Fortnightly Publication Highlighting Latest Insights From IRF Providers

Company Research

Technology

A broken IPO trading ~60% below its $25 listing price, with potential to double over the next year and deliver a 3x return over 4 years. Recent share price weakness is due to a market that has indiscriminately punished the entire software sector, as well as the company's usage yield compressing, which bearish analysts have misinterpreted as an erosion in pricing power. NAVN is the technological leader in a $185bn corporate travel and expense market, disrupting legacy incumbents with a unified platform and a differentiated model. The stock trades at ~2.9x EV/FY26 sales based on guided revenue of ~$685m - a clear dislocation for a platform growing ~29% with 74% gross margins and 13% operating margins. A path to 30%+ margins exists at scale. The setup is likened to Booking.com in 2009 when it was trading under $100/share.

Edition: 232

- 20 March, 2026

Academy Sports & Outdoors (ASO US) US

Consumer Discretionary

John Zolidis’ investment case is based on a positive inflection in same-store sales producing valuation expansion as investors give more credit to unit growth and the longer-term opportunity. He believes this thesis remains intact as comps improved to -1.4% in FY25 (vs. -5.1% in FY24) and have turned positive in early FY26, with Q1 likely >2%. While the recent >10% share price drop reflects macro concerns and weak transaction trends (-6.4% in Q4), John views this as partly intentional, driven by ~10% price increases and a shift towards higher-income customers. This mix shift should support higher gross profit per ticket despite lower traffic. With the shares trading at 8x P/E and 5x EV/EBITDA (FY26 estimates) and a 9% FCF yield, ASO is a “bargain”, with an eye towards the upcoming analyst day as a near-term positive catalyst.

Edition: 232

- 20 March, 2026

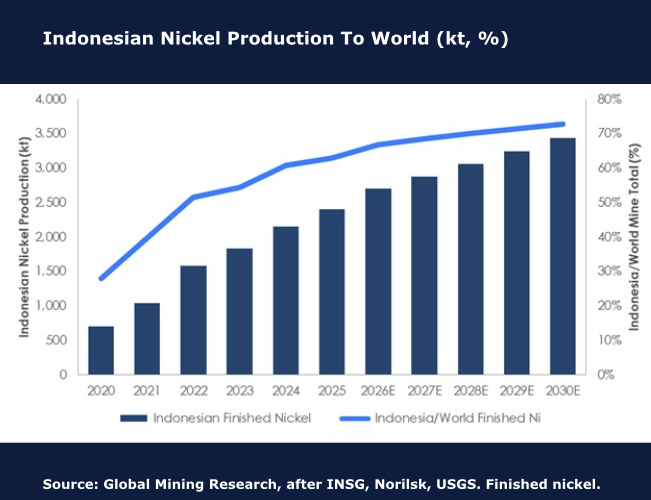

Nickel may yet surprise

Recent events brought spot nickel up to ~US7.80/lbafterabriefreturnto US8.00/lb. The three major developments that led to this are the Iran war, a decision by the Indonesian government to dramatically cut thermal coal mining permits from 790Mt to 600Mt, and another decision to cut laterite nickel mining permits to 260-270Mt versus 2025 at 379Mt. GMR has calculated an annual nickel demand growth rate at 6.2% CAGR over the last decade, but the unceasing volumes from Indonesia (see chart) have been the issue. New changes may see parts of the global nickel cash cost curve move by ~US$1.50/lb. If laterite ore is really cut back heavily, then the price impact should add to that, but very large inventories could limit substantive price moves for some time. This is all potential; good news for producers like Vale SA, Glencore PLC or MMG Ltd. It’s too late for the Cuban producers where the lack of fuel is triggering closures.

Edition: 232

- 20 March, 2026

Silver futures (SIK26) forecasts

With the attainment of the new low under 78.06, the Technical Analysis Group have closed half of their NT Strategic Short position, established into strength at 95/96, and are placing a trailing stop at 87.70 on the remainder of the trade. Price action from 97.30 has yet to reveal any urgency or impulsiveness to the downside. The team are expecting near term relative outperformance in gold vs silver, and are bullish the 'RATIO' whilst above 57.59, seeking upside in the near term to 67 +/-, and 72.66+. Since raising risk, they have seen a +12% rise to 64.47. The team continues to remain long term bullish and regardless of whether or not they’re in the higher degree 4th wave, they do not expect downside under their proposed 60 +/- 10 LT Long Term Range Base, before ultimately eclipsing this year’s 121.78+ high in the resumption of the underlying bull trend, exposing their next major upside attraction levels of 138 and 165 (see chart).

Edition: 232

- 20 March, 2026

Energy shocks are disinflationary

Barry Knapp examines how the current energy price spike functions as an adverse aggregate demand shock rather than a traditional inflationary driver. The US economy was already showing signs of weakening, causing rising energy costs to act as a “tax” on consumers, suppressing economic activity and threatening to push a fragile economy into a deeper slowdown. The USD is rising alongside energy prices, causing the cost of energy to increase even further. The popular idea that energy shocks automatically bring about long-term inflation can be refuted by looking at history through a different lens: the high inflation of the 1970s was a result of fiscal policy, and the 2022 surge in foods prices actually saw goods prices peak at the moment of the inflation but the disinflationary shock was masked as fiscal spending was still flooding the market. He is waiting for a 10% drop in the S&P500 before considering entry into cyclical sectors.

Edition: 232

- 20 March, 2026

Nigeria: Oil prices present another story

Jonathan Anderson remarks that, again, Nigeria has exceeded expectations on macro adjustment in a low oil price world. Over the past two years the authorities unified and stabilised the NGN rate, hiked rates to positive real levels, tightened fiscal policy, reduced money and credit growth, squeezed import demand, put the external balance in surplus and brought inflation down at home. Even so, Jonathan wasn’t enthused about asset markets with oil at $65/barrel. Sovereign bond and local equity prices already ran aggressively last year, and coming into 2026 he felt both markets were overdone at then-prevailing oil prices. Even the naira trade was likely "running out of steam" with potential fiscal pressures rebuilding. With oil over US$100/barrel, however, it's another story. If global crude prices stay in the triple digits, this makes every market look cheaper - and Jonathan would be particularly interested in FX carry and dollar debt once again.

Edition: 232

- 20 March, 2026

A World War III involving China is increasingly inevitable

David Murrin believes that the US could secure the Strait of Hormuz in three to four months should it utilise the full range of sensors and combat assets outlined in David’s latest report. However, he anticipates that the US will struggle to deploy and sustain such a high operational tempo, potentially extending the conflict well beyond that timeframe. In addition, there is a high probability that the depletion of American mid-course interceptors, the concentration of US naval and missile defence assets in the Gulf at the cost of Pacific and Atlantic deployments, and the disruption of oil flows as production facilities are damaged during missile/bomb exchanges will generate significant strategic compression. This will, in high probability, provide China with an opportunity to launch a major military campaign across the Pacific without warning to seize control out to the third island chain, potentially in parallel with a Russian escalation against NATO. In his latest report, David explores the possibility of the Iran situation sparking a global war.

Edition: 232

- 20 March, 2026

The Euro’s extremely important juncture

The Euro’s (€1.1416) monthly chart shows a breakout from a 17-year Down-channel, with the currency trading as high as €1.2083 in January this year, up 27% from the Sep 2022 low. Chris Roberts comments how a sustained breakout from the channel, following the 14-year, 40%+ fall in 2008-22, could potentially be very bullish. The near 6% fall from the recent high has taken the Euro back to the rising 20-month WMA and the 9-month RSI back to Neutral 50. Chris is 40% long from €1.1572 and would look to add on a break above the Jan high. His stop stays at a daily close below €1.0954.

Edition: 232

- 20 March, 2026

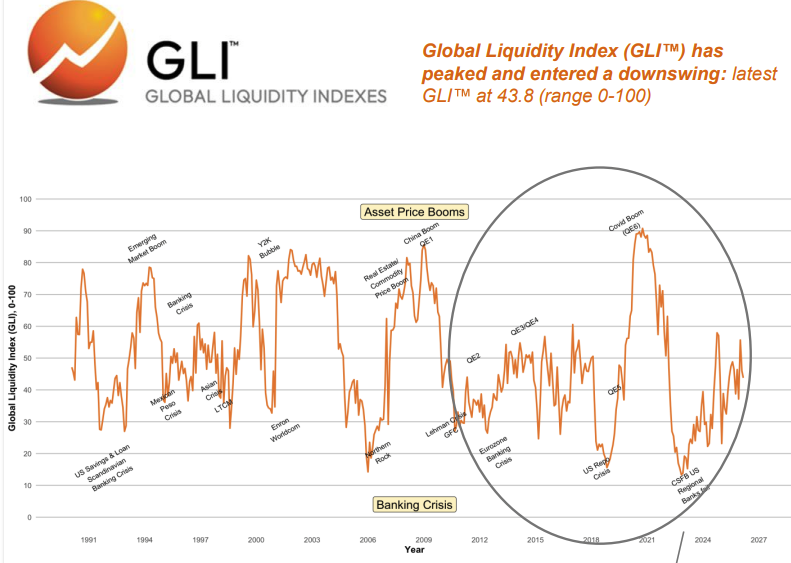

Black Swans vs Blue Owls

Michael Howell’s Global Liquidity Index (GLI) has peaked and entered a downswing, pushing market conditions towards a ‘Risk Off’ environment. This systemic downturn, rather than the oil spike alone, is the primary force eroding portfolio performance and explains growing stresses in private credit, as exemplified by troubles at firms like Blue Owl. While the Iran conflict-driven oil price spike acts as a negative Black Swan shock, its impact is compounded by the already weakening liquidity cycle. The Fed is managing liquidity to avoid market crashes, while the PBoC is aggressively injecting liquidity. This divergence justifies holding gold and explains why Chinese markets are at an earlier, more favourable stage of the investment cycle. With the liquidity downturn expected to last 12-15 months, the recommended strategy is to pare back credit and US tech exposure. Investors should rotate towards defensive assets like commodities (gold, oil), gradually add to mid-duration Treasuries, and increase holdings in Chinese stocks.

Edition: 232

- 20 March, 2026

AI: The economics of compute

sees the real story of GTC being the business model of compute. As AI rolls out, capacity demand is moving rapidly towards inference, and Richard would not be surprised to see it end up at 90% of the total market for AI infrastructure. He has long argued that the business case for compute is broken. NVIDIA Corp is claiming they can fix this with its new chips, increasing the revenue per GW by 5x. If true, it would change the economics of compute, and the company stands to improve the economics of AI computing more than anyone else. The fact that the market didn’t understand what Nvidia is trying to say means that it will continue to worry about longer-term growth, and the shares may continue to drift, possibly representing an opportunity to invest in the best AI company at an increasingly attractive valuation. Richard continues to hold Samsung Electronics Co Ltd and Qualcomm Inc for AI, Ouster Inc for robotics, and nuclear power.

Edition: 232

- 20 March, 2026

Financials

Galliano's Financials Research

Victor Galliano upgrades the stock to Buy, arguing that the recent partial disposal of its stake in Nintendo could mark the start of a broader unwind of the bank’s large strategic equity portfolio - its primary source of potential shareholder value creation. The sale generated a ¥75.1bn gain (c.¥90bn proceeds) and reduced Kyoto’s stake from 4.2% to 3.3%, though the remaining holding still represents more than 30% of the bank’s market value. With ¥160bn in gains on stock sales, Kyoto has also been able to crystallise roughly ¥90bn of losses on government bonds, bringing its unrealised losses on the domestic government bonds still on its balance sheet close to zero. Kyoto trades at the lowest PBV among Japan’s top ten banks, while its 4.1% dividend yield also has scope to rise.

Edition: 232

- 20 March, 2026

Regulated Utilities: No place to hide - compressing equity risk premiums

Utilities

Canadian regulated utilities are up ~10% YTD, outperforming the TSX, as rising geopolitical risk has driven a flight to safety and multiple expansion across defensive sectors. The re-rating has pushed equity risk premiums to levels that are difficult to justify against the prevailing rate backdrop and Veritas believes risk-adjusted returns have become materially less compelling at current valuations and recommends underweighting the sector. Their report covers Canadian-listed regulated utilities in their coverage (Emera, Fortis, Hydro One, Canadian Utilities, ATCO). Veritas’ analysis is structured around 3 analytical pillars: 1) current sector valuations relative to a yield-implied terminal capitalisation framework; 2) the macro backdrop governing utility equity performance; and 3) the company-level funding dynamics that determine whether rate base growth translates into per-share value creation.

Edition: 232

- 20 March, 2026

Technology

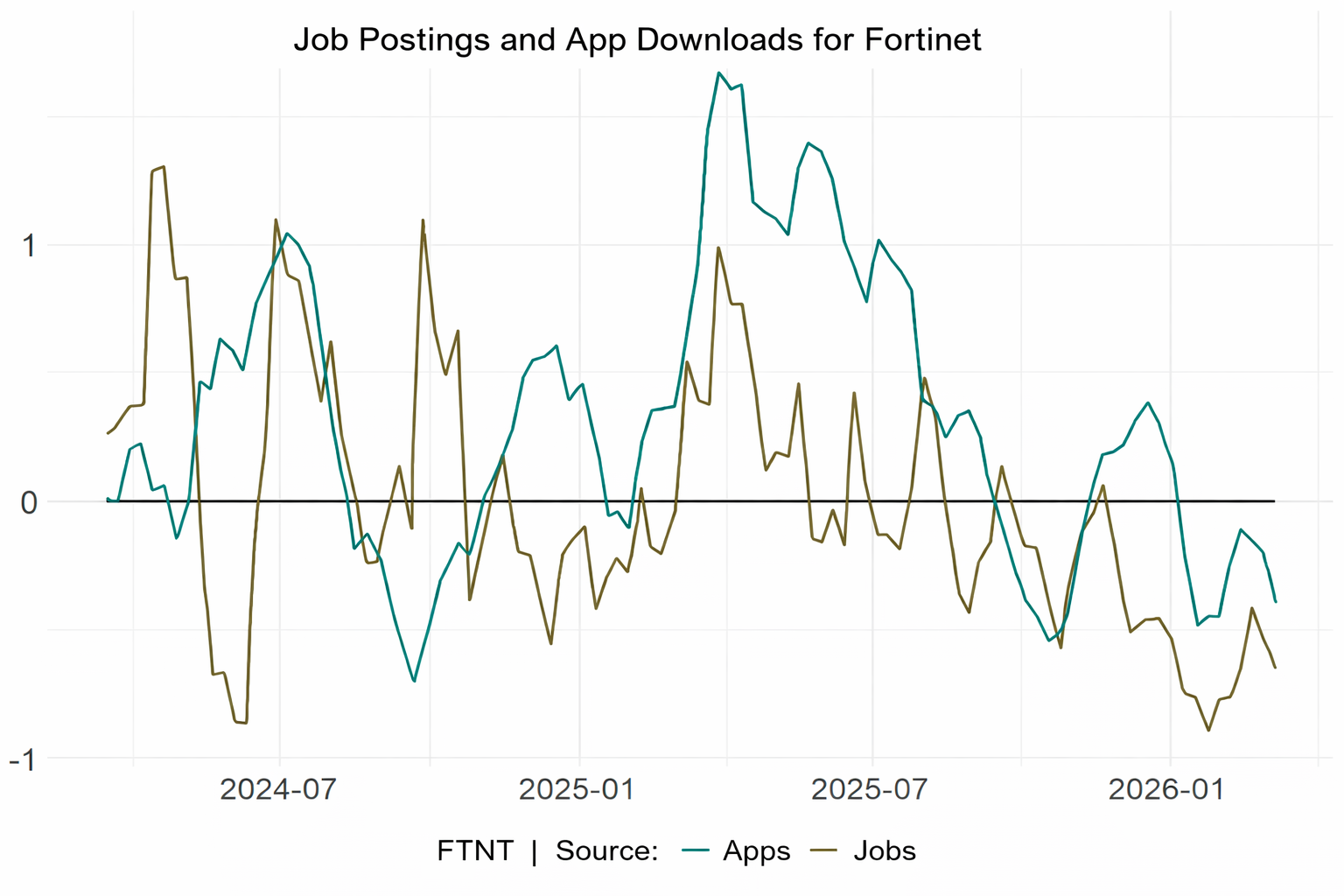

Structurally exposed to the shift from hardware firewalls to cloud-based security platforms and from network-based to an identity-based model, FTNT is losing ground to Zscaler and Cloudflare. Alternative data signals reinforce this view with FTNT ranking in the lowest quartile of AnteData’s measurement of coding activity trends, while freelancer job demand tied to its technologies is declining and downloads of its authentication app are falling. Although the company still holds ~18% of the global firewall market, revenue growth has slowed from ~20% in 2023 to ~12% currently, with AnteData expecting normalisation towards ~5%. With a net income margin already at 27%, they see limited scope for further expansion, making the ~34x earnings valuation appear demanding.

Edition: 232

- 20 March, 2026

American Eagle Outfitters (AEO US) US

Consumer Discretionary

The Retail Tracker sees improving momentum at AEO, driven by a rebound in Aerie, which returned to growth in late 2025 following assortment resets and a renewed focus on its younger customer. They expect this momentum to continue, supported by a positive contribution from Offline despite some lingering assortment inconsistency. By contrast, the core Eagle brand remains mixed: denim is "solid" with exposure to emerging trends such as ripped jeans and bootcut styles, but tops lack impact (the online range is much better than in store). Increased marketing spend - including partnerships with high-profile celebrities and country music events - is driving traffic and sales. With the stock down ~30% amid recent market volatility, AEO is an attractive opportunity at current levels.

Edition: 232

- 20 March, 2026

Bear’s Den Idea Forum

Short-focused events consistently rank among MYST’s best-performing Idea Forums with their last one yielding a ~70% hit rate and ~8.7% average positive alpha. The dominant theme at this meeting centred on companies confronting new competition driving share loss and margin compression, while other high-level topics included businesses facing AI-related challenges; “fading” cyclical recoveries; and GLP-1-driven demand destruction. MYST felt Calix (BEAD subsidy unwind favours lower-cost solutions + forensic red flags) and TransMedics (organ transplant tech leader facing share loss amid new competition) were “unique” and worth investigating, while convincing bearish arguments were also presented on A O Smith, Dollar General, Old Dominion Freight Line and Uber.

Edition: 232

- 20 March, 2026

Guidance warning season

Despite rising geopolitical risk, European corporate guidance has yet to reflect the potential economic impact. In AIR’s recent management meetings, discussion focused almost entirely on AI, with little attention paid to the Iran conflict despite surging energy prices and supply-chain stress that historically drive earnings revisions. The combination of unpriced macro risk and AI-driven sectoral disruption creates a credible basis for expecting a meaningful wave of 2026 earnings guidance revisions across European equities in the coming weeks. And the performance gap between the companies on the right side of these structural shifts and those on the wrong side will broaden. Stock winners include AI infrastructure beneficiaries such as Arm, Elmos, Aixtron and STM, alongside defence exposure at Exosens and Indra Sistemas. Euronext and Auto1 are also seen as largely insulated. Under pressure are Stroeer, Freenet and SES. In IT services, the sector is splitting between “The Conquerors” (Accenture, Cognizant, Reply) and “The Endangered” (Capgemini, Atos, Sage, Dassault Systemes, SAP).

Edition: 232

- 20 March, 2026

Helium: A commodity on the rise

Ben Finegold points out how the global helium market is a structural oligopoly, Qatar accounting for ~30% of the world’s helium supply. A prolonged conflict in the Middle East that disrupts production or shipments through the Strait of Hormuz could put a third of the world’s supply at risk. More importantly, the availability of helium iso-containers – critical to maintaining a global supply/demand balance – could be disrupted for at least 6 months. Demand for the commodity is accelerating, particularly in the aerospace industry where it is irreplaceable as a propellant of fuel. It is also used in semiconductor manufacturing and healthcare, where substitutes have yet to be found. How should investors play it? The Renergen Helium project, owned by ASP Isotopes Inc, produces both LNG and high-purity liquid helium from the same gas field, and is one of the world’s most significant helium developments and aims to become a major supplier.

Edition: 231

- 06 March, 2026

Start slowly closing oil positions on any further rise in price

William (Buff) Brown observes that the US/Israeli-Iranian conflict has spread throughout the region with major interruptions in oil transit in the Arabian Gulf, with Iranian missile strikes in neutral Gulf countries, i.e. Oman, Bahrain, UAE, etc. While most were strikes directed against US assets, there were also strikes against civilian areas. With regard to oil transit, Iran has claimed that the Strait of Hormuz is effectively “closed”. However, it is not closed in the sense that Iran is, as of yet, targeting vessels en masse and/or has mined the 2-mile-wide outbound channel. The situation remains highly dynamic, however, and could change one way or another at any time. In any event, with the prompt NYMEX crude oil contract trading above $70.00 per barrel, he suggests maintaining the status quo for the time being, but on any further material price strength slowly begin closing out long positions. He does not recommend going short as prices rise.

Edition: 231

- 06 March, 2026

Wheat joins the bull market

Spot wheat stands at USD5.91. Chris Roberts points out how the USD4.50-5.50 area is viewed as a floor, based on price action since 2007 (floors and ceilings can be penetrated but sustained moves are needed to change them). The 64% decline in 2022-25 is in line with other major falls since 1996, that range from -63% to -73%. The 9-Quarter RSI bottomed just below Low Neutral 40, similar to the 2016 low. Chris’s base case is that commodity bull market has resumed and he has a number of commodity-related longs. In the Grains and Oilseed complex, he has longs in soybean and soymeal and is now looking to add wheat.

Edition: 231

- 06 March, 2026

South Korea: Words of warning

Jonathan Anderson observes that Korean equities shot up another 50% in the first two months, making Korea the best-performing market on the planet in 2026 so far. He notes that this is heavily due to the AI boom and Samsung, but "domestic Korea" has continued to rally this year as well. However, there's still no support from domestic macro. As before, Korea's economy is flatlining or contracting almost everywhere he looks: durables, construction, retail, credit, earnings. And while exports are rebounding, memory prices still haven't been able to bring Korea back to the EM-wide average trend. Jonathan says it will be hard to motivate further gains in local names. Equity multiples have already eliminated the famed "Korea discount" and continue to rise at the margin, i.e., corporate reforms have already been priced in well in advance of actual results - and there's no sign that the rally is boosting earnings and growth potential as of yet.

Edition: 231

- 06 March, 2026

South Africa’s macro big bang is underway

Krutham (formerly known as Intellidex)

According to Peter Attard Montalto, the macro big bang is underway in South Africa and has entered a new phase of focus on risk premia compression. The yield curve has extended its repricing lower as the fiscal credibility reset at the 2025 budget statement has held - and was reinforced by Budget 2026 last month. The 10-year yield is around 8.2% as of March 2nd, its lowest level in 5+ years. Sovereign risk premia have continued to compress, as the fiscal golden threads remain intact despite not-too-exciting growth, while the de jure shift to a 3% inflation target has helped anchor longer-run inflation expectations and real rates. With the SARB delivering back-to-back 25bps cuts in May and July, followed by a further cut in November, the front end has repriced lower, and the curve has flattened, with the belly and long end doing most of the work as fiscal uncertainty turned into fiscal positivity and inflation risk premia compressed.

Edition: 231

- 06 March, 2026

Buy the dip on China tech

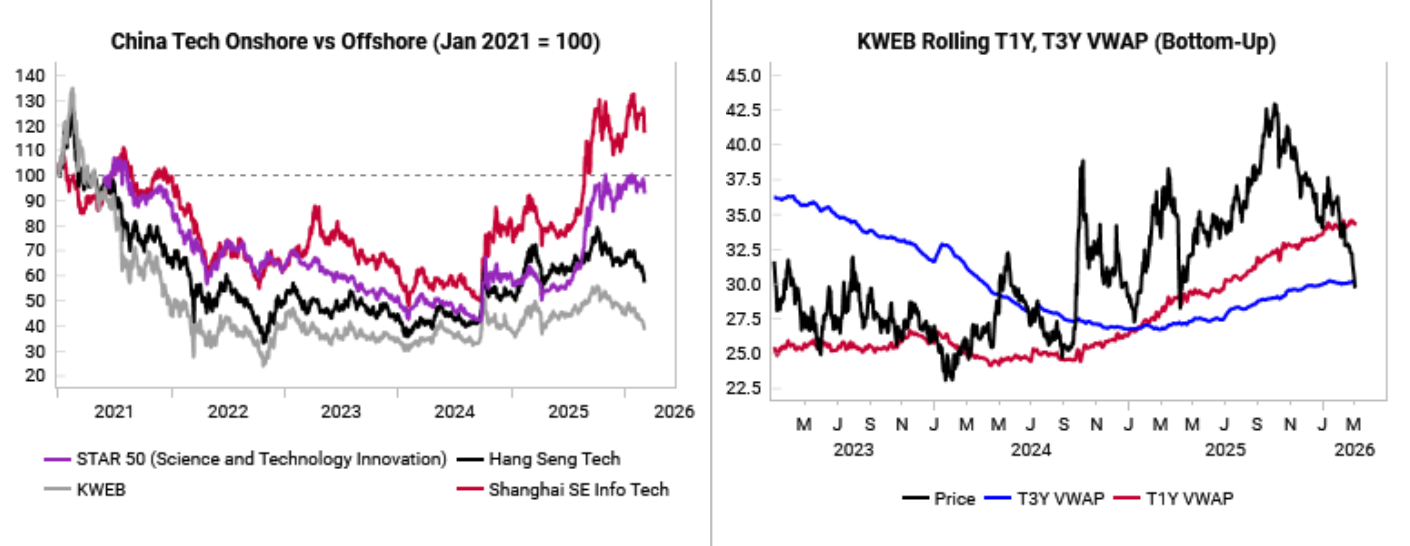

Offshore Chinese tech equities have materially lagged onshore equities over the past 6 months, suffering big drawdowns even as onshore equities make new highs. The KWEB China Tech ETF has now fallen down major support levels at the T3Y VWAP (see charts). The Variant Perception team are starting to see more LPPL crash exhaustions signals for Chinese tech stocks, while their fast money speculative flow proxy shows that they are approaching contrarian buy levels for KWEB. MSCI China is now underperforming the MSCI EM index by a wide margin, with the trailing 1-year relative performance below -2 standard deviations. Despite this, Chinese small caps have been outperforming large caps, a positive divergence that bodes well for future Chinese equity returns. There is a chance the Iran situation will worsen, and Chinese assets will be further caught up in the energy shock, but there is already a decent amount of dislocation priced into Chinese tech equities. Ultimately, this is an attractive entry point for investors.

Edition: 231

- 06 March, 2026

US manufacturing PMI does not set a new trend

Carl Weinberg points out that the US manufacturing PMI for February printed above its break-even level for a second month in a row, signalling an expansion in the sector. This is a surprise, and a positive one at that. However, Carl notes that the uncomfortable truth is that the correlation between headline ISM manufacturing and current-quarter GDP growth over the last decade is below 0.30. The economy has demonstrated it can grow without industrial growth, which has declined as a share of overall economic activity. The manufacturing sector is sick, barely growing at all. It has been contracting for a long time, and a print or two above 50 does not set a new trend. In short, manufacturing does not appear to be responding well to Trump’s economic policies. Tariffs do not seem to be increasing the business of existing firms, as this survey suggests, or creating new jobs in new firms as the payroll employment data suggest.

Edition: 231

- 06 March, 2026

Approaching peak AI hysteria

People are gregarious and instinctively follow the impulses of the herd, remarks James Aitken. The past two weeks have been a reminder of the mob mentality, and with dystopian projections on AI hysteria reaching millions of views, James believes we are approaching peak AI hysteria. Just remember when scouring the news: why am I reading this now and who benefits? XAI, Anthropic and OpenAI are all in windows to raise absurd amounts of money at lofty valuations, so it’s no surprise everyone is getting almost daily updates on LLMs about their improvements. DRAM, NAND and H100 rental prices suggest the AI juggernaut and associated memory shortage continues, yet so violent has been the recent shakedown that companies that would seem to have little risk of being disrupted by AI have been smashed, too. Just look at the current P/E of Microsoft (green) vs the current P/E of Colgate (red).

Edition: 231

- 06 March, 2026

G-III Apparel Group (GIII US), VF Corp (VFC US), Dillard's (DDS US) US

Consumer Discretionary

Hedgeye provides updates on 3 of their top Retail shorts. For GIII, they expect the next guide for the year to be an absolute disaster; forecasting a 20%+ cash flow hit from the the loss of major Calvin Klein and Tommy Hilfiger licenses back to PVH, while prior channel stuffing and tougher retail conditions could force the company to increase markdown support to key partners. Meanwhile, VFC is caught between a heavy debt burden and weakening brand momentum; Hedgeye believes a massively dilutive equity raise will ultimately be required. And finally, DDS remains a mispriced security, trading at ~12x EBITDA despite a sharply decelerating model and the company overearning by 800-1,000bp. That suggests that the real earnings power is between $10-20 per share. 5x earnings, is an appropriate department store multiple, suggesting 80-90% downside.

Edition: 231

- 06 March, 2026

China Internet: Opportunity after KWEB’s ~30% drop from its Oct peak

Sector valuation, as measured by 86Research’s proxy basket, now stands at a distressed 15.4x. Over the past 3 years, there has been 5 KWEB drawdowns >20% and each peak-to-trough episode lasting 3-6 months, suggesting the current correction could be nearing its end. Several catalysts may also help stabilise sentiment including Trump’s visit to China, the upcoming Two Sessions (additional stimulus) and improving economics from China’s AI leaders. In this issue of 86TradeIdeas, the team highlights several quality names that could command significantly higher multiples in a normalised market, including Trip.com, Atour and DiDi, alongside Beike, which could benefit from further housing policy support. Kuaishou and Baidu offer differentiated exposure to key AI verticals. Despite near-term geopolitical uncertainty, they see compelling re-rating potential across these names in the coming months.

Edition: 231

- 06 March, 2026

Why (some) EM Telcos’ multiples could double

Communications

The resumption of pricing power is one of the key drivers of the rally in EM Telcos and perhaps the area where consensus is most sceptical. In this note New Street analyses which markets have the greatest potential for sustained pricing power, looking at key issues: affordability and regulatory and competitive structure. Where these come together they see the potential for a multi-year period of above-inflation revenue growth from the core telco business. They also show that where pricing power is sustained, EM Telco multiples have doubled. As this plays out across the industry the scope for above market returns are high, and New Street remains (very) bullish on EM Telcos.

Edition: 231

- 06 March, 2026

Real Estate

CEO Andrew Florance’s destructive leadership style makes him unfit to lead CSGP’s costly residential pivot. His rigid, totalitarian micromanaging is incompatible with the disciplined, multi-front execution now required, making his past strengths his current greatest liabilities. CSGP would be better served with Florance receding into an Executive Chairman role, where his visionary strategic brilliance could be offset by a disciplined operational CEO more focused on ROI than empire building. Paragon’s research includes interviews with former senior executives at CSGP who worked with Florance for more than 36 years combined.

Edition: 231

- 06 March, 2026

Energy

A large-cap trading at just ~11x earnings, with a ~12% FCF yield and will pay owners a 10% yield in the very near future. The Coterra deal markedly increases DVN’s stature and shale production in the Delaware Basin without incremental acquisition debt, adding ~4,600 high-return drilling locations, nearly half with sub-$40/bbl breakevens. The combined company expects $1bn+ in annual synergies and plans a $5bn buyback, materially lifting FCF/share and NAV/share. Nevertheless, investors have yet to adequately reflect DVN’s improved fundamentals in its share price, with it continuing to trade at a sharp discount to other E&P players in terms of both P/OCF and at a high required FCF yield. For each 0.5x improvement in its P/OCF multiple or a 1pp decrease in its FCF yield, DVN’s share price will rise by ~$5.

Edition: 231

- 06 March, 2026

Gross margins are rolling over, but net margin expectations remain high

Median gross margins for the Top 500 peaked at 46.4% in Feb 25 and have since fallen to 44.9% in Jan 26, yet bottom-up forecasts imply continued strong net income growth - likely reflecting embedded AI-driven productivity assumptions. Historically, Trivariate finds valuation multiples correlate more closely with gross profit growth than net income growth, implying further multiple expansion will require renewed gross margin strength or a structural shift in how markets reward earnings. Their quantitatively derived longs (e.g. Merck, T-Mobile, McDonald’s) have had recent multiple expansion and are forecasted to have margin expansion, but not more net margin than gross margin expansion. While shorts (e.g. Amphenol, Salesforce, Arista Networks, Las Vegas Sands) screen for gross margin contraction but net margin expansion, reducing estimate achievability.

Edition: 231

- 06 March, 2026

Temenos (TEMN SW) Switzerland

Technology

US expansion is the key swing factor for TEMN over the next 12 months. With a well-resourced US sales team, a localised product suite and a pipeline growing faster than any other region, GR20 sees favourable conditions for deal conversion in 2026. They also believe the recent “Claude Cowork effect” that weighed on software valuations is fading, with sector multiples appearing to have bottomed. In GR20’s view, current valuations imply limited terminal value in DCF models - an anomaly given TEMN’s positioning and growth prospects. The stock trades at an undemanding 4.2x/3.9x 2026/27 EV/sales and 11.9x/10.9x EV/adjusted EBIT.

Edition: 231

- 06 March, 2026

Moncler (MONC IM) Italy

Consumer Discretionary

The shift from puffer-only to broader fashion outerwear (wool, shearling, fur) has expanded consumers’ wardrobes, with MONC well positioned at the intersection of function and luxury. Its core styles are not overly trend-led, supporting their status as long-term investment pieces with resale value. Pricing sits above Canada Goose and Herno, but below Prada and Loro Piana, sustaining an attractive premium tier. Beyond outerwear, The Retail Tracker sees opportunity in functional yet fashionable handbags (e.g., a travel line between Rimowa and Away). Footwear remains strong but still lacks a viral breakout moment. Meanwhile, early signs of a streetwear revival could lift visibility for Stone Island and help the brand extend beyond its core. Under new leadership, renewed energy in the stock could support a move back towards the 52-week high.

Edition: 231

- 06 March, 2026

Accounting red flags surface in latest filings

At Nexans, supplier financing increased, with payables under third-party bank arrangements rising from €341m at FY24 to €449m at FY25. Receivables securitisation and factoring programmes also grew, from €181m to €201m over the same period. Nordex saw contract assets rise from 37 to 48 days equivalent, offset by a matching surge in trade payables that neutralised cash flow impact. Accor disclosed a notable jump in long-term loans to Orient-Express entities following deconsolidation, while Airbus recorded an increase in receivables past due (from 25% of total receivables to 31%) and a release of provisions amounting to a total of €634m, a large amount of which was via “other risks and charges”.

Edition: 231

- 06 March, 2026

Venezuela: The fiscal receivership trap

Over a month after Maduro was removed, Venezuela is operating under a modern form of US fiscal receivership. Niall Ferguson remarks that history doesn’t point to a positive outlook, with previous examples rarely increasing revenues or creating long-lasting institutional change. Iraq showed that going all out with military occupation and recovered oil production, deep bond haircuts can still materialise. Genuine democratic transitions, like those in Spain or Paraguay, can take decades to materialise. Niall sees the most likely outcome for Venezuela being a modified Chavismo with closer ties to Washington. This is not the “different Venezuela” Secretary Rubio envisions but rather a rebranded authoritarianism, at least in the short term. Despite the market rally, Niall sees Venezuelan and PDVSA bonds as high-risk.

Edition: 230

- 20 February, 2026

India: Sounds nifty

The iShares MSCI India ETF (INDA US, USD52.89) has been ranging for 7.5 months following an initial 18% rally from the Mar 2025 low. Chris Roberts views the INDA’s Mar 2025 low as an important cyclical trough. At USD47.60, the ETF had retraced an exact 50% of the 2023-24 cyclical bull market. Note that RSI has been ranging between Low Neutral 40 and High Neutral 60, typical of a rangebound market. Chris remains 60% long the NSE Nifty (last 25,471) from 24,627.69 but will only add to Indian exposure if the INDA US breaks above the Jun high of 56.01.

Edition: 230

- 20 February, 2026

Bangladesh: Reform agenda focuses on deregulation and costs

Asif Khan observes that 49 individuals, primarily newly elected Members of Parliament from the Bangladesh Nationalist Party and its allied parties, were sworn in on February 17th as ministers and state ministers in the new cabinet led by BNP Chairman and Prime Minister Tarique Rahman. In policy-related remarks, newly appointed Finance and Planning Minister Amir Khosru Mahmud Chowdhury outlined a reform agenda focused on deregulation and reducing the cost of doing business. Meanwhile, the newly appointed Commerce Minister indicated that the government will seek a deferment of Bangladesh’s graduation from the Least Developed Country (LDC) category by at least three years.

Edition: 230

- 20 February, 2026

Argentina: A positive outlook

Niall Ferguson has argued that Argentina needs to show more and say less on reserve accumulation if it hopes to roll over its dollar debt maturities. The new year began with the central bank accumulating reserves at an impressive pace and Argentina’s country risk compressing sharply to ~500 basis points. Niall believes Economy Minister Caputo could soon be in a position to issue a bond in international markets, as Ecuador recently did at a comparable spread. Moreover, Argentina and the United States have concluded a trade and investment agreement, underscoring President Javier Milei’s steadfast political alignment with President Donald Trump. Niall remains optimistic about the Milei administration’s political and macro durability, and reforms are passing in Congress. However, he expects the FX outlook to continue dampening growth potential, forecasting ~3% growth this year along with a consolidated fiscal surplus.

Edition: 230

- 20 February, 2026

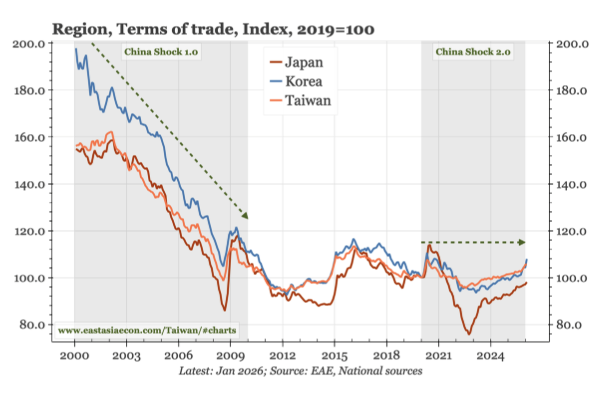

Asia and the China Shock 2.0

There’s a lot of talk about China Shock 2.0, where the flood of capital goods exports from China will be deflationary for the rest of the world. However, for the rest of Asia, Paul Cavey argues that the impact will be considerably less than that in the 2000s. That era saw a sharp deterioration in the terms of trade of nations across Asia, brought on by the huge demand for commodities from China which had offset the fall in electronics prices that occurred in the same period. By contrast, the last five years has seen export prices contributing positively to the terms of trade for the first time since at least the 1990s, helping offset the impact of the rise in import prices. The more stable terms of trade should provide support to Asian currencies. Asia is certainly exposed to China’s move up the value-added chain, with Korea looking particularly vulnerable, but the impact is likely to stop there.

Edition: 230

- 20 February, 2026

US: A staple diet

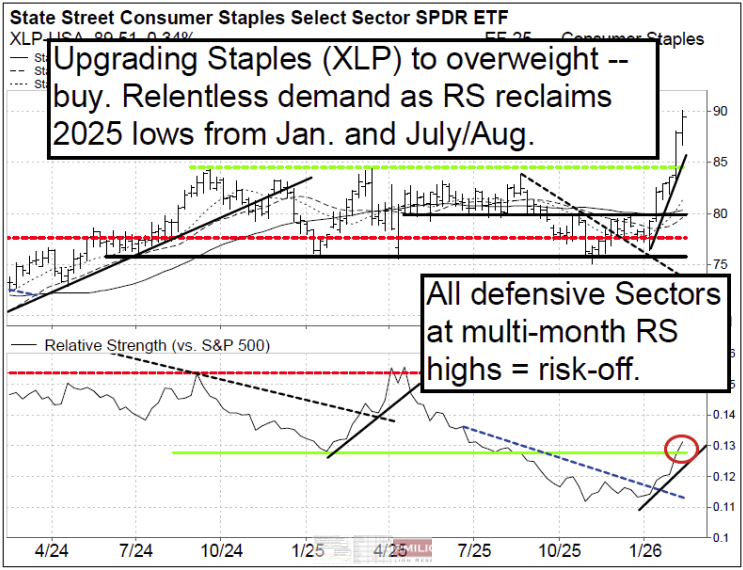

The Vermilion team will maintain their near-term bullish outlook on the S&P500 and Russell2000 as long as crucial support levels of 6780-6824 on SPX and $255-$257 on IWM continue to hold, although they do expect a period of consolidation/pullback. The team also maintain their bullish intermediate-term outlook, and recommend buying pullbacks, as long as market dynamics remain constructive and the SPX is above 6480-6520 and IWM is above $245. Staples (XLP) are at 7+month RS highs and the team are upgrading Staples to overweight (see chart).

Edition: 230

- 20 February, 2026

TBonds join the risk-off rotation

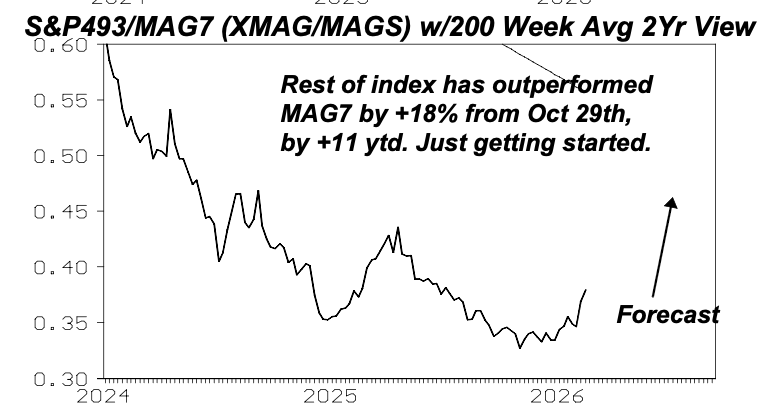

Michael Belkin’s model closed most short bond positions last week as he adds US and global sovereign bonds as new long positions, at what is now a major inflection point for US and global long-term interest rates. Michael’s hunch is that the recent risk-off move in sector rotation is now moving from equities into fixed income, with the MAG7 stocks in massive liquidation and the S&P500 unchanged on the year. Meanwhile, energy, consumer staples and utilities are all up, signalling a massive risk-off move in sector rotation. Of course, that’s the last thing Wall Street expects; the same sell-side strategists who said the software stock selloff was overdone never said to sell in the first place! Michael’s forecast for the Nasdaq points down big, both intermediate- and long-term. He maintains his bullish forecast for the value/growth and S&P493/MAG7 spreads, already up +13%ytd and +11%ytd (see chart).

Edition: 230

- 20 February, 2026

The post-1945 international order no longer exists

Brunello Rosa notes that the 62nd Munich Security Conference took place at a moment of profound uncertainty for the international system. Under the stark theme “Under Destruction”, much of the conference can be understood through two lenses: the Trump administration’s National Security Strategy, and the contrasting keynote speeches delivered in Munich by German Chancellor Merz and US Secretary of State Rubio. Chancellor Merz said the post-1945 international order “no longer exists”. A widening rift has emerged between Europe and the United States. Rubio gave a conciliatory address, emphasising that the United States and Europe “belong together”, but he also echoed Merz’s conclusion that “the old world is gone”. The conference ultimately laid bare a central paradox. Transatlantic tensions are real, structural, and unlikely to dissipate. Yet disengagement is not an option. In a world defined by fragmentation, rivalry, and competing visions of order, continued engagement may be strained, but it remains indispensable.

Edition: 230

- 20 February, 2026

STOXX 600: Leaders coming up to resistance

Valerie Gastaldy points out that the STOXX 600 has outperformed US indices in 2025. The strongest contributors to this performance have been Basic Resources, Telecom, Utilities, and Oil and Gas. Valerie notes that these sectors may still have a few additional percentage points of upside before three of them retest their 2007 highs. Banks, meanwhile, approached resistance again a couple of weeks ago. In the past, reactions at comparable levels have been relatively benign. However, if several leading sectors were to encounter resistance simultaneously in the coming days or weeks, Valerie says it would make the achievement of new index highs more challenging.

Edition: 230

- 20 February, 2026

Consumer Staples

OWS reiterates their short on COCO following 4Q25 results, arguing the print reinforces their original thesis that the company’s perceived supply chain “moat” is overstated. Management disclosed ongoing US market share losses and flagged heavier promotions, distributor incentives and stepped-up SG&A to defend growth. Private label competition is intensifying, pricing benefits are set to fade through FY26 and inventory has surged to 106 days, increasing the risk of further discounting. Meanwhile, ~96% of revenue still comes from coconut water, underscoring limited platform diversification. With insiders adopting new 10b5-1 selling plans and shares still trading at ~3.9x FY26 sales, OWS sees meaningful downside with a TP of $31 (35% downside).

Edition: 230

- 20 February, 2026

Insider buying in beaten-down Tech stocks

Technology

Smart Insider flags a number of insider buys at Hexagon, Sage and ATOSS following recent share price weakness, ranking all 3 stocks +1 (highest rating). At HEXA, the new CEO, Chief Strategy Officer and Vice Chair made their first purchases, buying a combined €3.4m of stock, shortly after results and the announced spin-off of Octave Intelligence. At SGE, 2 long-serving non-execs bought stock, including one director tripling his holding in a rare purchase and at a higher price than his last buy 5 years ago. At AOF, the CEO invested €11.6m (adding 4% to his stake) and the long-tenured CFO made his first-ever purchase - a notable shift from a series of smaller sales.

Edition: 230

- 20 February, 2026

Financials

The investment thesis is straightforward: EG's market cap is $13.7bn, its book value is $15.5bn and it generates >$2bn per year from investment income alone. In other words, EG could make no money at all through its core reinsurance and insurance businesses every year, and still be undervalued. It is an incredibly low bar for positive returns. The core risks would be heavy insurance losses going forward or significant deterioration in the investment portfolio. The losses required would need to be much more serious than simply a ‘bad catastrophe’ year, it would require multiple years of dreadfully written business. Ben Jones thinks this is highly unlikely, especially as the group is moving in the correct direction by limiting casualty business and purchasing additional cover for previously written long-tail business.

Edition: 230

- 20 February, 2026

Vinci (DG FP) France

Industrials

Robert Crimes updates its long-term forecasts for the stock and increases his TP to €192 (40% upside). The company boasts a high-quality mix of French autoroutes, international airport concessions, while Energies benefits from global megatrends driven by energy transition and digital transformation. In 2026-30E, Robert estimates DG will generate >€30bn of cumulative FCF pre-dividends. He assumes ~€20bn is returned to shareholders including €17bn of dividends, supporting a DPS CAGR of +10% over the period, plus €3bn of net share buybacks, while still leaving c.€8bn of additional capital available for debt reduction (yet Group ND/EBITDA is already low at 1.3x in 2026E), long-duration acquisitions (most likely airports) to increase the company's weighted average Concession duration or enhanced shareholder distributions.

Edition: 230

- 20 February, 2026

Aditya Vision (AVL IN), Brainbees (FIRSTCRY IN), Bluestone Jewellery (BLUESTONE IN) India

Consumer Discretionary

Iii conducted channel checks across the 3 companies to assess demand, competition and store economics. Footfall is flat to modestly down, growth is increasingly promotion- or online-led and store-level productivity appears constrained - pointing to normalisation rather than reacceleration in discretionary demand. On FirstCry, consensus expects multichannel growth to reaccelerate to mid-to-high teens via RocketBees and FC Quick, however, Iii believes execution delays and intense competition will keep growth in low single digits. For Bluestone, the Street assumes Q3’s operating leverage and ~12% pre-IndAS EBITDA margin are sustainable, but Iii expects margins to deteriorate within 1-3 quarters as seasonally weaker revenues expose a high fixed-cost base. At AVL, incremental store expansion appears supported by discounting and channel inventory build rather than productivity-led leverage.

Edition: 230

- 20 February, 2026

Technology

Arete describes TSMC’s 4Q25 call as one of the most significant tech updates in years. There were some seismic statements from the normally conservative management team: $52-56bn 2026 capex, “significantly higher” three-year spend, AI accelerator growth at a mid- to high-50% CAGR to ’29 and a 25% five-year overall revenue CAGR. Arete believes TSMC has unmatched visibility across the AI supply chain and is effectively fully booked at the leading edge through 2027, with hyperscaler capex underpinning multi-year demand. They model N2 capacity ramping to ~295k wpm by YE28 and see pricing power (including US wafer premiums) sustaining low-to-mid 60s gross margins. Despite execution and hiring risks, Arete lifts their TP to NT$2,770 (45% upside), viewing earnings growth - not multiple re-rating - as the key driver.

Edition: 230

- 20 February, 2026

Indika Energy: Moody's downgrades ratings to B1 from Baa3

Materials

Lucror broadly agrees with Moody’s downgrade, consistent with their “Negative” Credit Bias since Aug 24. Weak metrics are set to deteriorate further amid higher-than-budgeted capex at the Awak Mas gold project and subdued thermal coal prices. Leverage is projected to rise to c.7.0x Debt/EBITDA in FY26 (from c.6.0x in FY25) before easing toward c.4.0x in FY27 as gold operations stabilise. Liquidity is viewed as adequate over the next 12-18 months, but covenant headroom will tighten, particularly around the 3.75x Net Debt/EBITDA test. That said, the Newcastle coal benchmark has stabilised for almost a year now, so, Indika’s credit metrics may not worsen much more going forward and Lucror agrees with Moody’s outlook revision to stable. They maintain a "Buy" recommendation on the INDYIJ 8.75 '29s at 99.6/8.9%/2.7Y, as the high yield more than compensates for the weak and deteriorating credit profile.

Edition: 230

- 20 February, 2026

Ero Copper (ERO CN) Canada

Materials

The company reported 2025 copper production of 64kt, below its latest 67-80kt guidance (previously 75-85kt). FY26/27 guidance has been cut, Tucumã costs increased and capex lifted materially vs. GMR’s previous expectations, extending a multi-year pattern of downgrades. Despite this, the shares fell only ~15% which was not much worse than other miners in the recent sell-off. On the positive side, Q4 production improved sequentially and GMR forecasts copper output to rise to 67kt in 2026 and 76kt in 2027, with Xavantina gold remaining highly profitable. However, on the back of the news, they have reduced NPV10 (copper US$4.75/lb real) by 33% to US$12.45/sh. The stock trades at ~2.5x valuation with FCF yields now much lower than previously estimated. To GMR the risk/reward is no longer attractive given the shares are near a five-year high. Downgrade to Sell.

Edition: 230

- 20 February, 2026