Fortnightly Publication Highlighting Latest Insights From IRF Providers

Company Research

What if copper reaches $7/lb?

With the metal starting 2026 with strong price momentum, David Radclyffe’s team examines the “what if” upside for the nine senior copper pure plays. In the year ahead, David estimates a 410kt copper deficit, as Grasberg and other issues feed through, and that is before production guidance downgrades are announced for some. The copper market is tight. Best leverage to higher copper prices is with First Quantum Minerals Ltd and Teck Resources Ltd, showing high EPS upside near term and with long-term upside to NPV assuming copper stays at US$7/lb indefinitely. Least upside is with Grupo México S.A.B. de C.V. and Ivanhoe Mines Ltd, albeit still good. GMR’s quality vs value screen highlights Grupo México S.A.B. de C.V. and Freeport-McMoRan Inc. as offering better value, although not with the best leverage. The chief risk is the obvious one, that copper is near-term overbought with long-term prices expected lower.

Edition: 227

- 09 January, 2026

Copper: Risk to the downside

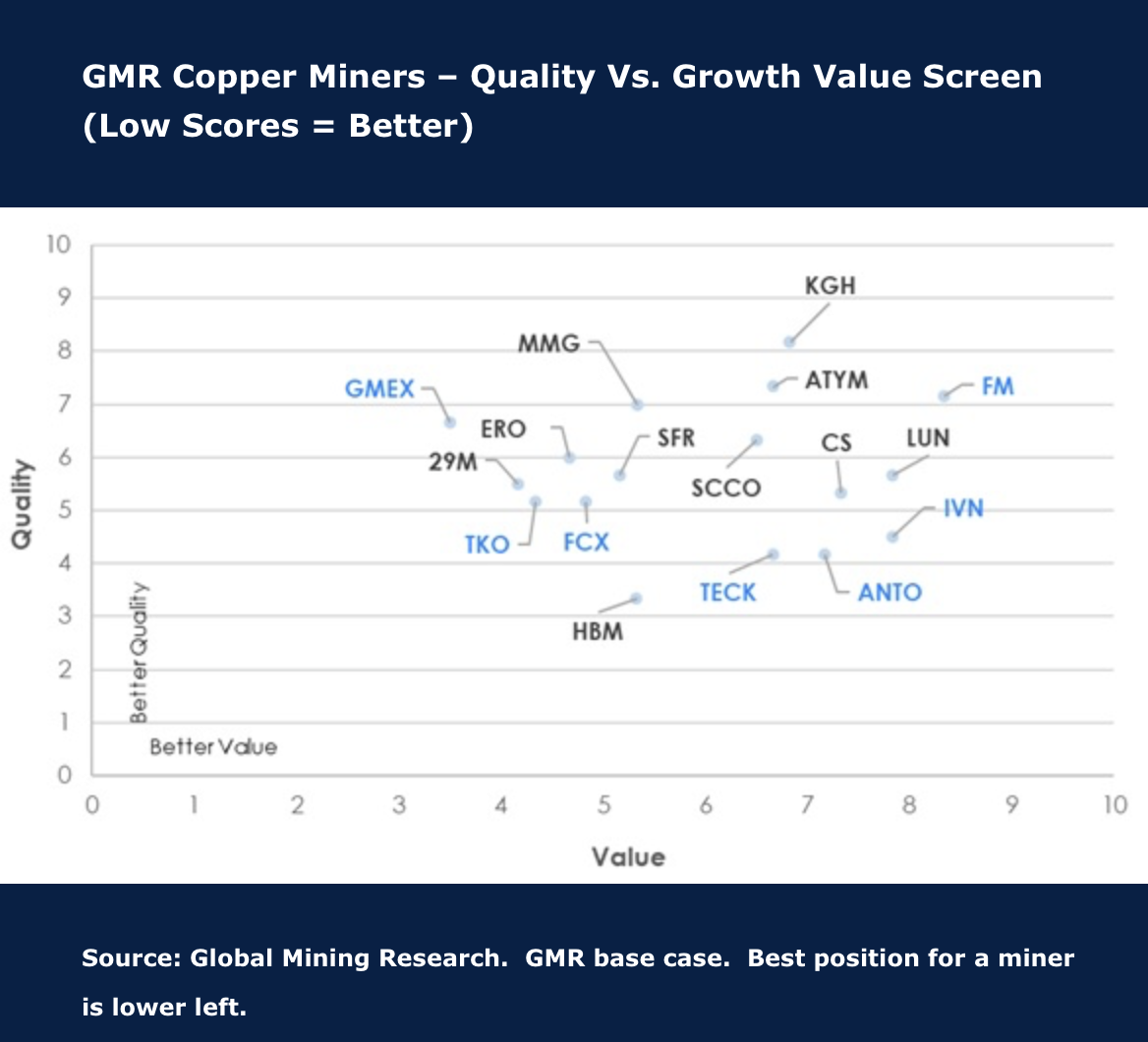

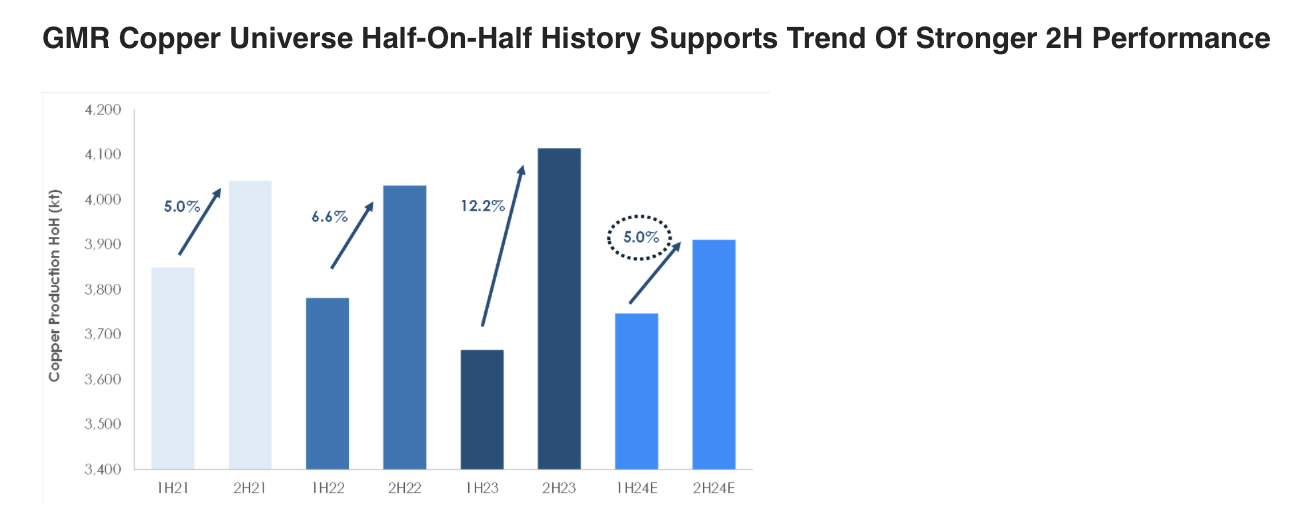

Copper prices had a strong start to the year. David Radclyffe’s review of the Q1/2024 performance versus 2024 guidance for the December year-end stocks helps put the market tightness into perspective. The key takeaway is that, as with gold companies, copper miners are banking on a strong H2/2024 to meet annual guidance figures. The risk is therefore to the downside, with once again copper producers struggling to either meet guidance or increase production appreciably. Only Hudbay Minerals, KGHM, Southern Copper, Freeport-McMoRan and First Quantum Minerals are tracking to 2024 production expectations. David’s preferred copper miners are in the small/mid-cap space on valuation grounds, including Atalaya Mining, Capstone Copper, Sandfire and Hudbay Minerals.

Edition: 187

- 31 May, 2024

Copper: Risk vs Reward

The post-Covid economic hangover has arrived. For copper this means equities have corrected, yet the metal is close to $4/lb. Markets have repriced risk, especially in small caps, but this is a short-term view. There is a case for investing while there is blood on the street, explains David Radclyffe, as he advises investors to position for a traditionally strong Q4. His preferred exposure is through more attractive and better value larger caps such as First Quantum Minerals and Lundin Mining Corp. He also upgrades 29Metals to a BUY given its better overall metrics to peers.

Edition: 138

- 24 June, 2022