Fortnightly Publication Highlighting Latest Insights From IRF Providers

Company Research

Retail predictions for the year ahead

Consumer

Gordon Haskett Research Advisors

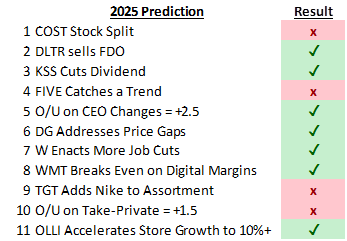

Looking back at GHRA’s 2025 Top 10 (+1) predictions, their batting average was good, hitting on 7 of 11 (see above). For the year ahead, their forecasts include: 1) Target announces an investment cycle on Mar 3rd with adjusted FY26 EBIT margin in the ~3.0%-4.0% range and a 2030 view of ~5.0%-6.0%. 2) Five Below launches Digital Loyalty Card. 3) Academy Sports adds another big brand…likely HOKA. 4) Costco unveils a special dividend and/or ramps share buybacks. 5) Ollie's embarks on large scale sales productivity effort. 6) Burlington takes a page (or two) out of the Ross Stores marketing playbook. 7) Someone gets acquired; BJ’s and Arhaus the most likely candidates. 8) Home improvement recovery gets pushed out…again.

Edition: 227

- 09 January, 2026

Retail Cross Currents: 4 key themes & top stock ideas

Consumer

Gordon Haskett Research Advisors

GHRA highlights an unusually volatile retail backdrop through late 2025 and early 2026, noting multiple “cross currents” affecting both consumers and retailers. Recent rating changes include downgrades for Dollar Tree (Reduce) and BJ's Wholesale Club (Hold), while upgrades cover Williams-Sonoma (Buy), Wayfair (Accumulate), Kohl's (Accumulate) and Dick's Sporting Goods (Hold). GHRA’s key investment themes emphasise: 1) stocks offering both EPS upside and multiple expansion (Five Below, Ross Stores, Burlington); 2) underappreciated turnaround stories (Kohl's, Dollar General); 3) selective “rate-trade” exposure favouring home furnishings over home improvement (Williams-Sonoma, Wayfair, Tractor Supply); and 4) secular winners / “Coffee Can” stocks (Walmart, Costco, TJX, Ollie's Bargain Outlet, Casey's).

Edition: 221

- 03 October, 2025

Consumer Discretionary

Janet Kloppenburg was impressed with BURL’s Q4 results and the company’s long-delayed 2.0 plan is now unfolding, supported by supply chain improvements and a shift towards an off-price sourcing model. BURL is also benefitting from acquiring its distribution centres, which enhances cost control. A more experienced buying team has helped to stabilise brand quality and product flow. Higher AUR levels also provide evidence that a higher quality consumer (who wants a deal) is now considering BURL as a value shopping alternative. Janet’s FY25 EPS estimate is $9.30, but looks for upside opportunity throughout the year with infrastructure now better prepared to drive +L to +MSD comps and greater margin and earnings flow through.

Edition: 207

- 21 March, 2025

Consumer Discretionary

Gordon Haskett Research Advisors

Ahead of the print, GHRA upgrades the stock to Buy and raises their 2Q24 SSS estimate to 4% (vs. guidance of 0%-2%), driving total sales growth of 12.7% to $2.4bn and EPS of $1.00. GHRA’s footfall data has inflected higher on a both a one and two-year stacked basis, while QTD traffic through the first two weeks of 3Q24 has stayed strong (Aug > Jul). Longer-term, they expect BURL's 2.0 Strategy to drive improved comps and margins. The company can close the performance gap to peers and while sceptics will argue that this expectation is largely reflected in the stock and valuation, GHRA thinks investors should barbell higher quality retailers with some turnaround / defensive characteristics to increase alpha.

Edition: 193

- 23 August, 2024

10Q / 10K filings analysis

Utilising AI, NLP, data analytics and qualitative analyst oversight, 280First can rapidly glean material / actionable insights from a company's financial reports. Recent alerts include: 1) Assured Guaranty - caution on liquidity claims; colour on impact from downgrade of financial strength. 2) Burlington - more positive views on comparable store sales. 3) Dollar Tree - may need to lower prices to remain competitive. 4) Keysight Technologies - seeing order cancellations? 5) Mattel - no longer focused on advancing e-Commerce and DTC business. 6) Salesforce - rethinking level of additional growth opportunities.

Edition: 183

- 05 April, 2024

European & US short ideas

Since Vision pitched their short thesis on Vidrala, Verallia and O-I Glass at our Equity Shorting Conference in mid-Mar the stocks have underperformed the Stoxx600 by ~8%. In the last couple of months they have also initiated 3 new European shorts, 3 new US shorts, and has readied a new $7bn+ European short (trades ~$20m/day and has short interest of <1%) for initiation next week. Please join Vision for a meeting while members of their team are in Paris (Jun 5th-6th), Zurich (Jun 7th) and London (Jun 8th-12th).

In the last 24 months, Vision has closed several shorts including: Allegro, AutoStore, Boohoo, Burlington, Colruyt, De'Longhi, Electrolux, Gerresheimer, H&M, Hargreaves Lansdown, Inditex, New Relic, Nokian Tyres, Peloton, Similarweb, Thule, Trex, TSMC, UiPath and Whirlpool.

Edition: 161

- 26 May, 2023

Broadlines & Hardlines Retail: Inventory review

Consumer Discretionary

Gordon Haskett Research Advisors

Across GHRA’s coverage inventory grew ~35% y/y on average in 1Q (or ~$40bn in aggregate) vs. average sales growth of just 3.5%, with the inventory/sales spread widening to ~31.5% (from 4.5% in 4Q). Another disappointing update from Target will further raise fears that retailers are over inventoried and gross margins will face increasing downside risk. This inventory overhang will take time to work through, but off-price retailers TJX and Burlington are well placed to benefit as it will create attractive closeout opportunities that could drive upside to 2H22 estimates.

Edition: 137

- 10 June, 2022

These retailers are primed for growth in 2022

Consumer Discretionary

Consumer stocks are climbing the wall of worry reflecting supply chain challenges, higher distribution expense, rising prices and tough comps. Hence, there is limited visibility on the consumer sector delivering yoy F22 earnings gains. JJK highlight a select few who are well positioned for growth, including the value focused off-price retailers (TJX, Burlington, Ross) and beauty leaders (Bath & Body Works, Estee Lauder, Ulta). Upgraded growth strategies and Europe’s emerging rebound should also drive strong upside at A&F, Capri Holdings, Lululemon, PVH, Ralph Lauren and Victoria’s Secret.

Edition: 120

- 01 October, 2021