Fortnightly Publication Highlighting Latest Insights From IRF Providers

Company Research

Cautious optimism in discretionary retail with Home Improvement a winner

Consumer Discretionary

Scott Mushkin turns incrementally more constructive on the 2026 outlook for discretionary retail, arguing that a gradual moderation in inflation for “have-to-have” items, lower interest rates and steady wage growth could create a better backdrop than a year ago. He sees middle-income households as the key beneficiaries and highlights home improvement as a relative winner, helped by potential catch-up demand after years of underspending on household durables. Against this backdrop, he upgrades both Lowe’s and Home Depot to Hold from Sell, almost 3 years after he downgraded them. Scott also believes the difficulties facing the in-home consumables industry could get worse in 2026 and would avoid most, if not all, the equities, especially companies such as Kroger and Target that compete directly with Amazon and Walmart, who will continue to use aggressive pricing to drive market share.

Edition: 229

- 06 February, 2026

Consumer Discretionary

Brian McGough reiterates his bearish view on FND despite the stock’s ~50% drop since his Apr 24 short call (vs. the S&P +33%). Brian is updating his analysis using his M.A.P.S. (Market Area Performance Study) framework, which tracks store performance by opening cohort. His latest findings suggest that stores opened in 2024 & 2025 are performing even worse than earlier cohorts, reinforcing that FND’s weak comps are structural, not cyclical. New units also show rising market overlap with the likes of Home Depot and Lowe's. While FND is often seen as a housing-recovery play, Brian expects another ~30% downside as earnings, growth guidance and unit expansion continue to disappoint.

Edition: 222

- 17 October, 2025

Something to Snack On: Amazon (AMZN) Drills Lowe's (LOW)

Consumer Discretionary

Amazon ran steep tool discounts over the holiday, highlighting Lowe’s pricing disadvantage. Across 25 items from brands like Bosch and Dewalt, Lowe’s averaged 27.5% higher prices; 15 items were cheaper on Amazon with average discounts of 34.6%, while only one was cheaper at Lowe’s. This follows R5's year-long observation that Lowe’s prices exceed Walmart’s on common goods. The wide gap raises concerns about Lowe’s gross margins and potential sales/earnings headwinds, even if housing improves. Meanwhile, Amazon’s aggressive pricing supports volume growth and advertising profits—a positive for AMZN but a structural challenge for broader retail.

Edition: 219

- 05 September, 2025

What’s the right beta for your portfolio?

Trivariate analysed the top 500 US equities for five factors beyond the market: size (top 100 vs. 401-500), growth vs. value, high-quality vs. junk, liquidity and momentum. They focused on 3 different portfolios (min-vol, max-Sharpe, max-return) to show a range of outcomes. Over the last 20 years, the “efficient frontier” or optimal beta for a median portfolio appears to be between 0.95 and 1. If you are looking to lower your portfolio beta efficiently, owning high-quality value stocks with relatively low liquidity is a prudent strategy (e.g. Exxon Mobil, Philip Morris, Lowe’s, Medtronic). If you want to take more risk, the optimal factor loadings would be to add to highly liquid growth stocks that are junk quality (e.g. Tesla, Applovin, Micron).

Edition: 204

- 07 February, 2025

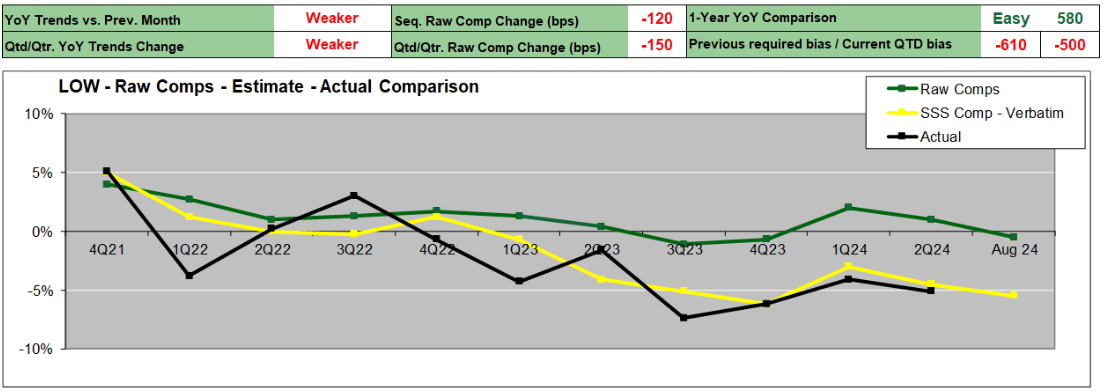

Consumer Discretionary

Aug sales trends are weaker than both Jul and 2Q24 trends, according to Verbatim’s latest channel checks. Customers are exercising caution due to economic uncertainty driven by a weak economy and the upcoming elections. To counter this, LOW’s is offering promotional deals and enhancing customer service. Last month’s bestselling products were Halloween related, as well as patio furniture and appliances. Verbatim’s Aug Comp Estimate is -5.5% vs. 2Q24 Actual Comp of -5.1%. Click here to access the full report.

Edition: 194

- 06 September, 2024

Home Improvement survey reveals disappointing results

Consumer Discretionary

Gordon Haskett Research Advisors

GHRA sees a notable drop in both households planning to undertake a home improvement project and the size / scope of that remodel. 1Q24 survey specifics include: 1) Home improvement plans in the next twelve months moderated ~300 bps sequentially to 53.7% but dropped meaningfully Y/Y from 62.3% in 1Q23. 2) 57.3% of respondents have delayed buying a home (up from 56.0% in 4Q23 and above the long-term average of 51.1%), with 56.7% of them instead planning to reinvest / upgrade their current home (down from 64.3% in 4Q23). 3) The amount consumers are budgeting for home improvement projects moderated sequentially to a 15-quarter low of $5,851, or -24% Y/Y. 4) Home Depot maintained its market share leadership, but the gap to Lowe's narrowed to the slimmest margin yet in GHRA’s survey.

Edition: 184

- 19 April, 2024

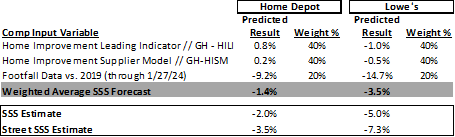

Home Depot (HD) & Lowe’s (LOW)

Consumer Discretionary

Gordon Haskett Research Advisors

GHRA’s 3-factor predictive model points to upside potential to their 4Q23 SSS estimates for HD and LOW. Based on the weighted average results from their 1) Home Improvement Leading Indicator; 2) Home Improvement Supplier Model; and 3) Footfall traffic data, GHRA believes there could be upside to their estimate for HD of -2.0% (vs. predictive model of -1.4%) and LOW of -5.0% (vs. -3.5%). GHRA is bullish on both stocks, but leans more favourably towards HD given its significantly higher PRO penetration (as DIY faces steeper headwinds while PRO backlogs remain healthy); accelerating store growth; and incremental $500m of cost savings in FY24 that help mitigate EPS downside.

Edition: 179

- 09 February, 2024

Costco (COST US) US

Consumer Staples

Gordon Haskett Research Advisors

Building off a strong February Week 4 when COST began to cycle significantly stronger comps from a year ago, the company saw an acceleration in trends during the month of March - posting a hugely impressive 11.1% core comp. According to GHRA, it is becoming increasingly clear that COST will “stomp the comp” in the coming months. Other companies well positioned to do the same include Dollar General, Target and Lowe's.

Edition: 108

- 16 April, 2021