Fortnightly Publication Highlighting Latest Insights From IRF Providers

Company Research

Academy Sports & Outdoors (ASO US) US

Consumer Discretionary

John Zolidis’ investment case is based on a positive inflection in same-store sales producing valuation expansion as investors give more credit to unit growth and the longer-term opportunity. He believes this thesis remains intact as comps improved to -1.4% in FY25 (vs. -5.1% in FY24) and have turned positive in early FY26, with Q1 likely >2%. While the recent >10% share price drop reflects macro concerns and weak transaction trends (-6.4% in Q4), John views this as partly intentional, driven by ~10% price increases and a shift towards higher-income customers. This mix shift should support higher gross profit per ticket despite lower traffic. With the shares trading at 8x P/E and 5x EV/EBITDA (FY26 estimates) and a 9% FCF yield, ASO is a “bargain”, with an eye towards the upcoming analyst day as a near-term positive catalyst.

Edition: 232

- 20 March, 2026

Nickel may yet surprise

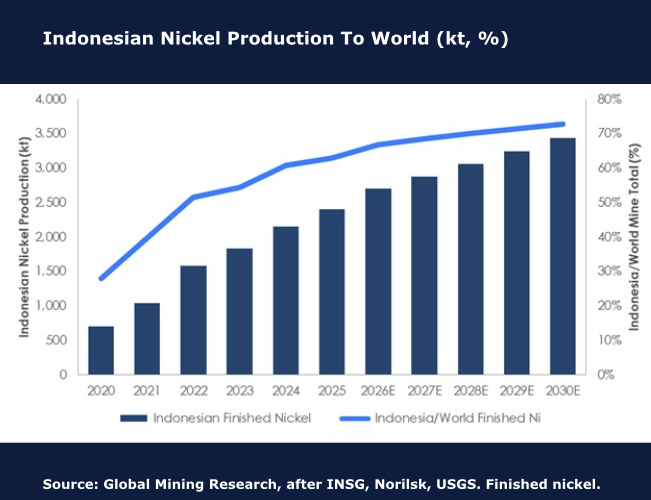

Recent events brought spot nickel up to ~US7.80/lbafterabriefreturnto US8.00/lb. The three major developments that led to this are the Iran war, a decision by the Indonesian government to dramatically cut thermal coal mining permits from 790Mt to 600Mt, and another decision to cut laterite nickel mining permits to 260-270Mt versus 2025 at 379Mt. GMR has calculated an annual nickel demand growth rate at 6.2% CAGR over the last decade, but the unceasing volumes from Indonesia (see chart) have been the issue. New changes may see parts of the global nickel cash cost curve move by ~US$1.50/lb. If laterite ore is really cut back heavily, then the price impact should add to that, but very large inventories could limit substantive price moves for some time. This is all potential; good news for producers like Vale SA, Glencore PLC or MMG Ltd. It’s too late for the Cuban producers where the lack of fuel is triggering closures.

Edition: 232

- 20 March, 2026

US: The case for 10% unemployment

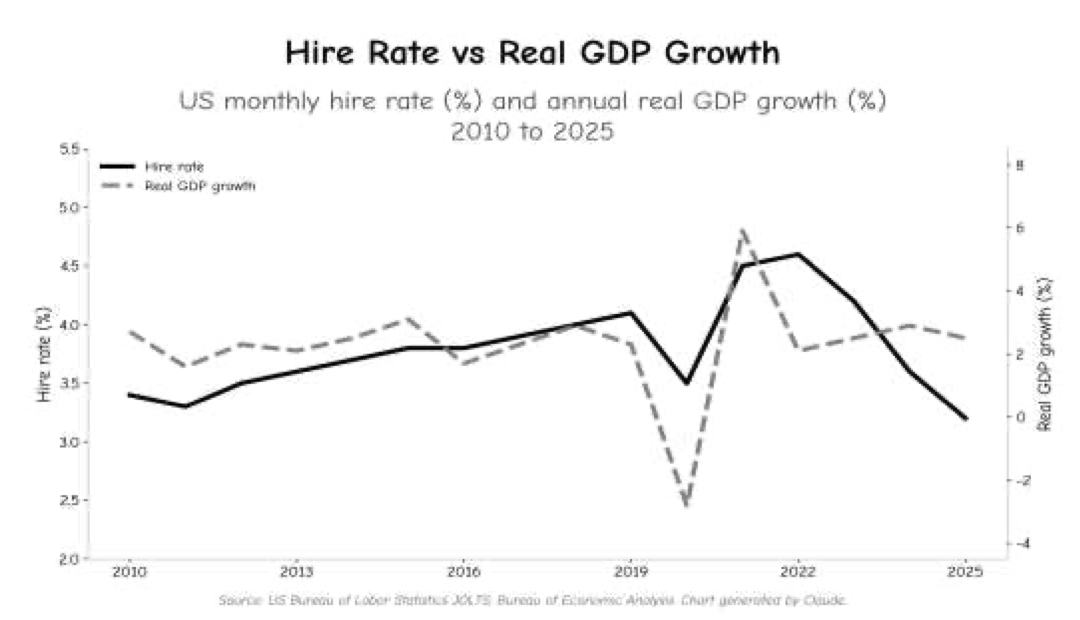

Paul Krake’s latest report rebukes the argument that AI-driven job displacement will be absorbed by new industries generating new work. It is an argument that Paul claims is taken seriously in policy circles, investment committees, and corporate boardrooms, yet it is deeply flawed. The hiring data already shows this, with the hire rate having falling 29% since the post-pandemic peak yet GDP has grown by 8% (see chart). AI is amplifying the pattern that labour is not required for growth. Just a 1 in 10 displacement of knowledge workers, which represent 45% of the US labour force, is enough to push unemployment towards 9% without a recession. Paul claims that the frameworks used to detect labour market stress are not built for an economy where growth and hiring decouple permanently. By the time the unemployment rate confirms what the hire rate has been signalling since 2022, the adjustment will have been compounding for a decade. 10% unemployment in the years ahead is not a tail risk, it is the base case.

Edition: 232

- 20 March, 2026

The Euro’s extremely important juncture

The Euro’s (€1.1416) monthly chart shows a breakout from a 17-year Down-channel, with the currency trading as high as €1.2083 in January this year, up 27% from the Sep 2022 low. Chris Roberts comments how a sustained breakout from the channel, following the 14-year, 40%+ fall in 2008-22, could potentially be very bullish. The near 6% fall from the recent high has taken the Euro back to the rising 20-month WMA and the 9-month RSI back to Neutral 50. Chris is 40% long from €1.1572 and would look to add on a break above the Jan high. His stop stays at a daily close below €1.0954.

Edition: 232

- 20 March, 2026

Space: A slow burn for investors

Industrials

Japan’s space sector remains in transition: technically ambitious, strategically important and increasingly commercial, but still fundamentally dependent on launch reliability and policy execution, with recent progress overshadowed by several high-profile setbacks. Looking ahead, Neil Newman highlights 3 developments which would signal meaningful acceleration in the sector and potentially justify thematic investment consideration: 1) improving the reliability and cadence of H3 launches; 2) continued deployment and monetisation of Earth-observation and SAR constellations; and 3) stronger government procurement as space capabilities become embedded in national infrastructure and security policy. Companies flagged in Neil’s report include Mitsubishi Heavy Industries, Mitsubishi Electric, NEC, IHI, iSpace, Astroscale, Synspective and Axelspace.

Edition: 232

- 20 March, 2026

Financials

Galliano's Financials Research

Victor Galliano upgrades the stock to Buy, arguing that the recent partial disposal of its stake in Nintendo could mark the start of a broader unwind of the bank’s large strategic equity portfolio - its primary source of potential shareholder value creation. The sale generated a ¥75.1bn gain (c.¥90bn proceeds) and reduced Kyoto’s stake from 4.2% to 3.3%, though the remaining holding still represents more than 30% of the bank’s market value. With ¥160bn in gains on stock sales, Kyoto has also been able to crystallise roughly ¥90bn of losses on government bonds, bringing its unrealised losses on the domestic government bonds still on its balance sheet close to zero. Kyoto trades at the lowest PBV among Japan’s top ten banks, while its 4.1% dividend yield also has scope to rise.

Edition: 232

- 20 March, 2026

Regulated Utilities: No place to hide - compressing equity risk premiums

Utilities

Canadian regulated utilities are up ~10% YTD, outperforming the TSX, as rising geopolitical risk has driven a flight to safety and multiple expansion across defensive sectors. The re-rating has pushed equity risk premiums to levels that are difficult to justify against the prevailing rate backdrop and Veritas believes risk-adjusted returns have become materially less compelling at current valuations and recommends underweighting the sector. Their report covers Canadian-listed regulated utilities in their coverage (Emera, Fortis, Hydro One, Canadian Utilities, ATCO). Veritas’ analysis is structured around 3 analytical pillars: 1) current sector valuations relative to a yield-implied terminal capitalisation framework; 2) the macro backdrop governing utility equity performance; and 3) the company-level funding dynamics that determine whether rate base growth translates into per-share value creation.

Edition: 232

- 20 March, 2026

Bear’s Den Idea Forum

Short-focused events consistently rank among MYST’s best-performing Idea Forums with their last one yielding a ~70% hit rate and ~8.7% average positive alpha. The dominant theme at this meeting centred on companies confronting new competition driving share loss and margin compression, while other high-level topics included businesses facing AI-related challenges; “fading” cyclical recoveries; and GLP-1-driven demand destruction. MYST felt Calix (BEAD subsidy unwind favours lower-cost solutions + forensic red flags) and TransMedics (organ transplant tech leader facing share loss amid new competition) were “unique” and worth investigating, while convincing bearish arguments were also presented on A O Smith, Dollar General, Old Dominion Freight Line and Uber.

Edition: 232

- 20 March, 2026

Allegro (ALE PW) Poland

Consumer Discretionary

the IDEA! remains constructive on the stock following FY25 results, highlighting strong ecosystem monetisation, robust cash generation and disciplined capital returns as key pillars of the investment case. The Polish marketplace continues to fund international expansion while sustaining attractive incremental margins, with ~63% drop-through. Management reiterated its leverage framework centred around ~1x net debt/EBITDA and announced a further PLN 1.6bn FY26 buyback, which the IDEA! sees as offering downside support. However, they caution that management may be underestimating the competitive trajectory of Chinese cross-border platforms such as Temu and Shein. While EU parcel duties from July could slow growth, the competitive threat is unlikely to disappear and could pressure domestic GMV growth over time.

Edition: 232

- 20 March, 2026

Buy the dip on China tech

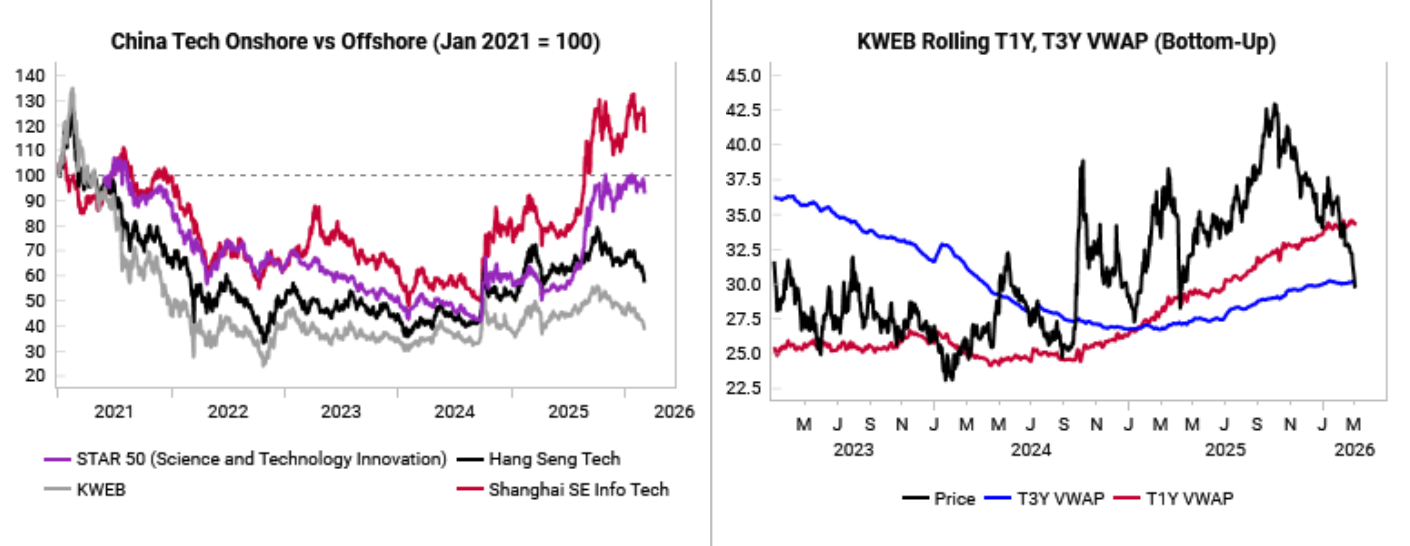

Offshore Chinese tech equities have materially lagged onshore equities over the past 6 months, suffering big drawdowns even as onshore equities make new highs. The KWEB China Tech ETF has now fallen down major support levels at the T3Y VWAP (see charts). The Variant Perception team are starting to see more LPPL crash exhaustions signals for Chinese tech stocks, while their fast money speculative flow proxy shows that they are approaching contrarian buy levels for KWEB. MSCI China is now underperforming the MSCI EM index by a wide margin, with the trailing 1-year relative performance below -2 standard deviations. Despite this, Chinese small caps have been outperforming large caps, a positive divergence that bodes well for future Chinese equity returns. There is a chance the Iran situation will worsen, and Chinese assets will be further caught up in the energy shock, but there is already a decent amount of dislocation priced into Chinese tech equities. Ultimately, this is an attractive entry point for investors.

Edition: 231

- 06 March, 2026

Brazil: Stagnation ahead

In the fourth quarter of 2025 Brazil’s GDP rose 0.1% QoQ s.a., broadly in line with the market median (0.1%) and BuySideBrazil’s projection (0.0%). Compared to 4Q/2024, GDP increased 1.8%. In Q4/2025 Brazil’s economic growth relative to 3Q/2025 was mainly driven by stronger exports and services. Services, slightly above expectations, posted a positive performance in the quarter, supported by higher consumer income amid a still-robust labour market. However, Andrea Damico says this momentum already shows signs of exhaustion, with a potential turning point in H1/2026. The key highlight is the sharp slowdown in domestic demand, with the weakest marginal performance in domestic absorption and private consumption since the end of the pandemic in 2021. The clearest sign of this fragility was the sharp decline in imports. Overall, this data reinforces Andrea’s view of cooling economic activity and stagnation in the first half of 2026. BSB’s projection for 1Q/2026 is 1.1% QoQ s.a.

Edition: 231

- 06 March, 2026

G-III Apparel Group (GIII US), VF Corp (VFC US), Dillard's (DDS US) US

Consumer Discretionary

Hedgeye provides updates on 3 of their top Retail shorts. For GIII, they expect the next guide for the year to be an absolute disaster; forecasting a 20%+ cash flow hit from the the loss of major Calvin Klein and Tommy Hilfiger licenses back to PVH, while prior channel stuffing and tougher retail conditions could force the company to increase markdown support to key partners. Meanwhile, VFC is caught between a heavy debt burden and weakening brand momentum; Hedgeye believes a massively dilutive equity raise will ultimately be required. And finally, DDS remains a mispriced security, trading at ~12x EBITDA despite a sharply decelerating model and the company overearning by 800-1,000bp. That suggests that the real earnings power is between $10-20 per share. 5x earnings, is an appropriate department store multiple, suggesting 80-90% downside.

Edition: 231

- 06 March, 2026

Online travel & AI

Consumer Discretionary

Gordon Haskett Research Advisors

Robert Mollins examines how OTAs are adapting to a rapidly changing environment driven by rising AI adoption. He focuses on 4 key themes: 1) AI as an emerging traffic channel; 2) structural advantages limiting disintermediation risk; 3) consumer-facing AI development across travel platforms; and 4) internal AI initiatives driving monetisation and cost-saving opportunities. AI companies have rapidly integrated tools into their assistants, raising concern over the technology’s ability to replicate functionality and reduce dependency on established platforms. Investor concern has extended beyond software into sectors with significant digital exposure, including online travel. While Robert acknowledges these risks, he believes AI assistants are more likely to evolve into a paid traffic channel rather than a vertically integrated travel marketplace capable of displacing Booking, Expedia and Airbnb.

Edition: 231

- 06 March, 2026

China: Channel checks on leading coffee & tea brands

Consumer Discretionary

The competitive environment across the country's leading beverage chains appears to be shifting from aggressive subsidy-led share grabs towards more rational pricing and product-led differentiation. For global investors, this suggests: 1) margin recovery potential after a prolonged discount cycle; 2) strengthened positioning for category leaders with innovation capabilities; and 3) continued consolidation towards scaled operators with diversified product offerings. Luckin’s near-term fundamentals look resilient with Jan SSSG likely >10% and pricing/ASP recovering sequentially. Mixue was modestly softer due to the CNY timing shift, while Guming was a clear relative winner among tea chains with SSSG/GMV +10-15% (still HSD even ex delivery fees) and momentum likely improved further in Feb on holiday & platform campaign effects.

Edition: 231

- 06 March, 2026

Industrials

With a market cap of $3.6bn, Nichias is an industrial insulation company that Asymmetric has followed for over 20 years. While the shares have outperformed the TOPIX over the long term, the performance gap has widened materially in recent periods, a trend Asymmetric believes can continue, highlighting the group’s: 1) cash-rich balance sheet and strong FCF, supporting rising shareholder returns; 2) ability to raise margins across its business segments; 3) exposure to maintenance work related to nuclear restarts in Japan; and 4) earnings gearing to the slower than initially expected SPE cyclical pick up.

Edition: 231

- 06 March, 2026

Applied Optoelectronics (AAOI US) US

Technology

Rosenblatt reiterates their Buy rating and Top Pick status on AAOI. The company invested $209m in capex in 2026 with a focus on increasing laser and transceiver capacity in Texas. This ongoing investment is poised to drive a tripling of Data Centre revenues in 2026 and even faster growth in 2027. Amazon and Oracle 800G demand are the primary revenue drivers in 2026 along with Microsoft's solid 100G and recently renewed 400G demand. By 2027, all these customers should also be buying 1.6T. Rosenblatt’s 2026 revenues/EPS estimates increase to $1.02bn/$1.18. For 2027 their respective figures are $3.3bn/$6.25. Their new TP of $125 is based on 20x CY27 EPS forecast - a conservative multiple to account for execution risk.

Edition: 231

- 06 March, 2026

AI driven 10Q / 10K text analysis

Since there are always reasons when companies change the wording in their financial filings, being alerted to these changes allows investors to realise potential risk factors and opportunities before they are reflected in the market. Recent alerts include: 1) AvalonBay Communities - bylaws last amended in Oct 23; is the added wording to its 2025 10K, prompted by takeover interest? 2) Diamondback Energy - loss of customers; Endeavor equityholders planning on selling shares? 3) GoDaddy - Microsoft partnership in trouble? 4) Align - more benign competitive environment. Caution on OSOs, DSOs and other large group practices. 5) Armstrong World Industries - better demand expectations. 6) Cigna - clients terminating / modifying contract terms?

Edition: 231

- 06 March, 2026

Not made in India

According to Jonathan Anderson, India has little chance of catapulting itself into middle-income levels without seriously raising its game on exports, in particular light manufacturing exports which would maximise employment, income and dollar earnings gains. Jonathan points out that there are no examples of sustained rapid services-led growth in any but the smallest emerging market economies – and certainly not in a case like India with a population of 1.4 billion. In practice, the only proven model that leverages on underlying comparative advantage for the populous low-income world is labour-intensive manufacturing. And until India jumps on the bandwagon, it will not be a breakout. This doesn't stop Jonathan from investing in India's domestic growth cycle on a cyclical basis, but it does very much inform how he sees the country's structural prospects.

Edition: 230

- 20 February, 2026

The best FX trade for 2026

In Stephen Jen’s view, USDJPY may be the best (i.e., with the highest Sharpe ratio) FX trade for 2026. With the dominant election victory, Stephen points out that the LDP has enough popular support for PM Takaichi to go through with her 3%-GDP worth of fiscal stimulus. With inflation still above the BOJ’s target (headline CPI is down to 2.1%, but core-core is still hovering around 3.0%), this prospective fiscal stimulus will likely be met with accelerated or earlier rate hikes by the BOJ. Stephen says that the US Fed and the BOJ will continue to converge in 2026, with the former cutting while the latter is hiking. Stephen argues that the US dollar itself is in a structural descent, and the particular policy mix in Japan should lead to a stronger JPY. He still views 125 as a very reasonable target for USDJPY this year.

Edition: 230

- 20 February, 2026

Consumer Staples

OWS reiterates their short on COCO following 4Q25 results, arguing the print reinforces their original thesis that the company’s perceived supply chain “moat” is overstated. Management disclosed ongoing US market share losses and flagged heavier promotions, distributor incentives and stepped-up SG&A to defend growth. Private label competition is intensifying, pricing benefits are set to fade through FY26 and inventory has surged to 106 days, increasing the risk of further discounting. Meanwhile, ~96% of revenue still comes from coconut water, underscoring limited platform diversification. With insiders adopting new 10b5-1 selling plans and shares still trading at ~3.9x FY26 sales, OWS sees meaningful downside with a TP of $31 (35% downside).

Edition: 230

- 20 February, 2026

Insider buying in beaten-down Tech stocks

Technology

Smart Insider flags a number of insider buys at Hexagon, Sage and ATOSS following recent share price weakness, ranking all 3 stocks +1 (highest rating). At HEXA, the new CEO, Chief Strategy Officer and Vice Chair made their first purchases, buying a combined €3.4m of stock, shortly after results and the announced spin-off of Octave Intelligence. At SGE, 2 long-serving non-execs bought stock, including one director tripling his holding in a rare purchase and at a higher price than his last buy 5 years ago. At AOF, the CEO invested €11.6m (adding 4% to his stake) and the long-tenured CFO made his first-ever purchase - a notable shift from a series of smaller sales.

Edition: 230

- 20 February, 2026

Vinci (DG FP) France

Industrials

Robert Crimes updates its long-term forecasts for the stock and increases his TP to €192 (40% upside). The company boasts a high-quality mix of French autoroutes, international airport concessions, while Energies benefits from global megatrends driven by energy transition and digital transformation. In 2026-30E, Robert estimates DG will generate >€30bn of cumulative FCF pre-dividends. He assumes ~€20bn is returned to shareholders including €17bn of dividends, supporting a DPS CAGR of +10% over the period, plus €3bn of net share buybacks, while still leaving c.€8bn of additional capital available for debt reduction (yet Group ND/EBITDA is already low at 1.3x in 2026E), long-duration acquisitions (most likely airports) to increase the company's weighted average Concession duration or enhanced shareholder distributions.

Edition: 230

- 20 February, 2026

Aditya Vision (AVL IN), Brainbees (FIRSTCRY IN), Bluestone Jewellery (BLUESTONE IN) India

Consumer Discretionary

Iii conducted channel checks across the 3 companies to assess demand, competition and store economics. Footfall is flat to modestly down, growth is increasingly promotion- or online-led and store-level productivity appears constrained - pointing to normalisation rather than reacceleration in discretionary demand. On FirstCry, consensus expects multichannel growth to reaccelerate to mid-to-high teens via RocketBees and FC Quick, however, Iii believes execution delays and intense competition will keep growth in low single digits. For Bluestone, the Street assumes Q3’s operating leverage and ~12% pre-IndAS EBITDA margin are sustainable, but Iii expects margins to deteriorate within 1-3 quarters as seasonally weaker revenues expose a high fixed-cost base. At AVL, incremental store expansion appears supported by discounting and channel inventory build rather than productivity-led leverage.

Edition: 230

- 20 February, 2026

Technology

Contrary to Street expectations, JNK supply chain research indicates AMBA's near-term strength masks structural headwinds. Book-to-bill remains above 1.0x, channel inventory is lean and pricing is stable. However, the underlying trajectory is weaker: FY27 revenue is tracking roughly flat Y/Y, reflecting rising customer and geographic concentration risk. Two customers account for more than one-third of China revenue, while Qualcomm design activity is increasing across AMBA accounts. In addition, Samsung remains AMBA's only foundry partner for leading-edge 3nm and 5nm nodes; whereas competitors source from multiple fabs. Limited consumer exposure further constrains diversification. Recent order strength does not mitigate the single-foundry dependency or competitive encroachment now visible in JNK's tracker data.

Edition: 230

- 20 February, 2026

Apollo: Data that changes the game

Libra’s flagship platform enables investors to observe, rank and act on fundamental market shifts across stocks, sectors and themes. Apollo highlights re-ratings, de-ratings and forecast changes - supporting timely, data-driven decision-making. Access to Apollo data allows investors to map changes in valuation, identify entry points and exit points, and the evolution of the (dynamic) investment cycle in real time. This ability to detect inflection points as they develop provided early evidence to build and maintain exposure to gold stocks while avoiding the subsequent de-rating in LVMH.

Edition: 230

- 20 February, 2026

Delivering alpha in 2025; positioning for 2026

Healthcare

In 2025, Bios published 12 short ideas and 2 longs, delivering a 78% absolute hit rate, with 7 of 14 positions closed intra-year. Notable winners included Anavex Life Sciences (~77% absolute return to short sellers), Butterfly Network (~49%) and Arcellx (~30%), while 89bio returned ~115% on the long side. Looking ahead, top short ideas for 2026 include a ~$40bn medtech facing reimbursement pressure, new competition and GLP-1 headwinds; a ~$20bn biotech exposed to excessive hype, competitive threats and clinical trial failure; and a ~$10bn commercial pharma/biotech likely to see material y/y sales declines and poor regulatory environment. On the long side, Bios highlights a $1.5bn development biotech with strong data and potential for FDA approval in 2H26 and a ~$600m biotech with multiple assets in development and 3+ years of cash, where material licensing / M&A potential exists.

Edition: 230

- 20 February, 2026

Accounting red flags emerge across multiple names

SMCI moves to Forensic Alpha's maximum ‘10’ risk rating after its 10Q revealed extreme working-capital swings: receivables surged from $2.5bn to $11bn in one quarter, heavily concentrated in a single customer, while payables ballooned to $13.8bn, masking weak cash conversion. Bloom Energy also remains a top concern, with a widening gap between adjusted and statutory earnings, rising contract assets and growing reliance on off-balance-sheet JVs. NiSource’s score rose on higher DSO and advances to unconsolidated VIEs, while Cummins saw a jump in sales to equity investees to $1.70bn, with receivables outstanding from these investees of $523m, suggesting extended credit terms. Other stocks flagged last week include Amentum, Atlassian, Becton Dickinson, Ford and Impinj.

Edition: 230

- 20 February, 2026

DSV (DSV DC) Denmark

Industrials

Following publication of its FY25 annual report, Iron Blue increases their DSV score by 4 points to 33/60 (top decile and fertile grounds for shorting), reflecting 1) more cost strip outs; 2) increased use of provisions accounting; 3) Schenker acquisition accounting (principally around general and bad debtor provisions fair value adjustments and possible future PPE sale & leasebacks); 4) increased pension deficit (including when adjusting for a high liabilities discount rate); 5) another doubling of whistleblower cases and deteriorated health & safety performance & target; and 6) a rise in the rate of employee unionisation to 41% from 30%.

Edition: 230

- 20 February, 2026

Ethiopia: Rising risk of full-scale conflict

According to Hugo Brennan, a resumption of full-scale armed conflict between government troops and Tigrayan forces is becoming increasingly plausible. The region is heavily militarised, tensions between federal and regional groups have been brewing for a while and now look at risk of boiling over. This matters to sovereign investors because a resumption of armed conflict in Tigray would pose both political and economic challenges for the government as well as potentially triggering another humanitarian crisis. Federal elections scheduled for June would be at risk of postponement, while ongoing efforts to restructure the country’s debt would likely be derailed. In addition, Ethiopia’s restructuring of its sole USD$1 billion Eurobond, one of the last outstanding under the G20 Common Framework, is at risk of tipping into litigation amid a disagreement over the terms between the bondholders and official bilateral creditors (led by France and China).

Edition: 229

- 06 February, 2026

Dow (DOW US) US

Materials

Forensic Alpha raises their risk score sharply after Dow’s 10-K highlights balance-sheet concerns tied to the Sadara JV with Aramco. Their report highlights a $901m negative investment balance linked to sustained losses at Sadara, reflecting Dow’s exposure through guarantees on ~$1.3bn of debt and a $500m revolving credit facility. Despite these losses, Dow’s net debt has risen only modestly and no new loans to Sadara have been disclosed. Forensic Alpha suggests the company has instead supported Sadara via favourable working capital movements, helping explain weak OCF over the past two years. Notably, 10-K language now indicates performance under guarantees is “no longer remote” ahead of Sadara’s 2026 refinancing. With negative FCF, restructuring costs and rising minority cash leakage, investors should question dividend sustainability and the growing gap between EBITDA and true cash flow.

Edition: 229

- 06 February, 2026

An early, data-driven read on MedTech trends

Healthcare

Medmine analyses purchase order data from 3,500+ US healthcare providers, providing investors with an early, differentiated read on demand and revenue drivers. Last year, they captured several trends including tariff impact & pricing resilience, supply chain disruptions, Pulsed Field Ablation (PFA) adoption in EP labs, TAVR market resurgence and a robotics supercycle. Crucially, Medmine’s models provide a more accurate read on company performance than comparable market estimates. They averaged a 1.5% error rate, compared to 4.1% for consensus through the first three quarters of 2025. Additionally, their models tracked within 1% of reported actuals in 68% of cases, while consensus estimates met that threshold in only 13% of instances. Their Q4 models, incorporating Dec data, are now available. Contact us below for further information.

Edition: 229

- 06 February, 2026

Consumer Discretionary

Brian McGough thinks the market is materially overestimating the company’s long-term earnings power. Investors are buying into BOOT’s ambition to expand from ~515 stores to 1,200, but Hedgeye’s M.A.P.S. (Market Area Performance Study) analysis suggests the company has already exhausted its most profitable “power alley” stores tied to mining, agriculture and construction - locations with a healthy 70/30 workwear-to-fashion mix. Incremental growth is now shifting to more expensive, fashion-heavy stores that rely on a Western Wear trend that Brian believes is in the late innings. In aggregate, he estimates BOOT needs ~7% comps just to leverage occupancy (the highest hurdle in retail), while many new stores carry rent escalators exceeding 10%. Brian sees sustainable EPS closer to ~$4 vs. consensus TAIL expectations >$8, implying up to ~75% downside.

Edition: 229

- 06 February, 2026

Randstad (RAND NA) Netherlands

Industrials

RAND offers an attractive risk-reward anchored by a “virtually guaranteed” dividend yield of 5.6%, providing support for the share price. The company’s FY25 FCF is more than sufficient to pay shareholders the conditional ordinary cash floor dividend of EUR 1.62 per share and is highly likely to be repeated thereafter. Beyond income, the IDEA! sees scope for a share price recovery as staffing markets across the company’s key geographies appears to have bottomed. The US market is improving, France may be nearing a trough and conditions in the Netherlands have stabilised. Trading on undemanding multiples (EV/EBITDA ~7.9x), RAND is preferred over Adecco and ManpowerGroup due to its superior FCF generation and sustainable capital returns.

Edition: 229

- 06 February, 2026

Materials

Asymmetric highlights Daido Steel as an under-followed stock that is increasingly coming into its own. The stock has surged ~85% since they turned bullish in Jun 25, helped by a strong H1, driven by rare earth free magnet demand amid tighter Chinese export controls and robust marine valve orders. Even after the rally, Daido only trades at 0.86x PBR and ~13x FY3/27E earnings (+20% Y/Y), with relatively low foreign ownership. Looking ahead, Asymmetric flags multiple profit catalysts: potential synergies from acquiring Kobe Steel’s Koshuha specialty furnace, an improving semiconductor cycle, rising demand for rare earth-free magnets for HEVs, and expanding exposure to engine shafts and components across aerospace, energy, shipping and gas turbines - supporting margin and earnings upside over the next 1-2 years.

Edition: 228

- 23 January, 2026

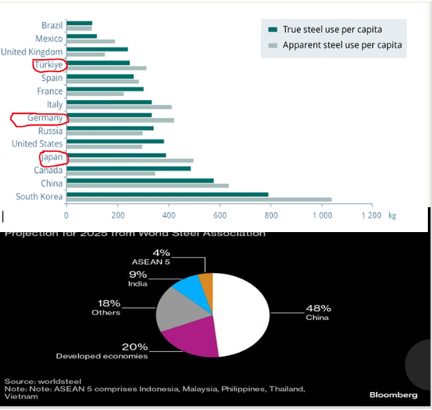

Iron ore: China’s urbanisation supercycle is over

James Burdass notes that China’s National Bureau of Statistics has reported a production of 960.81 million tonnes of steel last year, 4.4% less than in 2024. This may not appear significant, but is in fact an important data point that every commodities investor needs to be aware of. In his presentation a year ago "The New World Order and Commodities", James showed just how far China's apparent steel use per capita could fall. He suggested at the time a fall of at least 200 million tonnes from the peak – the trend is definitely on the way towards that. Falling materially below 1 billion tonnes for the first time since 2018 is the official obituary for the "Urbanisation Supercycle." It signals to every Iron Ore investor (Rio Tinto, BHP, Vale) that the volume cap is in place. This has the potential to be a headwind for the global steel sector for years to come.

Edition: 228

- 23 January, 2026

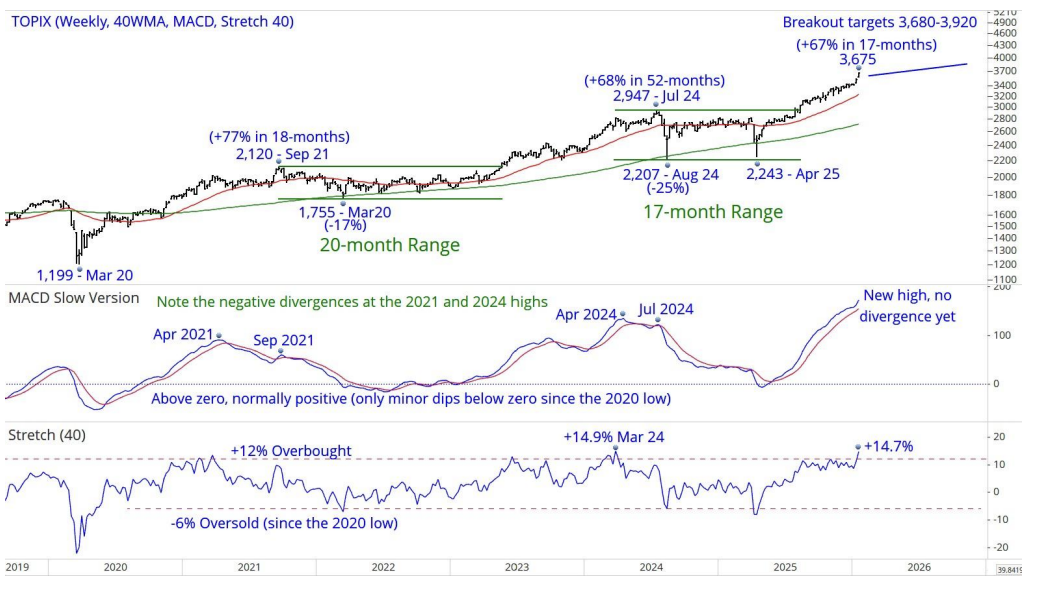

Big in Japan

The Topix’s (3,659) breakout from the 2,207-2,947, 17-month range targets an advance to 3,680-3,920. Last week’s new ATH of 3,675, essentially puts the index into the target zone. The break above the 1,700-1,825, 28-year ceiling in 2021, targeted a minimum of 3,400-3,650+, now marginally exceeded. The prior behaviour of the MACD indicator (peaking before price) leads Chris Roberts to expect further net gains before a large correction, as seen in 2021-22 and 2024, occurs. He is 65% long from 2,925. Sell 5% at 3,658, 5% at 3,678 and 5% at 3,698 to take partial profits. The stop for all longs moves up to a daily close below 3,194 from 2,780.

Edition: 228

- 23 January, 2026

Barito Pacific (BRPT IJ) Indonesia

Materials

Prajogo Pangestu (Chairman since Jan 1993) bought 3m shares at IDR 2,830 per share, spending US$502,000. This is 3x the price of his last purchase 11 months ago. While small relative to his 71% ownership of the company, the purchase is in line with his prior purchases. He has also been timely on most of those prior purchases with an 18% average 6-month return. This is an interesting purchase as the stock has fallen from an all-time high in October. Smart Insider are ranking the stock +1 (highest rating).

Edition: 228

- 23 January, 2026

Earnings season screens

Mill Street has developed an "Earnings Screen Score" ranking methodology that draws on selected inputs from their MAER (Monitor of Analysts’ Earnings Revisions) stock database to identify companies which have strong near-term fundamental momentum going into an earnings report. Mill Street’s research indicates that companies scoring highly in their ranking have a much higher chance of near-term improvements in analyst expectations than those that score poorly. Stocks most likely to produce positive near-term analyst estimate activity in the next couple of weeks include Lam Research, Regeneron Pharmaceuticals and Teradyne. Bottom ranked stocks include LyondellBasell, Eaton and Marathon Petroleum. Click here to access the full report.

Edition: 228

- 23 January, 2026

Quantum Computing (QUBT US) US

Technology

QUBT has legitimate quantum assets across photonics, compute, security and sensing, alongside burgeoning thin-film lithium niobate (TFLN) fabs that could supply both internal and industry demand for integrated quantum photonics, nonlinear optics and optical waveguides. The company is also acquiring fabs (LSI) from Luminar for <5x revenue, improving P&L optics and diversifying into another key laser market. With $1.6bn of cash and no debt, QUBT’s interest income currently exceeds operating expenses. Rosenblatt likes the risk-reward, citing exposure to quantum computing, fab-driven product integration, customer acquisition in fast-growing optical communications, optionality around photonic gate-based quantum computing and the potential to embed quantum security into consumer edge devices. They initiate coverage with a Buy rating and TP of $22 (80% upside).

Edition: 228

- 23 January, 2026

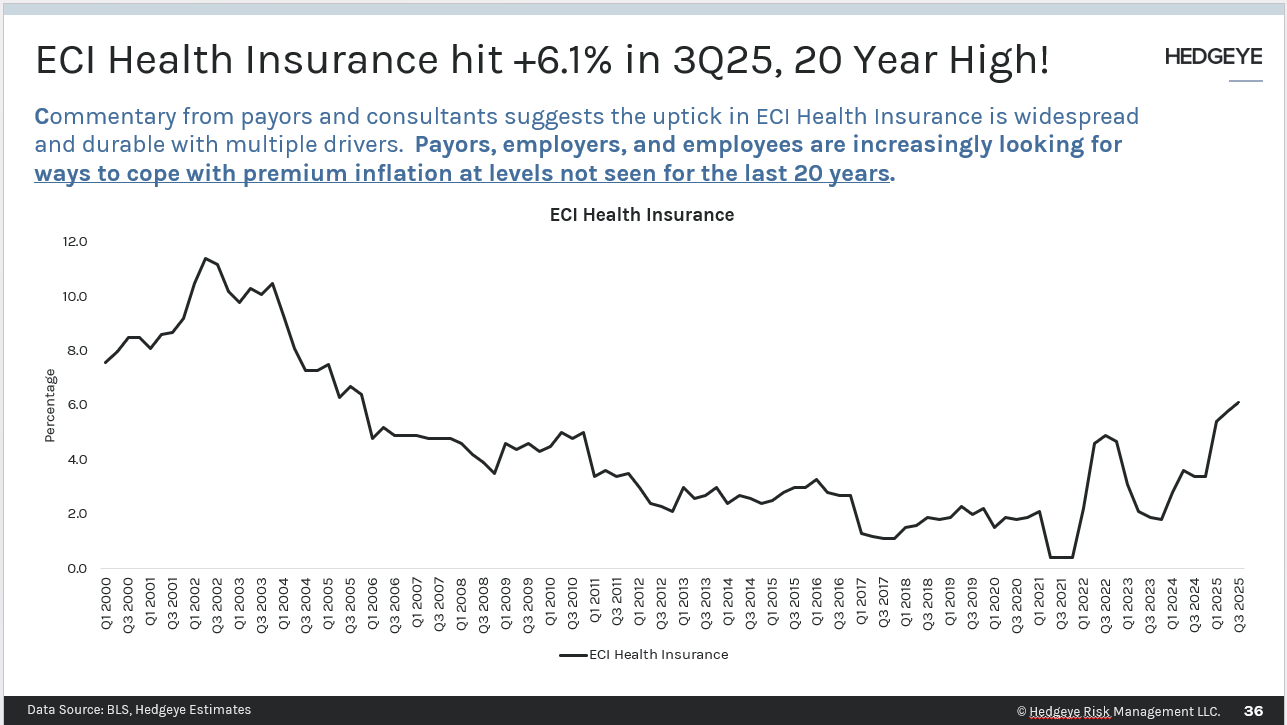

Healthcare

2025 mirage sets up 2026 disaster - slowing volume trends, accelerating labour costs and mounting policy headwinds are converging into a “perfect storm”. While 4Q25 may appear resilient due to pull-forward utilisation ahead of Jan 1st plan resets, Hedgeye expects brutal comps in 1Q26. They contend that Medicaid supplemental payments and unusually low uninsured volumes (due to immigration enforcement) flattered 2025 margins - tailwinds that are likely to reverse in 2026. With employer premium inflation at a 20-year high (+6.1% in Q3), insured lives are set to shrink just as labour costs accelerate amid unsustainably low SG&A ratios, driving significant margin pressure. Additional policy headwinds under the Trump Administration are working to shrink the population of insured medical consumers, amplifying the pressure already seen.

Edition: 228

- 23 January, 2026

Glencore & Rio Tinto: Easy to buy, not easy to integrate

Materials

GMR is sceptical on a potential tie-up between RIO and GLEN, citing material integration and execution risks. They highlight stark contrasts in management culture and business models, alongside challenges around thermal coal exposure, sovereign risk tolerance and regulatory scrutiny given combined copper output. Assuming US$1.5bn of annual synergies, GMR estimates RIO could bid up to £5.40 per GLEN share for the merger to be, on average, neutral on Earnings/share and NCFO/share out to 2028. Following GLEN’s recent rally, GMR downgrades the stock to Hold and moves RIO to Sell on deal risk. Their proprietary Acquisition Rationale score reinforces caution: GlenRio scores just 9/18, a level that historically underperforms peers over the next 24 months.

Edition: 228

- 23 January, 2026

Gold/Silver: No longer just a commodity

James Burdass reminds us that 2025 was the year when the gold stealth bull market turned into a mega bull market for precious metals (as his regular readers will know, this was a key call for Commodity Intelligence). Silver has seen one of the most pronounced catch up trades in its history. The 2020-2024 ratio was in the abnormal zone (80-120/1), which assisted us to make that call. At 56, the silver/gold ratio is now just below the 30-year average of about 65. James says that gold and silver have transitioned from being just a commodity to visible allocations by central banks, funds and other investors. He still thinks there is scope for more generalists to replace their exposure to US Treasuries with an allocation to precious metals, as fiscal dominance sets in.

Edition: 227

- 09 January, 2026

Brazil: The effects of fiscal impulse

Buysidebrazil’s latest report examines the effects of fiscal impulses on the investment decisions and capital structure of Brazilian companies listed on B3. They find that an expansionary fiscal shock of 1% of GDP is associated with: (i) a reduction of up to 4.14% in the investment rate after one quarter; (ii) a decline of up to 2.77% in leverage after six quarters; and (iii) an increase of up to 4.73% in cash liquidity after three quarters. This behaviour signals bad news for productivity and long-term development, since persistent private investment retraction compromises capital accumulation and the incorporation of new technologies, reinforcing the productive stagnation that has characterized the Brazilian economy in recent decades. As for the year ahead, the team project the exchange rate at BRL 5.50/USD, expect continued disinflation and further deceleration in economic activity, and the beginning of a monetary easing cycle.

Edition: 227

- 09 January, 2026

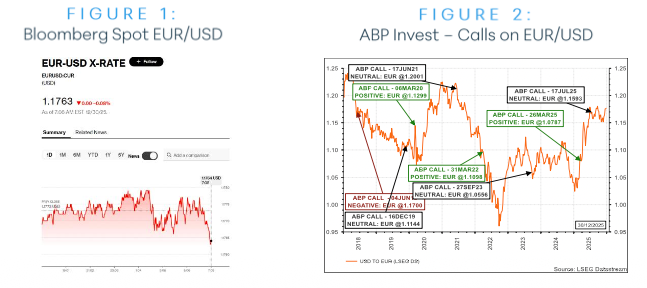

Upgrading EUR/USD to positive

ABP Invest recently upgraded EUR to positive against the USD. This goes against their intuition that the USD could be a stronger currency in 2026 on either a stronger-than-expected US economy or a deteriorating US economy that triggers the safe-haven characteristics of the greenback. However, given the second consecutive month of an improving overall score differential between the currencies, the team felt the decision-making process should not be impacted by their qualitative expectations. In March 2025 they turned positive EUR/USD at 1.0787, given their concerns on US developments driven by Trump and the surprising pick up in underlying European economic data - the decision turned out to be quite timely. Should the recent slower economic patch in the US continue and the long-awaited fiscal push take place in Europe, alongside positive momentum from Russia/Ukraine developments, there could be further upside.

Edition: 227

- 09 January, 2026

Roaring productivity vs the AI bubble

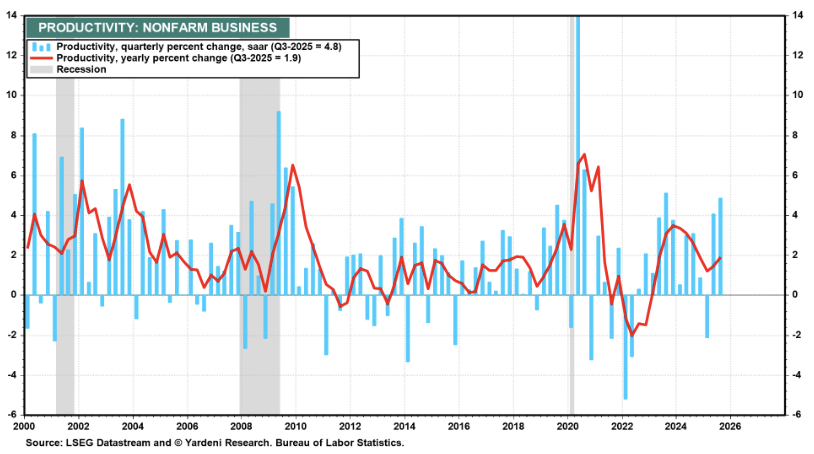

The latest Bloomberg Businessweek had the AI bubble as the cover story. Some may take this as a sign to be nervous, but from a contrarian perspective Ed Yardeni argues that it’s bullish as it signals the bubble won’t burst, if it even exists. People have AI fatigue. Ed recently recommended underweighting the Mag-7 as their AI arms race is forcing them to spend billions on infrastructure that could quickly become obsolete, and that could be unprofitable as competitors squeeze their margins. Ed believes the air can be let out of the AI capital-spending bubble over time without it bursting and causing a recession. Meanwhile, AI is starting to boost the productivity of the users of this tech, especially the S&P 500’s Impressive 493. Non-farm business sector labour productivity increased 4.9% (saar) in Q3-2025, as output increased 5.4% and hours worked increased 0.5% (see chart). Q2-2025 productivity was revised up from 3.3% to 4.1%. These are striking numbers!

Edition: 227

- 09 January, 2026

2025 winners & surprises; top themes & names for 2026

Technology

Last year, SPR's field-driven insights helped identify meaningful momentum in names such as Ciena, Snowflake, MongoDB, CrowdStrike and Datadog, while also flagging emerging headwinds in areas like UC/CC, vulnerability management and parts of storage. Looking ahead to 2026, their focus sharpens on where AI moves from hype to measurable ROI, how infrastructure refresh cycles finally materialise and where platform consolidation reshapes security, data and software delivery. From AI agents and identity as the new control plane to broadband acceleration and go-to-market disruption, SPR sees multiple inflection points ahead and meaningful opportunities for those tracking real-world signal over noise. Click here to access their report.

Edition: 227

- 09 January, 2026

Retail predictions for the year ahead

Consumer

Gordon Haskett Research Advisors

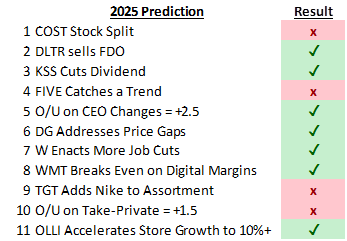

Looking back at GHRA’s 2025 Top 10 (+1) predictions, their batting average was good, hitting on 7 of 11 (see above). For the year ahead, their forecasts include: 1) Target announces an investment cycle on Mar 3rd with adjusted FY26 EBIT margin in the ~3.0%-4.0% range and a 2030 view of ~5.0%-6.0%. 2) Five Below launches Digital Loyalty Card. 3) Academy Sports adds another big brand…likely HOKA. 4) Costco unveils a special dividend and/or ramps share buybacks. 5) Ollie's embarks on large scale sales productivity effort. 6) Burlington takes a page (or two) out of the Ross Stores marketing playbook. 7) Someone gets acquired; BJ’s and Arhaus the most likely candidates. 8) Home improvement recovery gets pushed out…again.

Edition: 227

- 09 January, 2026

Turning 2025’s performance dispersion into alpha

Trendrating highlights that last year’s exceptionally wide performance dispersion created a powerful backdrop for active investors able to systematically capture winners and sidestep losers. Their US Large and Mega Cap model demonstrated how timely, rules-based trend signals helped clients meaningfully improve outcomes - increasing exposure to stocks in sustained uptrends while cutting risk in deteriorating names, as evidenced by their Winners & Losers track record. With 300+ institutional users, the firm positions trend capture as a repeatable source of alpha and risk control. The same disciplined approach is applied globally, with their Developed EU and Asia-Pacific models showing similarly strong performances.

Edition: 227

- 09 January, 2026

Ahold Delhaize (AD NA) Netherlands

Consumer Staples

Iron Blue initiates coverage on Ahold with a score of 26/60, which is top quartile and fertile grounds for shorting. They highlight FY24’s spike higher in balance sheet vendor allowance receivables, with days outstanding hitting a 10-year high. The €147m Y/Y rise was the highest in 8 years and equated to 5% of FY24 PBT adj, or 0.2% EBITA margin. Ahold has consistently stripped out of earnings one-off restructuring charges and asset impairment expenses. FY24 earnings also saw a Y/Y benefit from lower inventories write downs. They also flag €2bn of additional debt not included in Ahold’s headline net debt calculation, including €1.3bn reverse factoring.

Edition: 227

- 09 January, 2026

Italy: Industrial Devolution

Italy’s industrial production undershot expectations in October, with production falling 1.0% month-on-month, a sharper contraction than the expected 0.3% decline. The pullback was broad-based across key categories: consumer goods output dropped 1.8%, capital goods declined 1.0% and intermediate goods slipped 0.3%. Energy production provided only a modest offset, rising 0.7%. On an annual basis, industrial output fell 0.3%. John Fagan points out that the year-on-year breakdown highlighted persistent structural weaknesses, with significant declines in chemical manufacturing (-6.6%), textiles and apparel (-5.0%), and refined petroleum products (-4.6%). The data reinforce the fragile momentum across Italy’s industrial base, which continues to face a combination of soft external demand, elevated input costs, and sector-specific pressures in chemicals and textiles. The sharp monthly swing also signals that September’s strength was not sustained, raising concerns about the durability of Italy’s manufacturing recovery.

Edition: 226

- 12 December, 2025