Fortnightly Publication Highlighting Latest Insights From IRF Providers

Company Research

Retail predictions for the year ahead

Consumer

Gordon Haskett Research Advisors

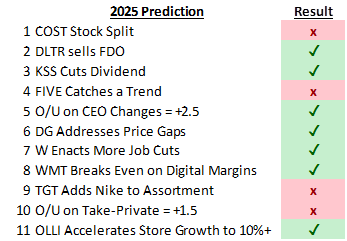

Looking back at GHRA’s 2025 Top 10 (+1) predictions, their batting average was good, hitting on 7 of 11 (see above). For the year ahead, their forecasts include: 1) Target announces an investment cycle on Mar 3rd with adjusted FY26 EBIT margin in the ~3.0%-4.0% range and a 2030 view of ~5.0%-6.0%. 2) Five Below launches Digital Loyalty Card. 3) Academy Sports adds another big brand…likely HOKA. 4) Costco unveils a special dividend and/or ramps share buybacks. 5) Ollie's embarks on large scale sales productivity effort. 6) Burlington takes a page (or two) out of the Ross Stores marketing playbook. 7) Someone gets acquired; BJ’s and Arhaus the most likely candidates. 8) Home improvement recovery gets pushed out…again.

Edition: 227

- 09 January, 2026

Retail Cross Currents: 4 key themes & top stock ideas

Consumer

Gordon Haskett Research Advisors

GHRA highlights an unusually volatile retail backdrop through late 2025 and early 2026, noting multiple “cross currents” affecting both consumers and retailers. Recent rating changes include downgrades for Dollar Tree (Reduce) and BJ's Wholesale Club (Hold), while upgrades cover Williams-Sonoma (Buy), Wayfair (Accumulate), Kohl's (Accumulate) and Dick's Sporting Goods (Hold). GHRA’s key investment themes emphasise: 1) stocks offering both EPS upside and multiple expansion (Five Below, Ross Stores, Burlington); 2) underappreciated turnaround stories (Kohl's, Dollar General); 3) selective “rate-trade” exposure favouring home furnishings over home improvement (Williams-Sonoma, Wayfair, Tractor Supply); and 4) secular winners / “Coffee Can” stocks (Walmart, Costco, TJX, Ollie's Bargain Outlet, Casey's).

Edition: 221

- 03 October, 2025

Consumer Discretionary

Gordon Haskett Research Advisors

Chuck Grom maintains a Buy rating on FIVE following a strong 1Q25, with 7.1% SSS growth and $0.86 EPS, both ahead of guidance. The company's swift turnaround, driven by leadership changes and a return to core strengths in merchandising, marketing, value and customer experience, has exceeded expectations. Traffic growth (6.2%) and broad-based sales gains support Q2 SSS guidance of 7-9%, which Chuck sees as potentially conservative by ~300bps. He believes FY25 EPS could plausibly exceed $5.50. FIVE stands out as one of the few names he covers that can strongly argue the case for both EPS upside and a higher multiple.

Edition: 213

- 13 June, 2025

Consumer Discretionary

Gordon Haskett Research Advisors

Chuck Grom expects to see FIVE return to its roots with a heighted focus on offering trend-right products at a compelling value in a fun store experience that the company has deviated from post-Covid. The Five Beyond strategy may get completely shut down. Meanwhile, GHRA’s proprietary data checks show trends seem to have bottomed and are even showing signs of some modest improvement. While the shortened holiday season, uncertainty around tariffs and overall consumer malaise remain high-level concerns, Chuck believes the risk / reward is favourable and upgrades the stock to Buy, setting a TP of $120, which implies ~40% upside from current levels.

Edition: 199

- 15 November, 2024

Consumer Discretionary

John Zolidis does not believe that FIVE’s current troubles are caused by deeper structural issues in the market and is confident the company will regain its merchandise discipline. He also applauds management’s decision to slow unit growth, which should lead to better ROICs, increased FCF and enable improvements in execution. Increased labour hours in the store will create pressure on the SG&A ratio, but it is the right thing to do. While the multiple for the stock may not reflate to the historical average of ~18x EV/EBITDA, it currently trades at just 8x. John expects the market to assign a much higher multiple as performance improves and sees 80%+ over the next 12 months.

Edition: 194

- 06 September, 2024

Consumer Staples

Hawkshaw published a bullish report on Five Below (FIVE) in advance of their 1Q conference call. While they correctly anticipated a miss and guide down, the magnitude was worse than expected, and the stock is down an additional ~15% (and 45% from the start of the year). Comps this year are now expected to be down 3-5%, as the lower income consumer is pulling back on discretionary spending. Full year expectations have been meaningfully de-risked and the stock is trading near its all-time low PE (22x). On Hawkshaw’s revised numbers, which assume margins recover as the macro pressure alleviates, they see 50-100%+ upside over 12-18 months.

Edition: 188

- 14 June, 2024

Consumer Staples

Gordon Haskett Research Advisors

Once again, the team from Philly steps up and delivers a knock-out punch to the bear thesis - FIVE's 3Q print / 4Q guide should pave the way for the stock to regain its recent momentum. As the group's brand awareness continues to augment, so too should the number of transactions and therefore sales. Moreover, when you layer in: a) $5 Beyond (only in 30% of the chain today); b) flexible pricing throughout the model; c) the continued evolution of ACO (Self-Checkout); and d) eventually a loyalty / personalisation mechanism…this AUV improvement should only continue to gain momentum.

Edition: 125

- 10 December, 2021