Fortnightly Publication Highlighting Latest Insights From IRF Providers

Company Research

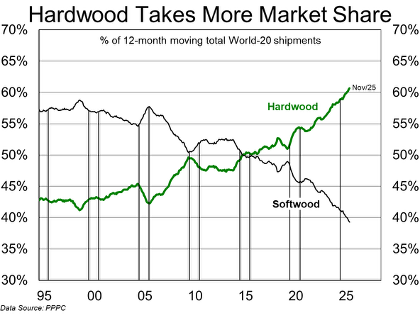

Hardwood gains more market share

The hardwood share of global pulp shipments reached an all-time high in 2025. As global hardwood pulp capacity has grown at a faster rate than softwood and given production costs are ~$300/mt lower, the potential rate of substitution of hardwood into established softwood markets has been a key variable in determining the demand growth rate of each grade. Hardwood pulp producers will clearly benefit, although they have challenges, including exposure to China’s rapid build-out of integrated domestic pulp capacity and the burden of recent huge greenfield mill capex. There’s also the threat that upcoming BHK capacity additions will simply step into expanded hardwood market opportunities. The ERA team see upside in Suzano SA but highlight that R$ swings may require nimble repositioning. They remain cautious on NBSK near pure-play Mercer International Inc given a very stretched balance sheet and little room to manoeuvre. Without more shuts, NBSK prices have little near-term upside.

Edition: 228

- 23 January, 2026

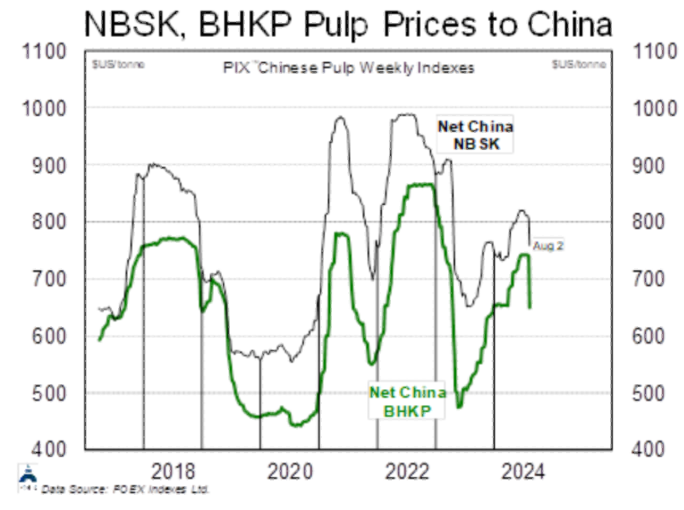

Pulp sellers blink in China

Pulp prices in China have been rangebound since early June, with Chinese buyers and sellers locked in a standoff. Given the huge week over week PIX China pulp price changes (chart), the producers have blinked first. PIX prices dropped $48 and BHK fell by an astounding $91, a correction of a magnitude that would usually take weeks to occur. Expect other international markets to see accelerated price drops as a result. The biggest market-pulp consumers are tissue producers and in ERA’s stock coverage Cascades is expected to benefit the most. Pulp producers are the losers, including Mercer International and International Paper. Expect pulp names to remain under pressure for at least a quarter, or until closures accelerate.

Edition: 192

- 09 August, 2024