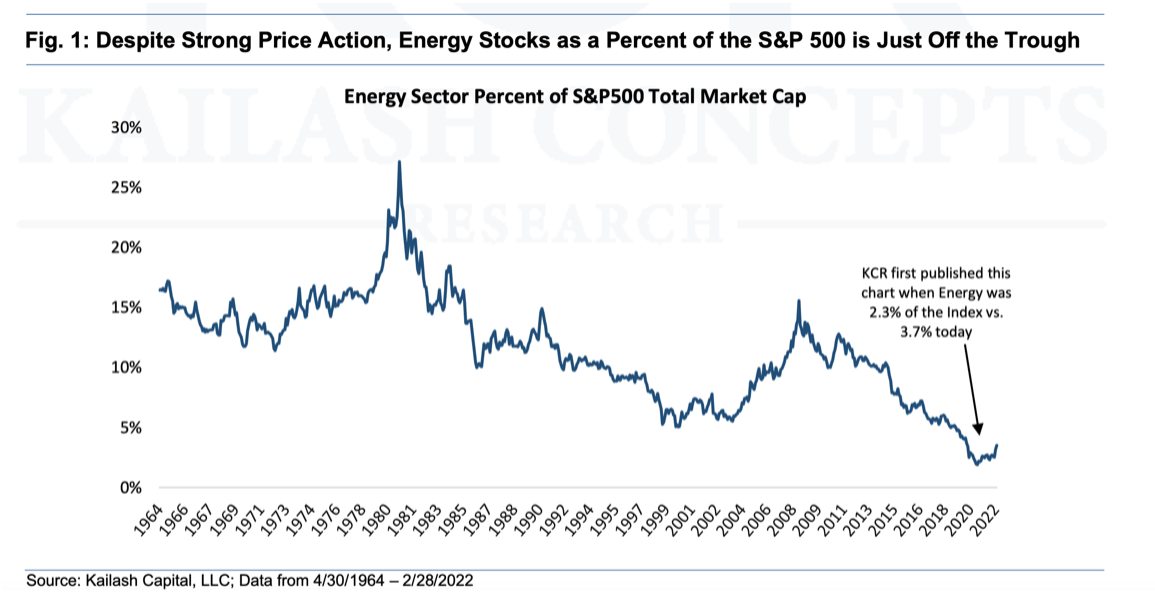

Undervalued energy stocks: The case for adding exposure

Energy stocks have even further to run. Incredibly, energy stocks continue to be the cheapest stocks in the market by a wide margin and have only been this relatively cheap once before in history. On top of this, oil & gas companies’ FCF yields are understating reality and investors are looking at the wrong companies! Recommendations include Devon Energy, Occidental Petroleum and APA Corp.

Edition: 131

- 18 March, 2022