Fortnightly Publication Highlighting Latest Insights From IRF Providers

Company Research

OpenClaw drives AI shift, but disruption risk overstated

Communications

86Research argues the rise of OpenClaw and AI agents is reshaping China’s internet ecosystem but believes market concerns are overstated. While agent frameworks could emerge as new traffic gateways and LLM platforms have already captured 8-10ppt of global traffic share, the firm sees disruption as more incremental than structural in core consumer use cases. China’s low software penetration supports rapid AI adoption but also limits near-term cannibalisation. Despite execution premiums being assigned to startups and ByteDance, 86Research believes incumbents such as Tencent and Alibaba retain strong underlying advantages and sufficient time to adapt. Recent share price weakness is therefore seen as a buying opportunity. However, they turn more cautious on Kuaishou, removing it from their Top Buy list amid intensifying competitive pressures.

Edition: 232

- 20 March, 2026

US Producer Price Index

For the January PPI report, John Ryding wrote the report "ought to be a blow to hopes of a quick return to 2% and further suggests that monetary policy is accommodative." The report for February adds to this assessment ahead of the oil shock adding to price pressures. Final demand PPI inflation rose to 3.4% from 2.9% on a 12-month basis with all major categories adding to the upward pressure (core goods, food, energy, and services--see table for details). On the old methodology basis for goods, the pipeline pressures were rising strongly even before the oil price shock. Not only is it too soon to say that PPI inflation is moving in a way that it is consistent with a gradual return to 2%, but it is also too soon to say if the upward move in inflation is levelling off.

Edition: 232

- 20 March, 2026

American Eagle Outfitters (AEO US) US

Consumer Discretionary

The Retail Tracker sees improving momentum at AEO, driven by a rebound in Aerie, which returned to growth in late 2025 following assortment resets and a renewed focus on its younger customer. They expect this momentum to continue, supported by a positive contribution from Offline despite some lingering assortment inconsistency. By contrast, the core Eagle brand remains mixed: denim is "solid" with exposure to emerging trends such as ripped jeans and bootcut styles, but tops lack impact (the online range is much better than in store). Increased marketing spend - including partnerships with high-profile celebrities and country music events - is driving traffic and sales. With the stock down ~30% amid recent market volatility, AEO is an attractive opportunity at current levels.

Edition: 232

- 20 March, 2026

Consumer Staples

Scott Mushkin remains cautious on TGT despite management acknowledging some operational challenges flagged in his field research. Recent store visits continue to reveal poor endcap execution, high levels of discarded items, long checkout lines, out-of-stocks and even extreme messiness. These nagging store operating challenges are likely to take more effort to overcome than management currently believes. He also sees several structural pressures ahead. TGT may need to sacrifice gross margin to improve price competitiveness, while everyday essentials could face deflation in 2026 amid heightened competition. Meanwhile, Walmart and Amazon are unlikely to cede share and TGT’s core demographic offers limited growth. Scott believes the recent swing to positive sales reflects easy comps and short-term consumer spending variability rather than a structural improvement in demand.

Edition: 231

- 06 March, 2026

Why (some) EM Telcos’ multiples could double

Communications

The resumption of pricing power is one of the key drivers of the rally in EM Telcos and perhaps the area where consensus is most sceptical. In this note New Street analyses which markets have the greatest potential for sustained pricing power, looking at key issues: affordability and regulatory and competitive structure. Where these come together they see the potential for a multi-year period of above-inflation revenue growth from the core telco business. They also show that where pricing power is sustained, EM Telco multiples have doubled. As this plays out across the industry the scope for above market returns are high, and New Street remains (very) bullish on EM Telcos.

Edition: 231

- 06 March, 2026

Moncler (MONC IM) Italy

Consumer Discretionary

The shift from puffer-only to broader fashion outerwear (wool, shearling, fur) has expanded consumers’ wardrobes, with MONC well positioned at the intersection of function and luxury. Its core styles are not overly trend-led, supporting their status as long-term investment pieces with resale value. Pricing sits above Canada Goose and Herno, but below Prada and Loro Piana, sustaining an attractive premium tier. Beyond outerwear, The Retail Tracker sees opportunity in functional yet fashionable handbags (e.g., a travel line between Rimowa and Away). Footwear remains strong but still lacks a viral breakout moment. Meanwhile, early signs of a streetwear revival could lift visibility for Stone Island and help the brand extend beyond its core. Under new leadership, renewed energy in the stock could support a move back towards the 52-week high.

Edition: 231

- 06 March, 2026

The best FX trade for 2026

In Stephen Jen’s view, USDJPY may be the best (i.e., with the highest Sharpe ratio) FX trade for 2026. With the dominant election victory, Stephen points out that the LDP has enough popular support for PM Takaichi to go through with her 3%-GDP worth of fiscal stimulus. With inflation still above the BOJ’s target (headline CPI is down to 2.1%, but core-core is still hovering around 3.0%), this prospective fiscal stimulus will likely be met with accelerated or earlier rate hikes by the BOJ. Stephen says that the US Fed and the BOJ will continue to converge in 2026, with the former cutting while the latter is hiking. Stephen argues that the US dollar itself is in a structural descent, and the particular policy mix in Japan should lead to a stronger JPY. He still views 125 as a very reasonable target for USDJPY this year.

Edition: 230

- 20 February, 2026

US: Fall in short-dated Treasury yields needs to be quicker

Graham Turner points out that US core inflation is trending just above 2.0%. The ex-food, energy & shelter CPI was up 2.20% in the 6-months to January, annualised. Meanwhile unemployment is falling, despite a rise in the labour market participation rate to new highs. The rapid adoption of AI suggests that the growth-inflation trade-off for the economy should improve. Therefore, the noninflationary growth path of the US economy is notching higher. Graham comments that how the Treasury market views the jobs and inflation data has been interesting. The two-year Treasury yield fell to 3.40% on Friday, the lowest since October 27th, 2022. This is pulling longer-dated yields down: break-even inflation rates are falling across the curve. The Treasury market has rightly concluded that stronger labour market data does not preclude lower interest rates when AI shifts the NAIRU lower. However, to prevent stock markets falling, the decline in short-dated Treasury yields is going to need to be quicker.

Edition: 230

- 20 February, 2026

Financials

The investment thesis is straightforward: EG's market cap is $13.7bn, its book value is $15.5bn and it generates >$2bn per year from investment income alone. In other words, EG could make no money at all through its core reinsurance and insurance businesses every year, and still be undervalued. It is an incredibly low bar for positive returns. The core risks would be heavy insurance losses going forward or significant deterioration in the investment portfolio. The losses required would need to be much more serious than simply a ‘bad catastrophe’ year, it would require multiple years of dreadfully written business. Ben Jones thinks this is highly unlikely, especially as the group is moving in the correct direction by limiting casualty business and purchasing additional cover for previously written long-tail business.

Edition: 230

- 20 February, 2026

Special Sits Idea Forum

MYST’s buyside events continue to draw impressive attendance while consistently delivering strong results. This Forum was notable for highlighting several foreign companies with imminent US listings (Ashtead, Guardian Metal Resources, SK Square) as well as Healthcare stocks (Cigna, Qiagen). Other ideas presented include:

Boise Cascade (BCC) - trough multiple at cycle bottom with potential business split under new CEO. TP $207 (145% upside).

Core Scientific (CORZ) - robust HPC pipeline not reflected despite buildout running ahead of schedule. TP $34 (95% upside).

Ralliant (RAL) - cyclical inflection masked by “one-time” cost headwinds. TP $60 (35% upside).

VSE (VSEC) - compelling entry point for “transformational” aerospace story. TP $300 (35% upside).

Edition: 230

- 20 February, 2026

Vista Energy (VISTAA MM) Mexico

Energy

Vista announced the acquisition of Equinor’s non-operating interests in Bandurria Sur and Bajo del Toro, reinforcing its scale in the core of Vaca Muerta with low-cost, oil-weighted, cash-generative production. EM Spreads views the transaction as credit supportive, adding immediate EBITDA at implied multiples well below Vista’s own trading levels, while limiting execution risk through producing assets and established infrastructure, despite YPF remaining operator. The earn-out structure further improves downside protection by linking additional payments to higher oil prices. At current levels, EM Spreads maintains their Overweight view on Vista, preferring the 2033s for their better risk-adjusted balance of carry, duration and Argentina exposure.

Edition: 229

- 06 February, 2026

Healthcare

RDNT’s AI narrative is materially overhyped relative to fundamentals. The AI business remains nascent, loss-making and largely unreimbursed, with equipment vendors increasingly bundling AI into imaging hardware, eroding RDNT’s perceived edge. Meanwhile, the core business remains highly capital intensive: imaging equipment is costly and capex has consumed ~50% of EBITDA for several years. Lately, that is 10% of sales in a mid-teens margin business, more than twice that of Two Rivers’ selected comp group. Operating leverage is limited as labour, equipment and supply costs continue to rise. While RDNT has reduced its leverage, it is still a concern at 4.4x forward EBITDA. The stock is priced to perfection, trading at all-time high EV/Sales, EV/EBITDA and earnings multiples. It has historically traded at a 40-50% EBITDA multiple discount to the comps - now it trades on par with them.

Edition: 229

- 06 February, 2026

UK: Weak employment trumps noisy inflation

Year-end employment data was weak, confirming the recent labour market slowdown, with the payroll fall of 53k exacerbating the 33k decline in November. December CPI data was mixed but on the cool side. Headline inflation printed hotter than expected at 3.4% y/y, but core inflation held steady at 3.2% when economists expected it to accelerate. Tight financial conditions will cap growth upside and further dampen inflation, while recent strength in hard activity data partly reflects pent-up industrial activity rather than broad-based momentum. BCA’s UK growth diffusion index appears to have bottomed, but at a very low level. More BoE cuts will be required, with barely two 25 bps cuts priced by year-end. Further weak data could bring an April cut into focus. BCA’s Global Fixed Income strategists’ highest-conviction view for 2026 remains an overweight in UK gilts, alongside GBP 2-year/10-year steepeners. Sterling remains mispriced versus the USD: UK equities have priced in weakness, but the currency has not, and BCA remain underweight GBP on a 12-month horizon.

Edition: 228

- 23 January, 2026

South Africa: Sparking the transition

Krutham (formerly known as Intellidex)

According to Peter Attard Montalto, South Africa’s climate transition is set to reach a pivotal moment of action in 2026. Peter says that carbon budgets, a tighter carbon tax and trade measures such as the Carbon Border Adjustment Mechanism move climate risk from disclosure into core business and financial decisions. At the same time, sustainability reporting will gain momentum to shift from voluntary practice to mandatory, investor-focused standards aligned with IFRS S1 and IFRS S2. However, Peter points out that most companies are not ready. Disclosures still focus on non-financial metrics and remain weakly linked to earnings, asset values and capital allocation. Data quality and systems lag, raising costs, limiting access to capital and increasing greenwashing. Clear ownership is now essential. Policy, regulation and market expectations must align. Companies and banks must embed reporting into strategy and risk management so it supports the transition to net zero rather than becoming another compliance exercise.

Edition: 227

- 09 January, 2026

SAP (SAP GR) Germany

Technology

Arete upgrades SAP to Buy, citing improving demand visibility as the ECC end-of-support deadline drives renewed urgency around S/4 and cloud migrations. Based on their CIO and partner checks, sentiment towards SAP has improved in 2025 vs. 2024, especially in the last few months, with more customers accelerating or restarting migration plans. While large-enterprise resistance persists, RISE adoption has shown clear signs of improvement. Arete sees limited displacement risk from GenAI, which CIOs view as years away from impacting core enterprise platforms; instead, GenAI may act as an indirect catalyst, easing migrations via automation and code clean-up. Applying a ~30x P/E multiple to their higher FY27E EPS yields a new €270 FY26 TP, implying 30% upside.

Edition: 227

- 09 January, 2026

Industrials

Judy Marks is a poor fit for the CEO role. Her tenure has been marked by share-price underperformance, repeated guidance cuts, underinvestment in innovation and purging experienced internal talent to make way for inferior DEI placements. Facing a weak China market, Marks has relied on repeated restructurings that have further hurt morale and credibility. Paragon’s research draws on interviews with former senior executives from OTIS, Siemens and Dresser-Rand, revealing a sharp contrast between her stronger reputation at Siemens and overwhelmingly negative feedback from OTIS insiders. Sources cite a fear-based culture, weak grasp of the core service model and poor capital allocation. Paragon argues Marks’ leadership style is misaligned with the company's need for stability, operational discipline and reinvestment.

Edition: 227

- 09 January, 2026

Shorts continue to deliver outstanding returns

In 2025, MYST’s short ideas delivered an +11.3% average LTD alpha and 73.5% hit rate. Having reviewed all the shorts presented across their buyside events, several shorts remain compelling including:

Adobe - churn to accelerate due to new click to cancel laws + FTC scrutiny. TP $245 (30% downside).

Coca-Cola Consolidated - KO stake sale a red flag amid structural volume decline + MAHA / SNAP headwinds. This idea was highlighted at MYST’s Consumer Ideas event last month and the shares have already fallen 10%. TP $110 (25% downside).

Flutter - structural challenge from prediction markets jeopardises core online sports betting economics. TP $150 (30% downside).

Oklo - fuel supply constraints + regulatory hurdles create multi-year execution risk. TP $20 (80% downside).

Edition: 227

- 09 January, 2026

South Africa: One notch down, guard up

Krutham (formerly known as Intellidex)

The SARB delivered the unanimous 25bp cut that Peter Montalto expected, but this was no dovish pivot: the CPI path was only nudged slightly lower and the language stayed cautious. The MPC is now comfortable moving into “less restrictive territory”. It means that the country now sits a little above the new neutral range around 6.50%. Looking ahead, Peter remains more conservative than the QPM on both inflation and the policy path. He still sees a stickier non-core wedge and slower expectations pass-through than the model assumes, given the fixed public-sector wage agreement, Nersa’s tariff pipeline and unusual food CPI seasonality, even though the de jure shift to a 3% target pulls the expectations profile down. That keeps Peter above the SARB’s inflation and repo projections: his baseline is no further change for roughly six months, and a clearer next leg down only in H2 2026 to 6.00% end 2026.

Edition: 226

- 12 December, 2025

Ivanhoe Mines (IVN CN) Canada

Materials

A 2026 copper turnaround story - IVN is now producing from all 3 of its core and globally significant mining assets. However, this has not been reflected in the share price following the seismicity event at Kakula in May 25. The market is focused on short term risks, but Kakula’s recovery is being managed and 3Q25 volumes (annualised at 285kt/yr) likely marks the bottom. With the 3 operating assets contributing in 2026 and a new smelter set to lower costs, GMR sees next year as the inflection point. IVN also offers major exploration upside - its 100%-owned Makoko district alone has 9.2Mt of copper identified, with additional drilling across Angola, Zambia and Kazakhstan providing further optionality not priced in. Trading at 1.4x P/NPV10, IVN’s growth, scalability and asset quality make the risk/reward compelling.

Edition: 226

- 12 December, 2025

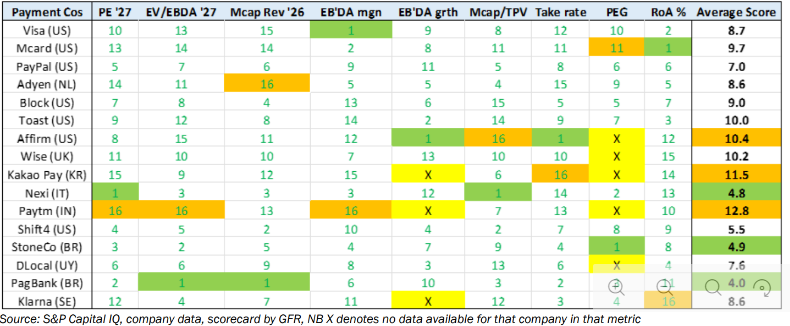

Payment Companies: 1H26 high conviction ideas

Technology

Galliano's Financials Research

Nexi is Victor Galliano’s top pick - it screens as one of the cheapest global payments names on market cap to revenue and market cap to TPV, with expanding EBITDA margins, rising take rate and improving cash opex discipline, all supported by increasing digital-payments penetration in Italy. PagSeguro remains his core LatAm Buy, despite strong YTD performance, valuations are still compelling and it ranks highly on Victor’s proprietary scorecard (see above), with a high net take rate relative to market cap to TPV. Affirm is the key Sell: Klarna’s IPO erodes scarcity value; valuation looks stretched on market cap to TPV and credit quality in its interest-bearing receivables is worsening. Klarna is one to watch - cheaper post-IPO, but BNPL competition and credit risks keep Victor on the sidelines pending a clear catalyst.

Edition: 226

- 12 December, 2025

September US retail sales up modestly but Q3 still strong

John Ryding points out that while the increase in retail sales was modest in September, for the quarter as a whole, sales were relatively solid with the control group measure of retail sales rising at the fastest rate (6.3%) since the first quarter of 2023. Core producer price inflation held steady in September at 2.9% but the increase over the last three months was a more rapid 4.7%. Jumping ahead to November, however, consumer confidence fell more sharply than expected as the median one-year inflation rate edged up to 4.8% from 4.7%, households’ perceptions of the labor market declined, and plans to buy autos and cars fell. John doesn’t see this report materially shifting the debate at the FOMC meeting on December 9-10 with the cut camp finding comfort in the inflation readings holding steady and the hold camp seeing potential faster price pressures in input costs and higher frequency inflation rates as well as the strength in retail sales for the quarter as a whole.

Edition: 225

- 28 November, 2025

Healthcare

Tom Tobin thinks there are several secular trends, including AI tailwinds, which makes RDNT a compelling idea even after its share price has rebounded in recent months. Core to Tom’s thesis is his ability to track Diagnostic Radiology staffing at RDNT, monitor turnover, and forecast volume and revenue per clinician. While the current valuation against consensus estimates appears stretched, he can model upside well into 2027 with a number of simultaneous secular tailwinds that justify the premium: 1) continued inpatient-to-outpatient imaging migration; 2) mix shift towards high-margin advanced imaging where demand is being driven by Alzheimer's, Oncology and Cardiology; and 3) AI tailwinds driving incremental revenue and operating leverage.

Edition: 225

- 28 November, 2025

Consumer Discretionary

Alibaba’s stepped-up AI investment is pressuring margins, but RFM argues it has now hit critical mass in open-source AI, making it the leading contender in China’s artificial intelligence race. Headline revenue growth in Q2 was only +5% Y/Y, but was +15% adjusting for disposals. The standout was Cloud Intelligence, +34% Y/Y, powered by surging demand for AI services. Qwen now has 180,000+ models on Hugging Face, more than double the No.2 player, giving Alibaba the network-effect scale needed to dominate China’s AI ecosystem. With core e-commerce stabilising and shares far cheaper than Amazon (17x FY26 P/E vs. 29x), RFM sees sentiment turning decisively positive.

Edition: 225

- 28 November, 2025

Technology

ZM delivered a "clean sweep" Q3 that should silence the sceptics. This was not just a beat-and-raise quarter; it was a validation of the company’s structural pivot from a meeting app to an AI-first work platform. With revenue and EPS ahead of forecasts, a raise in FY26 guide and a fresh $1bn buyback authorisation, management is demonstrating immense confidence in the company's capital allocation and operational execution. The real story for investors, however, is the tangible monetisation of AI: usage is up 4x Y/Y and paid AI features are now anchoring 9 out of 10 large CX deals. With the core business stabilising and the AI/CX growth engines firing on all cylinders, ZM offers a rare combination of deep value (trading at ~3.2x EV/Sales vs. peers at 3.7x) and highly profitable growth.

Edition: 225

- 28 November, 2025

How to beat the S&P500 - the Q&A that matter

Trivariate examines six core issues for long-only managers benchmarked to the S&P500: 1) Beta: despite long-term data favouring sub-1.0 beta portfolios, this is currently nearly impossible given the high-beta “Great 8”. 2) Alpha vs. Risk: ~75% of holdings should be for risk management. 3) Diversification: run both a broad risk book and a concentrated alpha book - essentially two portfolios in one; holding a higher number of stocks vs. history. 4) Position Sizing: take large, conviction-weighted bets in names with high company-specific risk / hard to replicate (e.g. Healthcare). 5) Blow-up Avoidance: avoid large exposures to bottom-decile FCF converters, large increases in inventory-to-sales, large intangible accruals and extreme valuations. 6) Macro: portfolio managers must consider what set of macro conditions are best for their portfolio performance.

Edition: 224

- 14 November, 2025

Consumer Discretionary

Breaking the value trap - 86Research’s report presents a focused analysis of GenAI-powered commerce, a strategic frontier they believe investors have overlooked. Market attention has remained concentrated on AliCloud’s reacceleration, while continuing to dismiss core commerce as a “value asset” trapped in macro drag. By spotlighting conversational interfaces and AI-enhanced ad tech as emerging structural advantages, 86Research sees a window of opportunity opening. A wave of initiatives has already unfolded in 2H25 and they expect Alibaba to further escalate its efforts in 2026, catalysing a period of positive news flow and re-rating potential.

Edition: 224

- 14 November, 2025

Industrials

Reno Bianchi argues that AAL’s core operating problem is management’s inability to control costs as effectively as competitors. Q3 was poor with a significantly deteriorating cash conversion rate and a substantial increase in the group's leverage metrics. He continues to recommend staying away from the risker parts of the group’s capital structure (equity and unsecureds) and also from the longer dated secured securities. He does not believe the fixed income market fully appreciates how speculative this credit really is.

Edition: 224

- 14 November, 2025

Consumer Discretionary

A story riddled with risk - Brian McGough argues DKS is priced for perfection despite mounting structural and cyclical headwinds. Core growth is tapped out and the House of Sport concept – its only unit growth driver - is not working; comping down 20% in year 2 and down again in year 3. Inventory issues, including a Critical Audit Matter on carrying value, and gross margin risks from tariffs on private-label apparel add further pressure. Apparel (40% of sales) has turned deflationary and the Foot Locker merger is seen as immediately margin-destructive, with no strategic merits and likely to strengthen competitors such as Academy and JD Sports. Brian is incrementally of the view that the 5-year CAGR for athletic footwear in the US is -300bp below pandemic-era trends and warns that at 10x EBITDA, a historical peak, DKS is over-owned, over-earning and due for a correction.

Edition: 223

- 31 October, 2025

Consumer Discretionary

The Retail Tracker notes continued improvement in URBN’s product assortments, describing the current offering as focused, confident and well-positioned for the holidays with stronger gifting and better alignment to its customer. New leadership is credited with sharper merchandising and more responsive assortments visible across stores, online and social media. Anthropologie and Free People remain strong, attracting younger shoppers while maintaining core customers, with standout accessories, home and active lines. Nuuly, the rental platform, continues to expand rapidly, offering tariff resilience and appealing to younger, price-sensitive consumers. The Retail Tracker has been positive on the name since early in the year and remains so.

Edition: 223

- 31 October, 2025

Eurozone: Consensus too optimistic on disinflation

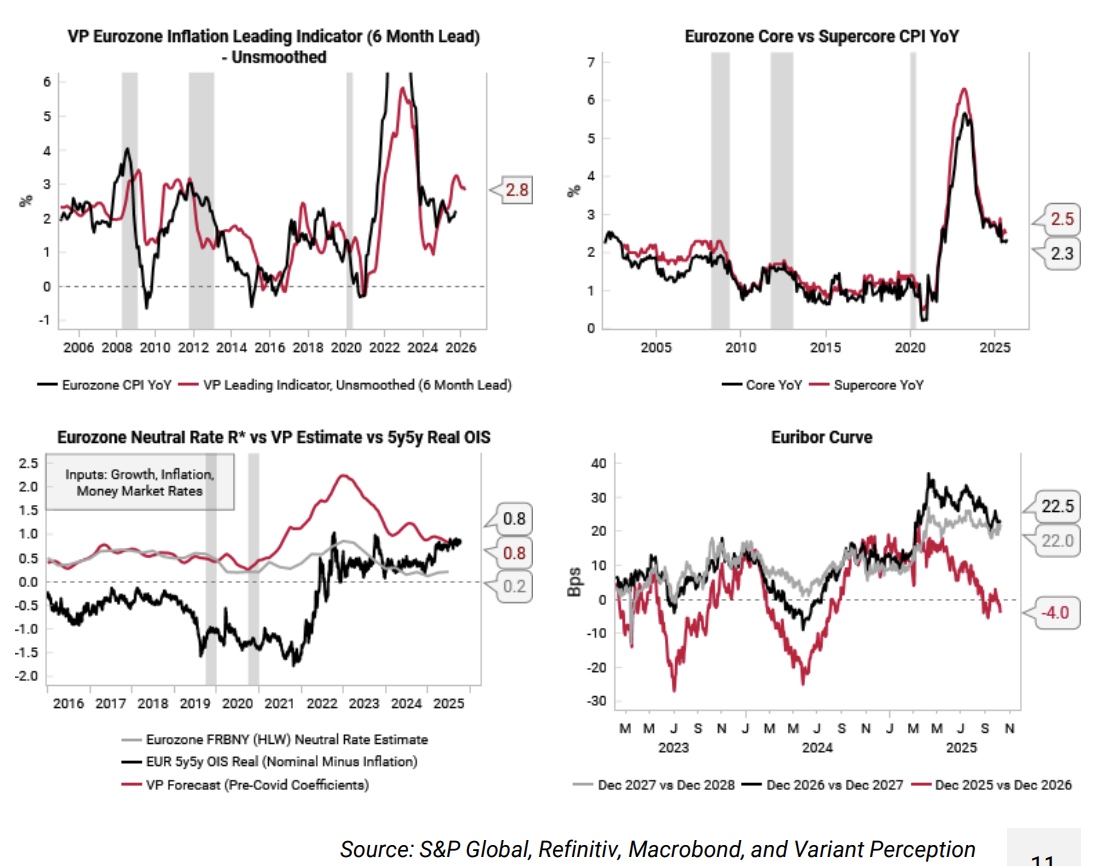

Consensus expectations see 2026 eurozone headline CPI at 1.8% and core CPI at 2%. The Variant Perception team suspects that inflation risks are tilted to the upside from here given the recovery in their eurozone growth leading indicators and the ECB rate cuts so far this year. Their main inflation leading indicator is rolling over from a high level, but the point estimate remains elevated at 2.8% (top left chart). Core and supercore CPI have also been slower to fall, still at 2.3 to 2.5% YoY (top right). The team put the real neutral rate (R*) for the eurozone at 0.8%, which is also where the 5y5y EUR real OIS is trading (bottom left). With headline CPI at 2%, there is good chance that ECB policy is already stimulatory, potentially creating inflation upside in 2026. The team take profits on their SOFR vs Euribor Dec 25/26 convergence trade established last month.

Edition: 222

- 17 October, 2025

Deutsche Boerse integrates social media intelligence in market surveillance software

While Deutsche Boerse has been an early adopter of social media monitoring for years, they have now taken the critical step of integrating Stockpulse's social analytics directly into their core Scila surveillance system. This integration provides comprehensive monitoring of 70,000+ global equities and cryptocurrencies with real-time social sentiment analysis, buzz metrics and seamless workflow integration within their mission-critical market oversight platform. This signals a broader trend toward holistic market surveillance encompassing trading data, news feeds and social sentiment. As social media increasingly shapes market dynamics, similar integrations are likely to follow globally. For investors, Stockpulse's insights into social sentiment, help spot emerging risks and opportunities before they hit the market. Contact us for a free trial / demo.

Edition: 221

- 03 October, 2025

China: The illusion of growth in China’s trust sector

Given the extreme financial stress in China, some may be surprised by the near record y/y growth in trust AUM to RMB29.6trn in 2024. However, Jonathan Anderson points out that nearly all of the growth came from passive products; true investment and financing trust AUM were essentially flat. Over a third of trust companies are technically insolvent or on the brink, and Jonathan doubts their long-term viability. Looking at the core active trust products, one will see them weighed down by unresolved defaults in the real estate and local government financial vehicle sectors, with freeze clauses on repayments placing a lot of active AUM into limbo. The impending collapse of many companies in the sector is unlikely to be a catalyst for broader financial contagion, but Jonathan mentions that its loss as a credit channel will still have wide implications.

Edition: 220

- 19 September, 2025

Galderma (GALD SW) Switzerland

Healthcare

While GALD shares have performed well since the company’s IPO, the stock remains in a "discovery phase", in which its valuation appears expensive amid consensus estimates that do not fully appreciate the underlying fundamental opportunity. Over 50% of cash flows are derived from Botox and dermal fillers, positioning GALD in a duopoly market with a wider moat and longer growth runway than traditional beauty peers. GALD's core skincare business is growing ~10% annually (relative to L’Oreal’s sub-5% revenue growth), driven by exposure to higher value, nascent life cycle segments. The investment case is further supported by the company’s new eczema treatment, Nemluvio, which could generate $5bn+ in sales vs. management’s $2bn guidance. TP CHF230 (60% upside).

Edition: 220

- 19 September, 2025

Industrials

FAN stands out as a high quality (29% FY24 FCF RoE) mid-cap building products and business services company that has bucked the trend of sluggishness across its core markets. The business has had a very successful buy-and-build strategy, using excess FCF and modest leverage to undertake earnings accretive M&A. The recent acquisition of Fantech exemplifies this and Fighting Financials thinks consensus estimates underestimate the full benefits of this deal. Beyond fundamentals, FAN also fits the profile of UK SMID-caps attracting takeover interest with 1) geographically diversified revenues; 2) high returns on capital; 3) modest leverage; and 4) suffering a discount due to trading on the troubled UK market.

Edition: 220

- 19 September, 2025

Technology

86Research attended Kuaishou’s Investor Day in Chengdu, where management highlighted how AI is boosting engagement and monetisation across its core community while scaling Kling AI. OneRec has already lifted time spent and GMV, with full rollout and ecommerce upgrades ahead. Management frames Kling as a sustainable long-term business in a US$140bn video market, though further proof points are still needed.

Edition: 219

- 05 September, 2025

Consumer stocks poised for a recovery

Consumer Discretionary

AIR expects a wave of upward revisions from European corporations in the coming months as tariff clouds thin, China stabilises, infrastructure spend ramps up and European rates remain low. The missing piece is consumer confidence, which should rebound quickly if geopolitical tensions ease. Consumer names like Inditex, Stellantis, LVMH, Diageo, Kering, Adidas, Nestle and Unilever look compelling after steep share price declines, with valuations back to decade-lows. Many of these firms are pursuing clear turnaround strategies focused on FCF generation, deep efficiency gains (utilising AI) and renewed focus on core businesses - supported by a trend toward insider CEO appointments, after a decade of appointing outsiders.

Edition: 218

- 22 August, 2025

Quantum computing primer unveils two new Buy ideas

Technology

Rosenblatt initiates coverage on D-Wave (Buy, $30 TP) and IonQ (Buy, $70 TP), identifying them as differentiated, high-conviction ideas in the rapidly expanding quantum computing market. QBTS offers unique exposure to quantum annealing - particularly suited for optimisation workloads - and is expected to grow revenues at a +66% CAGR from 2025-2030. IONQ, a leader in trapped-ion architectures, is positioned to exceed $1bn in revenue within the next few years, with significant upside from its product roadmap and ecosystem development. These initiations are framed by Rosenblatt’s comprehensive quantum computing primer, which outlines the core principles, architectures and commercialisation pathways shaping the industry’s next era and underpins the firm’s bullish stance on both names.

Edition: 217

- 08 August, 2025

Consumer Staples

Scott Mushkin downgrades DG to Sell, citing widening price gaps with competitors, which threaten margins and volume share gains over the next 12-18 months. R5’s latest fieldwork shows a total basket premium of 9% vs. Walmart - well above the typical 3-7% range. Scott now sees pressure from WMT starting to impact the back half of 2025; while Amazon’s push to speed up delivery times in rural areas, coupled with its low pricing for everyday essentials also appears be gaining momentum. At the same time, Dollar Tree is making inroads into DG’s core markets. Finally, regulatory risks from SNAP eligibility changes and the MAHA movement targeting sugary foods are expected to negatively impact sales.

Edition: 217

- 08 August, 2025

Data centre market outlook

Real Estate

Kolytics’ report, the first in a series on the data centre sector, examines how the landscape is evolving amid surging AI-driven demand, mounting infrastructure pressures and a shift in focus from compute capacity to power availability. As the AI revolution transitions from hype to application, investor attention is shifting from core performance to grid access as the primary constraint. While current market conditions remain favourable and landlords benefit from pricing power amid grid bottlenecks, elevated valuations leave limited room for execution missteps. Risk-adjusted opportunities remain attractive; however, the materialisation of substantial downside risks could swiftly reshape the outlook. REITs covered include Digital Realty, Equinix and Iron Mountain.

Edition: 217

- 08 August, 2025

Consumer Discretionary

John Zolidis reiterates his bearish view on CAKE, warning that the multi-year tailwind from aggressive menu price hikes is ending. From 2023-2025, the company raised prices by over 20%, boosting restaurant-level margins to an 8-year high despite a ~5% decline in traffic. However, pricing is set to decelerate to 3.5% in 2H25 (vs. 4.0% in H1) and that slowdown doesn’t account for the rollout of new, lower-priced menu items. Meanwhile, non-core concepts continue to dilute margins. After reviewing Q2 results, which featured a 1.2% comp and 7% EPS growth (the slowest in 3 years), John sees little justification for the stock’s 30% rally over the past 3 months.

Edition: 217

- 08 August, 2025

Materials

WCC has issued a positive profit alert, forecasting 1H25 net profit to rise 80-100% Y/Y. Lucror reiterates a Buy on the WESCHI 4.95% 2026s at 90.5 / 16% YTW / 0.9Y, noting the attractive yield for a short holding period. The bonds have rallied ~10 points since mid-Jun, supported by Xinjiang asset sales, which enable WCC to repay over one-third of the USD 600m notes. A tender offer and new issuance could follow. Further non-core disposals in Guizhou and growth in African operations may improve refinancing flexibility and recovery value. Despite expected negative FCF in H1 due to capex and acquisitions, fundamentals are improving.

Edition: 216

- 25 July, 2025

Colombia: A shock to the downside

The Pacifico Research team interpret June’s inflation reading with caution. The monthly variation was at the lower end of Bloomberg’s survey forecasts for the second consecutive month. However, the most significant monthly declines were concentrated in volatile components such as perishable food and energy. As a result, the normalization of core inflation is proceeding more slowly than that of headline CPI. While the slowdown in monthly inflation aligns with seasonal patterns, this was the lowest June figure since 2021. Of the volatile downward contributions, the most significant was electricity, but this should see a less pronounced decrease in July. Food was also a contributor, as expected, but rent saw a downside surprise. Looking ahead, this result introduces a downward bias for July inflation due to the high weight of effective and imputed rent, which together account for 25% of the CPI basket, while also increasing the degree of uncertainty.

Edition: 215

- 11 July, 2025

Consumer Discretionary

Once a top post-Covid long idea, EXPE has ceded leadership to peers and the broader travel industry. Hedgeye believes the bull thesis - centred on margin expansion, mix shift and market share stability - has grown stale and is now reversing. Investors are 1) underestimating the magnitude of near term deceleration in the core B2C platform, 2) underestimating EXPE’s exposure to regional demand issues and incremental competition, 3) overestimating EXPE’s ability to leverage marketing and drive higher margins, and 4) significantly overestimating EXPE’s ability to maintain (or even grow) share of the total accommodation market in the coming years. While the stock screens as cheap, the risk/reward still skews negative, especially compared to Booking, their preferred long in Online Travel. Hedgeye's EXPE target price offers ~30% downside.

Edition: 215

- 11 July, 2025

Argentina: Three scenarios for FX and inflation

Inflation in May was below expectations again and core price inflation decelerated. Inflation was 1.5% MoM. Inflation in June will be in the vicinity of 2% MoM, according to Marcos Buscaglia’s estimates. As a result, national inflation may drop below 40% YoY for the first time since March 2021. The government is prioritising the reduction of inflation over other objectives such as the purchase of reserves. With this in mind, Marcos lays out three scenarios for the FX and inflation until yearend. In the baseline scenario (50% probability), the peso weakens but remains inside the target band, in the risk scenario (20% with upside risks) it jumps to the top of the band, and in the government-preferred one (30% with downside risks) it weakens very mildly. In the baseline scenario, inflation remains contained at or below 2.5% MoM, but it stops declining, ending 2025 near 32%.

Edition: 214

- 27 June, 2025

What’s trending in Retail

Consumer Discretionary

Each week, The Retail Tracker offers an insightful perspective on retail, fashion and consumer trends and what it means for the stocks. So far this year, Garage is a standout, nailing the “sexy x comfy” aesthetic for teens and taking share from Aerie and Pink. Gap and Old Navy are “crushing it” with consistently strong assortments, offsetting tariff challenges through fewer markdowns. Meanwhile, Urban Outfitters and Nuuly are gaining traction, with Nuuly emerging as a promising rental and tech-driven play. Aritzia is showing good momentum with its best assortment in some time. Department stores may be in free fall, but the best Macy’s stores have never looked better. In contrast, Lululemon is losing its way, expanding beyond its core and diluting its brand identity, while Bath & Body Works' range of new items is exhausting.

Edition: 214

- 27 June, 2025

Consumer Discretionary

Gordon Haskett Research Advisors

Chuck Grom maintains a Buy rating on FIVE following a strong 1Q25, with 7.1% SSS growth and $0.86 EPS, both ahead of guidance. The company's swift turnaround, driven by leadership changes and a return to core strengths in merchandising, marketing, value and customer experience, has exceeded expectations. Traffic growth (6.2%) and broad-based sales gains support Q2 SSS guidance of 7-9%, which Chuck sees as potentially conservative by ~300bps. He believes FY25 EPS could plausibly exceed $5.50. FIVE stands out as one of the few names he covers that can strongly argue the case for both EPS upside and a higher multiple.

Edition: 213

- 13 June, 2025

Japan: Inflationary habits

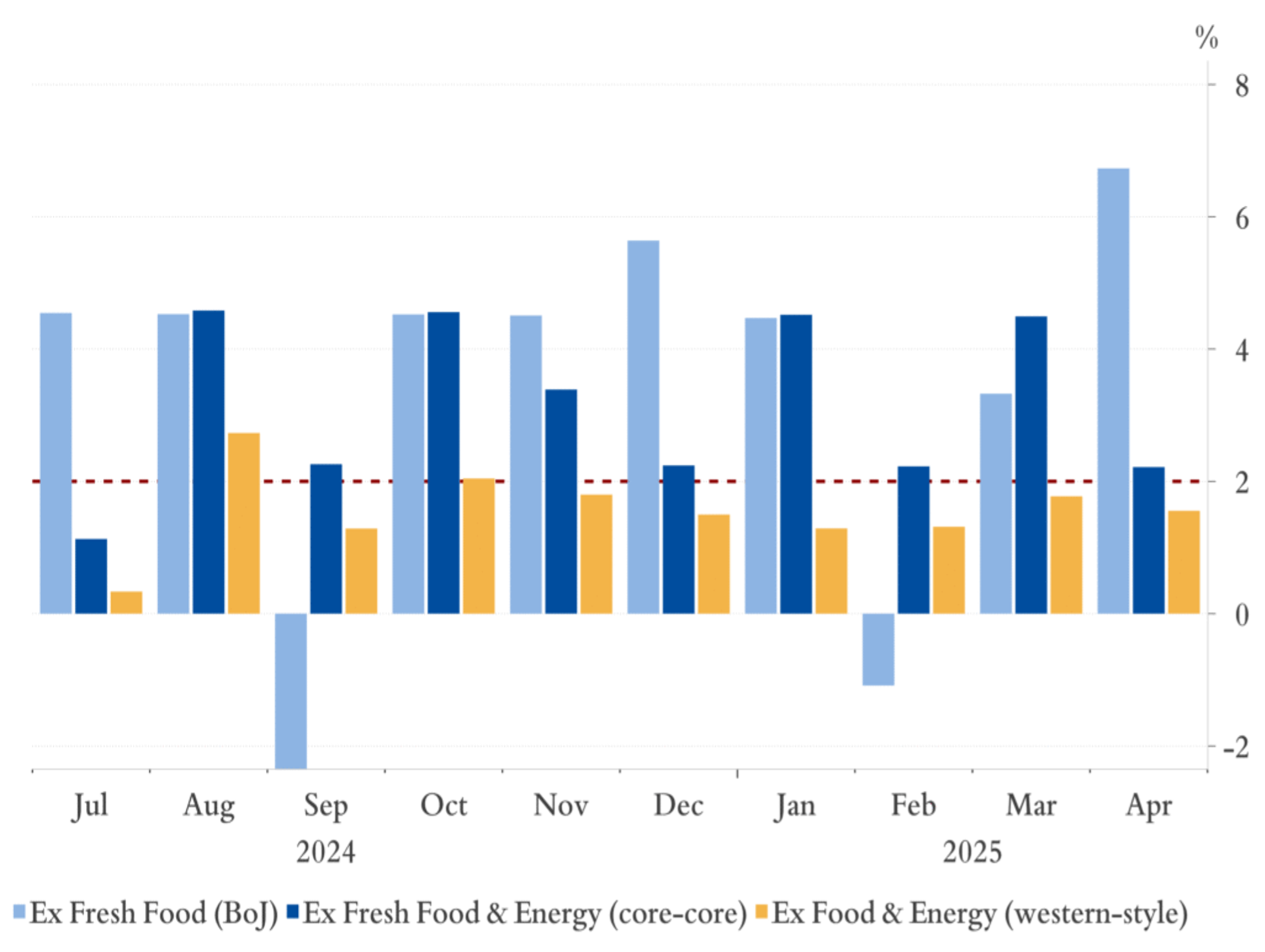

Riccardo Trezzi’s models suggest that Japan is experiencing a persistent inflationary trend, around the BoJ’s 2% target. Riccardo estimates that in April, the BoJ’s core index (excluding fresh food) rose 6.7% MoM SAAR (see chart). As for the other two core inflation measures, the index excluding fresh food and energy (core-core) increased 2.2% MoM SAAR, while the index excluding both food and energy (US-style core) rose 1.6% MoM SAAR. Given potential seasonal adjustment distortions, Riccardo continues to emphasize looking at NSA levels, which suggest that price pressures remain persistent and even higher than last year. His models remain well above the BoJ’s forecasts for core-core in FY2025 and FY2026, with the central bank’s current forecast implying an unrealistic average MoM of less than 10bps sa for core-core this year.

Edition: 212

- 30 May, 2025

Feeling Chile

Chile is entering electoral mode, with candidates competing for support, but over half of voters remain undecided. While voters may punish the outgoing leftwing administration, the moment is ripe for an anti-elite candidate with a law-and-order, pro-growth message. Marcos Buscaglia has revised his 2025 GDP growth forecast to 2.1% from 1.9%, despite expecting a slowdown in the second half. Inflation surprised to the downside at 0.2% month-on-month (vs. 0.3% expected), but core prices rose, and the fiscal anchor remains under pressure, suggesting inflation is likely to exceed consensus. Although some expect rate cuts, Marcos believes the central bank should maintain or raise rates to restore its lost inflation anchor, as his Taylor Rule model does not support cuts. However, with the central bank considering a 25bp cut at its last meeting, a reduction remains plausible.

Edition: 211

- 16 May, 2025

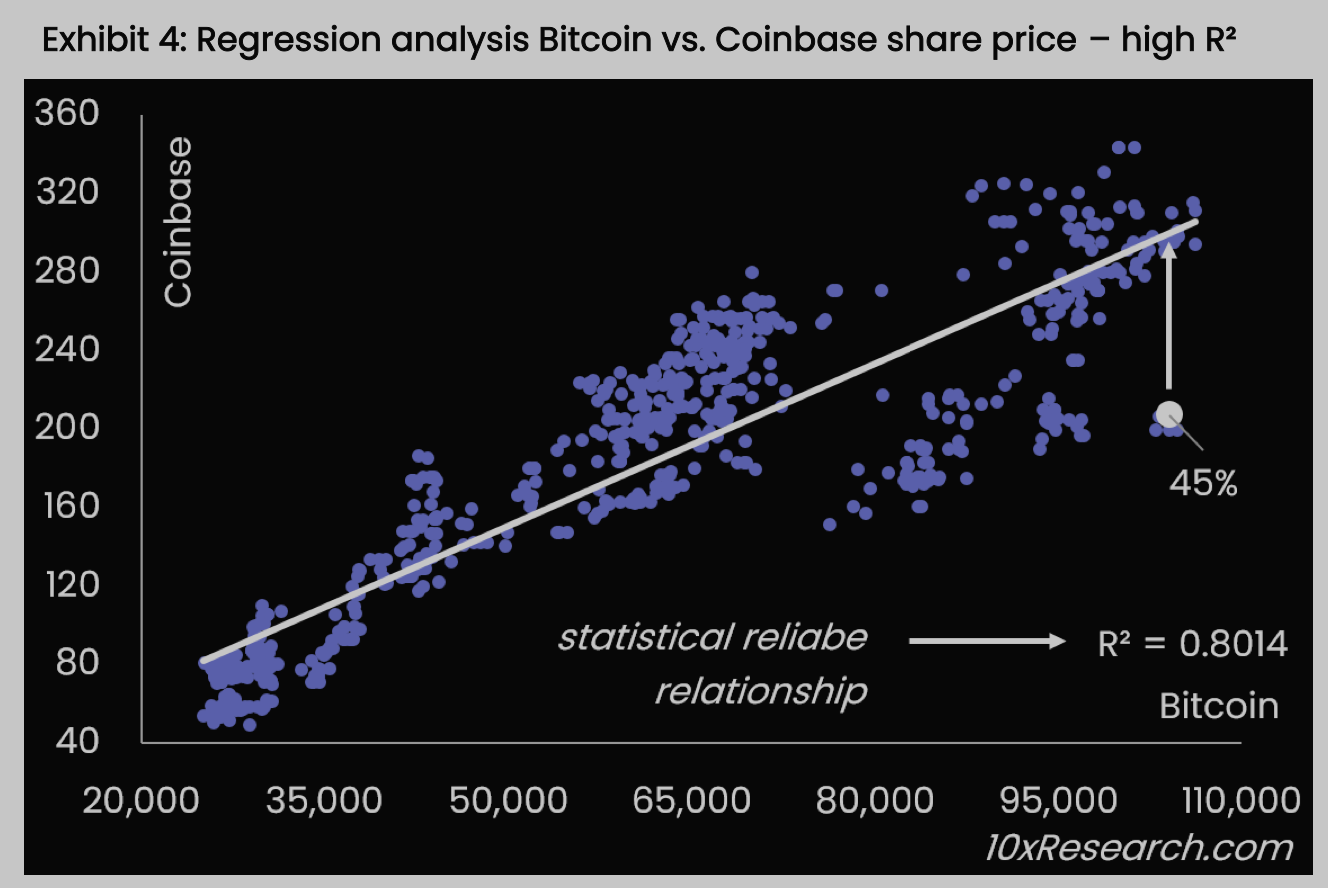

Crypto: Soaring higher

Bitcoin's explosive +160% rally since January 2024 has exposed the fragile economics of Bitcoin miners, with most struggling to keep pace. 10x Research reveals that only a few miners, such as Core Scientific, which achieved +187% gains, have outperformed Bitcoin, while others face rising costs and declining profitability. In contrast, Coinbase offers a more compelling opportunity, with a clear correlation between its stock price and Bitcoin, making it a better play in the current market; their regression with Bitcoin analysis reveals a potential upside of +45%. The team also recommend a spread trade: long Bitdeer vs short Marathon Digital. As Wall Street eyes crypto IPOs worth $100 billion, the stakes have never been higher for the crypto industry.

Edition: 211

- 16 May, 2025

Shell: To Be(P) or not to Be(P); that’s the question

Energy

Analysts at the IDEA! weigh in on media speculation about a potential Shell acquisition of BP. While Shell has the financial strength to pursue a deal, acquiring BP would involve taking on its $77bn of debt and other long-term liabilities, including those from the Deepwater Horizon spill. Although synergies are possible, integration would be costly and could disrupt Shell’s shareholder returns, which is key to closing its valuation gap with US peers. The deal would also bring in non-core assets and regions Shell has been moving away from, along with notable cultural differences. the IDEA! suggests caution and favours Shell sticking to its current strategy or exploring other deals instead.

Edition: 211

- 16 May, 2025